Executive summary:

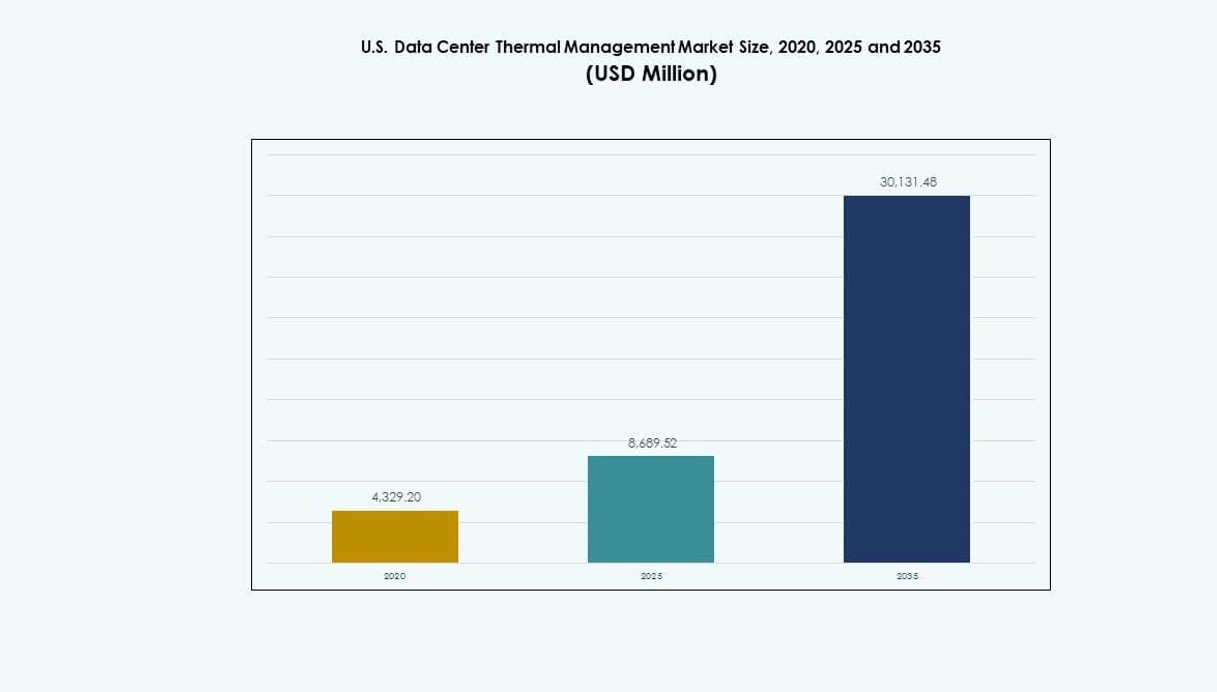

The U.S. Data Center Thermal Management Market size was valued at USD 4,329.20 million in 2020, reached USD 8,689.52 million in 2025, and is anticipated to reach USD 30,131.48 million by 2035, at a CAGR of 13.16% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| U.S. Data Center Thermal Management Market Size 2025 |

USD 8,689.52 Million |

| U.S. Data Center Thermal Management Market, CAGR |

13.16% |

| U.S. Data Center Thermal Management Market Size 2035 |

USD 30,131.48 Million |

Growth in AI workloads, high-density server racks, and hyperscale deployments is reshaping thermal management needs. Businesses are adopting liquid cooling, AI-based monitoring, and modular systems to improve efficiency and reduce energy consumption. Innovation in direct-to-chip and immersion cooling helps meet sustainability goals and operational uptime. The market has become a strategic focus for investors aiming to back infrastructure that supports scalable, resilient, and energy-efficient data centers across the country.

The Western U.S. leads the market due to climate benefits, large-scale hyperscale hubs, and renewable energy access. The Midwest is emerging quickly, driven by low land costs, strong grid infrastructure, and tax incentives. The Southeast shows rising demand as cloud adoption and enterprise data needs grow. Each region’s share is shaped by environmental, regulatory, and economic factors, influencing cooling technology preferences and deployment models.

