Executive summary:

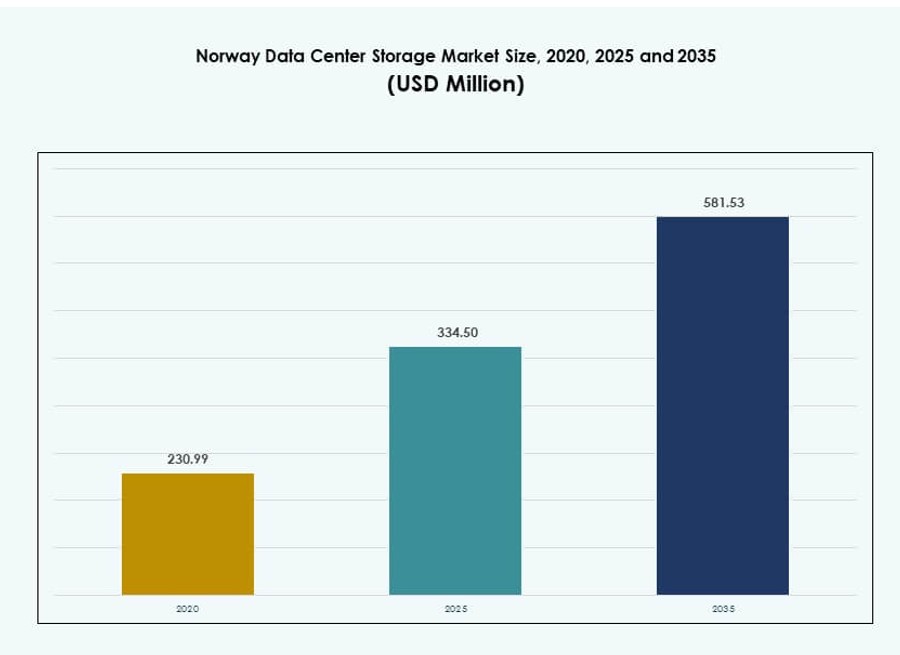

The Norway Data Center Storage Market size was valued at USD 230.99 million in 2020 to USD 334.50 million in 2025 and is anticipated to reach USD 581.53 million by 2035, at a CAGR of 5.63% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Norway Data Center Storage Market Size 2025 |

USD 334.50 Million |

| Norway Data Center Storage Market, CAGR |

5.63% |

| Norway Data Center Storage Market Size 2035 |

USD 581.53 Million |

The market is expanding as enterprises shift from legacy systems to advanced storage infrastructure. Increasing adoption of AI workloads, hybrid cloud models, and data compliance frameworks is driving demand for high-performance storage. Innovation in all-flash arrays, software-defined storage, and energy-efficient systems supports modernization goals. Public and private sector investments are focusing on secure, low-latency, and scalable solutions. Businesses view reliable storage as essential for digital transformation, operational continuity, and regulatory alignment.

Oslo and Eastern Norway dominate the market due to strong connectivity, high enterprise concentration, and hyperscale deployments. Western Norway is emerging rapidly, supported by green energy access and climate advantages for efficient operations. Northern and Central regions are gaining traction through edge deployments and public digitalization projects. Regional balance is shifting toward sustainable, distributed, and scalable storage strategies across the country.

Market Dynamics:

Market Drivers

Accelerated Digitalization Across Industries Driving Storage Infrastructure Transformation

Rapid digital transformation across banking, healthcare, and telecom sectors is triggering storage infrastructure upgrades. Businesses in Norway are moving away from legacy hardware toward scalable, high-performance storage systems. The surge in data from cloud-native apps, analytics, and IoT is fueling demand for resilient architectures. The Norway Data Center Storage Market is gaining strategic importance as enterprises need secure and fast data access. The shift supports software-defined storage, flash arrays, and virtualized environments. Public and private institutions now prioritize flexible infrastructure to support AI, automation, and real-time analytics. Government digitalization initiatives further reinforce demand. It benefits vendors offering advanced storage platforms. Enterprises view robust storage infrastructure as essential for operational agility and service continuity.

- For instance, Green Mountain’s Rennesøy facility supports NVMe flash arrays delivering up to 20 GB/s bandwidth for cloud-native workloads, as per their infrastructure specs for handling IoT data surges.

