Executive summary:

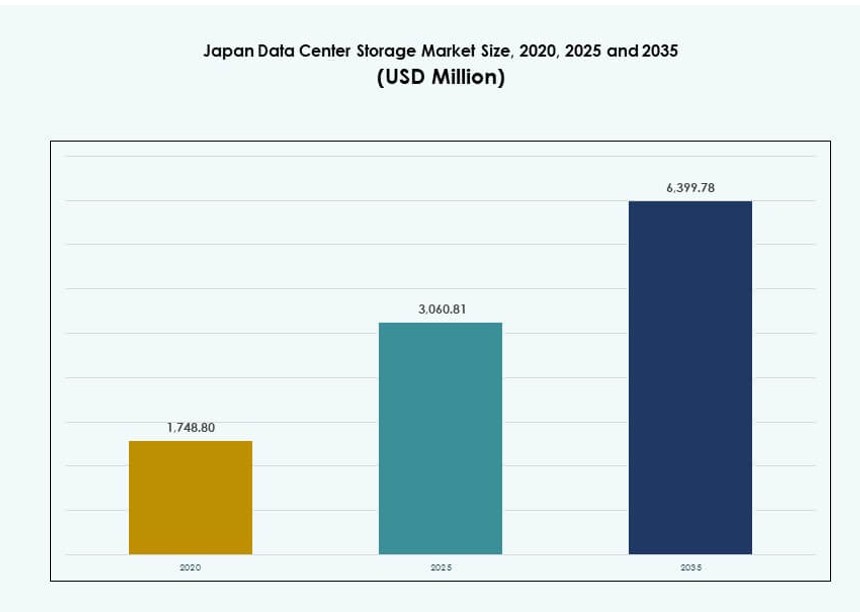

The Japan Data Center Storage Market size was valued at USD 1,748.80 million in 2020 to USD 3,060.81 million in 2025 and is anticipated to reach USD 6,399.78 million by 2035, at a CAGR of 7.57% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Japan Data Center Storage Market Size 2025 |

USD 3,060.81 Million |

| Japan Data Center Storage Market, CAGR |

7.57% |

| Japan Data Center Storage Market Size 2035 |

USD 6,399.78 Million |

Rising demand for cloud-native applications, AI workloads, and edge computing is reshaping enterprise storage strategies in Japan. Businesses are investing in all-flash arrays, software-defined storage, and NVMe solutions to improve speed and scalability. Regulatory focus on data localization and cybersecurity is influencing storage infrastructure decisions. Enterprises seek hybrid models that combine cloud agility with on-premise control. These shifts position the storage market as vital to Japan’s digital competitiveness and long-term innovation.

Tokyo leads the market due to its dense network hubs, strong enterprise base, and hyperscale cloud availability. Osaka follows as a disaster recovery zone and a growing secondary hub. Regional cities like Fukuoka and Sapporo are emerging with government-backed smart infrastructure and lower-cost development. These trends highlight geographic diversification and growing demand for localized, resilient storage across Japan.

Market Dynamics:

Market Drivers

Adoption of High-Density Storage Architectures to Support Edge and AI Workloads

The Japan Data Center Storage Market is driven by the rapid shift toward high-density and scalable storage systems. Edge computing expansion and AI workloads demand real-time data handling with low latency. Enterprises deploy high-throughput storage solutions to manage this transformation. Flash arrays and NVMe-based systems are increasingly replacing legacy architectures. Integration with AI processors and GPUs is becoming standard. These shifts enhance performance and reduce response time for critical services. The market benefits from Japan’s tech-driven economy and early adoption culture. Investors view storage infrastructure as key to enabling next-gen digital applications. It opens recurring revenue models via managed services and hybrid cloud.

Government Push for Digital Transformation Fuels Enterprise Storage Expansion

National policies like Japan’s “Digital Garden City” strategy and smart infrastructure investments support accelerated IT upgrades. Government data initiatives require high-volume, high-availability storage infrastructure. Local governments and ministries are enhancing disaster recovery and data backup protocols. This elevates demand for software-defined and multi-site storage clusters. Public-private partnerships boost regional colocation and cloud expansions. Storage vendors benefit from procurement in healthcare, transport, and education sectors. Japan Data Center Storage Market reflects this national digital focus. It aligns with cybersecurity mandates and sovereignty goals. Enterprises leverage compliant infrastructure to meet evolving legal standards.

