Executive summary:

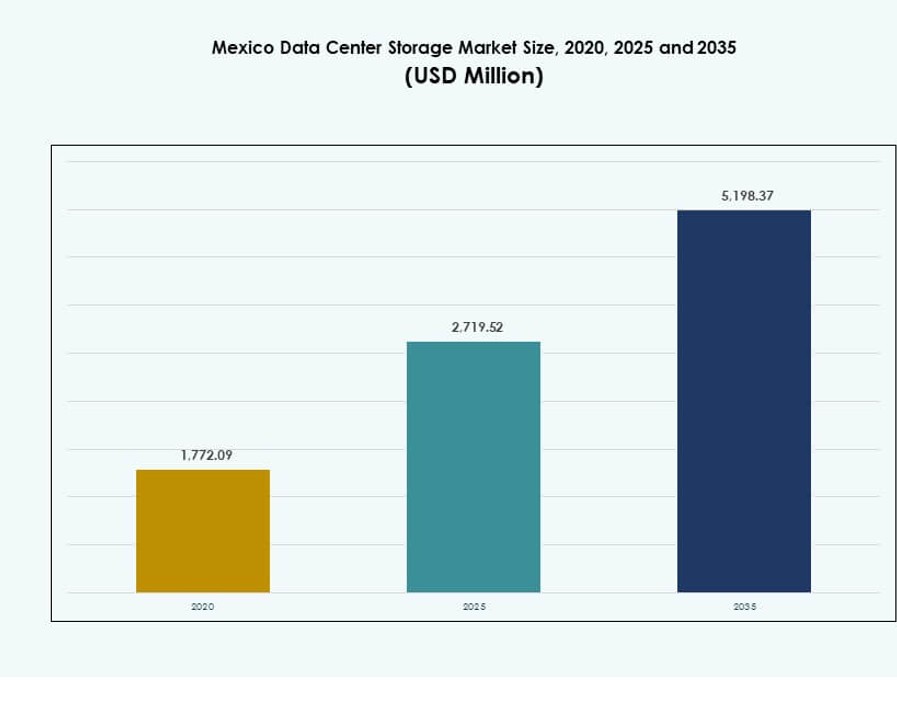

The Mexico Data Center Storage Market size was valued at USD 1,772.09 million in 2020 to USD 2,719.52 million in 2025 and is anticipated to reach USD 5,198.37 million by 2035, at a CAGR of 6.63% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Mexico Data Center Storage Market Size 2025 |

USD 2,719.52 Million |

| Mexico Data Center Storage Market, CAGR |

6.63% |

| Mexico Data Center Storage Market Size 2035 |

USD 5,198.37 Million |

The market is witnessing rapid growth driven by cloud adoption, AI integration, and enterprise digitalization. Companies are modernizing infrastructure with software-defined and all-flash storage systems. Innovations in data protection, hybrid deployment models, and NVMe protocols are transforming storage performance and cost efficiency. Strategic investments by hyperscalers and rising demand from telecom and financial sectors elevate the market’s value. It plays a critical role in enabling data resilience, operational continuity, and regulatory compliance, making it a key focus for both technology providers and institutional investors.

Central Mexico leads due to strong fiber connectivity, hyperscale data centers, and colocation expansion in urban hubs. Northern Mexico is emerging as a growth zone, supported by industrial activity and proximity to the U.S. Southern and coastal regions remain underdeveloped but show increasing potential with subsea cable landings and edge infrastructure projects. Regional differences in energy access and enterprise readiness influence the pace of storage deployment.

Market Dynamics:

Market Drivers

Rising Cloud Adoption Driving Storage Modernization Across Enterprise IT Workloads

Enterprises across Mexico are migrating from legacy IT infrastructure toward cloud-based models. This shift accelerates the adoption of flexible, scalable, and high-performance storage systems. The demand for virtualized workloads, disaster recovery, and remote access boosts interest in advanced storage solutions. Cloud providers are expanding in Tier I cities to support public, private, and hybrid models. Businesses prefer solutions that enable on-demand scalability, lower latency, and seamless data access. This trend supports demand for Storage Area Networks (SANs), all-flash arrays, and software-defined storage. The Mexico Data Center Storage Market benefits from this ongoing shift in enterprise computing strategies. Cloud-native applications and containerized environments will further reinforce market momentum.

- For instance, AWS opened its Mexico (Central) Region in January 2025, bringing local data residency and lower‑latency storage services to enterprises and reducing dependency on distant global regions.

