Executive summary:

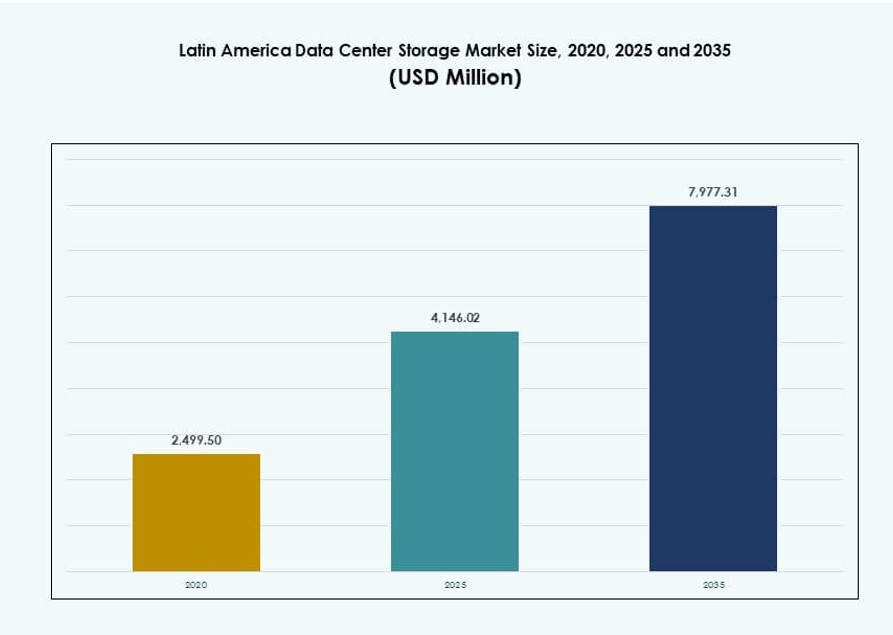

The Latin America Data Center Storage Market size was valued at USD 2,499.50 million in 2020 to USD 4,146.02 million in 2025 and is anticipated to reach USD 7,977.31 million by 2035, at a CAGR of 6.70% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Latin America Data Center Storage Market Size 2025 |

USD 4,146.02 Million |

| Latin America Data Center Storage Market, CAGR |

6.70% |

| Latin America Data Center Storage Market Size 2035 |

USD 7,977.31 Million |

The market is expanding due to rising demand for low-latency storage and scalable infrastructure across sectors like fintech, e-commerce, and cloud services. Enterprises are adopting hybrid cloud platforms and flash-based systems to support real-time analytics and AI applications. Regulations around data localization are influencing infrastructure strategies. The region is becoming strategically important for investors targeting edge deployments, regulatory-compliant platforms, and high-growth service verticals. Market players are integrating software-defined and high-density storage to improve efficiency and performance.

Brazil leads the regional landscape due to its cloud availability zones, hyperscale investments, and large enterprise base. Mexico follows with expanding digital hubs in Querétaro and a strong fintech ecosystem. Chile is gaining traction with its stable energy grid and international cable access. Colombia and Argentina are emerging markets, supported by government digitalization initiatives and enterprise cloud adoption. These trends position Latin America as a high-potential region for storage-centric data center growth.

Market Dynamics:

Market Drivers

Rising Digital Transformation Across Industries Fuels Data Storage Infrastructure Growth

The Latin America Data Center Storage Market is expanding due to rapid digitalization across industries. Financial institutions, healthcare, and retail sectors are shifting operations to digital platforms. This creates constant demand for secure, scalable, and accessible storage. Government-backed digital agendas are pushing public sector data onto cloud and hybrid platforms. Enterprises require real-time data access to enhance analytics and business continuity. Cloud-native applications, IoT ecosystems, and enterprise mobility are becoming storage-intensive. The market supports critical infrastructure for national data governance. Investors see value in expanding resilient storage hubs. It forms the digital foundation for regional economic modernization.

- For instance, Mexico’s government cloud strategy led to the migration of hundreds of terabytes of public data to hybrid cloud platforms by 2024, enhancing digital governance and driving demand for secure, high-availability storage across regional data centers.

