Executive summary:

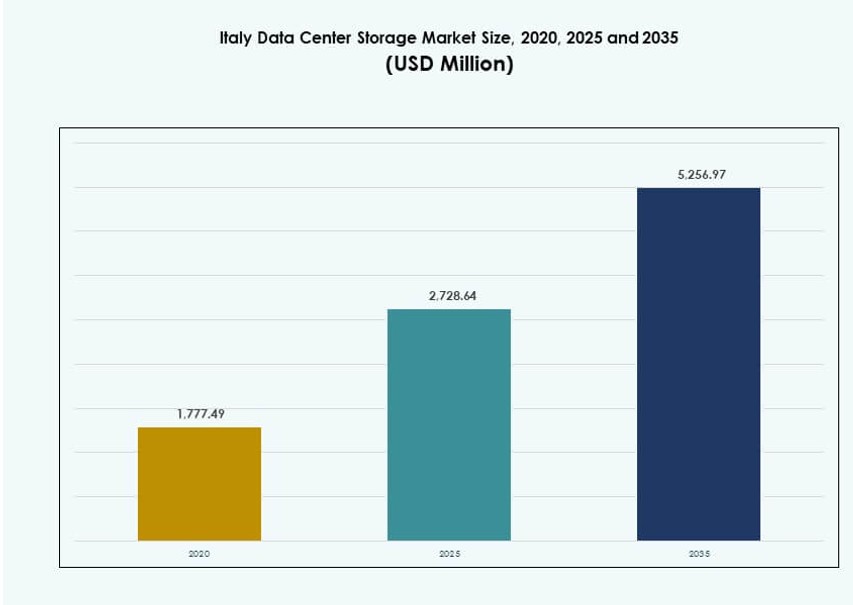

The Italy Data Center Storage Market size was valued at USD 1,777.49 million in 2020 to USD 2,728.64 million in 2025 and is anticipated to reach USD 5,256.97 million by 2035, at a CAGR of 6.72% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Italy Data Center Storage Market Size 2025 |

USD 2,728.64 Million |

| Italy Data Center Storage Market, CAGR |

6.72% |

| Italy Data Center Storage Market Size 2035 |

USD 5,256.97 Million |

Demand for scalable, secure, and high-speed storage systems is growing rapidly across Italy. Businesses are shifting from traditional infrastructure to cloud-first and hybrid models, driving adoption of software-defined and flash storage solutions. Innovations like NVMe, edge storage, and AI-powered storage management are transforming operations. Enterprises seek solutions that ensure compliance, performance, and cost efficiency. These shifts position storage infrastructure as a foundation for Italy’s digital economy. The Italy Data Center Storage Market plays a critical role in enabling seamless operations, real-time analytics, and workload portability across industries.

Northern Italy dominates the market, supported by hyperscale growth, cloud investments, and enterprise concentration in Milan and Turin. Central Italy, particularly Rome, is gaining traction with strong government and public sector digitization programs. Southern Italy and island regions are emerging, fueled by localized edge infrastructure, land availability, and incentives. This geographic shift is enhancing data coverage, regional storage resilience, and market inclusivity.

Market Dynamics:

Market Drivers

Shift Toward Cloud Workloads Accelerating Storage Infrastructure Overhaul in Italy

The Italy Data Center Storage Market is expanding due to rising enterprise cloud adoption. Italian firms across sectors are shifting from legacy systems to scalable, high-performance storage architectures. Cloud-native applications, AI-driven services, and IoT adoption are increasing storage complexity. This pushes demand for reliable, low-latency, and high-throughput storage systems. Enterprises seek flexible solutions like software-defined storage and hyperconverged infrastructure. Hybrid cloud setups are now common, combining on-prem and cloud storage for agility. Vendors tailor offerings to support mixed environments and regulatory needs. The Italy Data Center Storage Market gains importance for businesses adapting to digital transformation. It supports business continuity, speed, and compliance with growing data regulations.

- For instance, Almaviva partnered with leading cloud providers to deploy hybrid cloud solutions for enterprise customers in Italy, enhancing data services and storage flexibility.

