Executive summary:

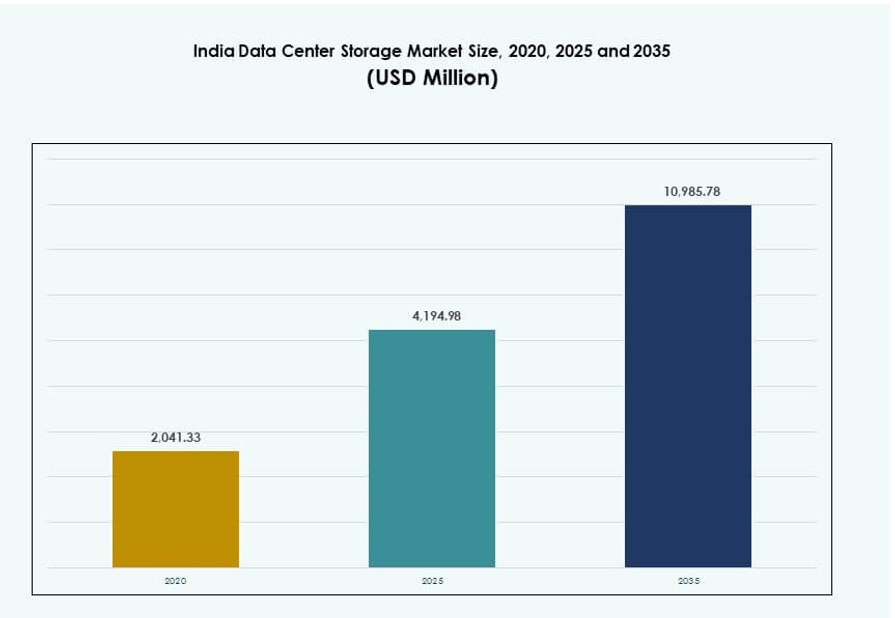

The India Data Center Storage Market size was valued at USD 2,041.33 million in 2020 to USD 4,194.98 million in 2025 and is anticipated to reach USD 10,985.78 million by 2035, at a CAGR of 10.05% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| India Data Center Storage Market Size 2025 |

USD 4,194.98 Million |

| India Data Center Storage Market, CAGR |

10.05% |

| India Data Center Storage Market Size 2035 |

USD 10,985.78 Million |

The market is expanding due to rising cloud adoption, digital services, and enterprise IT modernization. Enterprises are shifting from legacy systems to flash, hybrid, and software-defined storage to support AI, analytics, and 5G. Demand is also driven by government data localization policies and increased use of cloud-native applications. Vendors focus on high-performance, secure, and scalable storage to meet dynamic workload needs. These trends make the India Data Center Storage Market strategically critical for both domestic and global technology investors.

Mumbai and Pune lead the market due to submarine cable access, hyperscale builds, and fintech demand. Chennai and Hyderabad are growing fast with policy support and strong enterprise activity. Bengaluru remains a major hub for IT-driven storage needs, while Noida and Bhopal are emerging due to colocation growth and new AI-ready infrastructure. These regions reflect the country’s expanding and distributed digital infrastructure.

Market Dynamics:

Market Drivers

Digital Transformation and Data Localization Driving Large-Scale Storage Expansion

The rapid digital transformation across sectors is creating massive volumes of data. Businesses in BFSI, telecom, retail, and manufacturing require secure, scalable, and high-speed storage. Government mandates on data localization push enterprises to store data within India, which increases demand for domestic data centers. Cloud-native application growth fuels both object and block storage solutions. Rising demand for edge storage from IoT, smart city, and 5G projects further boosts deployment. The India Data Center Storage Market benefits from these regulatory and enterprise-level shifts. IT infrastructure modernization continues as enterprises migrate legacy systems to virtualized environments. Public sector digitization and smart governance initiatives also contribute to growing storage needs. Strategic investments in storage are now central to business continuity planning.

Cloud Migration and Hybrid IT Accelerating Storage Infrastructure Development

Cloud adoption is increasing across public and private sectors, driving storage infrastructure modernization. Businesses are adopting hybrid IT models that combine on-premise and cloud environments. This shift requires high-speed, low-latency, and resilient storage architectures. Organizations prefer flexible storage solutions that can scale with demand, without compromising security. Tier-1 cities are seeing hyperscale data centers rise to support growing enterprise workloads. The India Data Center Storage Market is expanding its reach beyond traditional hubs, led by demand for hybrid cloud and private storage. New-age technologies such as AI, blockchain, and machine learning demand high-performance and distributed storage. Managed service providers are developing storage-as-a-service offerings to meet evolving enterprise needs. These dynamics redefine storage infrastructure strategies across industries.