- For instance, AT Tokyo’s data center facility supports high-density configurations up to 20kVA per rack with remote monitoring capabilities.

Cloud-Native Workloads Drive Hybrid and Multi-Cloud Storage Demand

Organizations are embracing hybrid cloud and multi-cloud setups to enhance agility and reduce vendor lock-in. This shift fuels growth in object-based storage and cloud-integrated storage systems. Cloud-native architectures demand seamless data movement across platforms. Japanese enterprises prioritize integration with AWS Tokyo, Azure Japan East, and Google Cloud Tokyo regions. Data sovereignty and latency concerns drive preference for in-country deployments. Japan’s cloud ecosystem supports storage APIs, analytics, and orchestration platforms. Japan Data Center Storage Market aligns with evolving enterprise IT strategies. Vendors offering open, container-friendly systems gain share. Investors favor firms addressing cross-platform interoperability and backup assurance.

Surge in Video Surveillance and IoT Applications Expands Storage Needs

IoT networks and smart city deployments are generating massive volumes of unstructured data. High-resolution video surveillance, traffic monitoring, and environmental sensors increase storage requirements. Japanese firms deploy tiered storage systems to manage cost and performance. Cold storage and tape libraries remain relevant for long-term archiving. Enterprises need fast-access storage for AI analytics and real-time alerts. Media, logistics, and retail sectors lead adoption. Japan Data Center Storage Market reflects rising sector-specific deployments. It attracts investments in modular storage and edge-ready designs. Businesses demand scalable capacity to handle growth without frequent system overhauls.

- For instance, Hitachi provides high-performance storage systems for video surveillance, enabling scalable management of large video footage volumes.

Market Trends

Rise of AI-Optimized Storage Infrastructure Tailored for GPU Workloads

Storage solutions designed for AI and ML processing are gaining traction. These systems focus on low latency, parallel data access, and high bandwidth. Enterprises integrate storage with NVIDIA DGX, AMD MI, or Google TPU environments. Japan Data Center Storage Market supports this shift with AI training clusters and inference zones. NVMe-over-Fabrics and scale-out file systems replace legacy setups. Vendors promote AI-specific storage appliances with on-device compute features. This trend benefits sectors such as robotics, finance, and genomics. Storage performance becomes a key metric in AI strategy execution. Data centers optimize architecture around compute–storage proximity.

Deployment of Green Storage Infrastructure in Support of Net-Zero Goals

Sustainability is reshaping procurement and deployment strategies for storage infrastructure. Enterprises prioritize energy-efficient storage arrays with intelligent cooling. Japan Data Center Storage Market sees a rise in carbon-aware operations and storage lifecycle management. Facilities choose low-power SSDs, eco-tape libraries, and automated power-down features. Regulatory pressure encourages ESG-aligned infrastructure adoption. Renewable-powered storage zones emerge in Northern Japan. Storage vendors offer carbon footprint dashboards and predictive energy analytics. Data centers partner with utilities to offset emissions. Green financing supports eco-aligned upgrades. Sustainability becomes a core parameter in storage procurement decisions.

Integration of Quantum-Resistant Storage Encryption and Security Protocols

Security concerns push demand for encrypted storage systems capable of resisting future quantum attacks. Japan Data Center Storage Market integrates post-quantum encryption and immutable storage systems. Financial, healthcare, and defense sectors prioritize tamper-proof backups and end-to-end encryption. Storage firmware undergoes tighter audits and regular patching. Hardware security modules (HSMs) are increasingly embedded in storage controllers. Multi-factor access and zero-trust principles shape access control. Vendors differentiate through NIST-aligned compliance and threat detection tools. This trend aligns with Japan’s national cyber resilience strategy. Secure storage becomes vital to ensuring data integrity across hybrid deployments.

