Executive summary:

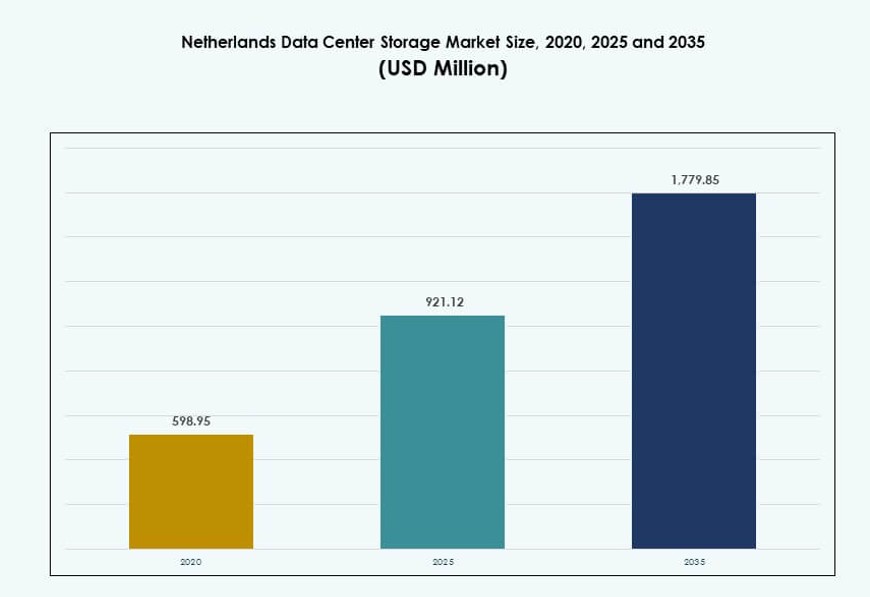

The Netherlands Data Center Storage Market size was valued at USD 598.95 million in 2020 to USD 921.12 million in 2025 and is anticipated to reach USD 1,779.85 million by 2035, at a CAGR of 6.75% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Netherlands Data Center Storage Market Size 2025 |

USD 921.12 Million |

| Netherlands Data Center Storage Market, CAGR |

6.75% |

| Netherlands Data Center Storage Market Size 2035 |

USD 1,779.85 Million |

Enterprises across the Netherlands are investing in high-performance, scalable storage to support cloud-native applications, virtualization, and real-time analytics. The shift toward AI and edge computing is creating demand for low-latency and resilient storage infrastructure. Businesses are modernizing with hybrid and all-flash solutions that improve speed, compliance, and security. Storage-as-a-Service models and software-defined platforms are gaining traction. The market plays a vital role in enabling digital transformation, operational agility, and regulatory alignment for enterprise and public sector workloads.

Amsterdam remains the dominant storage hub due to its extensive subsea connectivity, colocation density, and proximity to hyperscalers. The Randstad region, including Rotterdam and Utrecht, is emerging as a strong secondary cluster driven by enterprise cloud adoption and smart city infrastructure. Northern areas like Groningen are growing steadily, supported by hyperscale projects and renewable energy integration, expanding the geographic spread of the Netherlands Data Center Storage Market.

Market Dynamics:

Market Drivers

Strong Cloud Computing Backbone Boosting Shift from Traditional to Modern Storage Solutions

The Netherlands Data Center Storage Market benefits from the country’s established cloud-first digital policies and infrastructure readiness. Businesses are shifting from legacy storage toward scalable, high-speed storage systems compatible with virtualized and cloud-native workloads. Public and private enterprises seek faster access, reduced latency, and storage flexibility to meet rising digital demand. The government’s support for digital transformation programs accelerates hybrid and multi-cloud storage rollouts. Tech vendors launch advanced storage platforms integrating AI-based automation to manage growing unstructured data. Enterprises prioritize storage architectures that scale with data center performance and energy efficiency. The market’s importance increases with rising storage demand from sectors like finance, telecom, and healthcare. Investors see strong growth potential in software-defined storage and NVMe-based platforms.