Green Data Center Policies and Abundant Renewable Energy Encouraging Sustainable Storage Deployment

Norway’s access to cost-effective hydropower and national carbon-neutral goals are influencing storage design. Energy efficiency in data centers is not limited to cooling but extends to storage systems as well. Storage platforms with lower power consumption and optimized data management are in demand. This energy advantage attracts hyperscale firms and multinational enterprises looking for sustainable infrastructure. It enhances the Norway Data Center Storage Market’s appeal to global investors focused on ESG metrics. The country’s climate policy creates competitive differentiation for energy-conscious storage deployment. Vendors offering low-emission storage solutions benefit from favorable regulatory alignment. It supports innovation in power-efficient SSDs and software-defined management. Demand grows for integrated platforms balancing performance with environmental impact.

Surge in AI, Edge Computing, and Industry 4.0 Initiatives Fueling Need for High-Speed Storage Systems

Edge computing and AI workloads are increasing across logistics, manufacturing, and energy sectors. These applications require fast, low-latency access to distributed data. It is pushing enterprises to adopt NVMe-based storage, hyperconverged infrastructure, and real-time replication. The Norway Data Center Storage Market supports these needs with innovation in high-throughput systems. Businesses are deploying edge data centers connected to regional hubs. Industrial clusters with automated workflows need high-performance storage for critical operations. AI models require fast read-write operations and multi-node sharing. Demand grows for flash-based and hybrid setups with AI-optimized software stacks. These trends place storage modernization at the core of next-gen IT infrastructure.

Evolving Regulatory Frameworks and Data Sovereignty Norms Enhancing Local Storage Infrastructure Investments

Tightening data protection laws in Europe are impacting storage choices across sectors. Enterprises are hosting critical workloads within national borders to comply with GDPR and local mandates. The Norway Data Center Storage Market benefits from investor trust and regulatory clarity. National strategies emphasize domestic infrastructure, enhancing on-premise and hybrid adoption. Businesses in BFSI, healthcare, and government prefer localized control over sensitive data. Vendors offer encrypted, scalable storage solutions with compliance-ready architecture. This drives interest in secure cloud-native storage hosted in Norwegian facilities. It attracts clients requiring transparency, low-risk storage models, and long-term infrastructure control. It helps build digital resilience through trustworthy and compliant data handling.

- For instance, Lefdal Mine Datacenter in Norway supports GDPR-compliant storage environments tailored for sensitive sectors like healthcare, using modular infrastructure and renewable power. Its secure underground location and vendor-neutral design enable deployment of scalable storage solutions, including NAS and high-density racks.

Market Trends

Adoption of All-Flash Storage Systems Accelerating to Meet High-Throughput and Low-Latency Demands

Organizations in Norway are increasingly replacing traditional spinning drives with all-flash arrays. It delivers faster IOPS, reduced latency, and improved durability for modern workloads. AI and real-time analytics place high demands on storage response times. This shift enhances performance for dynamic enterprise environments. Flash solutions offer better scalability and space optimization. The Norway Data Center Storage Market is witnessing a gradual dominance of SSDs over HDDs. It aligns with operational priorities like speed, uptime, and compactness. The reduced energy footprint of flash drives also supports green computing goals. Businesses gain from higher reliability, performance consistency, and maintenance efficiency.

Shift Toward Software-Defined Storage Solutions Improving Resource Efficiency and Hybrid Cloud Flexibility

The decoupling of storage hardware and software is transforming infrastructure planning across enterprises. Software-defined storage (SDS) enables centralized control, dynamic provisioning, and seamless scalability. Organizations seek flexibility to manage data across on-premises and cloud environments. The Norway Data Center Storage Market benefits from SDS integration into hyperconverged and multi-cloud architectures. It empowers IT teams with automation and simplified data lifecycle management. Cost predictability and vendor independence also drive adoption. Vendors now offer SDS solutions tailored for AI, backup, and multi-tier storage. It helps enterprises standardize policies, ensure availability, and avoid data silos. SDS promotes agile, cost-efficient data infrastructure.