Shift Toward AI-Driven Storage Management and Predictive Analytics

AI and ML are embedded into storage management platforms for workload forecasting and automated performance tuning. Japan Data Center Storage Market leverages this trend to reduce operational complexity and unplanned downtime. AI systems predict drive failures, optimize IOPS distribution, and suggest capacity expansion. Storage-as-a-Service (STaaS) platforms gain adoption with smart tiering and usage-based billing. Enterprises prefer vendors offering AI-enabled dashboards and autonomous provisioning. This trend boosts efficiency in resource allocation and energy usage. It supports service-level objectives with fewer human interventions. AI-driven tools become essential for managing petabyte-scale environments.

Market Challenges

High Real Estate and Energy Costs in Core Data Center Regions

Land scarcity and high power tariffs in major cities such as Tokyo and Osaka limit capacity expansion. Storage providers face constraints in expanding footprint due to premium costs. Japan Data Center Storage Market must address this by pursuing vertical construction and modular rack designs. Power purchase agreements for renewable sources face grid limitations. Government incentives are limited in high-demand zones. Complex zoning laws and seismic risk add to development hurdles. Enterprises consider shifting storage nodes to suburban or rural sites. High costs affect ROI calculations for both hyperscale and mid-sized players. Balancing performance with cost remains a critical challenge.

Legacy IT Ecosystems Limit Full Migration to Advanced Storage Models

Many enterprises still rely on legacy systems with rigid architectures and siloed storage pools. Japan Data Center Storage Market growth is slowed by compatibility issues during cloud or flash transitions. Migration involves complex data mapping, downtime risks, and user retraining. IT teams lack expertise in container storage and cloud orchestration. Budget constraints delay replacement cycles. Vendors struggle to integrate old systems with software-defined storage platforms. This slows hybrid model adoption across key industries. Regulatory compliance adds another layer of complexity. The transition to modern storage models remains uneven across sectors.

Market Opportunities

Edge Storage Demand Grows in Support of 5G and Localized Compute

The expansion of 5G and smart infrastructure boosts demand for edge-native storage systems. Japan Data Center Storage Market can capture this opportunity by offering rugged, low-latency, and compact storage appliances. Industrial zones, smart campuses, and IoT clusters require real-time data access and retention at the edge. Vendors gain share by offering interoperable edge–core–cloud storage ecosystems. Local governments back infrastructure upgrades with regional grants.

AI-Driven Content Platforms Create Need for Scale-Out Object Storage

Streaming, gaming, and content creation sectors require massive, flexible, and cost-efficient storage models. Japan Data Center Storage Market benefits from the need for petabyte-scale object storage with fast retrieval speeds. Companies offering platform-integrated APIs and high-throughput storage gain a competitive edge. Demand is growing for vendor-neutral storage that scales without performance loss.

Market Segmentation

By Storage Type

Traditional storage continues to hold a significant share in the Japan Data Center Storage Market, driven by long-term IT setups in legacy sectors. However, all-flash storage is rapidly expanding, thanks to its speed and efficiency in handling AI workloads. Hybrid storage solutions gain momentum among mid-sized enterprises aiming for cost-performance balance. Growth is supported by vendors offering flexible storage tiering for dynamic data requirements.

By Storage Deployment

Network-attached storage (NAS) systems dominate deployment due to their scalability and shared access benefits. Japan Data Center Storage Market sees strong growth in SAN systems for mission-critical applications, especially in finance and government. Direct-attached storage (DAS) remains relevant in localized environments. Enterprises increasingly deploy multi-layered architectures combining SAN and NAS systems for redundancy and performance.

By Component

Hardware remains the dominant component in the Japan Data Center Storage Market, reflecting ongoing investment in physical infrastructure. SSDs and advanced storage arrays contribute to high capital allocation in hardware. Software is gaining momentum through storage virtualization, orchestration, and backup management tools. Growth in software-defined storage supports agility and reduces vendor lock-in across hybrid environments.