Rapid Digitalization of Enterprises Leading to New Storage Workload Patterns

Across industries, Dutch companies are accelerating their digital journey through cloud apps, smart devices, and IoT integration. These transformations increase storage requirements, especially for handling streaming data, AI workloads, and analytics in real time. Enterprises demand infrastructure that offers low-latency performance, storage tiering, and seamless disaster recovery. New-age applications require storage systems to support multi-protocol access and flexible scalability. Data center operators offer all-flash and hybrid arrays to meet these expectations. BFSI and healthcare sectors, bound by data compliance regulations, adopt secure on-prem or hybrid storage deployments. This creates an opportunity for vendors offering encryption, backup, and deduplication tools. Continuous IT modernization fosters demand for integrated solutions rather than siloed storage models.

- For instance, Leaseweb has offered its scalable object storage solution from the Netherlands, supporting S3‑compatible object storage that lets businesses store and retrieve massive unstructured datasets with high durability and availability. This supports real‑time application data delivery and flexible capacity management.

Emergence of Edge Storage Needs with Growth in Smart Cities and Remote Connectivity

Smart city development across Dutch municipalities is driving distributed infrastructure needs. From traffic monitoring to public safety systems, edge computing increases reliance on low-latency, decentralized storage. IoT networks and video surveillance deployments push storage closer to the data source. Businesses invest in micro data centers with ruggedized, compact storage units. Telecom firms scale 5G networks, which demand intelligent storage closer to mobile base stations. These edge workloads often rely on hyperconverged or software-defined solutions. The growing remote workforce trend boosts localized cloud access and secure backup needs. Vendors develop storage appliances supporting lightweight AI inference at the edge. As cities digitize further, efficient and scalable storage becomes mission-critical.

Government-Led Digital Policy Frameworks and Compliance-Driven Modernization Push

The Netherlands government has launched initiatives focused on cybersecurity, digital infrastructure resilience, and data localization. Enterprises modernize storage infrastructure to align with the EU’s data privacy mandates and sustainability goals. Regulatory frameworks like GDPR increase demand for auditable, secure storage systems. Green storage solutions also see growth as data centers aim to meet energy benchmarks. Hardware vendors integrate energy-efficient SSDs and liquid-cooled drives into their offerings. The government’s commitment to expanding broadband coverage further supports rural digital infrastructure. Public sector institutions also migrate to secure, high-availability private cloud systems. Collaboration between tech vendors and government agencies leads to customized solutions for sensitive workloads.

- For instance, Microsoft has acquired 50 hectares of land in Middenmeer to expand its Netherlands data center campus, which supports local cloud and storage infrastructure growth and shows government and industry alignment on sovereign digital capacity.

Market Trends

Rising Adoption of All-Flash Arrays in Hyperscale and Enterprise Data Centers

All-flash storage continues gaining traction due to declining costs and performance advantages over HDDs. Enterprise workloads now demand faster read/write speeds and better IOPS, driving the shift to SSD-based arrays. Hyperscalers deploying in Amsterdam and nearby regions prefer flash systems for their AI and analytics platforms. Vendors offer flash-based NVMe systems with improved endurance and lower energy use. Financial institutions and e-commerce players upgrade to flash storage for real-time transaction processing. Healthcare and research centers adopt it for imaging and genomic analysis. Green data centers promote flash for its lower cooling and space needs.

Shift Toward Hyperconverged Infrastructure (HCI) with Embedded Storage Features

Dutch enterprises explore hyperconverged solutions to simplify operations and improve resource efficiency. HCI integrates compute, networking, and storage into a single, scalable unit. These solutions help businesses reduce hardware footprints and centralize IT management. Storage becomes software-defined and policy-driven in these models. Vendors promote HCI platforms optimized for VDI, ERP, and private cloud use cases. Startups and SMEs prefer HCI for its plug-and-play capabilities and lower setup cost. Telecom and media firms adopt it for content delivery and unified backup.

Growing Preference for Object-Based Storage for Archival and Unstructured Data

Object storage adoption is growing as firms deal with increasing volumes of unstructured content. Enterprises prefer it for archiving multimedia, medical records, IoT logs, and analytics backups. Object storage systems offer scalability and retrieval flexibility compared to traditional file or block systems. Cloud-native startups in the Netherlands use object storage for hosting scalable SaaS applications. Public agencies adopt it for digital record preservation and large dataset storage. Media companies use object stores to archive high-resolution video content for future reprocessing. Open-source platforms also expand use of object APIs across backup and container storage.