Adoption of Cloud and Hybrid Environments Supporting Storage Virtualization

Cloud infrastructure growth is a key driver for the storage market across Latin America. Businesses prefer hybrid and multi-cloud models for flexibility and compliance. Storage virtualization supports efficient resource utilization and improves data availability. Managed service providers are expanding offerings in storage-as-a-service. Data center operators are upgrading to tier III+ facilities for hosting enterprise and government data. Virtualized environments require robust backup, disaster recovery, and secure storage layers. It accelerates adoption of flash and software-defined storage systems. Cloud deployments across major metros push regional nodes to expand. Latin America Data Center Storage Market benefits from this regional decentralization.

Growth in Fintech, E-Commerce, and Streaming Services Boosting Low-Latency Storage Needs

Latin America’s booming digital economy is led by fintech apps, e-commerce growth, and content streaming platforms. These applications generate large volumes of structured and unstructured data. Real-time transaction processing, personalization engines, and content delivery need high-speed storage. The market sees increasing demand for NVMe-based solutions and edge caching. Financial inclusion programs and mobile banking drive secure backend storage investments. E-commerce platforms seek regional data localization and compliance. Streaming services deploy edge nodes to serve localized content faster. It reinforces the need for distributed, low-latency storage across key metro clusters. Storage vendors see the region as a high-potential frontier.

- For instance, Nubank in Brazil handles over 1 billion transactions monthly and leverages high-performance storage architecture, reportedly using NVMe-based systems to achieve sub-millisecond latency across its digital banking platforms, as outlined in its 2025 technical infrastructure updates.

Cybersecurity and Data Sovereignty Regulations Driving Onshore Storage Development

Stronger data protection frameworks across Latin American countries are pushing companies to store sensitive data locally. Government mandates for sovereign cloud and public sector compliance demand certified storage environments. Regulatory standards such as LGPD in Brazil and Habeas Data in Colombia require strict control over data access. Enterprises must implement backup and disaster recovery mechanisms to meet audit needs. The Latin America Data Center Storage Market is adapting through localized offerings with end-to-end encryption. Vendors now offer compliance-ready storage tailored for financial, legal, and healthcare workloads. It creates sustained demand for in-country infrastructure investment. Compliance-readiness is now a core selection criterion.

Market Trends

Migration from Traditional Storage Models to Software-Defined and Cloud-Native Platforms

Enterprises in Latin America are replacing legacy storage systems with more flexible, software-defined alternatives. Software-defined storage (SDS) supports automation, scalability, and hardware-agnostic operations. It aligns with the region’s growing adoption of containerized workloads. Cloud-native storage also enables better integration with DevOps pipelines. Storage vendors are embedding AI features for predictive maintenance and capacity planning. Latin America Data Center Storage Market reflects a shift toward programmable infrastructure. Organizations seek agility in provisioning storage aligned to application demands. SDS also enhances cost efficiency by separating control and data planes. The market is evolving towards intelligent, self-healing storage systems.

Edge Computing Expansion Creating New Demand for Distributed Storage Nodes

Edge computing deployments are rising to support latency-sensitive applications such as IoT, smart cities, and autonomous logistics. Brazil, Mexico, and Chile are investing in regional hubs beyond Tier-1 metros. This shift demands storage nodes embedded closer to data sources. Distributed object storage, local caching, and ruggedized systems are gaining traction. Telecom providers are co-locating storage with 5G and fiber infrastructure. The Latin America Data Center Storage Market supports this decentralized shift by enabling micro data centers and regional PoPs. These edge zones host real-time analytics and security functions. It drives the demand for compact, high-performance storage appliances.

Sustainability and Green Storage Infrastructure Becoming Strategic Differentiators

Sustainability goals are reshaping procurement in Latin American data centers. Operators seek energy-efficient storage systems with low power consumption per terabyte. Flash storage adoption is rising due to lower heat generation and higher data density. Vendors promote circular economy models through storage device recycling and upgrade programs. Environmental certifications now influence client RFPs. Enterprises align data center investments with ESG mandates. The Latin America Data Center Storage Market is witnessing demand for green data centers with reduced carbon footprints. Renewable energy sourcing and smart cooling are becoming standard for hyperscale facilities. Sustainability has become a business enabler, not just a compliance need.