Market Dynamics:

Market Drivers

Rising AI Workloads and High-Density Rack Deployments Necessitate Efficient Cooling Infrastructure Across Facilities

AI workloads continue to reshape data center design across the United States. High-density racks exceeding 30 kW per cabinet have become common in hyperscale and enterprise environments. Efficient thermal solutions are necessary to manage growing heat loads and ensure optimal performance. Operators now integrate direct-to-chip and immersion cooling to meet performance and sustainability goals. The U.S. Data Center Thermal Management Market gains importance as data intensity increases across digital services. Businesses prioritize thermal reliability to prevent downtime and prolong equipment life. Innovations in cooling directly reduce OPEX for hyperscalers and colocation providers. The market creates a strategic edge for investors focused on long-term operational efficiency. Cooling has shifted from a utility function to a business-critical infrastructure pillar.

Technological Advancements in Liquid and Hybrid Cooling Support Dense IT Architectures in Next-Generation Facilities

Liquid cooling systems are seeing faster adoption due to their efficiency in handling high-density IT loads. Direct-to-chip and immersion solutions now support AI, HPC, and blockchain data centers with precision temperature control. Hybrid cooling blends air and liquid technologies to extend existing infrastructure without full retrofits. These approaches improve PUE and lower water usage in resource-sensitive locations. It helps hyperscalers futureproof new deployments while meeting ESG benchmarks. The U.S. Data Center Thermal Management Market benefits from rising integration of smart controls in thermal infrastructure. AI-enabled sensors optimize fan speeds, coolant flow, and heat exchange cycles based on real-time load. This drives demand for DCIM and AI optimization software. Operators now treat thermal strategy as central to data center lifecycle planning.

- For instance, Meta has outlined a roadmap to shift its data centers toward direct‑to‑chip liquid cooling to support high‑density AI workloads and improve thermal performance. The company is adapting new cooling designs that allow liquid cooling to work with existing infrastructure and enable higher rack power densities than traditional air‑only systems.

Shift Toward Sustainability Goals and Compliance Mandates Promote Adoption of Efficient Thermal Technologies

Environmental regulations and corporate ESG targets push operators to improve cooling performance. Companies now pursue LEED, Energy Star, and other certifications that require strict thermal management benchmarks. Efficient systems contribute to carbon reduction goals through energy savings and reduced refrigerant use. The U.S. Data Center Thermal Management Market aligns with federal and state-level decarbonization strategies. Enterprises shift from legacy air cooling to energy-efficient alternatives to comply with these mandates. Cooling vendors integrate low-GWP refrigerants and closed-loop systems to support sustainability efforts. Water conservation concerns also fuel demand for adiabatic cooling and air-side economizers in arid regions. Thermal innovation becomes a tool to secure investment, improve brand image, and meet stakeholder expectations.

- For instance, Microsoft is piloting closed-loop zero-water cooling designs at its Phoenix data center, aiming to save over 125 million liters of water annually per site through elimination of evaporative cooling.

Increased Strategic Investment from Hyperscale and Cloud Providers Fuels Infrastructure Modernization

Hyperscale expansion drives capital investment in next-generation cooling infrastructure across multiple U.S. states. Major cloud operators prioritize low-latency delivery, high efficiency, and robust cooling at scale. It drives widespread retrofitting of legacy facilities and greenfield construction with advanced thermal systems. The U.S. Data Center Thermal Management Market supports operators aiming to reduce cost per MW while increasing performance per rack. Strategic capital flows into modular cooling systems, integrated controls, and predictive analytics. Data center REITs and infrastructure funds consider thermal maturity a key investment criterion. Efficient cooling improves asset value and lease appeal across colocation markets. Investors view thermal management as essential to uptime, density scalability, and long-term operational ROI.