Growth in Managed Storage Services Driven by Complexity and Talent Shortage

More enterprises opt for managed or Storage-as-a-Service models to avoid infrastructure maintenance burdens. These services cover capacity planning, tiered storage, data migration, and security updates. Providers deliver SLAs tied to performance, compliance, and uptime. Businesses avoid upfront CAPEX by shifting to monthly OPEX-based models. This is especially appealing to mid-sized companies lacking in-house storage specialists. Managed storage is bundled with disaster recovery and backup-as-a-service. It supports fast provisioning of capacity for seasonal or project-based workloads.

Market Challenges

Escalating Energy Demand and Sustainability Concerns Impact Storage Infrastructure Expansion

The expansion of storage capacity in Dutch data centers increases overall power consumption, posing a key challenge. High-density storage arrays and flash systems require optimized power and thermal management. Energy-efficient designs are crucial to comply with local and EU-level carbon reduction targets. Operators must invest in liquid cooling or immersion solutions to manage heat from high-performance storage devices. The cost of deploying green storage solutions remains high for mid-market players. Energy shortages in peak periods can affect continuous operation of large storage clusters. Government pressure to improve PUE scores impacts storage system configuration choices. Meeting sustainability benchmarks while delivering high performance adds complexity. The Netherlands Data Center Storage Market must align energy usage with environmental standards to sustain growth.

Rising Data Protection Mandates and Risk of Compliance Violations

Data protection laws across Europe place heavy compliance responsibilities on storage infrastructure. GDPR and evolving local mandates require secure data handling, retention policies, and breach response plans. Storage vendors must embed encryption, access control, and audit features into their offerings. Businesses handling cross-border data must adopt geo-redundant and regulatory-aware storage solutions. A single compliance gap can lead to reputational damage and legal penalties. Managing sensitive workloads across hybrid or multi-cloud environments further increases complexity. Legacy systems without compliance readiness pose upgrade burdens. The Netherlands Data Center Storage Market faces the challenge of balancing agility with growing regulatory scrutiny.

Market Opportunities

Expansion of AI Workloads Creates Demand for Low-Latency and Tiered Storage Architectures

AI and ML adoption is rising across logistics, healthcare, and public services in the Netherlands. These workloads need rapid data access, parallel processing, and scalable capacity. Vendors offering GPU-optimized storage with AI-ready platforms see strong interest. Tiered storage solutions combining SSDs, object stores, and backup support diversified workloads. The Netherlands Data Center Storage Market will grow as more enterprises invest in AI-led digital transformation.

Colocation and Hybrid Cloud Providers Driving Storage-as-a-Service Growth

Colocation operators expand partnerships with storage vendors to offer pay-per-use models. These services appeal to enterprises looking for flexibility, security, and scalability without hardware ownership. Integration of backup, DR, and file sharing into managed storage boosts customer value. The Netherlands Data Center Storage Market benefits from this shift toward opex-driven infrastructure strategies.

Market Segmentation

By Storage Type

All-Flash Storage leads the segment due to its speed, efficiency, and adoption in AI-heavy and transaction-intensive workloads. Hybrid Storage follows closely, offering a cost-effective balance for mixed workloads. Traditional storage holds a declining but steady presence in backup and archival use cases. The Netherlands Data Center Storage Market shows strong movement toward flash-based and hybrid configurations that optimize performance and cost.

By Storage Deployment

Storage Area Network (SAN) systems dominate due to their reliability and speed in handling critical enterprise applications. Network-attached Storage (NAS) gains traction in content-heavy sectors like media and education. Direct-attached Storage (DAS) continues serving edge sites and remote facilities. The Netherlands Data Center Storage Market sees growing adoption of SAN and NAS in virtualized environments.

By Component

Hardware contributes the majority share, driven by investment in physical arrays, drives, and enclosures. Software components, including management and virtualization tools, are gaining fast due to automation and control needs. The Netherlands Data Center Storage Market emphasizes smart software layers to enhance hardware performance and security.

By Medium

Solid-State Drives (SSD) lead the medium segment owing to their superior performance and durability. HDDs still maintain relevance for backup and archival needs due to cost-efficiency. Tape storage continues to serve niche use in large-scale cold storage setups. The Netherlands Data Center Storage Market witnesses steady SSD growth across performance-critical sectors.