Hybrid Cloud Storage Models Gaining Traction for Workload Distribution and Regulatory Compliance

Enterprises are adopting hybrid models to combine control of private infrastructure with cloud scalability. Workloads are being distributed based on data sensitivity, latency needs, and compliance. Critical data remains on-site while less sensitive data moves to public cloud. The Norway Data Center Storage Market supports these setups with secure, integrated storage platforms. Vendors provide unified storage with policy-based tiering across multiple environments. This model balances cost, speed, and control for Norwegian businesses. It enables disaster recovery, workload migration, and seamless hybrid operations. Compliance concerns further reinforce hybrid preference for healthcare, BFSI, and public sector workloads.

Growing Demand for Cold Storage Solutions for Archival, Backup, and Compliance Requirements

Long-term data retention is becoming critical across regulated sectors. Organizations require reliable, cost-effective solutions for infrequently accessed data. Cold storage, including tape and low-cost HDDs, supports backup, recovery, and audit trails. The Norway Data Center Storage Market sees demand rise from government, legal, and research entities. Cold storage complements active storage with low energy consumption and extended durability. Vendors are integrating tape libraries and archival platforms with cloud connectivity. It enables air-gapped security and immutable backups. Enterprises benefit from reduced storage costs and improved compliance posture. It plays a vital role in data protection strategies and ransomware mitigation.

Market Challenges

High Cost of Storage Infrastructure Upgrades Limiting Adoption Among Mid-Sized Enterprises

The cost of adopting advanced storage technologies remains a key barrier for smaller businesses. Flash arrays, hyperconverged systems, and SDS platforms require significant upfront investments. This challenge is particularly visible in sectors with constrained IT budgets. The Norway Data Center Storage Market faces slower penetration of cutting-edge solutions in SMEs. It hinders full-scale modernization and delays migration from legacy storage. Licensing costs and integration complexity add to the burden. Vendors must address this gap through scalable, modular, and affordable models. Without financial flexibility, smaller enterprises risk operational inefficiencies. It creates a divide between innovation leaders and lagging segments.

Shortage of Local Data Storage Talent and Complex System Integration Delaying Enterprise Deployments

Managing modern storage environments requires expertise in hybrid cloud, SDS, and security protocols. Norway faces a skills shortage in storage management and data operations. Enterprises struggle with designing and maintaining compliant and resilient architectures. This shortage slows rollout of storage upgrades across sectors. The Norway Data Center Storage Market depends on local talent for long-term infrastructure sustainability. Integration across legacy and modern platforms adds complexity. Training requirements and support challenges limit the pace of adoption. Vendors must invest in knowledge transfer, localized support, and automation. Without skilled professionals, enterprises may underutilize advanced storage solutions.

Market Opportunities

Rising AI, HPC, and Research Investments Creating Demand for High-Performance, Scalable Storage Systems

Norway’s investments in research, life sciences, and high-performance computing are growing steadily. These sectors generate large volumes of structured and unstructured data. The Norway Data Center Storage Market can serve this need with high-capacity, low-latency systems. Vendors offering scalable and parallel storage platforms gain a competitive edge. Purpose-built flash arrays and NVMe fabrics enable breakthroughs in simulation and deep learning. It opens growth avenues in enterprise and academic deployments.

Colocation and Edge Deployments Offering Expansion Paths for Storage Providers in Regional Hubs

Emerging edge locations outside Oslo are creating new demand for distributed storage setups. Industries require fast access to localized data for logistics, monitoring, and automation. The Norway Data Center Storage Market benefits from colocation facilities expanding to these zones. Providers offering modular, energy-efficient, and rugged storage infrastructure can tap into this shift. Edge-to-core integration enhances data visibility, redundancy, and disaster recovery. It allows storage vendors to diversify footprints and strengthen market presence.

