Executive summary:

The Indonesia Data Center Storage Market size was valued at USD 1,203.49 million in 2020 to USD 2,233.77 million in 2025 and is anticipated to reach USD 5,168.74 million by 2035, at a CAGR of 8.66% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Indonesia Data Center Storage Market Size 2025 |

USD 2,233.77 Million |

| Indonesia Data Center Storage Market, CAGR |

8.66% |

| Indonesia Data Center Storage Market Size 2035 |

USD 5,168.74 Million |

The market is growing due to increased cloud adoption, government-led digitalization, and expansion of fintech and e-commerce platforms. Enterprises are shifting from legacy systems to hybrid and software-defined storage to handle massive unstructured data. Rising deployment of AI and IoT applications is driving demand for scalable and low-latency storage solutions. Storage innovation is central to business continuity, security, and performance. Investors see long-term opportunity in high-density, sustainable infrastructure. Regulatory frameworks on data localization also influence purchasing and deployment decisions.

Jakarta remains the dominant hub due to its infrastructure, connectivity, and concentration of hyperscale and enterprise data centers. Batam, Surabaya, and Bandung are emerging due to subsea cable access, land availability, and regional enterprise demand. These regions benefit from government incentives and rising edge storage deployments. Outside Java, infrastructure gaps slow expansion but offer potential for localized modular deployments and digital inclusion strategies.

Market Dynamics:

Market Drivers

Surge in Data Generation from E-Commerce, Fintech, and Social Media Ecosystems Across Urban Centers

Indonesia’s digital economy has grown rapidly due to the expansion of e-commerce platforms, mobile banking, and digital wallets. These activities generate vast amounts of structured and unstructured data. Large volumes of transactional and consumer behavior data demand advanced storage infrastructure. Companies require fast, reliable systems that offer low-latency access. The Indonesia Data Center Storage Market addresses these needs through purpose-built solutions. It supports enterprises transitioning from traditional IT setups to cloud-based models. Market growth aligns with rising internet penetration across urban hubs. Continuous digital services adoption across Jakarta, Bandung, and Surabaya further supports storage demand. National strategies also encourage digital infrastructure investments.

- For instance, Tokopedia serves over 100 million monthly active users, making it one of Indonesia’s largest digital commerce platforms. The scale of user activity generates very high volumes of transactional and behavioral data. This operating scale underscores the need for robust, scalable data storage and cloud infrastructure to support peak traffic periods.

Enterprise and Government Cloud Migration Fueling Storage Infrastructure Modernization Projects

Private and public organizations are shifting to cloud-based storage to support digital transformation efforts. Government-backed initiatives under the Digital Indonesia vision prioritize modernization of IT architecture. Critical sectors like healthcare, education, and governance are adopting hybrid and private clouds. These shifts increase demand for scalable and secure storage technologies. Storage infrastructure upgrades help streamline workflows and enable real-time data analysis. The Indonesia Data Center Storage Market benefits from public-sector digitization, especially in smart city deployments. Cloud-centric infrastructure reduces cost while increasing accessibility. Organizations across all sizes are also investing in disaster recovery and business continuity solutions. These transitions enhance market growth prospects.

- For instance, Indonesia’s Ministry of Finance has undertaken data center modernization efforts to improve digital governance. These include consolidating legacy systems and upgrading to a smarter IT infrastructure to enhance fiscal data management and service efficiency.

Growth of Edge Storage Demand Driven by Smart Cities, IoT, and Real-Time Data Applications

Urbanization and smart city initiatives require edge computing to reduce latency and enable local processing. Applications such as intelligent traffic systems, remote healthcare, and smart grids produce data close to end-users. Edge storage solutions reduce the burden on central data centers while improving responsiveness. Telecom operators are expanding their edge node footprints to serve low-latency use cases. The Indonesia Data Center Storage Market supports these deployments with compact, ruggedized, and scalable edge storage units. Real-time analytics, video surveillance, and autonomous systems also rely on decentralized data storage. Growth of industrial IoT and connected devices in manufacturing zones boosts demand. Edge-based architecture complements centralized data storage for high-efficiency operations.

Regulatory Push for Data Sovereignty and Domestic Infrastructure Enhancing Local Storage Investments

Indonesia mandates local storage of sensitive data through data sovereignty laws. These regulations create new opportunities for domestic data centers and cloud providers. Enterprises must invest in compliant infrastructure that stores and manages data within national borders. The Indonesia Data Center Storage Market has responded by scaling in-country capacity and enhancing cybersecurity standards. Government certifications and tax incentives accelerate local facility development. Global cloud providers such as Google, AWS, and Microsoft are also setting up local zones. This localization ensures better service delivery and regulatory compliance. It increases demand for secure, tiered storage platforms across industries. Strong legal frameworks strengthen investor confidence in the Indonesian digital economy.

