Executive summary:

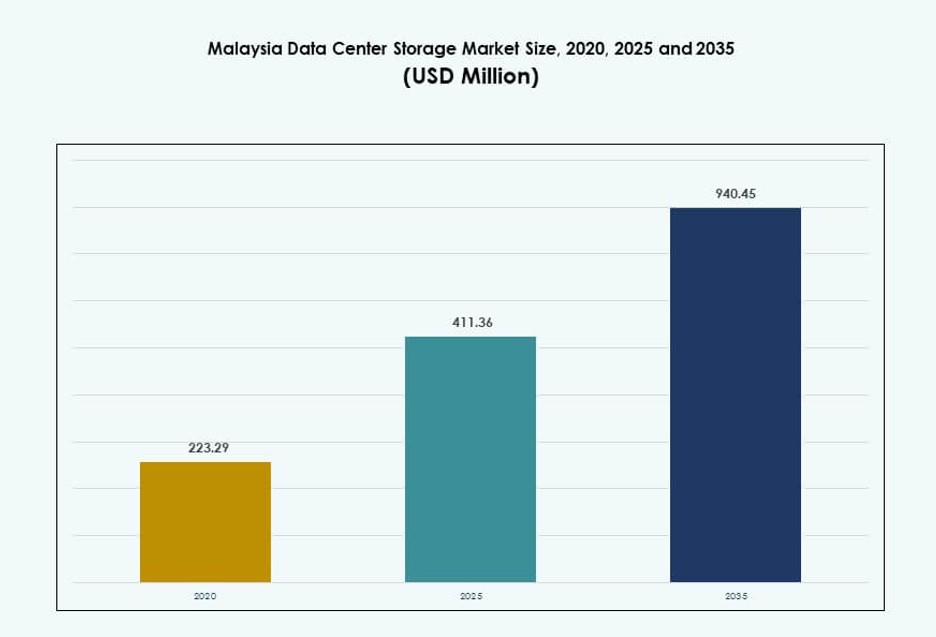

The Malaysia Data Center Storage Market size was valued at USD 223.29 million in 2020 to USD 411.36 million in 2025 and is anticipated to reach USD 940.45 million by 2035, at a CAGR of 8.53% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Malaysia Data Center Storage Market Size 2025 |

USD 411.36 Million |

| Malaysia Data Center Storage Market, CAGR |

8.53% |

| Malaysia Data Center Storage Market Size 2035 |

USD 940.45 Million |

Malaysia is experiencing rapid demand for scalable, low-latency storage infrastructure driven by cloud migration, digital transformation, and AI adoption. Enterprises and government bodies are upgrading legacy systems to flash and hybrid storage solutions to support data-intensive operations. Regulatory focus on data localization and rising edge deployments from telecom operators are reshaping infrastructure strategies. Investments from global cloud players and local service providers enhance the country’s storage capabilities, making the market increasingly vital for enterprise resilience and regional data operations.

Central Malaysia, particularly Kuala Lumpur, Cyberjaya, and Selangor, leads the market due to dense infrastructure, connectivity, and data center clustering. Johor is emerging as a strategic location for hyperscale investments due to proximity to Singapore and available land. Northern and East Malaysian regions are slowly adopting storage solutions through government projects and edge computing use cases. This geographic spread reflects a balanced growth outlook across urban and industrial zones.

Market Dynamics:

Market Drivers

Rising Demand for Low-Latency Enterprise Applications Fueling Infrastructure Modernization Across Urban Clusters

Malaysia is witnessing strong enterprise adoption of cloud-native storage and AI-integrated platforms. Digital-first business models across sectors require faster access to high-volume data sets. Companies upgrade to all-flash and hybrid architectures to improve latency and performance. Malaysia’s government supports digital economy targets under MyDIGITAL, which drives enterprise cloud spending. Tier III+ data centers are expanding capacity to match demand for real-time analytics. Telecom players are launching new edge facilities to reduce latency. Businesses adopt software-defined storage to centralize control across distributed environments. The Malaysia Data Center Storage Market benefits from these shifts in workload architecture. It enables critical industries to handle rapid data processing.

