Executive summary:

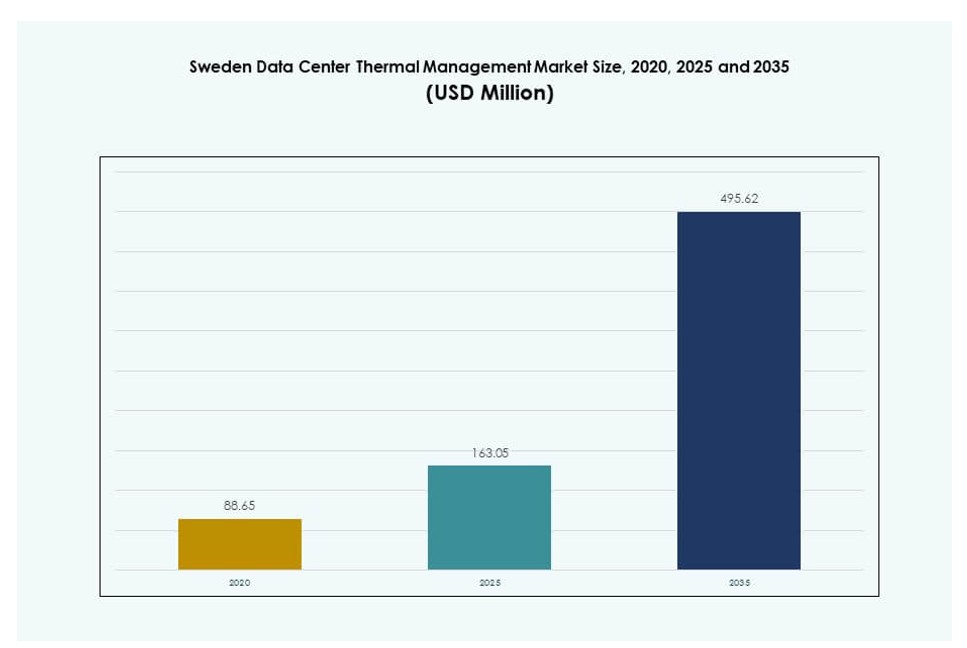

The Sweden Data Center Thermal Management Market size was valued at USD 88.65 million in 2020, increased to USD 163.05 million in 2025, and is anticipated to reach USD 495.62 million by 2035, at a CAGR of 11.70% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Sweden Data Center Thermal Management Market Size 2025 |

USD 163.05 Million |

| Sweden Data Center Thermal Netherlands Market, CAGR |

11.70% |

| Sweden Data Center Thermal Management Market Size 2035 |

USD 495.62 Million |

The market is driven by the adoption of high-density computing, AI workloads, and energy-efficient cooling technologies. Operators are shifting toward liquid cooling, smart airflow management, and thermal automation to manage increasing rack power densities. Innovation in heat reuse and district heating integration further enhances operational sustainability. Businesses prioritize modular and scalable cooling to ensure cost-effective expansion. The market holds strategic importance for investors aiming at ESG-aligned infrastructure with reduced carbon intensity and improved thermal reliability.

Geographically, Stockholm leads the market due to its dense concentration of hyperscale and colocation facilities. Northern regions like Luleå are emerging rapidly with cold climate advantages and abundant renewable energy sources. Southern cities such as Malmö and Gothenburg are seeing moderate growth, fueled by edge deployments and enterprise demand. Regional diversity supports Sweden’s role as a key Nordic data hub.

Market Dynamics:

Market Drivers:

Strong Integration of Renewable Energy and District Heating Enhances Sustainability and Efficiency

Sweden’s abundant renewable energy resources and advanced district heating systems create a strong foundation for efficient thermal management in data centers. Operators leverage waste heat recovery from servers to supply nearby residential or industrial heating. The Sweden Data Center Thermal Management Market benefits from these integrations, which align with national climate goals. Companies such as EcoDataCenter already utilize 100% renewable power and send excess heat into the local grid. This reduces both energy costs and environmental impact. Investors favor Sweden for its low-carbon digital infrastructure strategies. Integration of district heating strengthens long-term cost control. Thermal systems using water-based cooling loops remain viable in this framework.

- For instance, Stockholm Data Parks initiative integrates over 20 data centers into the municipal heating network, supplying surplus heat to warm approximately 30,000 apartments.

