Executive summary:

The Nepal Data Center Storage Market size was valued at USD 62.55 million in 2020 to USD 110.43 million in 2025 and is anticipated to reach USD 234.67 million by 2035, at a CAGR of 7.75% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Nepal Data Center Storage Market Size 2025 |

USD 110.43 Million |

| Nepal Data Center Storage Market, CAGR |

7.75% |

| Nepal Data Center Storage Market Size 2035 |

USD 234.67 Million |

The market is driven by Nepal’s digital transformation, expanding internet penetration, and demand for secure enterprise storage. Government digitization, fintech growth, and telecom network expansion are accelerating adoption of modern storage technologies. Businesses seek scalable, energy-efficient systems like all-flash arrays and software-defined storage to meet workload needs. Investment in hybrid models is rising to address latency, compliance, and resilience. The Nepal Data Center Storage Market holds strategic value for investors supporting connectivity, sovereign infrastructure, and cloud growth.

Kathmandu Valley leads the market due to its advanced network infrastructure, enterprise density, and concentration of telecom and government hubs. The region benefits from carrier-neutral facilities, submarine cable gateways, and reliable power. Pokhara and Chitwan are emerging as regional centers with improving connectivity and enterprise demand. These locations support edge deployments and DRaaS solutions. Growing infrastructure outside the valley indicates a gradual decentralization of Nepal’s data storage ecosystem.

Market Dynamics:

Market Drivers

Government Digital Push and E-Governance Fuel Data Storage Requirements Across Public Infrastructure

Nepal’s government is actively promoting digital transformation through policies that support e-governance, national identity databases, and tax digitization platforms. These systems require robust, scalable storage infrastructure for data continuity, compliance, and real-time service delivery. Projects under the Digital Nepal Framework demand localized storage to maintain sovereignty and ensure faster access. Public cloud adoption remains low, pushing agencies to build secure on-premise and hybrid solutions. These shifts increase long-term storage spending across ministries and public service bodies. The Nepal Data Center Storage Market benefits from this strong institutional demand for infrastructure modernization. It has become a pillar of national digital resilience. Government data centers are also investing in backup and archival technologies to prevent data loss. This centralized strategy drives early-stage data infrastructure growth across regions.

- For instance, Nepal’s National ID Management System enrolled over 17 million citizens by February 2024, requiring centralized on-premise data storage at Singha Durbar servers for sovereignty, as confirmed by government officials.

Rise in Mobile Internet Penetration and Digital Service Consumption Driving Enterprise Storage Needs

Mobile usage growth is reshaping Nepal’s enterprise data strategy, with millions relying on mobile apps for payments, learning, and entertainment. Businesses are modernizing their IT infrastructure to handle the rising influx of user data. This change includes integrating scalable storage platforms to support databases, CRM tools, and customer-facing platforms. With more enterprises using edge platforms and real-time analytics, there’s an increasing need for low-latency, high-availability storage. Many telecom operators and ISPs are scaling colocation storage to serve growing regional traffic. It enables content delivery and caching closer to end-users. Nepal Data Center Storage Market now plays a key role in ensuring consistent performance and data accessibility. Telecom firms are also deploying flash arrays and hybrid systems to optimize core applications. The country’s evolving consumption patterns make enterprise storage a central component of digital expansion.

- For instance, by late 2025, Ncell served approximately 12.95 million subscribers and accounted for over 52% of its revenue from mobile data services. According to NTA reports, broadband usage surged across its upgraded 2,200+ tower network, prompting Ncell to implement edge caching storage and localized processing to manage high-latency and bandwidth-sensitive workloads across Nepal.

Banking, Fintech, and Insurance Sectors Investing in Compliant and Scalable Storage Infrastructure

Nepal’s BFSI sector is digitizing operations at a fast pace, prompted by increasing use of mobile banking, QR payments, and UPI-based services. These transactions generate sensitive and high-volume data requiring secure, compliant storage systems. Financial institutions are adopting SAN and NAS configurations to optimize data access and reduce latency. Legacy systems are being replaced by hybrid models that combine cloud elasticity with on-premise control. Backup and DRaaS are gaining traction to meet regulatory mandates and enable continuous operations. The Nepal Data Center Storage Market supports these institutions by offering localized, high-availability systems. It helps reduce dependence on external infrastructure. This transformation is critical for building consumer trust in digital finance platforms. Financial sector storage will remain a dominant contributor to overall demand.