Growing Adoption of AI, IoT, and Smart Manufacturing Increasing Data Storage Requirements

AI and IoT applications generate large volumes of structured and unstructured data across industries. Industrial automation and smart manufacturing create demand for scalable, flexible storage systems. Enterprises deploy object-based storage to retain sensor data from connected devices. The transition to smart city infrastructure also drives centralized storage requirements. Cloud-based storage services expand to support edge-to-core data movement. Businesses rely on real-time insights for predictive maintenance and operational efficiency. These trends increase demand for advanced storage platforms and data management solutions. The Malaysia Data Center Storage Market continues to benefit from this widespread technology adoption. It remains integral to long-term digital transformation.

- For instance, under the Malaysia Digital (MD) initiative, the Data Centre and Cloud vertical secured RM30.95 billion in approved investments as of June 2025, including RM13.45 billion committed by data centre companies. This reflects strong demand for scalable storage driven by AI, IoT, and automation needs across key sectors.

Regulatory Push for Data Localization Creating Growth in Domestic Storage Infrastructure

Malaysia enforces data residency laws that require certain public and private sector data to remain local. The Personal Data Protection Act and sector-specific compliance frameworks have driven localized storage setups. Financial institutions and healthcare providers deploy on-premise or hybrid storage to meet regulations. Cloud service providers collaborate with local operators to meet compliance. Data center operators expand facilities in Cyberjaya and Johor to host compliant infrastructure. These shifts ensure data sovereignty and security. Enterprises align storage strategies with regulatory expectations. The Malaysia Data Center Storage Market benefits from this alignment. It enables trusted digital services in regulated sectors.

- For instance, Microsoft and AWS have launched Malaysia cloud regions with local infrastructure to meet data residency and compliance requirements under Malaysia’s Personal Data Protection Act (PDPA), enabling more regulated workloads to be hosted within domestic data centers.

Strategic Positioning as a Regional Hub Encouraging Multinational Cloud and Storage Investment

Malaysia’s proximity to Singapore and central location in ASEAN attract hyperscale investors. Johor and Cyberjaya emerge as regional nodes for cloud and storage networks. Lower land costs, tax incentives, and power availability enhance attractiveness. Global cloud providers set up availability zones to serve Southeast Asia. Enterprises across the region route storage workloads through Malaysian data centers. Carrier-neutral facilities support redundant connectivity to international cable landings. The Malaysia Data Center Storage Market benefits from this strategic positioning. It enables regional cloud expansion and cross-border storage operations.

Market Trends

Shift Toward Sustainable Storage Infrastructure Designs Driven by Energy Efficiency Goals

Operators are integrating energy-efficient technologies into storage infrastructure to meet ESG mandates. Malaysia’s data centers use renewable power mix and intelligent cooling to lower carbon footprints. Enterprises adopt storage platforms with lower idle power consumption. Flash arrays replace high-power legacy disks in sustainability-led refresh cycles. Green data centers deploy AI to optimize power-to-storage utilization ratios. Sustainability certifications are now part of colocation selection criteria. The Malaysia Data Center Storage Market reflects this transition. It promotes energy-conscious storage deployment for future-ready facilities.

Rise in Multi-Cloud Storage Adoption for Flexibility, Compliance, and Cost Optimization

Enterprises avoid vendor lock-in by using multi-cloud storage solutions across public and private clouds. Data sovereignty laws are met by using localized cloud zones for regulated workloads. Backup, disaster recovery, and archival strategies span multiple cloud regions. Object and block storage are provisioned dynamically for different applications. Storage software enables orchestration across environments with policy control. Businesses optimize costs using hot–cold tiering across providers. The Malaysia Data Center Storage Market supports this model with hybrid-friendly infrastructure. It ensures operational agility and compliance continuity.

Increased Focus on Cyber Resilience Driving Demand for Secure, Immutable Storage

Organizations prioritize cyber-resilient storage systems amid rising ransomware attacks. Immutable storage snapshots and air-gapped backup systems are deployed widely. Storage encryption at rest and in transit is now standard. Enterprises adopt zero-trust architecture to prevent unauthorized access. Compliance-driven sectors require real-time data integrity checks. RTO and RPO objectives are being shortened with fast-recovery solutions. The Malaysia Data Center Storage Market integrates these features. It offers secure platforms for data continuity and recovery assurance.