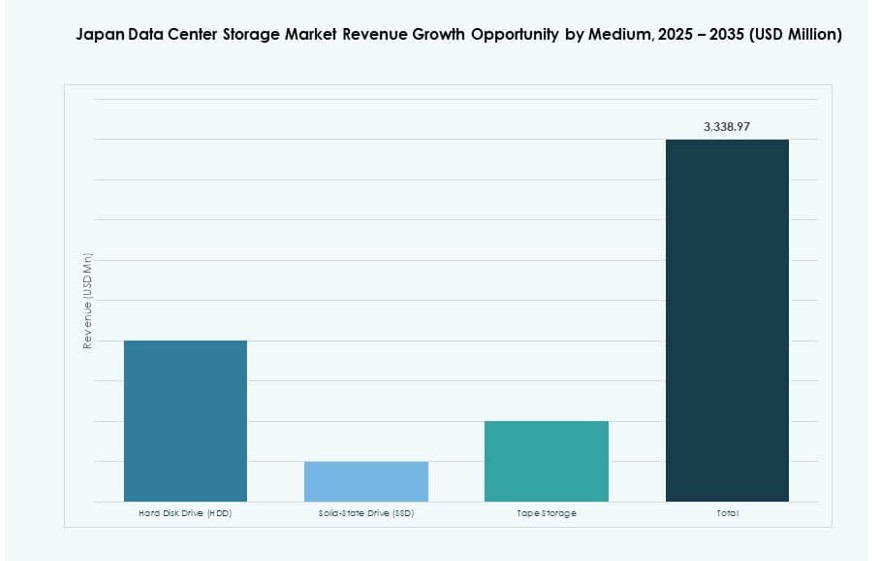

By Medium

Solid-state drives (SSD) lead due to their performance and falling cost per GB. Japan Data Center Storage Market also retains use of hard disk drives (HDDs) in backup and archival storage due to affordability. Tape storage sees renewed interest in cold storage applications, particularly in compliance-heavy industries. Enterprises blend all three to build tiered and cost-efficient storage models.

By Deployment Model

Cloud-based storage is growing rapidly, driven by SaaS models and remote work trends. On-premises deployments still hold value in sectors requiring high control and security. Hybrid models are increasingly preferred to balance agility with compliance. Japan Data Center Storage Market reflects this shift with vendor offerings that span across deployment modes.

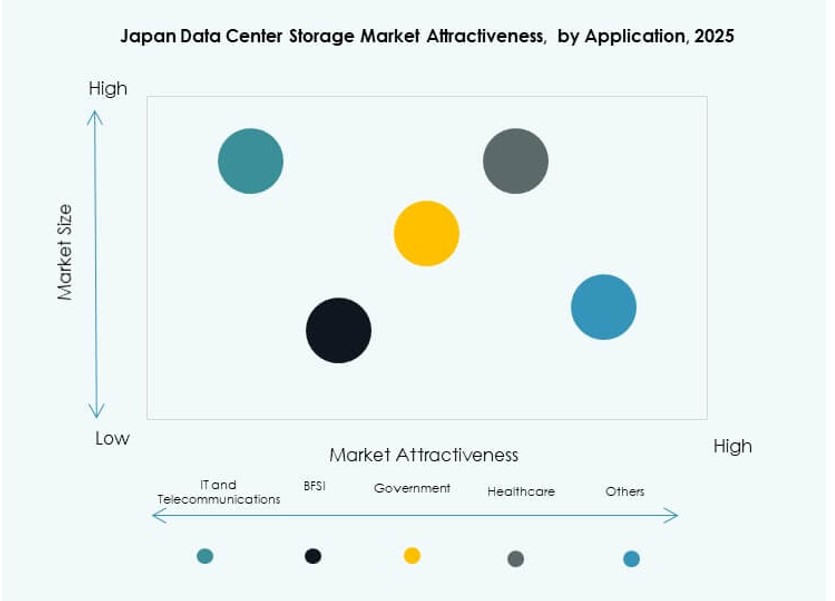

By Application

IT and telecommunications lead application demand, followed by BFSI and government sectors. These industries require high-availability, low-latency storage environments. Healthcare and research are emerging as key growth areas due to increased data complexity and regulation. Japan Data Center Storage Market benefits from sectoral digitization and regulatory storage mandates across verticals.