Widespread Adoption of Liquid Cooling Systems in AI and High-Density Workloads

The shift toward high-density computing, driven by AI and GPU workloads, increases heat loads per rack. Operators in Sweden adopt liquid cooling technologies to manage these intensifying thermal demands. The Sweden Data Center Thermal Management Market sees rising use of direct-to-chip and immersion cooling to support new deployments. Research facilities and AI clusters require targeted, low-latency cooling methods. Enterprises running machine learning workloads report 25–30% better thermal efficiency using liquid-based systems. Local firms collaborate with global vendors to customize solutions. The technology supports better PUE and equipment longevity. This creates interest from hyperscale and colocation operators seeking efficiency.

Government Incentives and Regulatory Support for Green Data Infrastructure Development

The Swedish government offers clear regulatory direction and support for energy-efficient digital infrastructure. Operators receive incentives for sustainable construction, efficient thermal systems, and energy reuse practices. The Sweden Data Center Thermal Management Market aligns with EU climate directives and Sweden’s digital roadmap. Government-backed R&D accelerates adoption of next-gen cooling designs. Local municipalities often co-develop district heat exchange programs with data center firms. Environmental certification frameworks favor smart thermal designs. These policies provide a stable growth environment for global investors. Efficient thermal systems become a prerequisite for operational licenses in some zones. This regulatory clarity attracts more hyperscale investment.

Strategic Role of Sweden in Nordic and EU Data Infrastructure Expansion

Sweden serves as a strategic digital hub in Northern Europe due to connectivity, power reliability, and geography. Global tech firms choose it for latency-sensitive workloads and green data initiatives. The Sweden Data Center Thermal Management Market grows as operators plan scalable thermal systems for Nordic expansion. Stockholm acts as the core interconnection zone, while northern regions attract cold-climate projects. Efficient cooling becomes central to regional competitiveness. Companies operating across Denmark, Norway, and Finland use Swedish sites to balance energy use. Sweden’s reputation for digital resilience supports long-term infrastructure confidence. Efficient thermal management ensures cost-efficient scaling for regional workloads.

- For instance, Conapto’s STHLM 3 NORTH facility in Stockholm leverages advanced cooling for high-density computing in the metro area.

Market Trends:

AI and Machine Learning Workloads Drive Cooling Innovation in High-Performance Clusters

AI and ML workloads accelerate adoption of advanced thermal technologies across Sweden. High-performance clusters require tighter thermal control, especially when running dense GPU configurations. The Sweden Data Center Thermal Management Market witnesses a shift toward rack-level and direct-to-chip cooling systems. Operators use thermal sensors and AI-driven software to balance cooling dynamically. In Stockholm, several hyperscale sites integrate AI workloads, necessitating smarter airflow and fluid routing. Vendors develop customized thermal models for real-time energy and performance balancing. This drives innovation in both hardware and software layers. Demand for AI-ready cooling increases across research institutions and private sectors.

Smart Thermal Management Software Gains Adoption in DCIM and Energy Optimization

Data center infrastructure management (DCIM) tools now include smart thermal modules to improve operational insights. The Sweden Data Center Thermal Management Market adopts AI-based platforms for predictive cooling control. Companies deploy DCIM with real-time temperature mapping, airflow analytics, and energy efficiency dashboards. These tools integrate with BMS and CFD simulations to identify hot spots and optimize equipment deployment. Startups and large vendors introduce hybrid modules combining AI, automation, and machine learning. Smart dashboards reduce cooling costs by up to 15% in mid-size facilities. Operators track thermal performance in real time to support capacity planning. Efficiency gains translate to better uptime and reliability.

Rise of Modular and Scalable Cooling Designs in New Data Center Construction

Developers prefer modular thermal designs to enable rapid deployment and future scalability. The Sweden Data Center Thermal Management Market embraces pre-engineered cooling systems for hyperscale and edge sites. Modular chillers, containerized units, and scalable liquid loops support flexible growth. Operators reduce lead times while ensuring thermal consistency. Prefabricated thermal modules integrate easily with digital twin platforms. Developers use modular approaches to comply with EU efficiency benchmarks. Several Nordic projects use modular cooling to deliver up to 60 MW phased capacity. This trend supports faster time-to-market in competitive colocation zones. Future expansions become smoother and cost-efficient.