Market Trends

Rising Adoption of All-Flash Storage Systems in High-Performance Enterprise Workloads

Enterprises are replacing legacy spinning disks with flash-based systems for better speed and reliability. All-flash arrays deliver superior IOPS performance required by analytics, AI/ML, and virtualization workloads. Financial services and telecom sectors demand consistent low-latency response. The Indonesia Data Center Storage Market is witnessing a shift from HDDs to SSDs in performance-critical applications. Energy-efficient flash systems also reduce operational costs. Storage refresh cycles favor modern infrastructure upgrades. Flash vendors offer tailored solutions for midsize businesses and hyperscalers. Improved cost per gigabyte makes adoption more feasible. Tiered storage models integrate flash for hot data and traditional drives for cold data.

Shift Toward Software-Defined Storage to Enable Scalability and Vendor-Neutral Architectures

Software-defined storage (SDS) decouples software control from physical hardware, offering agility and scalability. SDS platforms enable enterprises to manage multi-vendor environments and avoid vendor lock-in. Cloud-native businesses prefer SDS for flexible capacity provisioning. The Indonesia Data Center Storage Market supports this shift through local and global SDS offerings. Kubernetes-based environments and container storage interfaces are gaining traction. SDS enhances storage automation, policy enforcement, and hybrid deployment. Startups and managed service providers use SDS to lower capital costs. Enterprise IT teams deploy SDS across on-premises, cloud, and edge nodes. This trend accelerates modernization of traditional data centers.

Increased Investments in Green Data Center Storage Infrastructure with Low Power and Cooling Demand

Energy efficiency has become a key decision factor in storage infrastructure selection. Enterprises and colocation providers seek storage systems that optimize space and power usage. Liquid cooling, intelligent tiering, and energy-efficient drives are gaining preference. The Indonesia Data Center Storage Market is experiencing growing demand for storage hardware with minimal heat generation. New facilities are designed for low PUE (power usage effectiveness) values. ESG mandates and green certifications also influence procurement strategies. Vendors focus on recyclable components and carbon-neutral operations. Smart power management improves reliability and reduces total cost of ownership. Sustainability-linked infrastructure attracts impact-focused investors.

Proliferation of Hybrid Storage Architectures for Workload-Specific Optimization Across Sectors

Hybrid storage combines flash and traditional drives to balance performance and cost. Organizations are increasingly segmenting workloads into hot, warm, and cold data categories. This approach allows faster access to mission-critical data and cost-efficient storage for archival content. The Indonesia Data Center Storage Market offers hybrid solutions tailored to sectors like healthcare, retail, and logistics. Workload-optimized storage aligns with application lifecycle needs. AI-based analytics enhance data tiering and migration. Hybrid models support multi-site and hybrid cloud strategies. Adoption rises in compliance-driven industries handling large datasets. These systems bridge the gap between legacy storage and full flash upgrades.

Market Challenges

High Cost of Infrastructure Deployment and Limited Access to Skilled Workforce

Deploying advanced storage systems involves substantial upfront investment in hardware, software, and physical infrastructure. High real estate and electricity costs in core regions raise barriers for new entrants. Many domestic firms hesitate to modernize due to capital constraints. Recruiting and retaining IT professionals skilled in software-defined and hybrid storage remains a challenge. The Indonesia Data Center Storage Market needs ongoing workforce training and education to bridge this skills gap. Shortages in cloud architecture, cybersecurity, and storage optimization reduce operational efficiency. Enterprises must balance cost with performance while building future-ready systems. Imported equipment also faces customs delays and taxation complexities.

Fragmented Regional Infrastructure and Connectivity Gaps Impact Uniform Market Growth

Beyond major metros, secondary and tertiary cities face limited digital infrastructure and unstable connectivity. Inadequate fiber coverage and unreliable power supply restrict edge and cloud expansion. The Indonesia Data Center Storage Market sees uneven growth across islands due to these disparities. Rural and remote regions often rely on slow networks and lack localized storage options. This imbalance limits access to modern applications and latency-sensitive services. Building edge nodes in such regions requires government and private sector collaboration. Operators must invest in robust site assessments, redundant connectivity, and modular designs. Infrastructure bottlenecks delay service rollout and reduce user satisfaction.