By Deployment Model

Cloud-based storage models are growing fast due to scalability and remote access support. Hybrid models are most preferred for combining control with flexibility. On-premises deployments remain important in sectors with strict compliance needs. The Netherlands Data Center Storage Market sees hybrid setups becoming standard across industries.

By Application

IT and Telecommunications account for the largest share, driven by growing cloud and mobile data demands. BFSI follows due to its need for secure, low-latency storage for real-time processing. Government and healthcare sectors invest in compliance-ready and encrypted systems. The Netherlands Data Center Storage Market expands across public and private use cases, with IT and BFSI leading adoption.

Regional Insights

Amsterdam Metropolitan Area Dominates with Over 60% Market Share

Amsterdam leads the Netherlands Data Center Storage Market, fueled by hyperscale activity, submarine cable access, and cloud data center clusters. The region is home to Europe’s largest internet exchange points and a high concentration of tech firms. Government-backed digital hubs and R&D zones further attract storage investment. Amsterdam’s strategic location and energy infrastructure support large-scale deployments. It remains the primary entry point for international cloud and storage providers in the country.

- For instance, Digital Realty and Equinix operate large multi-tenant campuses in Amsterdam that host high-availability storage infrastructure connected to over 100 network service providers and global cloud platforms.

Randstad Region Emerging as the Second Growth Cluster with ~25% Share

The Randstad region, including The Hague, Rotterdam, and Utrecht, shows fast growth. Enterprises from finance, public administration, and logistics sectors invest in hybrid cloud storage systems. Colocation providers and telcos expand data centers beyond Amsterdam to serve regional needs. The area benefits from fiber connectivity, enterprise density, and 5G expansion. It supports decentralized storage demand and business continuity strategies.

- For instance, the IOEMA subsea cable selected Greenhouse Datacenters in Westland as its Dutch landing point, strengthening international connectivity between the Netherlands, UK, Germany, Denmark, and Norway. The project enhances regional data flow and supports AI-ready, high-capacity workloads across Northern Europe.

Northern and Eastern Netherlands Represent Niche Growth Zones (~15%)

Cities like Groningen and Enschede contribute through edge data centers, university research infrastructure, and smart city projects. These regions host local ISPs, academic networks, and public cloud users. Infrastructure expansion is slower compared to the west but growing steadily. Green energy availability and lower land costs attract some operators. The Netherlands Data Center Storage Market finds long-term growth potential in these emerging regions.

Competitive Insights:

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- IBM Corporation

- NetApp

- Seagate Technology

- Cisco Systems, Inc.

- Veeam Software

- Lenovo Group

- Interxion

- NorthC Datacenters

The Netherlands Data Center Storage Market features a strong mix of global OEMs, cloud-centric innovators, and regional colocation providers. Dell Technologies, HPE, IBM, and NetApp lead with comprehensive product portfolios in all-flash, hybrid, and software-defined storage systems. Cisco and Lenovo maintain a competitive edge with integrated infrastructure and edge storage solutions. Seagate and Veeam specialize in data protection, backup, and storage media offerings. Interxion and NorthC Datacenters focus on managed and colocation-based storage solutions across strategic Dutch hubs. Competitive intensity remains high, with players leveraging sustainability, NVMe-based performance, and hybrid cloud enablement to expand share. The Netherlands Data Center Storage Market continues evolving around service-driven models, AI-ready platforms, and vendor collaborations targeting sector-specific needs.

Recent Developments:

- In December 2025, Antin Infrastructure Partners announced the acquisition of NorthC Datacenters, covering 25 colocation sites across the Netherlands, Germany, and Switzerland, with over 140 MW of grid capacity targeting enterprise storage users.

- In November 2025, Digital Realty expanded its presence in the Netherlands by launching an AI-optimized data center to meet high-performance storage demand across enterprise and hyperscale users.

- In November 2025, Google opened a new AI-focused data center in Winschoten, Groningen, increasing cloud storage and compute capacity in the northern Netherlands.

- In September 2025, NorthC Datacenters completed the acquisition of six data centers from Colt Technology Services, adding over 25 MW of capacity and strengthening its footprint in Amsterdam and the broader Benelux and DACH regions.

- In June 2025, Hewlett Packard Enterprise secured a major storage deal with Digital Realty, deploying HPE Alletra Storage MP B10000 in 300+ global data centers with Dutch implementation support from Infradax.