Heat Reuse Becomes a Commercially Viable Strategy for Energy Recovery

Data centers in Sweden increasingly view waste heat reuse as a revenue-generating model. The Sweden Data Center Thermal Management Market benefits from partnerships between operators and district heating networks. Local utilities purchase excess heat to serve homes, offices, and public buildings. This enhances ROI on cooling systems while reducing strain on local heating grids. Companies like Stockholm Exergi engage with data centers for sustainable urban heating. Waste heat recovery also helps operators meet ESG targets. Heat reuse solutions now include thermal storage, enabling 24/7 supply. This trend creates new business models for energy management.

Market Challenges:

High Capital Costs and Long ROI Periods for Advanced Liquid Cooling Infrastructure

Deploying advanced cooling systems often involves high initial investment in specialized infrastructure. Liquid cooling requires changes in data center layout, power management, and equipment compatibility. The Sweden Data Center Thermal Management Market faces budget constraints in mid-size or brownfield projects. ROI periods for immersion and direct-to-chip systems can exceed five years without incentive support. Operators also face downtime risks during retrofitting. Vendors must address standardization issues across hardware platforms. Maintenance complexity rises with advanced systems. These factors limit adoption in non-hyperscale environments. Liquid cooling uptake remains slow among legacy operators due to conversion costs.

Skilled Workforce Shortage and Vendor Dependence for System Design and Maintenance

Sweden faces a shortage of trained technicians and engineers who specialize in advanced cooling systems. Operators rely heavily on a limited pool of international vendors for design, integration, and maintenance services. The Sweden Data Center Thermal Management Market sees delays in deployment schedules due to workforce constraints. Custom solutions often need imported expertise, which raises cost and complexity. Local education institutions offer limited programs focused on thermal engineering in digital infrastructure. Vendor lock-in also restricts flexibility during system upgrades. These talent gaps slow innovation cycles. Coordinated training programs remain underdeveloped across Nordic countries.

Market Opportunities:

Government Backing for Sustainable Infrastructure Supports Incentivized Growth Paths

Public and private sector alignment around carbon neutrality creates strong growth pathways. The Sweden Data Center Thermal Management Market benefits from grants and tax offsets for green cooling adoption. Operators that integrate with local heating grids gain added revenue streams. Cities partner with data centers to build circular energy ecosystems. This policy support opens new funding routes. Developers use these programs to build future-proof facilities.

Edge Data Centers and 5G Expansion Create Demand for Compact Thermal Solutions

Edge deployments driven by IoT and 5G need compact and efficient thermal systems. The Sweden Data Center Thermal Management Market supports this shift with localized liquid cooling units and AI-integrated fans. Urban micro data centers and telecom nodes seek modular cooling solutions. This segment creates new opportunities for thermal vendors focused on edge-specific needs.

Market Segmentation:

By Data Center Size

Large data centers dominate the Sweden Data Center Thermal Management Market due to extensive hyperscale and colocation deployments. These facilities account for over 55% of the market share, driven by high-density workloads. Medium-sized data centers follow, benefiting from enterprise upgrades. Small data centers play a niche role in edge and regional deployments. Thermal solutions for large data centers focus on hybrid systems and integration with DCIM platforms.