Technology Advancements Powering the Shift to High-Speed, Energy-Efficient Storage

Enterprise IT teams are upgrading from traditional spinning disk storage to SSD and NVMe systems. Flash-based storage improves read/write speeds, power efficiency, and reliability. This shift is evident in mission-critical applications that demand real-time access and analytics. Vendors are bundling storage with AI-ready hardware to enable edge data processing. Software-defined storage solutions also improve utilization and reduce hardware dependency. In the India Data Center Storage Market, these innovations are reshaping procurement decisions. Storage systems are also being optimized for low latency and greater fault tolerance. Automation and storage orchestration further improve agility in data-intensive environments. These advancements support next-gen workloads across enterprise and government ecosystems.

- For instance, Tata Consultancy Services (TCS) enables NVMe-based and AI-ready storage integration across enterprise transformation projects, helping clients accelerate data throughput and workload efficiency in performance-intensive environments.

Government and Private Sector Investments Building a Strong Storage Ecosystem

Large investments are flowing into hyperscale and enterprise data centers. Central and state governments offer incentives on land, power, and connectivity. Policy support for digital infrastructure under the National Data Centre Policy encourages private participation. Telecom operators are partnering with hyperscale players to expand storage in Tier-2 and Tier-3 locations. Strategic alliances among cloud service providers and colocation firms are driving storage deployments. The India Data Center Storage Market benefits from coordinated action between stakeholders. New facilities emphasize energy efficiency, modularity, and scalability. Multinational firms are building captive storage environments to meet compliance. The domestic ecosystem continues to attract global interest due to data volume and processing needs.

- For example, AdaniConneX announced hyperscale facilities in Chennai with multi-MW capacity plans, partnering for enterprise connectivity. Specific 30 MW, 100 Gbps, or 200-client metrics remain unconfirmed in public releases.

Market Trends

Shift Toward Green Data Storage and Renewable Energy Integration

Sustainability is becoming a core focus for storage infrastructure development. Data center operators now integrate solar, wind, and hybrid energy systems. Energy-efficient storage hardware and software optimization reduce carbon footprint. Vendors are offering power-managed storage with AI-driven cooling and smart energy routing. Green building certifications like IGBC and LEED are influencing infrastructure design. The India Data Center Storage Market embraces this trend as enterprises align with ESG goals. Hyperscale players now select sites based on renewable energy availability. Energy consumption metrics are used to benchmark efficiency across storage tiers. These developments improve long-term cost efficiency and appeal to impact-focused investors.

Rise in Edge Storage to Support Latency-Sensitive Applications

5G rollouts, autonomous systems, and IoT applications require ultra-low latency. Businesses demand local storage at the edge to process data in real time. Edge data centers integrate compact storage systems closer to end-users. These systems reduce data backhaul to core sites and improve application response. In India, smart manufacturing, retail automation, and telemedicine push edge deployments. The India Data Center Storage Market evolves by supporting decentralized data needs. Vendors now offer ruggedized, modular storage for edge nodes. Edge solutions also improve reliability in areas with unstable connectivity. This decentralization shapes the future of data management across urban and rural regions.

Growth in AI-Optimized and High-Density Storage Solutions

AI workloads require storage with high throughput and consistent IOPS performance. Vendors are offering AI-optimized storage with GPU integration and scalable fabric architecture. High-density storage systems reduce physical footprint and improve data center economics. In India, enterprises use such systems for fraud detection, recommendation engines, and real-time analytics. The India Data Center Storage Market leverages this trend to meet AI adoption needs. Hyper-converged infrastructure (HCI) platforms integrate storage and compute for seamless scalability. These architectures allow rapid deployment and simplified management. Demand for intelligent tiering and automation continues to rise among enterprise IT teams.

Growing Focus on Cybersecurity and Ransomware-Resilient Storage

Data breaches and ransomware attacks increase demand for secure storage. Businesses implement immutable backups, encryption-at-rest, and multi-factor access controls. Air-gapped and cloud-isolated storage models gain traction. Vendors offer intrusion detection features embedded within storage firmware. Enterprises in India prioritize regulatory compliance in BFSI, healthcare, and government sectors. The India Data Center Storage Market reflects growing demand for robust, cyber-resilient systems. Storage vendors collaborate with cybersecurity firms to integrate real-time threat monitoring. Solutions supporting rapid recovery and forensic logging are now standard for critical workloads.

Market Challenges

Infrastructure Constraints and Power Availability Impact Deployment Scale

Power and cooling infrastructure gaps slow deployment timelines in several Indian regions. High-density storage systems require consistent electricity and reliable cooling. In Tier-2 and Tier-3 cities, such utilities are limited or cost-intensive. Land acquisition issues and regulatory clearances also delay greenfield data center projects. The India Data Center Storage Market must address these constraints to meet its long-term targets. Operators invest heavily in redundancy, but operating costs remain high in non-metro areas. Diesel generator reliance affects sustainability and uptime during outages. These limitations affect performance benchmarks and deter some investors. Local utilities must partner with data center firms for scalable solutions.