Rise of Digital Services Fueling Need for High-Performance Storage Systems

Data-heavy services streaming, fintech, telemedicine are growing rapidly across Italy, creating huge storage needs. These services require fast access, redundancy, and scalability. Storage vendors are focusing on performance improvements via NVMe-based flash systems and intelligent tiering. Demand for data locality and low-latency access is pushing edge data center growth. Public and private sector IT upgrades further stimulate infrastructure investments. Energy efficiency remains critical, driving adoption of storage that uses less power per gigabyte. Storage planning now aligns with strategic IT goals rather than pure capacity expansion. The Italy Data Center Storage Market becomes central to enabling real-time services and digital customer experiences.

Enterprise Data Protection Needs Driving Demand for Modern Backup and Archival Solutions

Italian enterprises are focusing more on data protection, disaster recovery, and regulatory compliance. Traditional backup systems are being replaced with modern, automated, and cloud-integrated storage solutions. Vendors offer snapshot-based, continuous data protection and ransomware-resilient architectures. Regulations such as GDPR enforce strict data retention and sovereignty requirements. This fuels investment in both on-prem and hybrid archival systems. Long-term storage formats like tape and cold storage still hold relevance for compliance use. Data tiering ensures critical data is kept on fast storage, while archives are stored cost-effectively. The Italy Data Center Storage Market plays a key role in enabling secure, compliant IT strategies for all sectors.

- For instance, Commvault offers its Metallic SaaS backup platform across Europe, including Italy, supporting enterprise workloads with cloud-integrated data protection. The platform is designed to reduce recovery times and enhance ransomware resilience for hybrid IT environments.

5G Expansion and Edge Computing Infrastructure Bolstering Storage Distribution Across Regions

The rollout of 5G and edge computing in Italy increases demand for decentralized, local storage capabilities. Telecom operators and cloud providers are deploying micro data centers to support low-latency services. These nodes require efficient storage solutions tailored for constrained environments. The architecture must be compact, energy-efficient, and easy to scale. Smart cities, autonomous mobility, and connected industry applications accelerate edge storage adoption. Data replication and caching strategies reduce latency and network load. Hardware vendors are optimizing products for edge-specific use cases. The Italy Data Center Storage Market sees long-term growth from this distributed infrastructure shift.

Market Trends

Growth of Software-Defined Storage Platforms Enabling Greater Control and Scalability

The Italy Data Center Storage Market is witnessing increased uptake of software-defined storage (SDS). Enterprises want more control over storage configuration and resource allocation. SDS solutions decouple hardware from management, improving agility. IT teams can scale resources dynamically, lower costs, and simplify operations. SDS also supports automation and seamless integration with orchestration platforms. Open-source platforms and vendor-neutral systems attract IT teams seeking flexibility. The trend supports hybrid and multi-cloud operations. This shift redefines how enterprises manage and provision storage infrastructure.

AI-Powered Storage Solutions Emerging to Automate Data Lifecycle and Improve Utilization

Artificial intelligence integration is transforming how storage systems operate across Italian data centers. Vendors now embed AI for workload prediction, data classification, and storage optimization. These systems enhance performance tuning, capacity forecasting, and automated tiering. AI helps identify redundant data, reducing storage waste and operational costs. Businesses use these features to meet compliance and business continuity goals. AI-powered analytics also support anomaly detection and preemptive maintenance. The Italy Data Center Storage Market integrates these tools to make systems self-optimizing. It reflects a larger move toward intelligent infrastructure in Italy.

Transition from HDD-Based Systems to Flash and NVMe for Higher Throughput Applications

The adoption of flash-based systems, particularly NVMe, is accelerating across Italian data centers. Organizations favor faster IOPS and reduced latency for mission-critical applications. Industries like finance, e-commerce, and AI/ML are shifting to NVMe for performance gains. Traditional HDDs remain in use but are now limited to archival roles. Vendors offer hybrid solutions to manage cost-performance balance. Flash storage is now more cost-competitive, especially in enterprise use. NVMe over Fabrics (NVMe-oF) extends performance benefits across storage networks. The Italy Data Center Storage Market is undergoing a major transition in medium type and architecture.