Cloud-Native Startups and IT Services Creating New Demand for Flexible Storage Models

Nepal’s tech startup ecosystem is growing, backed by incubators and cross-border investments. These digital-native businesses need API-integrated storage solutions that scale with user growth and app activity. Many startups operate entirely on SaaS models, requiring storage that supports DevOps, CI/CD pipelines, and containerized environments. The demand for NVMe, SSD arrays, and software-defined storage (SDS) is expanding across the startup space. Cloud-based and hybrid models enable faster application rollouts and cost-efficient scaling. Hosting and IT service companies are also driving storage adoption to support SMEs and government clients. The Nepal Data Center Storage Market is enabling this flexible infrastructure by supporting both shared and dedicated storage environments. It is becoming a foundational layer for innovation, business continuity, and real-time digital engagement. The market’s strategic value will continue to grow with the tech ecosystem.

Market Trends

Shift Toward Green Data Center Storage Solutions to Address Power Constraints and Carbon Goals

Nepal’s limited energy availability and push toward sustainability are encouraging operators to adopt energy-efficient storage systems. The integration of SSDs and flash storage reduces cooling needs and improves performance per watt. Facilities are investing in greener architectures using low-power controllers and intelligent power management features. Storage cooling solutions are being optimized using passive or liquid-based designs. The government is promoting solar-based backup systems to power edge storage environments. Demand for green data center certifications is rising, especially in public projects. The Nepal Data Center Storage Market is aligning with these eco-conscious practices to reduce operational costs. It positions the market as an attractive option for impact-focused investors. Storage vendors are now bundling energy dashboards with infrastructure for better monitoring.

Growth in Disaster Recovery-as-a-Service (DRaaS) and Backup Solutions for Data Redundancy

With the rise in cybersecurity threats and physical risks like earthquakes, businesses are prioritizing offsite backups and disaster recovery storage. DRaaS offerings are gaining popularity among BFSI, healthcare, and government entities. These services provide continuous replication, automated failovers, and geographically distributed backups. Organizations prefer local providers for better control and compliance with data localization policies. Tape storage is being used in limited form for deep archival due to cost advantages. SAN systems with redundancy and failover capabilities are being deployed in Kathmandu and major cities. The Nepal Data Center Storage Market now includes multiple players offering tiered storage plans bundled with DRaaS. It helps enterprises maintain uptime and regulatory readiness. These trends contribute to a more resilient digital ecosystem.

Rise in Content Delivery Platforms Driving Edge Storage Deployment in Tier-2 Cities

Video streaming, e-learning, and gaming platforms are expanding outside Kathmandu to reach new consumer bases. This content shift is creating demand for distributed edge storage that ensures low-latency delivery. Telecom and CDN providers are establishing micro-data centers closer to high-consumption zones. These setups require compact, scalable storage optimized for fast read/write speeds. NAS systems and object storage are being used to support cached content and real-time updates. SSDs are favored for IOPS-intensive applications. The Nepal Data Center Storage Market is expanding geographically, reflecting this digital consumption pattern. Storage vendors are introducing modular units that can scale with local demand. This regional deployment helps reduce central infrastructure load.

Increased Adoption of Virtualized Storage for Cost-Efficient Infrastructure Modernization

Businesses in Nepal are increasingly adopting storage virtualization to maximize utilization and reduce hardware dependency. SDS platforms allow centralized management and better resource pooling across departments. Virtualization supports dynamic allocation based on workload intensity. It helps minimize upfront CAPEX for SMBs while offering enterprise-level performance. Several providers offer storage services bundled with hyperconverged infrastructure. The trend supports agile infrastructure planning and fast provisioning cycles. The Nepal Data Center Storage Market reflects this change through increased demand for software-centric models. It helps data centers manage hybrid workloads more efficiently. This trend will likely accelerate as businesses seek scalable, low-maintenance solutions.

Market Challenges

Limited Infrastructure Readiness and Power Reliability Pose Major Constraints to Storage Expansion

Nepal faces structural limitations in developing high-capacity data centers, especially outside the Kathmandu Valley. Unreliable electricity supply and limited grid stability increase dependence on generators and raise storage deployment costs. High land prices and insufficient zoning regulation add to site development challenges. Many enterprises hesitate to invest due to the complexity of maintaining 24/7 uptime. Bandwidth constraints and latency also affect performance of cloud-based storage platforms. Local hardware supply chains are underdeveloped, leading to reliance on imports and higher TCO. The Nepal Data Center Storage Market experiences slower scale-up timelines due to these systemic gaps. It must navigate these constraints to ensure consistent service delivery. Without strong infrastructure support, long-term growth remains vulnerable.