Market Opportunities

Expansion of Local Manufacturing, Fintech, and Digital Health Driving Custom Storage Needs

Indonesia’s digital-first industries demand secure, high-throughput storage tailored to each sector. Fintechs require encrypted transaction storage, while manufacturers seek real-time sensor data processing. Telemedicine platforms need scalable image archiving and retrieval. The Indonesia Data Center Storage Market supports these sectors with domain-specific storage architecture. Customization ensures regulatory compliance and data integrity. Growth in sectoral cloud adoption opens new product categories and service models.

Emergence of Indonesia as a Regional Data Center Hub in Southeast Asia

Indonesia’s central geography and large user base offer a strategic edge in Southeast Asia. Global hyperscalers and regional players plan new facilities in Batam, Bekasi, and Surabaya. Favorable policies, undersea cable access, and renewable energy options make the country attractive. The Indonesia Data Center Storage Market will benefit from these developments through rising demand for storage integration, migration, and backup solutions. Localized capacity boosts resilience and service availability.

Market Segmentation

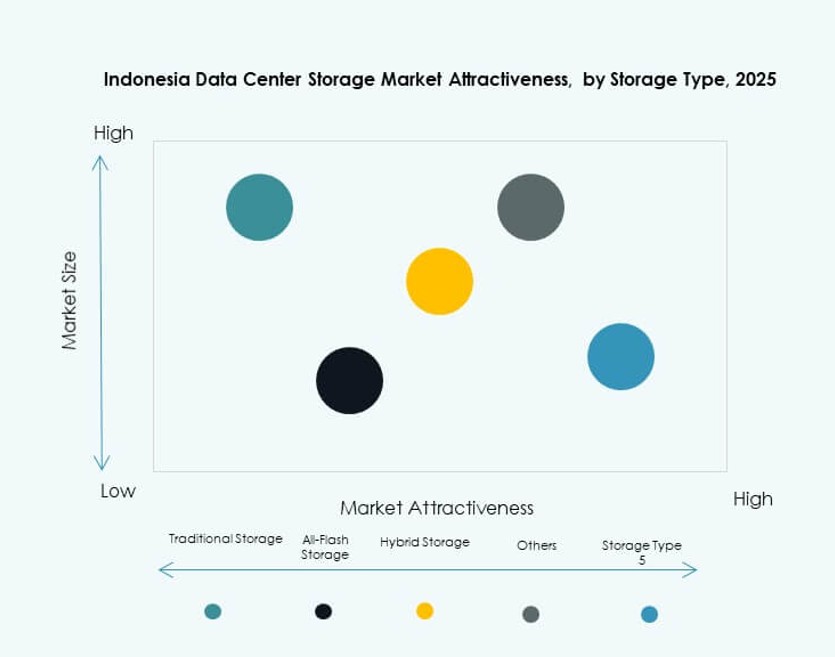

By Storage Type

The Indonesia Data Center Storage Market is dominated by hybrid storage solutions, offering a balance between speed and cost. Enterprises adopt hybrid models to optimize workloads across flash and disk environments. All-flash storage adoption is growing in high-performance sectors like BFSI and telecom. Traditional storage remains relevant in cold data applications, while emerging types address edge storage needs. Vendors offer flexible combinations to meet varying performance and budget requirements.

By Storage Deployment

Storage Area Network (SAN) systems lead the Indonesia Data Center Storage Market due to their reliability in handling mission-critical workloads. SAN is widely deployed in enterprise data centers and large-scale cloud environments. NAS systems are gaining traction among SMBs and content-heavy applications. DAS systems are used for localized storage but have limited scalability. New entrants experiment with software-defined deployment for agility and centralized management.

By Component

Hardware holds the majority share in the Indonesia Data Center Storage Market, driven by continuous upgrades and facility expansion. Enterprises invest in scalable drives, switches, and servers for capacity and performance. Software is growing fast, led by SDS, data deduplication, and backup management platforms. Software innovations allow centralized control and hybrid deployment flexibility. Integration of AI and automation in storage software adds to its value.

By Medium

Hard Disk Drives (HDDs) dominate storage volume in archival and cold data use cases, offering cost efficiency at scale. Solid-State Drives (SSDs) are growing fast due to performance advantages in transactional and analytics workloads. Tape storage remains niche, used in archival setups requiring high durability. Vendors provide hybrid media solutions for better tiering and lifecycle management. Enterprises optimize costs using mixed storage media across workloads.