Regional Insights

Greater Tokyo Region Holds Over 55% Market Share Due to Density and Connectivity

Tokyo remains the dominant region in the Japan Data Center Storage Market, accounting for over 55% share. It hosts key colocation hubs, financial institutions, and hyperscale availability zones. The area benefits from dense fiber networks, skilled workforce, and proximity to customers. Real estate scarcity and power constraints challenge future expansions, prompting vertical builds and repurposed urban sites. Vendors prioritize Tokyo for premium storage offerings and enterprise-grade reliability.

- For instance, NTT’s Tokyo 10 Data Center provides space capacity for approximately 5,600 racks with a maximum power receiving of 40,000kVA from three different substations.

Kansai Region (Osaka) Accounts for 20% with Disaster Resilience and Cloud Expansion

The Kansai region, centered on Osaka, represents about 20% of the Japan Data Center Storage Market. It serves as a disaster recovery and secondary site for many Tokyo-based firms. Osaka benefits from growing public cloud footprints and grid reliability. Hyperscale providers like Microsoft and AWS expand their presence in the region. The area’s regulatory flexibility and power stability support regional storage growth. Local governments promote digital infrastructure through economic zone policies.

- For instance, AirTrunk is expanding its hyperscale footprint in Osaka to support rising AI and cloud workloads. Hokkaido continues to attract data center providers seeking renewable power access and cooler climates that enable low-PUE operations.

Hokkaido, Fukuoka, and Other Emerging Regions Share 25% with Niche and Localized Demand

Northern and southern regions collectively hold 25% of the Japan Data Center Storage Market. Hokkaido appeals to providers seeking green power and cooler climates for low PUE. Fukuoka sees enterprise interest due to cross-border proximity with Asia and growing tech adoption. These regions offer land availability and regional incentives. Data centers in these zones serve regional governments, SMBs, and content firms. Growth depends on better subsea connectivity and workforce expansion.

Competitive Insights:

- Fujitsu Limited

- NEC Corporation

- Hitachi Vantara

- Toshiba Corporation

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- NetApp

- IBM Corporation

- Huawei Technologies Co., Ltd.

- Micron Technology, Inc.

The Japan Data Center Storage Market features strong competition between global technology leaders and domestic incumbents. Fujitsu, NEC, Hitachi, and Toshiba dominate the local ecosystem with deep integration into enterprise and government IT. Global players such as Dell Technologies, HPE, and IBM focus on hybrid deployments and smart storage management. NetApp and Huawei compete in flash storage and cloud-integrated systems. Vendors invest in NVMe, software-defined storage, and AI-driven orchestration to gain a technical edge. Partnerships with hyperscalers and regional cloud providers shape long-term positioning. It favors players offering secure, low-latency, and energy-efficient infrastructure aligned with Japan’s digital transformation roadmap.

Recent Developments:

- In November 2025, NEC Corporation expanded its strategic partnership with Broadcom focusing on modern infrastructure adoption relevant to data center advancements in Japan. The partnership emphasizes joint efforts in cloud and AI-driven services, aligning with Japan’s data center storage ecosystem growth.

- In September 2025, Keppel DC Reit purchased a Tokyo data center for $707 million. This acquisition marks the REIT’s second data center addition in Japan, expected to boost earnings immediately amid rising AI-driven demand for infrastructure in the Asia-Pacific region.

- In May 2025, NEC Corporation strengthened its strategic partnership with IFS to enhance cloud services in Japan, including building a secure cloud environment at NEC’s Inzai Data Center for IFS Cloud ERP deployment.

- In March 2025. Mitsui & Co. acquired a 20MW hyperscale data center in Japan’s Kanagawa prefecture. In this deal, Mitsui invested 18 billion yen ($121 million) through its subsidiary Mitsui & Co. Realty Management, taking a 50% stake alongside institutional investors, as a seed asset for a new digital infrastructure fund aimed at expanding its data center business.