Edge Infrastructure Expansion Creating Demand for Decentralized and Agile Data Storage Models

Edge computing is gaining traction in Mexico due to rising IoT use, content delivery networks, and latency-sensitive workloads. This shift requires localized data processing and real-time analytics near the source. Storage systems are evolving to support edge applications with smaller footprints, faster input/output operations, and energy-efficient performance. The need to manage massive data from surveillance, smart city projects, and industrial automation supports storage deployment beyond traditional hubs. The Mexico Data Center Storage Market responds with solutions built for rugged edge environments and remote operations. Vendors focus on decentralized architectures, compact NAS systems, and flash-based platforms tailored for the edge. The distributed model improves resilience and supports regional growth.

Adoption of AI and Big Data Platforms Accelerating Storage Technology Evolution

Artificial intelligence, machine learning, and data analytics require high-throughput storage with massive capacity and low latency. Organizations in sectors like BFSI, healthcare, and telecom are deploying AI workloads that demand NVMe-based systems, GPU-optimized architecture, and parallel file storage. This technological leap transforms storage from passive data holders to active enablers of intelligent computing. The Mexico Data Center Storage Market supports this shift by promoting smart storage solutions, automated tiering, and AI-integrated management tools. These systems enhance performance, reduce operational costs, and improve insights from unstructured datasets. High-performance computing adoption in scientific research and predictive modeling also contributes to growth.

Private Sector Investments and Government Incentives Enhancing Strategic Role of Storage Infrastructure

Strategic investment from both domestic enterprises and global hyperscalers is boosting Mexico’s digital backbone. Government-backed initiatives and tax benefits attract foreign investors to establish IT infrastructure zones. Businesses see long-term value in deploying robust storage that complies with data protection norms and cybersecurity regulations. The Mexico Data Center Storage Market gains relevance as firms treat storage not just as a utility, but a strategic asset. Strong storage architecture ensures business continuity, legal compliance, and data sovereignty. Local manufacturing and skilled IT workforce further lower barriers to storage technology adoption. Mexico’s positioning as a tech hub in Latin America makes storage investments critical for future competitiveness.

- For instance, CloudHQ announced a US $4.8 billion investment to build six hyperscale data centers in Querétaro, Mexico, covering 52 hectares and designed to support cloud computing and AI workloads with up to 900 MW of capacity.

Market Trends

Rising Demand for Software-Defined Storage (SDS) to Enable Scalability and Automation

Software-defined storage decouples software from hardware, allowing better scalability, vendor flexibility, and cost optimization. Mexican enterprises adopt SDS to automate storage provisioning, optimize workloads, and reduce manual intervention. It supports heterogeneous environments, making it easier to integrate with cloud platforms and legacy infrastructure. SDS improves resource utilization, aligns with DevOps, and enhances resilience. IT teams benefit from centralized management and real-time analytics. The Mexico Data Center Storage Market witnesses growing SDS adoption across BFSI and telecom sectors. Open-source SDS platforms gain interest among budget-conscious firms. Flexibility and automation will continue to drive SDS momentum.

Growing Use of NVMe Protocols to Improve Latency and Drive High-Speed Data Access

Non-Volatile Memory Express (NVMe) protocols offer lower latency, higher input/output operations, and improved efficiency over traditional storage. Enterprises in Mexico shift toward NVMe-based storage systems for AI, analytics, and virtualization workloads. NVMe supports direct communication between applications and SSDs, eliminating controller bottlenecks. This results in faster response times, better performance, and lower power use. Data centers favor NVMe over SATA and SAS for mission-critical applications. The Mexico Data Center Storage Market reflects this shift with vendors launching NVMe-enabled SANs and all-flash systems. NVMe-over-Fabrics extends its benefits to larger network environments. These protocols redefine high-performance storage standards.

Increased Preference for Green Storage Infrastructure Focused on Energy Efficiency and Sustainability

Environmental sustainability is becoming a core goal for data center operators in Mexico. Storage infrastructure contributes to power consumption and heat generation, prompting demand for energy-efficient systems. Vendors now offer storage with optimized cooling, low-power SSDs, and intelligent power scaling. Green data centers reduce total cost of ownership and appeal to ESG-conscious investors. The Mexico Data Center Storage Market supports sustainability by promoting low-carbon technologies and recyclable components. Flash-based systems replace power-hungry spinning disks. Certifications and audits push companies to adopt greener storage options. This trend aligns with broader goals of reducing the digital sector’s carbon footprint.