Market Trends

Integration of AI and Predictive Analytics Enhances Thermal Performance and Reduces Energy Waste in Real Time

AI adoption in thermal systems improves operational precision across high-density environments. Sensors and control modules enable real-time monitoring of heat load and airflow across zones. Predictive algorithms adjust cooling outputs before thermal thresholds are breached. It improves system responsiveness and reduces energy waste during non-peak periods. The U.S. Data Center Thermal Management Market benefits from the shift to software-defined cooling intelligence. Cloud-based DCIM platforms centralize environmental controls for multisite facilities. Predictive maintenance lowers system failures and extends equipment lifespan. Machine learning adapts thermal delivery to changing IT workloads and seasonal patterns.

Adoption of Liquid Cooling in Edge and Micro Data Centers Expands Beyond Hyperscale Applications

Liquid cooling now extends to smaller facilities serving edge workloads and AI inference zones. Edge computing demand rises in healthcare, manufacturing, and telecom sectors. These applications generate localized heat loads requiring compact, high-efficiency cooling. The U.S. Data Center Thermal Management Market reflects broader adoption of immersion and direct-chip cooling in containerized modules. Liquid systems enable quiet, vibration-free operation in urban or space-limited environments. Edge providers benefit from modular liquid systems with fast deployment timelines. This trend supports the decentralization of compute while maintaining thermal resilience. High-performance edge computing depends on localized cooling innovation.

Growth in Retrofits and Thermal Modernization Projects Drives Demand for Scalable and Modular Systems

Aging infrastructure in legacy enterprise and colocation facilities presents modernization opportunities. Many sites were built before AI workloads and now face thermal bottlenecks. Operators deploy modular cooling units to support phased capacity upgrades. It allows performance improvement without full-scale shutdowns or construction. The U.S. Data Center Thermal Management Market sees rising interest in scalable row- and rack-based systems. Retrofitting with variable-speed fans, liquid-ready rear doors, and high-efficiency chillers extends facility lifespan. Upgrades align with evolving thermal standards and provide a pathway to meet sustainability targets. Scalable solutions suit both Tier III/IV data centers and localized edge hubs.

Expansion of Sustainable Cooling Practices Including Air Economization and Waste Heat Reuse

Operators incorporate design elements that maximize free cooling during colder months. Air-side economizers and indirect evaporative systems reduce mechanical load. Some data centers capture and reuse waste heat for district heating or building energy. The U.S. Data Center Thermal Management Market supports thermal strategies that align with circular energy use models. Northern U.S. states enable longer economizer cycles due to favorable climate. Thermal designs that reduce PUE while cutting water usage receive positive regulatory and community support. It reinforces cooling’s role in broader environmental and infrastructure planning.

Market Challenges

High Capital Costs and Technical Complexity Limit Adoption of Advanced Cooling Technologies Across Smaller Operators

Deployment of liquid cooling and hybrid systems often requires high upfront investment. Smaller data centers struggle with retrofitting costs, facility layout limitations, and operational downtime. Equipment like CDU systems, immersion tanks, and advanced monitoring platforms require trained personnel. It adds technical complexity for operators without in-house thermal expertise. The U.S. Data Center Thermal Management Market faces barriers in low- and mid-tier markets where ROI timelines are longer. Lack of standardized cooling interfaces across servers and racks complicates integration. Financing and technical partnerships play a critical role in enabling broader adoption. Operational risk from improper installation also deters rapid rollouts.

Water Availability Constraints and Regulatory Pressure Challenge Cooling System Scalability in Drought-Prone Regions

Cooling technologies that rely heavily on water face scrutiny in western and southern U.S. states. Water-intensive systems raise environmental concerns and risk non-compliance with future regulations. The U.S. Data Center Thermal Management Market must adapt by advancing low-water and closed-loop designs. It creates pressure to shift toward air cooling, dry chillers, and refrigerant-based alternatives. Some operators relocate or delay expansions due to regional water scarcity. Community opposition also emerges around proposed high-usage facilities. Environmental permitting delays impact deployment timelines. Cooling vendors invest in R&D to align with emerging standards and water usage caps.