AI and Analytics Workloads Driving High-Capacity, High-Speed Storage Investments

Latin American enterprises are increasing their use of AI, machine learning, and business intelligence tools. These workloads require fast storage access to train models and run inferences. Flash arrays, NVMe drives, and GPU-ready storage configurations are in demand. Industries such as healthcare, finance, and logistics are scaling their AI operations. The Latin America Data Center Storage Market supports this trend with high-throughput, low-latency systems. Enterprises prefer scalable storage that integrates with AI platforms. Predictive analytics needs petabyte-scale, real-time accessible storage. Vendors cater to this segment with tiered storage, AI-optimized file systems, and parallel data pipelines.

Market Challenges

Lack of Unified Digital Infrastructure and Policy Gaps Slowing Market Expansion

One major challenge is uneven digital infrastructure development across Latin America. While Brazil and Mexico have advanced facilities, many countries lag behind in connectivity and data regulation. This fragmentation makes regional deployment and compliance complex for enterprises. Data center operators face difficulties standardizing storage architecture across borders. The Latin America Data Center Storage Market is constrained by varied legal frameworks and inconsistent infrastructure quality. Policy gaps around data transfer, cross-border access, and disaster recovery create operational risk. These issues delay regional cloud rollouts and hinder seamless storage provisioning. Addressing fragmentation requires regulatory harmonization and investment in national backbone networks.

High Import Duties, Currency Instability, and Capital Constraints Limiting Deployment

Hardware imports for data center storage face heavy tariffs in some countries, raising setup costs. Local procurement channels remain limited, especially for advanced storage systems like all-flash arrays. Currency depreciation and inflation increase capex uncertainty. Many regional players lack access to long-term financing for infrastructure upgrades. The Latin America Data Center Storage Market is impacted by limited supply chains for storage components. Investors seek cost-optimized models to de-risk exposure. These factors force operators to delay or downscale expansions. Local manufacturing and financing partnerships are needed to improve affordability and project timelines.

Market Opportunities

Rising Adoption of AI, Fintech, and 5G Services Creating Strong Demand for Scalable Storage

Latin America’s growing digital economy offers strong potential for next-generation storage solutions. AI, 5G, and fintech platforms require low-latency, high-availability storage. Operators can scale regionally by aligning with telecom and hyperscaler investments. The Latin America Data Center Storage Market offers opportunities in flash systems, edge deployments, and hybrid cloud integration. Demand will surge in Tier II cities and cloud interconnect zones. Service providers who offer flexible, localized, and compliant storage will gain traction.

Policy-Driven Digital Sovereignty and Data Localization Efforts Encouraging Onshore Storage Investments

Governments across Latin America are enforcing stricter data localization and digital sovereignty laws. These policies create opportunities for certified storage facilities tailored for sensitive workloads. Enterprises prefer local infrastructure to meet compliance mandates. The Latin America Data Center Storage Market supports this need through domestic build-outs and sovereign cloud initiatives. Operators that offer in-country DRaaS, backup, and secure vaulting will attract regulated industries. This trend opens doors for both greenfield and brownfield storage deployments.