Skilled Talent Shortage and Limited Vendor Ecosystem Impact Technology Maturity and Innovation

Nepal’s IT workforce is still evolving, with a limited number of professionals specialized in data storage architecture, security, and operations. This shortage restricts the speed at which advanced storage solutions can be implemented and maintained. Managed services are underutilized due to a lack of vendors offering enterprise-grade SLAs. Local partners often lack experience with high-density SANs, flash arrays, or hyperconverged systems. Enterprises must rely on regional consultants or foreign vendors, which raises costs and integration delays. The Nepal Data Center Storage Market lacks a robust partner network for post-deployment support and customization. It slows innovation cycles and reduces confidence in adopting new architectures. Bridging the talent and vendor gap is critical for long-term maturity.

Market Opportunities

Rising Cloud Localization and Data Sovereignty Mandates Open Room for Domestic Storage Players

Nepal’s evolving regulatory landscape encourages data to remain within national borders, creating strong demand for local data storage infrastructure. This supports the growth of domestic cloud and colocation providers. Local operators can build value through low-latency, compliant storage offerings tailored to public sector and BFSI needs. The Nepal Data Center Storage Market presents a significant opportunity for early movers offering region-specific configurations. It allows providers to bundle storage with analytics and cybersecurity services, increasing customer retention.

Edge Computing and 5G Deployment Creating Scope for Micro Data Centers with Modular Storage

With telcos preparing for future 5G rollouts and digital consumption growing outside Kathmandu, there is a clear opportunity in regional edge storage. Compact, modular storage systems deployed closer to end-users can support content delivery, local caching, and analytics. These setups will be crucial in emerging digital zones like Pokhara and Butwal. The Nepal Data Center Storage Market will benefit by enabling vendors to offer mobile, containerized units tailored to edge performance needs. This trend supports faster service delivery and resilience.

Market Segmentation

By Storage Type

Traditional storage holds the largest share due to its widespread use in legacy government and banking systems. All-flash storage is growing rapidly due to lower latency and higher performance, especially in enterprise workloads. Hybrid storage is gaining attention among SMEs seeking flexibility and cost control. The Nepal Data Center Storage Market is shifting toward hybrid models in mid-size facilities and managed service platforms.

By Storage Deployment

Storage Area Network (SAN) systems dominate due to their scalability and performance in core enterprise workloads. NAS systems are widely used for file-based storage across media, education, and government agencies. DAS remains relevant for entry-level deployments and edge setups. The Nepal Data Center Storage Market shows strong preference for SAN in telecom and BFSI sectors, while NAS adoption is rising in public IT modernization.

By Component

Hardware holds the major share driven by investments in racks, enclosures, and SSD/HDD units. Software segment is expanding with increasing use of SDS, virtualization, and data management platforms. As IT maturity grows, vendors bundle both hardware and management software to offer complete solutions. The Nepal Data Center Storage Market sees growing demand for integrated platforms combining both components.

By Medium

HDD leads the market due to affordability and its use in archival storage. SSD adoption is increasing in high-performance systems across telecom and enterprise verticals. Tape storage holds minimal share and is limited to deep backup in select institutions. The Nepal Data Center Storage Market is experiencing a shift from HDD to SSD for real-time applications and mission-critical use cases.

By Deployment Model

On-premises deployment is dominant, driven by control, compliance, and connectivity concerns. Cloud-based models are growing among startups and IT service providers. Hybrid deployments are being explored by BFSI and healthcare sectors for workload flexibility. The Nepal Data Center Storage Market will see gradual hybrid adoption as connectivity and bandwidth improve.