Market Opportunities

Expansion of AI and Cloud Computing Infrastructure Unlocks Demand for Specialized Cooling Technologies

AI growth requires purpose-built cooling systems that handle high-density processing cores. Hyperscalers lead demand for modular thermal systems with integrated monitoring and automation. The U.S. Data Center Thermal Management Market gains from the rising need to maintain thermal stability in low-latency workloads. Companies seek thermal solutions that improve performance per watt and align with ESG priorities. Edge and cloud facilities offer long-term opportunities for distributed liquid cooling deployments.

Federal and State Incentives for Green Infrastructure Promote Investment in Sustainable Thermal Solutions

U.S. government policies support energy efficiency through grants, tax credits, and green certifications. Cooling upgrades become eligible for incentive-backed modernization programs. The U.S. Data Center Thermal Management Market benefits from these frameworks by enabling capital access for retrofits and new builds. Clean cooling solutions position operators to secure funding, improve community acceptance, and gain competitive advantage in site selection processes.

Market Segmentation

By Data Center Size

Large data centers dominate the U.S. Data Center Thermal Management Market due to high-density workloads and extensive capacity needs. Hyperscale operators drive demand for advanced thermal systems that support over 30 kW per rack. Medium data centers see growth from regional colocation and AI training deployments. Small facilities, often at the edge, adopt compact liquid or hybrid systems to fit spatial and power constraints. Scalability, efficiency, and modularity shape thermal strategies across all size tiers.