Market Segmentation

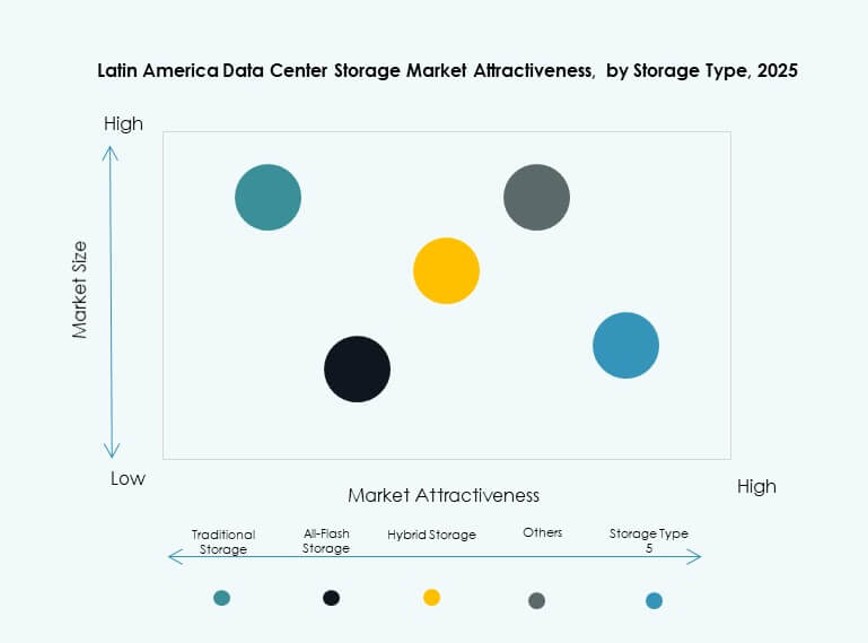

By Storage Type

Traditional storage continues to hold relevance, especially in legacy environments across mid-sized enterprises. However, hybrid storage is gaining ground due to its blend of cost efficiency and performance. All-flash storage is seeing rapid growth in financial services and AI-heavy applications where latency is critical. Others, including object-based systems, are rising in content delivery and surveillance sectors. The Latin America Data Center Storage Market sees hybrid storage emerging as a dominant type due to its flexibility across diverse workloads.

By Storage Deployment

Storage Area Network (SAN) systems dominate the deployment landscape for mission-critical workloads. Enterprises value their reliability and ability to scale in centralized environments. Network-attached Storage (NAS) is popular among media and content providers for easier file sharing. Direct-attached Storage (DAS) is used in smaller setups and edge deployments. The Latin America Data Center Storage Market shows SAN as the leading deployment method, especially in financial and government sectors.

By Component

Hardware makes up the majority share, driven by demand for SSDs, servers, and racks. Software is growing faster, powered by adoption of SDS, backup software, and AI-based management tools. Hardware upgrades are frequent among Tier III+ facilities, while software drives optimization. In the Latin America Data Center Storage Market, hardware currently dominates, but software’s share is increasing with the shift to cloud-native storage.

By Medium

Solid-State Drives (SSD) are gaining market share over Hard Disk Drives (HDD) due to better speed and energy efficiency. Tape storage still exists for long-term archival, especially in public sector and legal firms. SSD use is growing in analytics, streaming, and financial operations. The Latin America Data Center Storage Market favors SSD for performance-intensive use cases, though HDD remains relevant for cold storage.

By Deployment Model

Cloud-based storage is rapidly rising, supported by hyperscaler expansion and SaaS platforms. On-premises remains important for compliance-heavy industries like healthcare and government. Hybrid models are preferred by large enterprises balancing control with flexibility. The Latin America Data Center Storage Market shows hybrid deployment leading adoption due to its ability to meet latency, control, and scale requirements.

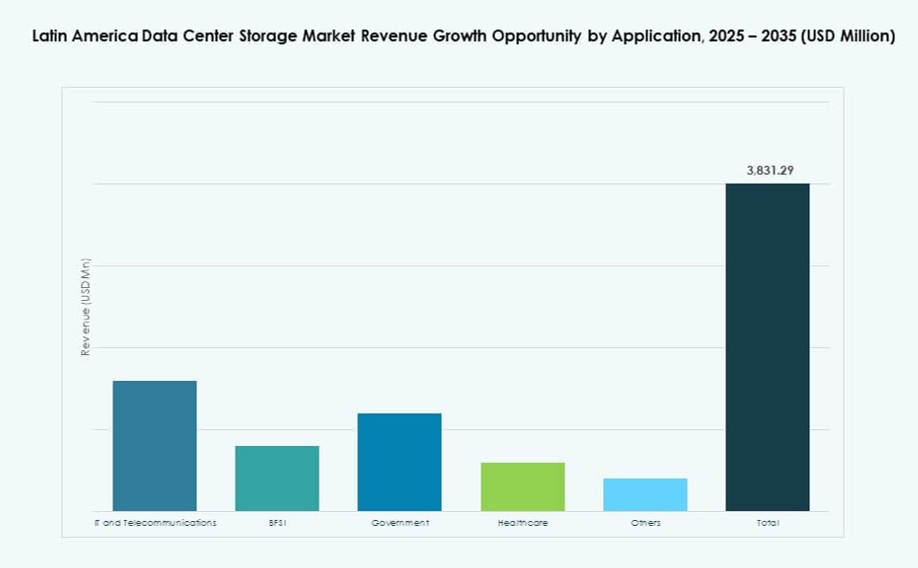

By Application

IT and Telecommunications lead in adoption due to digital transformation, 5G rollout, and AI integration. BFSI follows closely, driven by fintech growth and digital banking. Government and healthcare sectors demand compliant and secure storage, especially with national data localization policies. The Latin America Data Center Storage Market sees strong uptake across IT, BFSI, and public sector verticals, with content and e-commerce fueling broader demand.