Expansion of Edge Storage Deployments for Real-Time and Remote Data Applications

Edge storage is being deployed to support remote work, industrial IoT, and smart city operations. Enterprises collect and process data closer to the source for reduced latency. Distributed storage nodes support traffic control, surveillance, and predictive analytics. Telcos embed micro data centers into 5G towers. Healthcare and logistics firms push data to edge for on-site decisions. These deployments reduce reliance on centralized infrastructure. The Malaysia Data Center Storage Market aligns with this edge-first shift. It supports diverse data flows across core and edge locations.

Market Challenges

Limited Availability of High-Capacity Power and Renewable Sources for Hyperscale Storage Growth

Malaysia faces infrastructure limitations in power supply and renewable energy access for hyperscale builds. Grid expansion lags behind demand in key industrial and suburban zones. Developers struggle to secure sustainable power purchase agreements. High-capacity workloads like AI training require predictable power, which adds risk. This creates bottlenecks in hyperscale cloud and storage rollout timelines. Cost of power is also rising in urban zones, affecting operational margins. This limits investor interest in developing large storage-intensive campuses. The Malaysia Data Center Storage Market needs coordinated policy and utility upgrades. It must overcome these gaps to support long-term growth.

Talent Gaps in Data Storage Specialization Slowing Advanced System Deployments

Shortage of skilled professionals in storage architecture, data governance, and software-defined storage affects deployments. Enterprises delay upgrades due to lack of in-house expertise for configuration and maintenance. Cybersecurity talent shortage also affects secure storage operations. Training pipelines remain limited for AI-driven storage technologies. Vendors invest in partnerships with universities to fill workforce gaps. Delays in talent onboarding extend lead times for full system implementation. The Malaysia Data Center Storage Market faces constraints in technical maturity. It must develop local talent ecosystems for sustained innovation.

Market Opportunities

Rising Regional Demand for Compliant Storage Infrastructure Creating Export and Partnership Potential

Neighboring countries face stricter compliance laws and infrastructure gaps, driving demand for Malaysian facilities. Local operators form alliances with foreign cloud providers to host regional workloads. Malaysia offers compliant storage zones for financial, healthcare, and public sector clients. The Malaysia Data Center Storage Market can export managed storage services. It positions itself as a regional compliance-ready storage hub.

Growth of Digital Services Among MSMEs and Startups Expanding Need for Modular Storage Platforms

Small businesses and digital startups require flexible storage solutions that scale with growth. Demand rises for modular, pay-as-you-go storage services. Local providers offer containerized storage with APIs and low latency. The Malaysia Data Center Storage Market supports this with localized offerings. It expands market access beyond large enterprises.