High-Density Storage and Modular Systems Gaining Ground to Optimize Physical Space

Space constraints and power limitations drive demand for high-density storage in urban data centers. Rack-optimized and modular systems improve scalability without large floor plan expansions. These systems simplify deployment and support standardized growth. Enterprises prefer modular systems for faster rollout and operational consistency. Vendors also offer prefabricated pods with integrated power, cooling, and storage. Italy’s growing edge infrastructure also benefits from compact storage formats. High-density systems address environmental targets by minimizing energy per terabyte. The Italy Data Center Storage Market now includes solutions built for energy, performance, and physical efficiency.

Market Challenges

Rising Power and Cooling Requirements Create Infrastructure Bottlenecks for Storage Systems

The shift toward high-performance flash and NVMe systems increases power consumption. These systems generate more heat and require enhanced cooling infrastructure. Many Italian facilities, especially older ones, lack modern cooling and power redundancy. This creates challenges in deployment, reliability, and cost. Space limitations in urban data centers worsen the issue. Operators need to retrofit or relocate to handle these needs, raising CapEx. Energy prices in Italy also affect operational costs of power-hungry storage arrays. The Italy Data Center Storage Market must navigate these constraints to support continued growth.

Compliance with Data Sovereignty and Protection Regulations Increases System Complexity

Italy enforces strong data protection frameworks aligned with the EU’s GDPR. Storage systems must provide traceability, access control, and audit readiness. Ensuring on-prem or regional data residency can complicate hybrid deployments. Multinational vendors must localize infrastructure or partner with regional providers. Ensuring encryption at rest and in transit is now mandatory across sectors. Complexity grows when managing backups and archiving across geographies. Legal risk and penalties push firms to overinvest in compliance tools. The Italy Data Center Storage Market must align technical features with evolving legal frameworks.

Market Opportunities

Hybrid and Multi-Cloud Strategies Create Demand for Interoperable and Scalable Storage Platforms

Italian enterprises are increasingly adopting hybrid models to combine agility and control. These setups require storage platforms that support seamless data movement. Interoperability across cloud and on-prem systems becomes a critical need. Vendors offering cloud-native and container-ready storage find strong demand. The Italy Data Center Storage Market benefits from this long-term digital shift. It enables firms to scale storage with business needs without vendor lock-in.

Industry-Specific Data Growth Unlocks Tailored Solutions for Healthcare, Finance, and Government

Different industries in Italy demand customized storage solutions to meet performance and compliance needs. Healthcare requires secure and high-throughput systems for imaging data. Finance prioritizes low-latency systems with strict audit trails. Government agencies look for resilient, sovereign-compliant storage. Vendors that address these vertical needs see faster adoption. The Italy Data Center Storage Market holds strong growth potential in industry-specific offerings.

Market Segmentation

By Storage Type

Hybrid storage systems dominate the Italy Data Center Storage Market due to their balance between performance and cost. These systems combine HDDs and SSDs, helping enterprises optimize data tiering strategies. Traditional storage still exists in legacy systems but is steadily declining. All-flash arrays are gaining share as prices fall and workloads require faster speeds. Niche systems, including object storage, serve specialized big data and backup needs.

By Storage Deployment

Storage Area Network (SAN) systems lead due to high-speed data transfer needs in enterprise IT setups. SAN is critical for mission-critical databases and virtualized workloads. Network-attached storage (NAS) follows, preferred for shared file access across teams. Direct-attached storage (DAS) finds use in edge and branch locations. Other deployment models, including object and scale-out file systems, are emerging in analytics and HPC workloads.

By Component

Hardware holds the largest share of the Italy Data Center Storage Market, with demand driven by infrastructure expansion. Storage arrays, racks, and drives make up the bulk of investments. Software gains traction due to growing SDS adoption, where management layers control heterogeneous environments. Storage software enables tiering, backup, and orchestration functions vital in hybrid and cloud-first environments.