By Cooling Technology

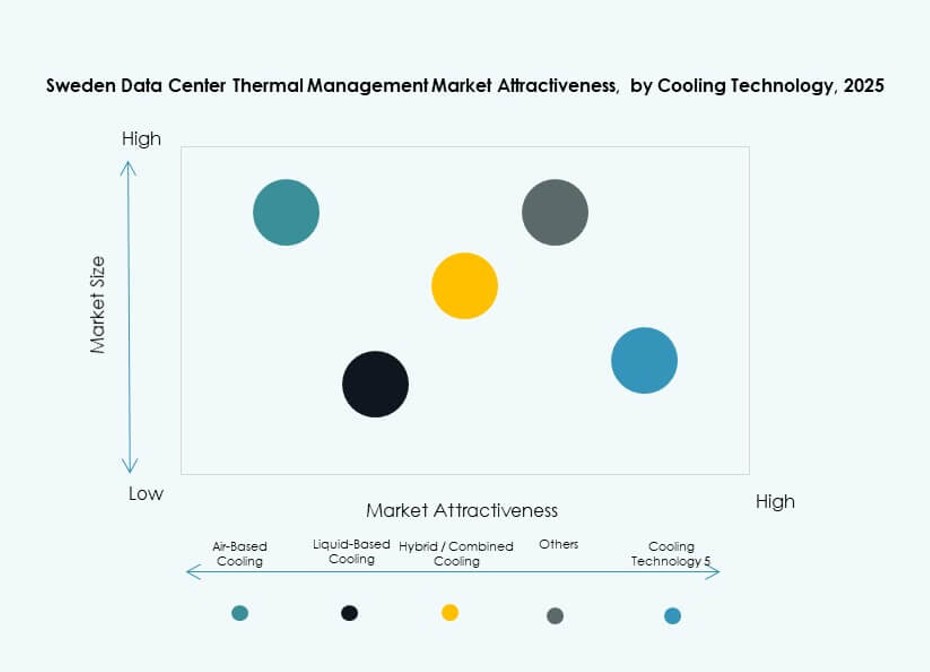

Liquid-based cooling holds the fastest growth rate, with direct-to-chip and immersion cooling leading adoption. Air-based cooling, including hot/cold aisle containment and rear door exchangers, remains common in legacy sites. Hybrid cooling systems gain traction due to their adaptability. Thermoelectric and phase-change cooling find limited applications. The Sweden Data Center Thermal Management Market sees increasing preference for sustainable liquid cooling across AI-ready infrastructure.

By Component

Hardware leads the market, accounting for over 60% share due to the dominance of physical cooling equipment. Software and services grow steadily as operators integrate AI-based optimization and monitoring. Services such as commissioning and predictive maintenance enable long-term value. The market emphasizes bundled offerings that combine all three components for end-to-end management.

By Hardware

Cooling units and chillers form the largest hardware segment, followed by heat exchangers and airflow devices. Fans and piping systems support secondary infrastructure layers. High-performance heat sinks gain interest in immersion and liquid setups. Operators invest in smart fans to enhance efficiency and reduce noise. Liquid distribution components evolve with AI-ready thermal modules.

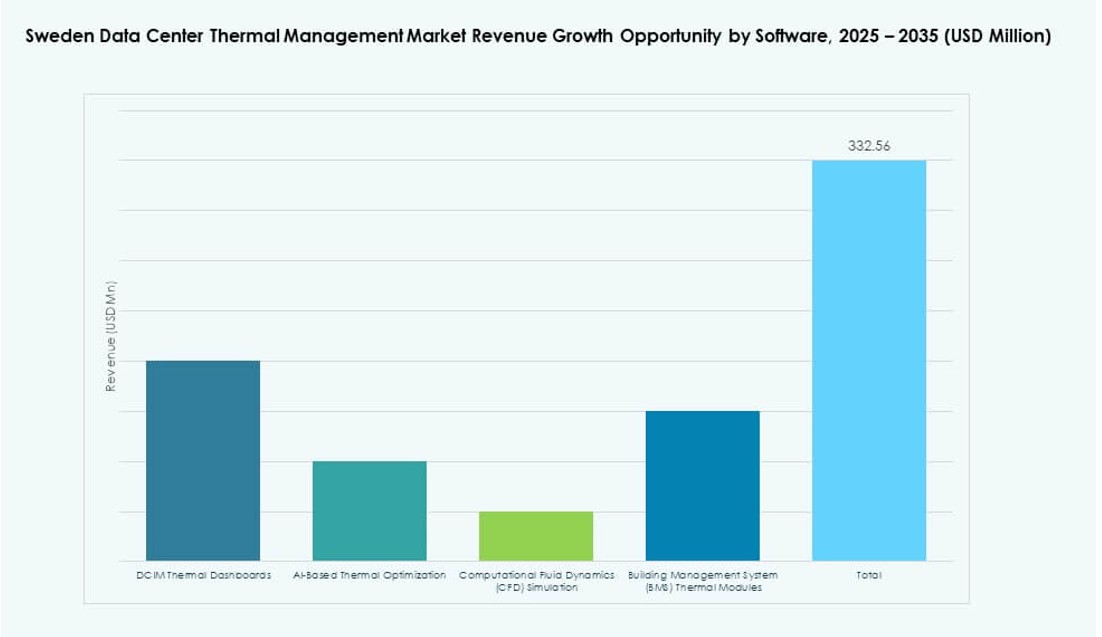

By Software

AI optimization and DCIM dashboards drive the software segment, supporting automated cooling control. CFD simulation tools enable advanced thermal modeling and planning. BMS integration improves multi-site monitoring. These tools help improve uptime and reduce energy costs. The Sweden Data Center Thermal Management Market sees increased deployment of AI-based thermal insights across hyperscale environments.