Market Segmentation

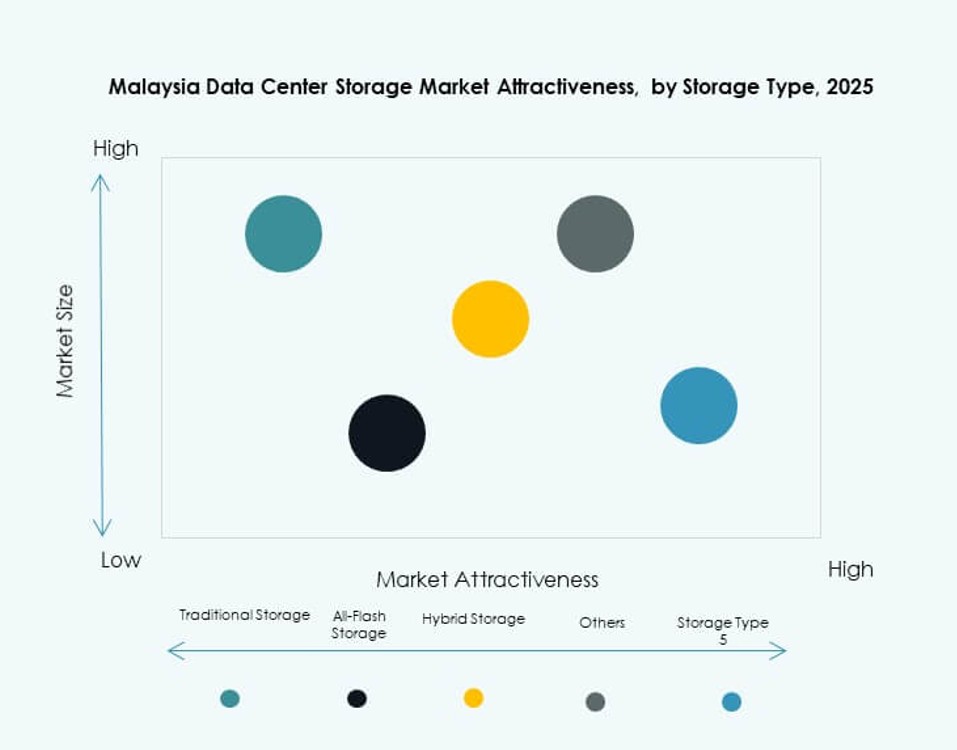

By Storage Type

Traditional storage systems continue to dominate in legacy enterprises and government setups due to familiarity and cost control. All-flash storage is growing fast across AI and financial applications due to its high-speed performance. Hybrid storage models combine the reliability of HDD with the speed of SSD, gaining adoption in large enterprises. The Malaysia Data Center Storage Market reflects a shift toward hybrid and flash-based storage among digital-native companies.

By Storage Deployment

Storage Area Network (SAN) systems lead the segment, especially in financial and high-availability applications. Network-attached Storage (NAS) is widely adopted across IT services and media firms due to easy scalability. Direct-attached Storage (DAS) remains relevant for small offices and branch deployments. The Malaysia Data Center Storage Market shows strong demand for SAN systems in centralized data center environments.

By Component

Hardware dominates the market due to large infrastructure rollouts by telecoms and cloud providers. Software is gaining traction with the rise of software-defined storage solutions. Enterprises are investing in storage virtualization and orchestration tools to enhance flexibility. The Malaysia Data Center Storage Market continues to rely on robust hardware foundations, but software is enabling advanced functionalities.

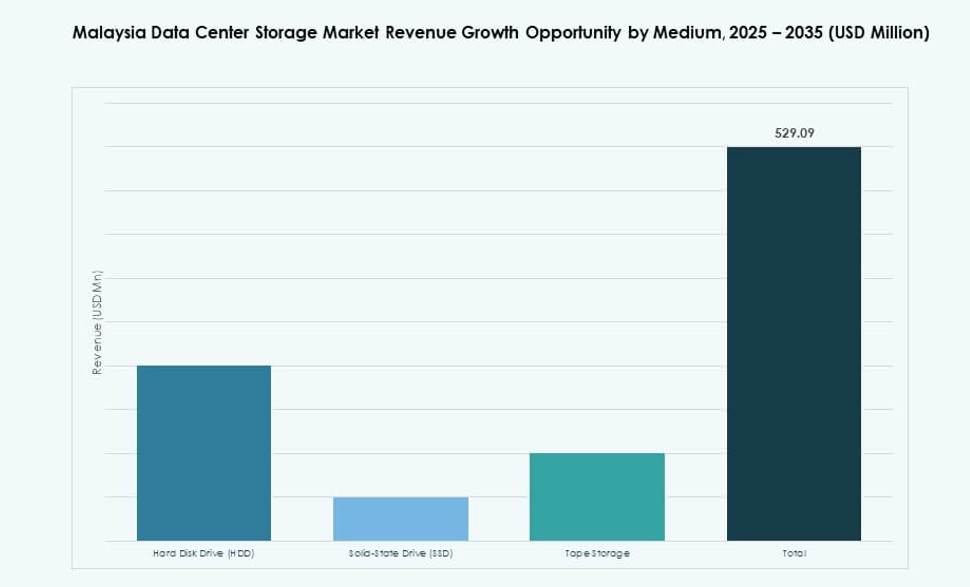

By Medium

Solid-State Drives (SSD) are driving growth due to their high throughput and declining cost per GB. HDD remains relevant for archival and backup storage needs. Tape storage is used by select government and media organizations for long-term cold storage. The Malaysia Data Center Storage Market reflects increasing SSD adoption across performance-intensive applications.