High Capital Investment and Legacy System Dependencies Reduce Flexibility

Storage infrastructure involves significant upfront investment in hardware, software, and facility build-outs. SMEs and traditional enterprises struggle to transition from legacy to modern systems. Budget constraints limit adoption of SSDs, HCI, and backup automation tools. IT teams also face skills gaps when managing multi-cloud or software-defined storage. In the India Data Center Storage Market, many firms still depend on outdated DAS or tape-based systems. Vendor lock-in and lack of interoperability restrict flexibility. Slow adoption of virtualization tools creates data silos and affects scalability. Enterprises must restructure their procurement and training models for faster modernization.

Market Opportunities

Expansion of Cloud-Native Services Unlocks Storage-as-a-Service Demand

Cloud-native businesses are rapidly scaling across fintech, healthtech, and edtech sectors. These firms prefer scalable, pay-per-use storage models with minimal CapEx. Providers now offer tiered Storage-as-a-Service (STaaS) with region-specific compliance. The India Data Center Storage Market can tap this trend by supporting cloud startups and digital-first firms. As SaaS adoption grows, demand rises for flexible and secure storage backends. Storage providers can gain from co-developing platforms with hyperscale and cloud-native partners.

Local Manufacturing and Policy Incentives Boost Domestic Storage Hardware

The Production-Linked Incentive (PLI) scheme supports local electronics and storage manufacturing. Firms are setting up SSD and HDD assembly plants in India. The India Data Center Storage Market benefits from this domestic ecosystem by lowering hardware imports. Policy support improves pricing and lead time for local deployments. Emerging vendors gain opportunities to serve enterprise storage segments with region-specific solutions.

Market Segmentation

By Storage Type

Traditional storage still holds a significant share due to legacy infrastructure in public sector and SMEs. However, all-flash storage is gaining rapid traction in enterprise and hyperscale environments due to faster IOPS and lower power use. Hybrid storage solutions combining SSD and HDD are widely adopted in mid-sized enterprises balancing performance and cost. The India Data Center Storage Market reflects this shift as flash-based adoption continues across critical applications.

By Storage Deployment

Storage Area Network (SAN) systems dominate due to high-performance demands in BFSI and telecom sectors. Network-attached Storage (NAS) systems serve content-heavy industries such as media, healthcare, and education. Direct-attached Storage (DAS) remains relevant in small-scale IT setups but is declining. The India Data Center Storage Market sees SAN and NAS expansion across enterprise workloads with increased cloud integration.

By Component

Hardware contributes the bulk of the revenue due to physical infrastructure investments. However, software components are gaining share due to rising adoption of virtualization, automation, and storage orchestration tools. Vendors bundle software-defined capabilities with their storage products to improve agility. The India Data Center Storage Market is moving toward intelligent, self-managing systems driven by AI and machine learning.

By Medium

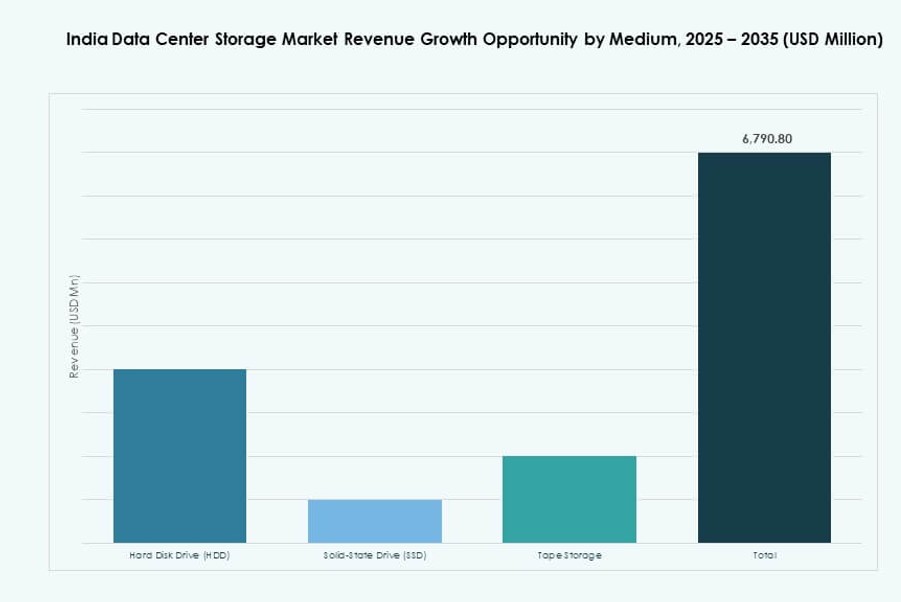

Hard Disk Drives (HDD) are still used in archival and cold storage applications, especially in legacy data centers. Solid-State Drives (SSD) lead high-speed and performance-critical environments. Tape storage is niche but remains in use for long-term backups and regulatory compliance. The India Data Center Storage Market sees SSD demand growing fastest due to price drops and AI-enabled applications.