By Services

Preventive maintenance and retrofits lead the services segment, ensuring uptime and energy compliance. Installation services gain value in modular and prefabricated setups. Monitoring as a service supports ongoing performance tracking. Service models shift from reactive to predictive, improving operational efficiency. Providers bundle software and services for comprehensive thermal management packages.

By Data Center Type

Hyperscale data centers lead with over 50% share, followed by colocation/cloud sites. Enterprise data centers invest in upgrades, focusing on hybrid cooling. Edge and micro facilities create demand for compact and modular solutions. Hyperscale players drive innovation in liquid cooling and thermal reuse. Colocation providers adopt mixed technologies to serve varied tenant needs.

By Structure

Room-based cooling dominates legacy facilities, while rack-based systems gain traction in high-density setups. Row-based cooling sees growth in modular deployments. Rack-level systems support AI workloads and fluid cooling configurations. The Sweden Data Center Thermal Management Market shifts toward more granular cooling structures. Vendors offer integrated solutions tailored to structure-specific needs.

Regional Insights:

Stockholm Leads National Deployment with Over 45% Market Share Due to Connectivity and Hyperscale Growth

Stockholm remains the dominant hub for Sweden’s data center activity. It hosts major colocation campuses, interconnection zones, and hyperscale buildouts. The Sweden Data Center Thermal Management Market sees high deployment of AI-optimized cooling in this region. Proximity to submarine cables and dense enterprise zones enhances its value. Urban density necessitates advanced thermal designs for uptime. Major players focus on retrofits and thermal automation.

- for instance, Axiado’s AI-driven Dynamic Thermal Management solution cuts cooling energy consumption by up to 50% through real-time predictive modeling based on server workloads, as demonstrated in a 100,000-server data center saving over $7 million annually.

Northern Sweden Emerges Due to Cold Climate and Renewable Power Abundance

Luleå and surrounding northern cities emerge as strategic zones for large-scale data infrastructure. These areas contribute nearly 30% of the market. Cold climate supports free cooling, reducing power consumption. Renewable energy sources and government incentives attract green infrastructure investment. Northern regions support long-haul storage and hyperscale AI training workloads. Lower operating costs increase site viability for global firms.

Western and Southern Regions Show Moderate Growth Through Enterprise and Edge Demand

Malmö, Gothenburg, and other southern zones account for the remaining 25% share. These regions see moderate activity focused on edge data centers, enterprise colocation, and telecom nodes. Local governments encourage digital infrastructure through zoning and tax reforms. Enterprise firms deploy smaller facilities with hybrid cooling systems. These zones benefit from cross-border data flow with Denmark and Germany. Regional players invest in scalable cooling to match growing workloads.

- For instance, Hitachi Energy announced a SEK 700 million expansion of its cooling systems factory in Landskrona, Sweden, in December 2025 to meet growing global demand. The facility will support increased production capacity and create new jobs in the region.

Competitive Insights:

- Munters Group AB

- Systemair AB

- SWEP

- Daikin Industries Ltd.

- Delta Electronics, Inc.

- Eaton Corporation

- Airedale International Air Conditioning Ltd.

- Asetek, Inc.

- Vertiv Group Corp.

- Trane Technologies plc

Competition in the Sweden Data Center Thermal Management Market remains dynamic with global and regional players striving for efficiency and sustainability leadership. Firms differentiate through advanced cooling hardware, software-driven thermal control platforms, and service packages that enhance uptime and reduce energy expenditure. Market leaders secure contracts with hyperscale and colocation operators by offering modular and scalable solutions tailored to high-density workloads. Smaller niche vendors gain traction in edge data center segments with compact, cost‑effective systems. Partnerships and localized service networks help companies reduce response times and build long‑term client relationships. Investment in R&D remains a priority to stay ahead in thermal analytics, predictive cooling, and liquid cooling solutions. This competitive ecosystem drives faster adoption of next‑gen thermal technologies across Sweden’s digital infrastructure.

Recent Developments:

- In December 2025, SWEP launched two new brazed plate heat exchangers, B327 and B224, designed for data center cooling with high flow rates, low pressure drop, and efficiency in compact formats for AI and high-performance computing. These products support single-phase applications, coolant distribution units, and heat recovery up to 1000kW, addressing high-density thermal loads.

- In November 2025, Daikin Industries Ltd. acquired Chilldyne, a leader in negative pressure liquid cooling systems for AI data centers, adding direct-to-chip technology to its portfolio.