By Deployment Model

Cloud-based deployment leads the segment due to demand for scalable, low-maintenance storage options. Hybrid models are growing in compliance-heavy sectors. On-premises deployments remain steady among government agencies and regulated industries. The Malaysia Data Center Storage Market shows strong hybrid cloud traction in financial services and public sector.

By Application

IT and telecommunications hold the largest share, driven by mobile data growth and service digitization. BFSI follows, with rising demand for secure and compliant data retention. Government and healthcare are expanding storage footprints for digital services and health records. The Malaysia Data Center Storage Market supports these verticals with specialized infrastructure and services.

Regional Insights

Central Region (Kuala Lumpur, Cyberjaya, Selangor) – 58% Market Share

The Central region leads the Malaysia Data Center Storage Market with over half of the national share. Cyberjaya and Selangor host many of the country’s Tier III and Tier IV facilities. Connectivity, government support, and skilled workforce drive concentration here. Enterprises choose this region for compliance-ready infrastructure and vendor availability. It serves as the backbone for both domestic and regional storage services.

- For instance, TM One’s Klang Valley Core Data Centre (KVDC) in Cyberjaya is certified by Uptime Institute as a Tier III facility and holds PCI DSS and ISO/IEC 27001 certifications, positioning it as a compliance-ready hub for enterprise workloads in the central region.

Southern Region (Johor, Melaka) – 26% Market Share

Johor is rapidly emerging due to its proximity to Singapore and dedicated data center parks. Investors leverage low land cost, power availability, and economic incentives in this corridor. It is becoming a preferred backup and disaster recovery location. Storage platforms in Johor often support cross-border and regional operations. The Malaysia Data Center Storage Market sees Johor as the fastest-growing subregion.

Northern and East Malaysia (Penang, Sarawak, Sabah) – 16% Market Share

Northern Malaysia, particularly Penang, is witnessing steady adoption from electronics and manufacturing firms. East Malaysia, including Sarawak and Sabah, lags in infrastructure but is gaining attention for edge deployments. Government projects and rural digitization are expanding demand in these regions. Connectivity challenges limit large-scale deployments but open niche edge storage opportunities. The Malaysia Data Center Storage Market sees these areas as emerging zones for future development.

- For instance, Open DC’s PE2 data center in Penang, launched in April 2025, is the state’s first large-scale next-generation facility with an initial IT load of 10 MW, scalable to 30 MW. Located in Bayan Lepas Technology Park, it supports high-performance workloads including AI and machine learning.

Competitive Insights:

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- IBM Corporation

- NetApp

- Huawei Technologies Co., Ltd.

- Cisco Systems, Inc.

- AIMS Data Centre

- TM One

- Cohesity, Inc.

- Bridge Data Centres

The Malaysia Data Center Storage Market features strong competition between global storage hardware leaders and regional infrastructure players. Dell Technologies, HPE, IBM, and NetApp dominate in enterprise deployments across BFSI, telecom, and government verticals. Huawei and Cisco enhance competitiveness through integrated networking and storage offerings. Local data center operators like AIMS Data Centre and TM One support cloud and hybrid deployments through colocation and managed storage services. Partnerships and cloud alliances shape the vendor landscape, with new investment coming from hyperscale players and telecom-backed ventures. The market favors vendors offering modular, secure, and scalable solutions across both public and private clouds. It continues to shift toward software-defined platforms and high-performance SSD-based infrastructure as demand accelerates across compliance-heavy and AI-driven workloads.

Recent Developments:

- In March 2025, Microsoft stated that it would launch its first Malaysia cloud region with three data centers by Q2 2025, a move intended to support rising regional needs for cloud storage, data residency, and AI services, thereby boosting the country’s data center storage footprint.

- In October 2024, Google announced a US$2 billion investment to build its first data center and Google Cloud region in Malaysia at Elmina Business Park, Selangor, aimed at supporting growing demand for cloud services, AI workloads, and data-intensive applications,

- In July 2024, AIMS Data Centre announced the launch of its new Bangunan AIMS (KL2) data center in Kuala Lumpur, adding 7.5 MW of capacity and expanding colocation and managed services to support Malaysia’s growing cloud and storage workloads.