By Deployment Model

Cloud-based deployment is growing rapidly due to cost flexibility, scalability, and remote management. On-premises models remain important in BFSI, government, and regulated sectors. Hybrid deployments that balance control with flexibility are now common in large enterprises. The India Data Center Storage Market supports all three models, but hybrid is emerging as the preferred choice.

By Application

IT and telecom sectors lead in storage adoption due to massive data processing needs. BFSI follows with stringent security and compliance-driven storage needs. Healthcare and government sectors see growth due to digitization initiatives. Other verticals such as retail and logistics also invest in scalable storage. The India Data Center Storage Market continues to diversify its application footprint across public and private sectors.

Regional Insights

Western India Leads with Mumbai and Pune Driving Over 35% Market Share

Mumbai remains the country’s largest data center hub, offering strong fiber connectivity, submarine cables, and financial services demand. Pune complements this with IT parks and hyperscale interest. Western India leads with over 35% of the India Data Center Storage Market. The region benefits from established infrastructure, skilled workforce, and government support for tech investments. Demand for cloud, fintech, and media workloads further boosts storage needs.

- For instance, CtrlS Datacenters operates Mumbai DC1 & DC2 with 5,555 racks and 42 MW power capacity in a Rated-4 facility. Pune complements this with IT parks and hyperscale interest.

Southern India Holds Around 30% Market Share with Chennai, Bengaluru, and Hyderabad as Key Centers

Chennai offers coastal cable landing stations and stable power, supporting hyperscale builds. Bengaluru remains a top tech hub with demand from startups and global firms. Hyderabad’s proactive policies and expanding IT zone make it a fast-growing market. Southern India accounts for nearly 30% of the India Data Center Storage Market. These cities offer a balanced mix of enterprise, cloud, and managed service demand.

Northern and Emerging Eastern Regions Hold 20% and 15% Respectively with Rising Colocation Growth

Delhi NCR anchors Northern India with strong enterprise presence and regulatory institutions. Noida and Gurugram see colocation growth and rising interest from hyperscale operators. In the East, Kolkata begins to attract storage infrastructure investments for regional connectivity and industrial support. Northern and Eastern regions combined hold 35% of the India Data Center Storage Market. Expansion in these regions is driven by government digitization, data sovereignty, and Tier-2 city demand.

- For instance, CtrlS’ Noida hyperscale data center is a Tier IV facility with 9-Zone security, a structure of B1 + G + 7 floors, and delivers up to 13 MW IT load. The site features liquid cooling for AI workloads and sources 60% of its power from solar energy.

Competitive Insights:

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- IBM Corporation

- NetApp

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Hitachi Vantara

- Lenovo Group

- Cohesity, Inc.

- Nutanix, Inc.

The India Data Center Storage Market is highly competitive, led by global vendors with strong channel networks and local partnerships. Dell Technologies and HPE maintain dominance through extensive enterprise deployments and full-stack storage solutions. IBM and NetApp focus on hybrid cloud and software-defined storage, serving BFSI and telecom sectors. Cisco and Lenovo offer integrated storage within broader infrastructure portfolios. Huawei and Hitachi Vantara strengthen their positions in high-density storage and AI workloads. Emerging players like Cohesity and Nutanix gain traction in hyper-converged and backup-driven architectures. It experiences dynamic competition with frequent product launches and cloud-native offerings. Market share shifts are driven by cloud integration, performance, data security, and regional service delivery.

Recent Developments:

- In December 2025, Cohesity invested significantly in India by doubling its engineering capacity in Bangalore and Pune to develop AI-augmented data security tools, including immutable storage for cyber resilience in data center operations.

- In April 2025, Hewlett Packard Enterprise (HPE) collaborated with Lupin to deploy private cloud solutions, optimizing costs and accelerating innovation with a focus on secure, efficient data storage for Indian enterprises.

- In February 2025, Dell Technologies announced the 2025 Partner Program emphasizing enhanced growth incentives for storage solutions and advancing its Partner First Strategy for Storage to foster collaboration and unlock revenue in data center environments.

- In January 2025, Lenovo Group entered a definitive agreement to acquire Infinidat, bolstering its high-end enterprise storage portfolio for modern data centers with improved performance and scalability relevant to India’s growing infrastructure needs.