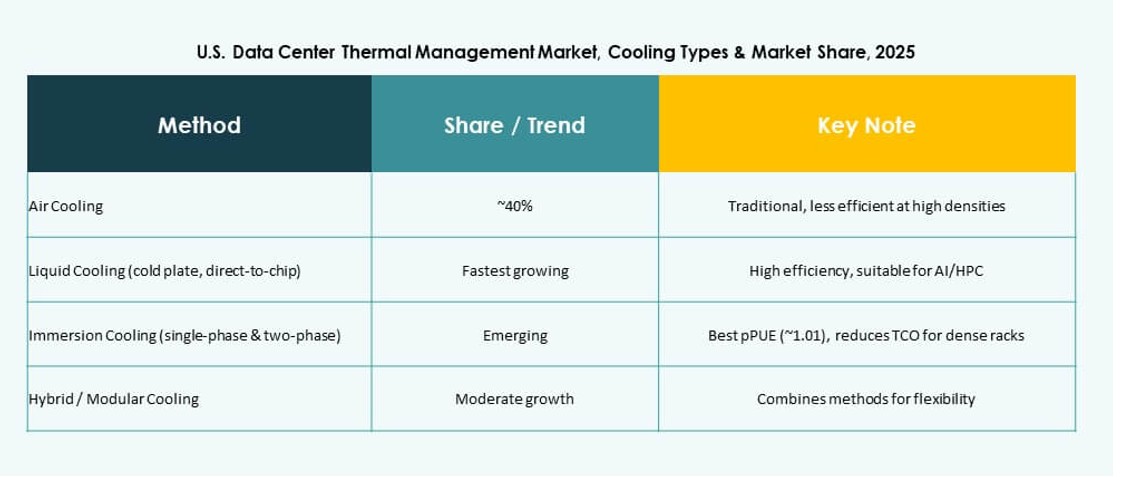

By Cooling Technology

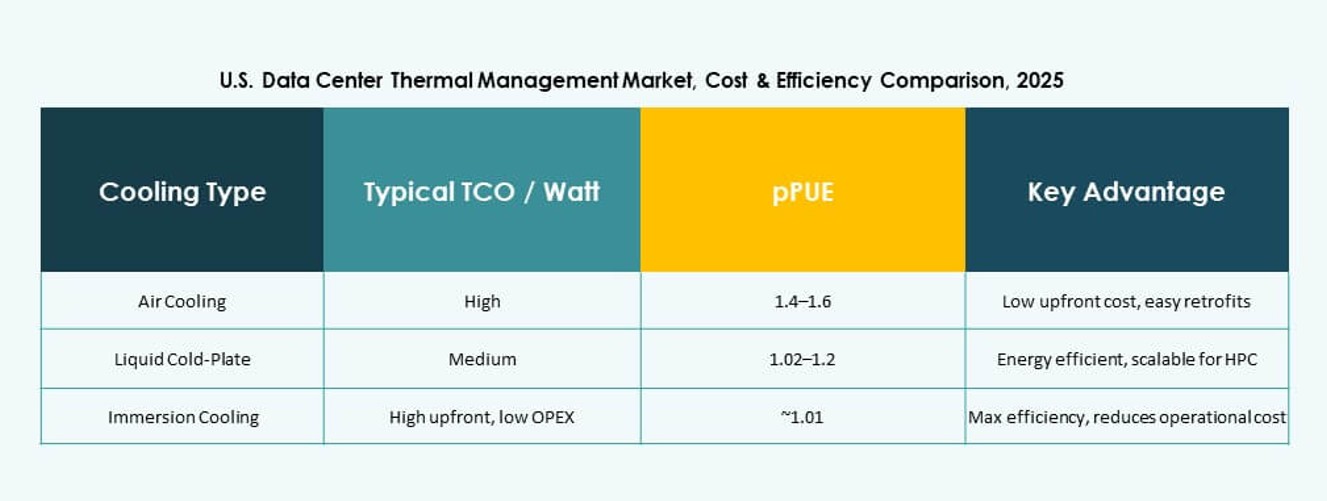

Air-based cooling remains dominant, especially in older and medium-density data centers. Direct air and hot/cold aisle containment remain widely used. However, liquid-based cooling shows the fastest growth, driven by AI, HPC, and blockchain demand. Direct-to-chip and immersion technologies improve thermal efficiency and density capacity. Hybrid cooling balances legacy air systems with liquid upgrades. Emerging methods like thermoelectric and phase-change see niche adoption in high-performance use cases.

By Component

Hardware continues to lead in value contribution to the U.S. Data Center Thermal Management Market, driven by chillers, fans, and heat exchangers. Software, especially AI-enabled platforms, gains importance for optimization. Services ensure continuity through preventive maintenance, retrofits, and remote monitoring. As data centers scale, demand rises for integrated solutions combining all three components.

By Hardware

Cooling units and chillers represent the largest share due to widespread usage across data center sizes. Heat exchangers and airflow devices play key roles in improving internal thermal flow. Rear door solutions and advanced piping systems enable more efficient liquid distribution. Component selection now depends on density targets, form factor, and sustainability goals.

By Software

DCIM dashboards remain foundational for centralized environmental control. AI optimization and CFD simulation tools support advanced modeling and automation. BMS modules integrate thermal controls into facility-wide energy systems. Software enhances cooling precision, predicts failures, and aligns operations with IT load patterns.

By Services

Installation and commissioning dominate initial demand in greenfield projects. Preventive maintenance sustains long-term performance and lowers total cost of ownership. Retrofits and upgrades support thermal modernization in legacy facilities. Monitoring as a service expands with remote-first management models. Flexible service packages ensure uptime and performance compliance.