Rapid Growth in Backup as a Service (BaaS) and Disaster Recovery as a Service (DRaaS)

Businesses face growing cybersecurity threats, regulatory audits, and compliance risks. This increases the need for secure and efficient data protection solutions. Backup as a Service and Disaster Recovery as a Service offer managed, scalable, and offsite recovery capabilities. They eliminate the need for in-house backup hardware, improving cost control. Service providers in Mexico bundle storage with encryption, replication, and recovery tools. The Mexico Data Center Storage Market expands with rising adoption of cloud-based DR solutions by SMEs. Automated failover systems and continuous backup models strengthen business continuity. BaaS and DRaaS become integral to storage service portfolios.

Market Challenges

Rising Energy Costs and Infrastructure Limitations Impacting Deployment of High-Density Storage

Energy costs in Mexico remain volatile and significantly affect operational expenses for data centers. High-performance storage systems, particularly those supporting AI and HPC workloads, demand constant power and efficient cooling. Many facilities lack access to sustainable energy sources or face grid instability. This limits the adoption of dense rack solutions and flash-based storage in Tier II regions. The Mexico Data Center Storage Market struggles with these limitations, especially among colocation providers and SMEs. Infrastructure upgrades remain costly, leading firms to delay modernization. This barrier affects performance, scalability, and long-term efficiency.

Data Security Risks, Regulatory Complexity, and Limited Skilled Workforce Restraining Adoption

Data sovereignty laws and compliance mandates create operational complexity for storage providers. Enterprises need localized data hosting and encryption standards aligned with GDPR-like norms. Breaches, ransomware, and insider threats force IT teams to focus heavily on cybersecurity, slowing deployment cycles. The Mexico Data Center Storage Market faces talent shortages in storage architecture, automation, and hybrid integration. Training gaps prevent optimal configuration and management of advanced systems. Vendors must invest in training and certifications to support adoption. These risks increase Total Cost of Ownership for sensitive applications.

Market Opportunities

Expansion of AI and Industrial IoT Creating New Demand for Intelligent Storage Platforms

Artificial intelligence and Industrial IoT adoption generates petabytes of unstructured data needing fast, scalable, and secure storage. This trend opens new revenue streams for vendors offering intelligent storage with machine learning for data classification and lifecycle management. The Mexico Data Center Storage Market taps into this need with AI-ready platforms. Edge storage and hybrid flash systems provide low-latency access while supporting analytics at scale.

Rising Demand for Localized Cloud Services Supporting Data Residency and Compliance Needs

Enterprises in Mexico increasingly seek localized storage to meet compliance and data residency norms. This creates opportunity for cloud providers and colocation players to offer regional cloud zones with integrated storage. The Mexico Data Center Storage Market benefits from partnerships between hyperscalers and local firms. Hybrid deployment models enhance adoption across regulated sectors.

Market Segmentation

By Storage Type

All-flash storage dominates the Mexico Data Center Storage Market due to its speed, low latency, and reduced power consumption. It outperforms traditional HDDs in mission-critical workloads and AI applications. Hybrid storage is also gaining ground, offering a balance between cost and performance. Traditional storage sees gradual decline, limited to cold storage and archival use. Others include object-based and tiered storage variants used in large-scale environments.

By Storage Deployment

Storage Area Network (SAN) systems lead this segment, widely used for high-speed block storage in enterprise environments. SAN supports structured workloads such as databases and ERP systems. Network-attached Storage (NAS) sees adoption in media, healthcare, and small enterprises due to ease of use. Direct-attached Storage (DAS) remains relevant for standalone servers and low-cost deployments. Other formats include object storage for big data and web-scale applications.

By Component

Hardware dominates the component segment, accounting for the bulk of the market value due to reliance on physical storage devices. SSDs, HDDs, and networking switches comprise major hardware components. However, software is growing with the rise of storage virtualization, automation, and SDS. Management platforms and monitoring tools are increasingly bundled with hardware deployments, improving control and performance optimization.

By Medium

Solid-State Drives (SSD) are gaining major market share due to faster data access, better energy efficiency, and compact form. SSDs replace HDDs in latency-sensitive applications, contributing to their growth. Hard Disk Drives (HDD) still hold relevance for archival, backup, and cold storage due to lower cost per GB. Tape storage is niche, used in archival and long-term backup for government and research sectors.