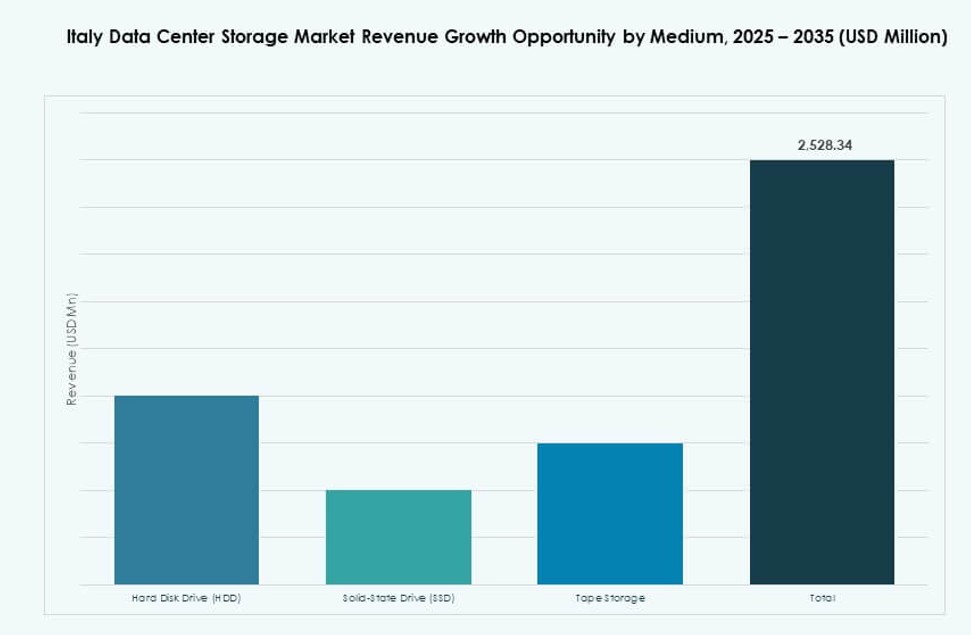

By Medium

Hard Disk Drives (HDDs) retain a significant share for archival and cold storage due to their cost-effectiveness. Solid-State Drives (SSDs) are growing rapidly with demand for faster data access and reduced latency. Tape storage remains relevant in government and healthcare segments for long-term archival, especially where air-gapping is needed for security. SSDs are expected to overtake HDDs in active workloads.

By Deployment Model

Cloud-based models are rising quickly, driven by digital transformation and demand for flexibility. Enterprises adopt cloud-native storage for scalability and lower CapEx. On-premises deployment remains strong in industries with data sovereignty needs. Hybrid deployment models dominate, allowing firms to balance security, cost, and performance. This hybrid dominance aligns with Italy’s maturing IT landscape.

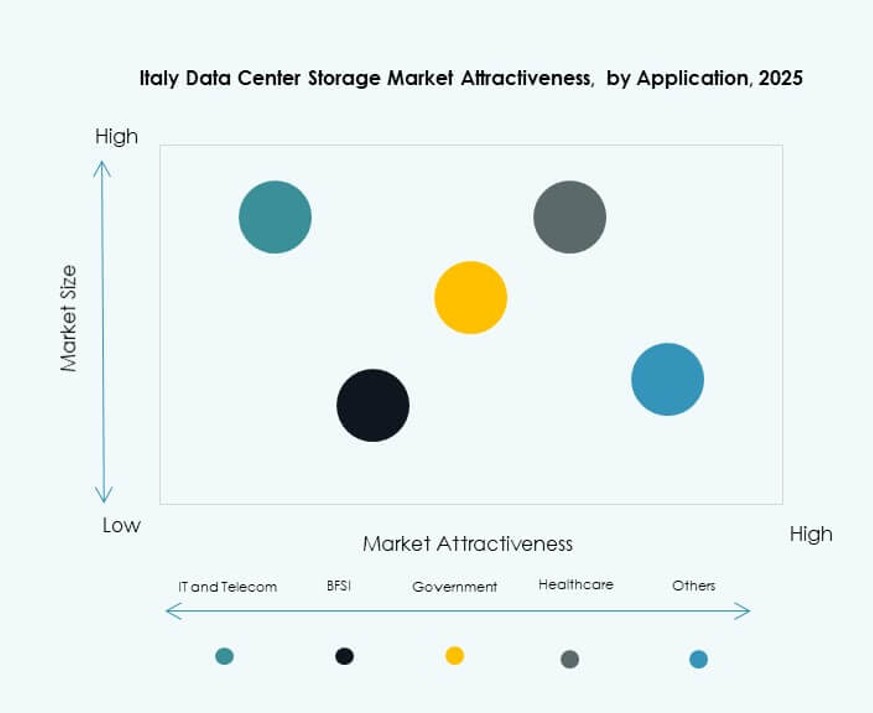

By Application

IT and telecommunications lead the Italy Data Center Storage Market, driven by digital services and connectivity expansion. BFSI follows due to secure, high-speed storage demands in transaction-heavy environments. Government agencies are digitizing services and expanding cloud use, driving public sector growth. Healthcare’s need for secure imaging and EMR storage supports steady demand. Other sectors include education, manufacturing, and retail, each contributing niche but growing requirements.