By Deployment Model

On-premises deployment remains significant in regulated sectors like finance and government due to compliance needs. Cloud-based models are gaining momentum with flexible capacity and remote access. Hybrid deployment is the fastest-growing model in the Indonesia Data Center Storage Market. Organizations use hybrid setups to manage sensitive data on-premises and leverage cloud for scalability. Deployment decisions depend on security, workload type, and cost considerations.

By Application

IT and telecommunications lead the Indonesia Data Center Storage Market, driven by digital service expansion and user data growth. BFSI follows closely, requiring high-speed, encrypted storage for financial records. Government adoption grows due to e-governance and public sector digitalization. Healthcare shows increasing demand for imaging and records storage. Other sectors like education, logistics, and retail also contribute to market diversification.

Regional Insights

Jakarta and Surrounding Metro Region Hold Over 55% Market Share Due to Dense Digital Activity

Jakarta dominates the Indonesia Data Center Storage Market due to its concentration of hyperscale, enterprise, and cloud providers. High population density, advanced digital infrastructure, and enterprise demand boost market share. Surrounding cities such as Bekasi and Tangerang attract colocation and managed service expansions. The capital region offers superior connectivity and reliable power supply. Government support for smart city initiatives further accelerates infrastructure build-out. International vendors prefer Jakarta for regional access and network latency advantages.

- For instance, NTT’s Jakarta 3 data center in Bekasi is a purpose-built four‑story facility with approximately 18,000 square meters of IT space and about 15.2 megawatts of initial IT capacity, designed to scale toward around 45 megawatts on the campus, supporting hyperscale and cloud workloads in Greater Jakarta

Batam, Surabaya, and Bandung Emerge as Secondary Hubs with 25% Market Share Combined

Batam leverages its proximity to Singapore and strategic position in international submarine cable routes. It hosts international operators building hyperscale and modular data centers. Surabaya and Bandung attract enterprise and cloud investments from regional industries. Their growing tech ecosystems and skilled workforce enhance regional storage capacity. These cities serve as disaster recovery and secondary hosting locations. The Indonesia Data Center Storage Market sees balanced expansion in these emerging corridors, boosting nationwide availability.

- For instance, Batam is directly connected to multiple international submarine cable systems that link Indonesia and Singapore, enabling low‑latency routes that support hyperscale and colocation facilities operated by regional and global providers on the island.

Rest of Java, Sumatra, and Eastern Indonesia Represent 20% Market Share but Face Infrastructure Gaps

Regions beyond the primary metros experience slower growth due to limited connectivity and power infrastructure. Java’s smaller cities show incremental demand from SMEs and public-sector deployments. Sumatra and eastern islands depend on edge nodes and modular systems. Market penetration remains low but shows potential due to rising mobile internet and e-governance programs. The Indonesia Data Center Storage Market supports gradual digitization in these areas with scalable and decentralized solutions. Investment in backbone infrastructure will improve regional inclusion.

Competitive Insights:

- DCI Indonesia

- Telkomsigma

- Nusantara Data Center

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- NetApp

- IBM Corporation

- Huawei Technologies Co., Ltd.

- Hitachi Vantara

- Cisco Systems, Inc.

The Indonesia Data Center Storage Market is defined by a blend of local data center providers and global storage technology leaders. DCI Indonesia, Telkomsigma, and Nusantara Data Center lead in domestic infrastructure and managed services, leveraging proximity to customers and regulatory compliance. Global players like Dell Technologies, HPE, and IBM offer scalable storage systems for enterprise and hyperscale use. NetApp, Hitachi Vantara, and Huawei focus on hybrid and flash-based deployments. It remains competitive due to rapid infrastructure expansion, government digitization programs, and high demand from cloud-native sectors. Vendors differentiate through automation, SDS platforms, and high-efficiency storage arrays. Strategic partnerships, ESG-linked investments, and service customization define leadership positions in this dynamic market.

Recent Developments:

- In July 2025, Anaplan announced the launch of a new data center in Indonesia to bring its planning and analytics services closer to local customers. The facility offers improved data performance, lower latency, and stronger security for Indonesian businesses.

- In March 2025, Digital Realty entered the Indonesian market by forming a 50‑50 joint venture with Bersama Digital Infrastructure Asia (BDIA). The new entity, Digital Realty Bersama, now owns and operates data center campuses in Jakarta, including CGK10 and the newly launched CGK11 facility.