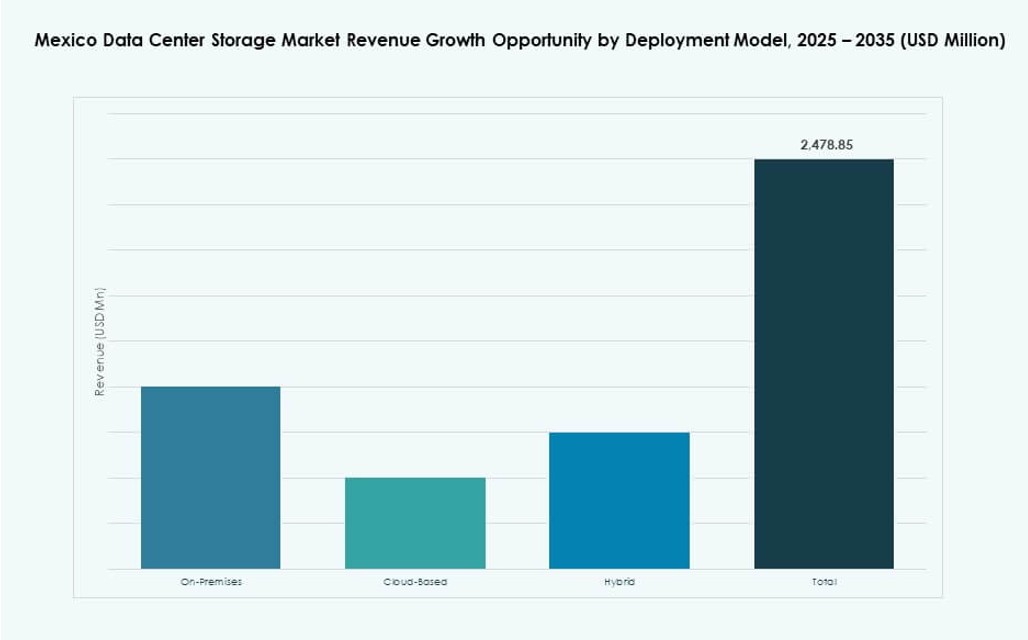

By Deployment Model

Cloud-based storage holds strong momentum, driven by demand for scalability, cost-efficiency, and remote access. On-premises deployment remains essential for government and regulated sectors requiring full control. Hybrid models blend both, offering flexibility, data redundancy, and workload-specific customization. The Mexico Data Center Storage Market favors hybrid adoption across BFSI and healthcare, where latency and compliance coexist.