Market Segmentation

By Storage Type

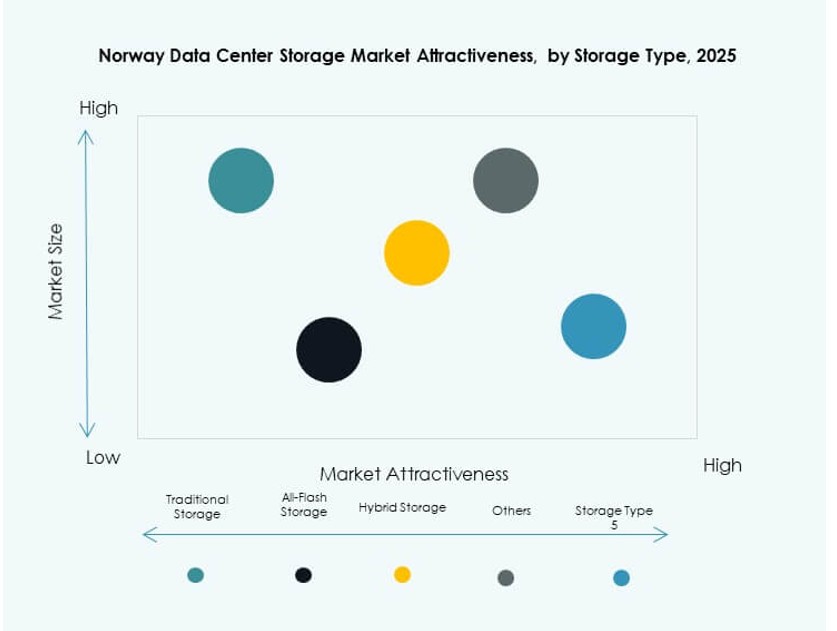

The Norway Data Center Storage Market is segmented into traditional, all-flash, hybrid, and other storage types. All-flash storage is gaining momentum due to its speed, reliability, and energy efficiency. It dominates high-performance and mission-critical applications across enterprise and research sectors. Hybrid storage is also growing as it balances performance with cost efficiency. Traditional HDD-based systems still support archival and backup functions in cost-sensitive deployments.

By Storage Deployment

Storage Area Network (SAN) systems hold the largest share due to their use in high-speed enterprise applications. They are preferred in BFSI, healthcare, and telecom workloads for their performance and reliability. Network-attached Storage (NAS) is growing in mid-sized enterprises and edge locations for its scalability and simplicity. Direct-attached Storage (DAS) remains relevant in cost-sensitive or single-server deployments across smaller setups.

By Component

Hardware holds the majority share in the Norway Data Center Storage Market, including drives, enclosures, and racks. Enterprises invest heavily in physical infrastructure to ensure durability and performance. However, software components, including SDS platforms and analytics, are rising in importance. Software enhances control, security, and optimization across hybrid and multi-cloud storage environments.

By Medium

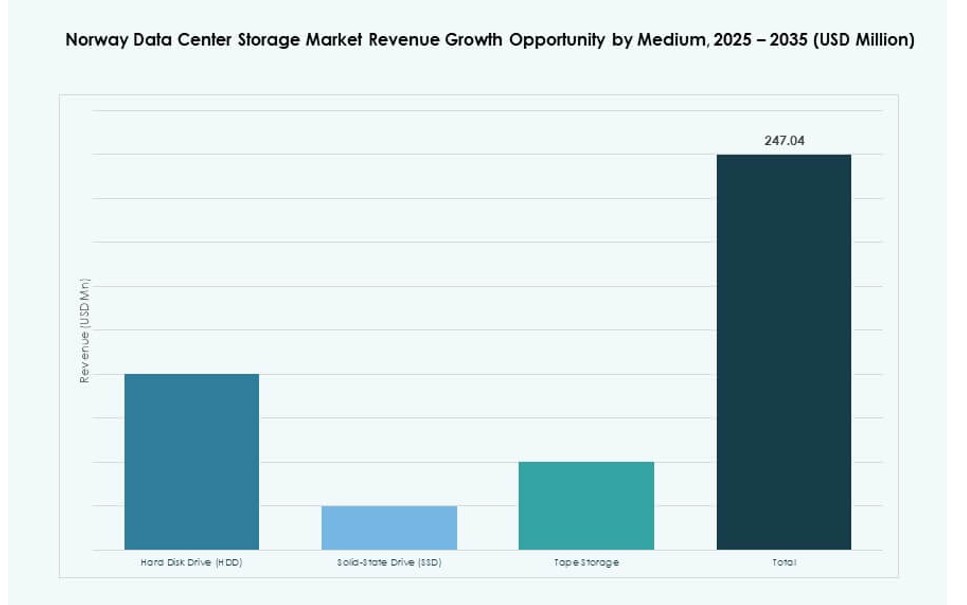

Solid-State Drives (SSDs) dominate due to their high-speed performance, low latency, and power efficiency. They are crucial in AI, analytics, and virtualized environments. Hard Disk Drives (HDDs) retain relevance for archival and bulk storage due to their lower cost per TB. Tape storage is used in government and research for long-term backup and cold storage needs, offering cost-effective compliance solutions.