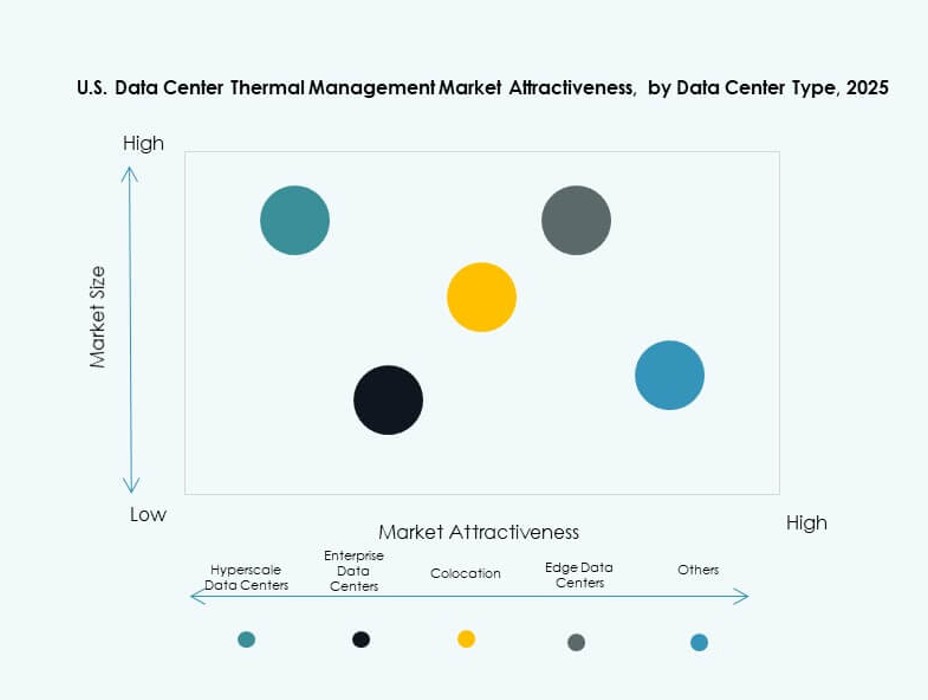

By Data Center Type

Hyperscale and cloud colocation lead the market with consistent expansion across U.S. hubs. Enterprise data centers invest in thermal upgrades for compliance and performance. Edge data centers use compact and efficient systems for remote deployments. It supports AI inference, 5G, and IoT in near-user zones. Diverse cooling needs across types create broad demand for tailored thermal strategies.

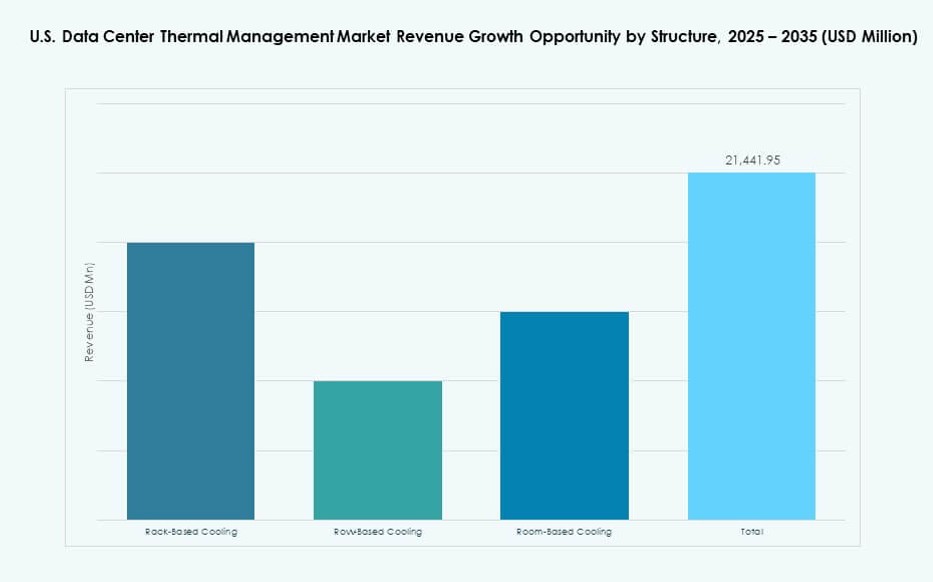

By Structure

Row-based and rack-based systems gain share due to modularity and high-density compatibility. Room-based cooling remains relevant in legacy and low-density settings. Operators now prefer scalable structures that adapt to IT growth and energy targets. It enables phased expansion with controlled capital outlay.