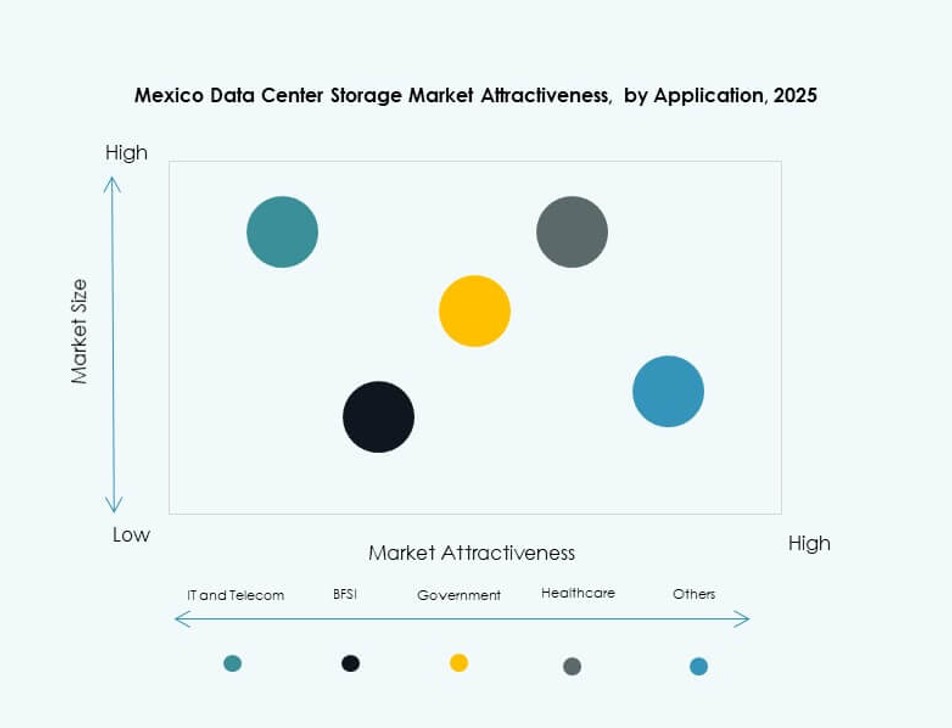

By Application

IT and Telecommunications account for the largest share in the Mexico Data Center Storage Market due to heavy demand for content delivery, subscriber data management, and 5G-related services. BFSI follows, driven by secure data processing, transaction records, and DRaaS use. Government projects adopt storage for digitization and secure citizen records. Healthcare sees rising use for medical imaging and compliance-driven data handling. Others include media, education, and manufacturing sectors.

Regional Insights

Central Mexico Leads the Market with 46% Share Due to Connectivity and Colocation Growth

Central Mexico, especially Mexico City and Querétaro, dominates the market with 46% share. The region benefits from robust fiber connectivity, data center density, and colocation presence. It hosts major facilities from global and domestic providers, including cloud nodes and enterprise deployments. Skilled labor availability and business-friendly zones support infrastructure investments. The Mexico Data Center Storage Market sees strong enterprise migration to central zones. Low-latency services and edge accessibility increase demand in this core region.

- For instance, Equinix opened its MO2 data center in Monterrey in Q3 2025, offering over 30,000 sq ft of colocation space optimized for AI and enterprise workloads. The facility supports hybrid cloud deployments and expands digital infrastructure in Northern Mexico.

Northern Mexico Holds 34% Market Share Driven by Industrial Hubs and Cross-Border Integration

Northern Mexico, including Monterrey and Ciudad Juárez, contributes around 34% to market share. The region’s proximity to the U.S. border supports cross-border digital trade and industrial data use. Manufacturing clusters drive real-time analytics and IoT workloads. Storage adoption rises in support of supply chain digitization and binational cloud access. It enables content delivery and low-latency edge storage for U.S. clients. Telecom upgrades and fiber backbones enhance its strategic importance.

Southern and Coastal Regions Account for 20% and Emerge with Subsea Cables and Edge Demand

Southern and coastal regions collectively represent 20% share and show early growth signs. Locations like Mérida and Veracruz benefit from subsea cable landings that improve global connectivity. Rising interest in edge computing and regional data zones encourages distributed storage deployment. Government-backed digitalization efforts expand storage demand in underpenetrated areas. The Mexico Data Center Storage Market anticipates higher growth in these regions through satellite POPs and modular infrastructure. Climate and energy availability shape deployment strategies.

- For instance, ODATA energized and expanded power infrastructure at its DC QR03 campus in Querétaro, including a 400 kV substation expansion and new transmission lines to support scalable data center energy requirements.

Competitive Insights:

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- NetApp

- Cisco Systems, Inc.

- IBM Corporation

- Seagate Technology

- Lenovo Group

- Huawei Technologies Co., Ltd.

- Hitachi Vantara

- Veeam Software

The Mexico Data Center Storage Market features strong competition among multinational vendors offering a mix of hardware, software-defined platforms, and integrated solutions. Dell Technologies and HPE lead with broad product portfolios that span on-premises, cloud, and hybrid deployments. NetApp and Cisco strengthen their position through partnerships and innovations in flash and SAN systems. IBM and Lenovo focus on enterprise AI and hybrid infrastructure demands. Vendors invest in NVMe, SDS, and sustainability-driven offerings to match rising performance needs and ESG goals. The market encourages consolidation and co-innovation through local alliances, hyperscaler collaboration, and edge deployments. It remains attractive for new entrants in software-centric and cloud-native segments.

Recent Developments:

- In December 2025, Hewlett Packard Enterprise (HPE) unveiled its new HPE StoreOnce 5720 and 7700 backup appliances designed for hybrid cloud environments. These innovations, set for release in spring 2026.

- In February 2025, Alibaba Cloud launched its first data center region in Mexico to expand local cloud resources. The facility supports storage-intensive workloads and improves infrastructure availability.

- In January 2025, Lenovo Group announced the acquisition of Infinidat to strengthen its high-end enterprise storage portfolio. The move enhances Lenovo’s cyber-resilient data management offerings.

- In March 2024, Dell Technologies collaborated with NVIDIA to validate its Dell PowerScale storage for the DGX SuperPOD platform. This enables enterprises to accelerate AI and generative AI workloads using advanced NAS solutions.