By Deployment Model

Hybrid deployment models lead the market due to their flexibility, combining on-premise control with cloud scalability. On-premises setups are common in regulated sectors requiring full data control and compliance. Cloud-based storage is growing rapidly, especially in startups and service sectors, for its ease of deployment and cost optimization. The hybrid approach balances speed, security, and compliance for modern IT ecosystems.

By Application

The IT and Telecommunications sector dominates the Norway Data Center Storage Market with growing needs for uptime and digital services. BFSI is also a key segment due to strict compliance and backup requirements. Government entities demand secure and localized storage for e-governance and public data. Healthcare is growing due to imaging, EMRs, and compliance-driven needs. Other sectors include retail, manufacturing, and logistics, adopting storage for operational efficiency.

Regional Insights

Oslo and Eastern Norway Leading with Over 62% Share Due to Hyperscale Deployments and Dense Fiber Infrastructure

Oslo and the surrounding Eastern region form the core of the Norway Data Center Storage Market. The area benefits from proximity to government agencies, financial hubs, and top telecom providers. It hosts hyperscale and colocation facilities with access to green power and advanced connectivity. Enterprises prefer this region for secure, high-speed infrastructure. The regional market accounts for over 62% of total share, driven by stable power, regulatory clarity, and talent availability.

- For instance, Bulk Infrastructure’s OS-IX facility delivers 14 MW of redundant renewable power with over 60 carrier connections and water-cooled racks up to 50 kW per rack. Enterprises prefer this region for secure, high-speed infrastructure.

Western Norway Emerging as a Green Data Center Hub with Over 22% Share Focused on Sustainability

Western Norway is becoming a preferred zone for sustainable data center storage development. Abundant hydropower, favorable climate, and submarine cable landings enhance its appeal. The region is ideal for hosting green data centers with cold climate advantages. Bergen and surrounding cities are witnessing growth in colocation and edge deployments. Western Norway holds over 22% market share, and vendors focusing on energy efficiency benefit from this concentration.

Northern and Central Norway Recording Gradual Growth with a Combined Share of Around 16%

Northern and Central regions are experiencing moderate expansion, driven by edge computing and public sector digitalization. These areas benefit from improving connectivity and distributed computing needs in energy and fisheries. Though infrastructure is less dense than Oslo, local governments support decentralization. The combined market share of these regions is approximately 16%, with long-term potential in edge storage and localized data processing applications.

- For instance, Bitdeer’s Tydal campus provides 175 MW of hydro-powered capacity with immersion cooling. Though infrastructure is less dense than Oslo, local governments support decentralization.

Competitive Insights:

- Tietoevry

- Atea

- Basefarm

- Crayon

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- IBM Corporation

- NetApp

- Cisco Systems

- Cohesity

The Norway Data Center Storage Market features a mix of global and Nordic players offering advanced infrastructure and integrated services. Tietoevry, Atea, and Basefarm lead the domestic landscape with strong regional footprints and localized solutions. Global vendors like Dell Technologies, IBM, and HPE offer scalable hardware and hybrid storage platforms. NetApp and Cohesity focus on software-defined storage and data management, while Cisco supports hyperconverged and SAN deployments. The competitive landscape emphasizes energy efficiency, regulatory compliance, and AI-ready storage systems. It drives innovation in flash arrays, SDS, and hybrid models tailored for enterprise and public sector clients. Players focus on sustainability, service reliability, and performance optimization to strengthen market share.

Recent Developments:

- In December 2025, Tietoevry partnered with Roaring through its Data Nest platform, enabling the insights firm to expand data product sales in Norway.

- In October 2025, Tietoevry Industry signed a multi-country agreement with Entercard to deliver multichannel services and digital transformation support across Norway and other Nordics, valued at EUR 15-17 million over five years.