Regional Insights

Western United States Leads in Hyperscale Thermal Innovation Due to Climate and Energy Advantages

The Western U.S. holds the largest market share at 34% in the U.S. Data Center Thermal Management Market. States like California, Oregon, and Utah support hyperscale campuses that benefit from cool climates and renewable power. Operators in these regions deploy indirect air economization and modular liquid cooling to reduce PUE. Low ambient temperatures allow longer free cooling cycles. Power availability and tech ecosystems further attract cloud investment. Western markets prioritize sustainable and high-density cooling infrastructure.

- For instance, Google leverages liquid cooling at scale across its TPU infrastructure to support high‑density AI workloads, using advanced coolant distribution designs that have doubled chip density compared to earlier air‑cooled systems. Its Cloud TPU v5p and AI Hypercomputer architecture integrate liquid cooling to drive performance and efficiency in large AI training environments.

Midwestern States Emerge as Strategic Hubs Due to Land Availability and Grid Reliability

The Midwest accounts for 28% market share, with strong growth in Illinois, Ohio, and Iowa. These states offer land availability, robust power grids, and tax benefits for data infrastructure. It drives expansion of cloud and colocation sites using air and hybrid cooling systems. Climate advantages reduce energy use in thermal operations. Midwestern operators retrofit older facilities with modern cooling to support AI and enterprise workloads. Investors view the region as a cost-effective alternative to coastal hubs.

- For instance, Microsoft is piloting closed-loop liquid cooling designs at its Mount Pleasant, Wisconsin data center, starting in 2026, as part of a broader strategy to eliminate water use for cooling. The company reported achieving a global average Water Usage Effectiveness (WUE) of 0.30 L/kWh in 2024.

Southeastern and Northeastern Regions Drive Growth Through Enterprise and Edge Facility Demand

The Southeastern U.S. holds 21% market share, led by Georgia, North Carolina, and Florida. These states host expanding enterprise and telecom deployments with diverse cooling needs. Northeastern markets, including New York and Massachusetts, contribute 17% share. These regions focus on edge facilities and financial sector data centers. High humidity and heat challenge cooling strategies, pushing innovation in dehumidification and precision systems. It encourages adoption of sealed-loop and air-side assisted solutions. Regional cooling strategies reflect varying climate, urban density, and regulatory environments.

Competitive Insights:

- Vertiv Group Corp.

- Schneider Electric

- Stulz GmbH

- Daikin Industries Ltd.

- Delta Electronics, Inc.

- Trane Technologies plc

- Eaton Corporation

- Airedale International Air Conditioning Ltd.

- Mitsubishi Electric Corporation

- Johnson Controls International plc

The U.S. Data Center Thermal Management Market remains highly consolidated, with leading players commanding significant shares across hardware and service segments. Vertiv, Schneider Electric, and Stulz lead in large-scale deployments for hyperscale and colocation clients. Their offerings include modular, hybrid, and liquid cooling systems optimized for high-density environments. Daikin, Trane, and Mitsubishi focus on HVAC-integrated solutions tailored for enterprise and room-based structures. Eaton and Delta Electronics strengthen their positions through smart control systems and AI-enabled software platforms. It remains competitive due to rising demand for integrated, efficient, and low-water thermal technologies. Product innovation, energy savings, and retrofit services define vendor differentiation. Partnerships, acquisitions, and data center design alliances expand reach and influence customer procurement strategies.

Recent Developments:

- In October 2025, Black Box Corporation partnered with Wind River to deliver intelligent edge and private cloud solutions, supporting data center infrastructure with features like AI workloads and scalable deployments.

- In August 2025, Daikin Industries Ltd. acquired Dynamic Data Centers Solutions, Inc., gaining hybrid air-liquid cooling for AI data center racks to boost efficiency without major infrastructure changes.