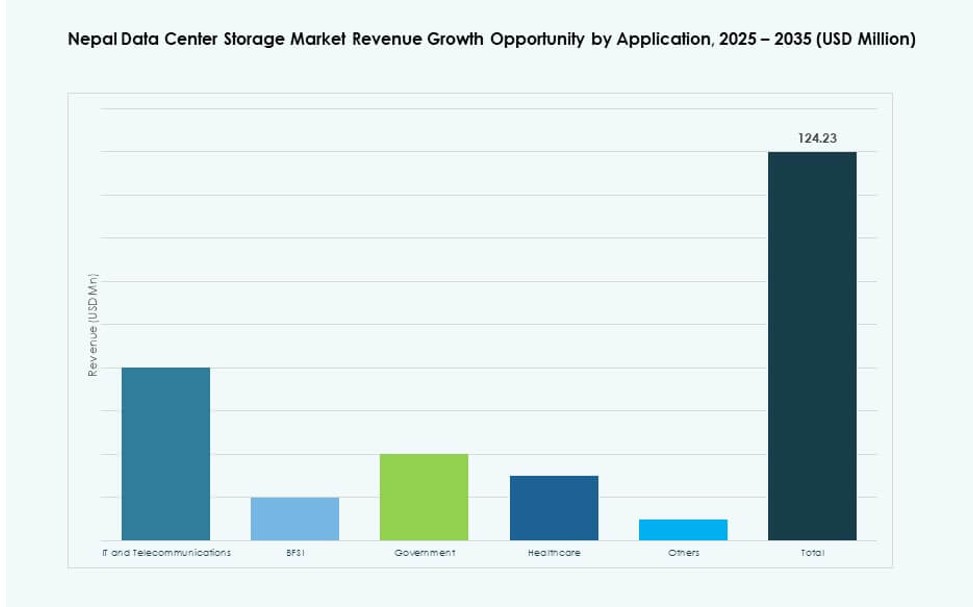

By Application

IT and Telecom sectors lead in storage consumption due to expanding user bases and content demand. BFSI holds the second-largest share, driven by secure, regulated data processing needs. Government projects and digital identity programs contribute steadily. Healthcare and others are emerging due to digital health records and sector-wide modernization. The Nepal Data Center Storage Market remains heavily influenced by telecom and BFSI storage trends.

Regional Insights

Kathmandu Valley Leads the Market with Over 60% Share Due to Network Density and Institutional Presence

Kathmandu Valley remains the dominant subregion in the Nepal Data Center Storage Market, accounting for more than 60% of the total share. It hosts major telecom hubs, government data centers, BFSI headquarters, and the country’s leading IT service providers. The region has better power supply, fiber connectivity, and talent access. Most new storage deployments, including SAN and hybrid cloud platforms, are concentrated in Kathmandu due to its infrastructure advantages. The valley also acts as a central backup and DR hub for nationwide workloads.

- For instance, Huawei is building a primary data center for Nepal Telecom in Kathmandu, signed via a Letter of Intent in January 2025, alongside a disaster recovery center 265 km away in Bhairahawa.

Pokhara and Chitwan Emergent Subregions with Growing Digital Infrastructure and Data Demand

Pokhara and Chitwan jointly contribute around 25% to the Nepal Data Center Storage Market, supported by rising regional enterprises and tech adoption. These cities have witnessed increased internet penetration and e-governance rollouts in recent years. Pokhara’s education and tourism sectors require content storage and regional CDN support. Chitwan benefits from healthcare and agriculture digitization programs. Both regions attract medium-scale storage deployments with NAS and cloud-based models. Their contribution is set to rise with decentralization policies.

Other Provinces Including Butwal, Biratnagar, and Nepalgunj Showing Early-Stage Growth

Remaining provinces collectively account for about 15% of the Nepal Data Center Storage Market. These include zones like Butwal, Biratnagar, and Nepalgunj, where state-level IT infrastructure and telecom services are improving. Local governments are establishing basic digital services, pushing demand for secure, edge-ready storage. However, limitations in power, land, and skilled personnel slow rapid growth. These regions represent long-term potential for micro data center expansion and modular storage offerings.

- For instance, DataWorld provides 9+ strategically located data centers across Nepal, including provincial areas, ensuring reliable storage networks as highlighted in their December 2025 updates.

Competitive Insights:

- WorldLink Data Center

- Nepal Telecom Data Center

- NEC Corporation

- NetApp

- IBM Corporation

- Dell Technologies

- Quantum Corporation

- Cisco Systems, Inc.

- DataDirect Networks

- Hitachi Vantara

The Nepal Data Center Storage Market features a mix of domestic operators and global technology providers. WorldLink and Nepal Telecom anchor the local ecosystem with colocation and cloud-based storage tailored to national infrastructure. Global players such as NetApp, IBM, and Dell offer advanced platforms for flash, hybrid, and software-defined storage, supporting enterprise and telecom clients. Cisco and DataDirect Networks enable high-performance deployments across BFSI and IT workloads. The market remains fragmented but is consolidating around value-added services like DRaaS, NVMe adoption, and SDS platforms. Vendors compete by offering localized support, integration with analytics, and energy-efficient solutions. Partnerships with public entities and local MSPs strengthen go-to-market strategies. It shows growing maturity, driven by regulatory alignment, startup demand, and hybrid architecture investments.

Recent Developments:

- In July 2025, IFC, alongside Standard Chartered Bank Nepal Limited, committed $29 million to WorldLink Communications and its subsidiary Data World Limited to expand fiber networks and data centers across Nepal, aiming to bridge the digital divide and foster economic growth.

- In February 2025, WorldLink Communications launched a new 3.5MW data center in Chandragiri, Kathmandu, featuring 520 racks and carrier-neutral operations to support Nepal’s growing data storage needs.

- In January 2025, Huawei signed a Letter of Intent with Nepal Telecom to build a NPR 484 million ($3.5m) primary data center in Kathmandu and a disaster recovery center in Bhairahawa.