Regional Insights

Northern Italy Holds Over 55% Share, Led by Milan’s Role as Digital Infrastructure Hub

Northern Italy dominates the Italy Data Center Storage Market with over 55% share. Milan serves as the primary data center cluster, housing hyperscale and colocation facilities. The region benefits from industrial concentration, network connectivity, and enterprise headquarters. Data center operators expand in Lombardy to serve AI, fintech, and telecom demands. Storage vendors target this area for high-performance and hybrid deployments. Northern Italy’s infrastructure maturity supports large-scale IT expansion.

- For instance, Equinix ML2 in Milan delivers 3 MW power capacity and 18,750 sq. ft. of colocation space with N+1 redundancy, supporting regional storage and interconnection needs.

Central Italy Accounts for 25% Share with Government and Public Sector-Led Demand

Central Italy, including Rome and Lazio, represents around 25% of the market. Government digitization programs and public sector modernization are primary growth drivers. Universities and research institutions also require advanced storage for HPC workloads. The colocation market is smaller but growing steadily. Vendors provide tailored storage to meet compliance and budget constraints. Central Italy supports hybrid storage growth in civic and academic sectors.

Southern Italy and Islands Contribute 20% Share, With Edge and Localized Infrastructure Investments

Southern Italy, including Naples, Bari, and Sicily, holds 20% market share. Storage growth is tied to edge data center development and regional investments. Telecom and utility firms deploy local IT infrastructure to reduce latency. Economic incentives encourage colocation providers to expand southward. Energy availability and land costs support greenfield projects. The Italy Data Center Storage Market sees this region as an emerging opportunity for distributed storage deployment.

- For instance, Aruba S.p.A. expanded its data center footprint in Italy in 2024 with enhancements to its core facilities to support hybrid cloud and high‑performance enterprise workloads.

Competitive Insights:

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- IBM Corporation

- NetApp

- Seagate Technology

- Veeam Software

- Huawei Technologies Co., Ltd.

- Engineering Group

- Toshiba Corporation

- Lenovo Group

The Italy Data Center Storage Market features a mix of global storage leaders and prominent domestic IT providers. Companies like Dell Technologies, HPE, and IBM dominate enterprise storage deployments across sectors due to their broad portfolios and service integration. NetApp and Seagate provide advanced storage hardware optimized for diverse workloads. Domestic firms such as Engineering Group and Almaviva compete in public sector contracts and managed services. Veeam and Cohesity specialize in backup and data protection, critical for regulated industries. Huawei, Toshiba, and Lenovo strengthen hardware supply options, often focusing on hybrid and flash-based solutions. The market remains competitive, with partnerships, innovation, and regional presence driving leadership positioning.

Recent Developments:

- In November 2025, Oracle launched its second cloud region in Turin, Italy, offering full access to Oracle Cloud Infrastructure services. This expansion enhances cloud storage availability and supports latency-sensitive workloads across Italian enterprise and public sector environments.

- In November 2025, A2A announced an updated investment plan of $27 billion, driven by rising demand for data center infrastructure in Italy. The plan includes significant enhancements in storage capacity to support hyperscale growth and enterprise digital transformation initiatives.

- In September 2025, Cubbit entered a Business Alliance Partnership with HERABIT to establish decentralized storage and compute services in the Emilia-Romagna region. The deployment includes an initial 2PB capacity aimed at enterprise clients, strengthening regional data center infrastructure in Italy.

- In June 2025, Dell Technologies introduced the Concept Astro platform, designed to optimize power usage in high-density data centers across Italy. The platform uses agentic AI and digital-twin modeling to reduce energy consumption while maintaining performance in storage-intensive environments.

- In March 2025, Almaviva announced a strategic partnership with Oracle to integrate its multilingual generative AI models, Velvet, into Oracle Cloud Infrastructure. This collaboration supports AI adoption across Italy and Europe, enhancing enterprise storage and compute capabilities on local cloud platforms.