Regional Insights

Brazil Holds the Largest Share in the Region with Over 40% Market Contribution

Brazil dominates the Latin America Data Center Storage Market with more than 40% share. It hosts hyperscale cloud regions from AWS, Google, and Microsoft, enabling high-scale storage adoption. São Paulo remains the primary hub due to strong infrastructure and enterprise concentration. Regulatory improvements and ESG-friendly policies attract global investments. Telecom and financial firms in Brazil are key drivers of enterprise storage. Growth also comes from smart city projects and 5G-linked deployments.

- For instance, Telefônica Brasil (Vivo) has upgraded its São Paulo data centers with high-performance flash storage to support rising 5G traffic and digital service expansion across its core metro network.

Mexico and Chile Jointly Contribute Around 35% Through Regional Hubs and Cloud Integration

Mexico and Chile account for about 35% of the regional storage market. Mexico benefits from proximity to U.S. cloud nodes, fintech activity, and government digitization. Querétaro is emerging as a data center corridor. Chile hosts South America’s top cloud landing points and submarine cable connections. Its stable power supply supports high-density deployments. The Latin America Data Center Storage Market sees both countries as strategic locations for edge and latency-optimized services.

Colombia, Argentina, and Peru Represent Emerging Growth Nodes with Localized Demand Patterns

Colombia, Argentina, and Peru form the emerging cluster contributing the remaining 25% share. Colombia’s digital economy is growing with demand for compliant storage in finance and healthcare. Argentina’s cloud demand is rising in education, retail, and media sectors. Peru’s smart infrastructure and government programs fuel data growth in urban zones. These countries are building Tier II and III facilities to support localized backup, archiving, and AI workloads. It creates long-term potential for storage vendors and infrastructure investors.

- For instance, in 2023, Claro Perú inaugurated a $50 million Tier III data center in Lima, developed in partnership with Huawei. The facility supports digital transformation and IoT applications, with Huawei’s OceanStor Dorado flash systems widely used for smart city and data-intensive workloads across the region.

Competitive Insights:

- Ascenty

- Odata

- Scala Data Centers

- Huawei Technologies

- Hewlett Packard Enterprise (HPE)

- Dell Technologies

- IBM Corporation

- Cisco Systems, Inc.

- Lenovo Group

- Seagate Technology

The Latin America Data Center Storage Market features a mix of global storage hardware leaders and regional colocation operators. Companies like HPE, Dell Technologies, and IBM offer comprehensive storage infrastructure and hybrid cloud solutions. Huawei and Lenovo are expanding hardware footprints with high-performance systems. Colocation specialists such as Ascenty, Odata, and Scala lead in hyperscale-ready facilities. These firms partner with cloud providers and storage vendors to deliver localized, compliant storage environments. The market is seeing increased competition around flash systems, software-defined storage, and backup automation. Vendors differentiate through energy-efficient infrastructure, edge deployment capabilities, and integration with AI workloads. It continues to attract both regional operators and global storage solution providers focused on compliance, scalability, and regional workload optimization.

Recent Developments:

- In December 2025, Actis launched TERRANOVA, a new hyperscale data center platform to accelerate Latin America’s digital growth, with its first site in Querétaro, Mexico, slated online in Q1 2026 and further campuses planned in Campinas, Brazil.

- In August 2025, ODATA, an Aligned Data Centers company and Mexico’s largest data center provider, launched its fourth hyperscale data center, QR04, near San Miguel de Allende in Querétaro, Mexico.

- In July 2025, Ascenty, a leading Latin American data center operator, announced a R$300 million ($55 million) investment in its fifth São Paulo facility, SPO05, spanning 40,000 sqm and 47MW to support cloud and AI workloads amid growing regional demand.