Executive summary:

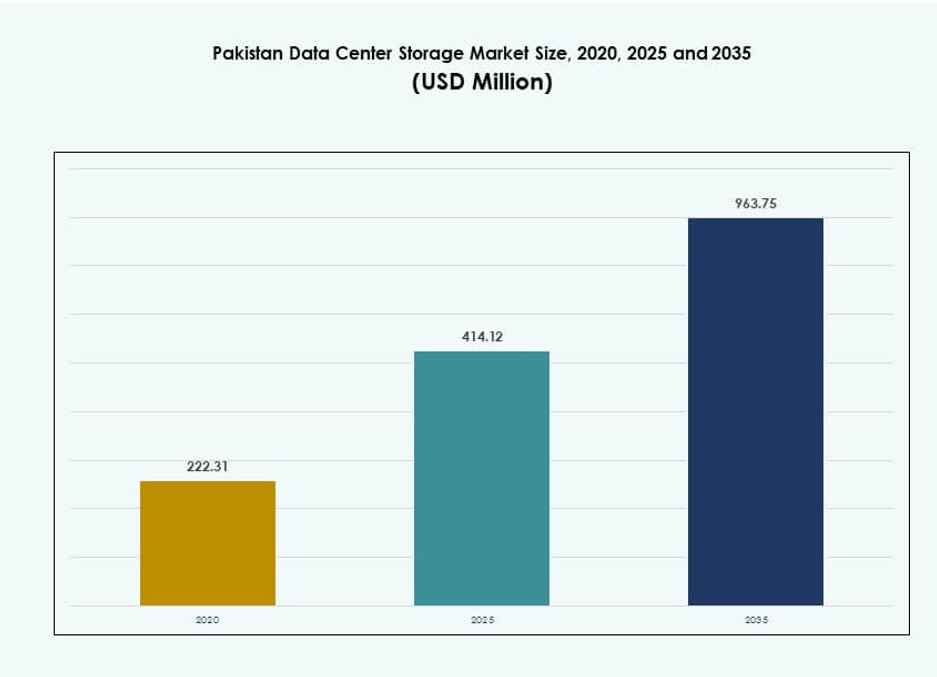

The Pakistan Data Center Storage Market size was valued at USD 222.31 million in 2020 to USD 414.12 million in 2025 and is anticipated to reach USD 963.75 million by 2035, at a CAGR of 8.73% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Pakistan Data Center Storage Market Size 2025 |

USD 414.12 Million |

| Pakistan Data Center Storage Market, CAGR |

8.73% |

| Pakistan Data Center Storage Market Size 2035 |

USD 963.75 Million |

The market is advancing rapidly due to the expansion of digital services, sovereign cloud initiatives, and rising enterprise data volumes. Telecom operators, BFSI firms, and public institutions are upgrading infrastructure to meet compliance, availability, and scalability needs. Innovation in hybrid cloud, NVMe flash arrays, and software-defined storage is reshaping storage deployment models. AI-driven applications and analytics platforms further boost high-performance storage demand. Businesses and investors view the market as vital for enabling digital transformation, data security, and long-term operational efficiency across critical sectors.

Karachi leads market share due to its submarine cable access, financial sector presence, and commercial infrastructure. Islamabad is gaining prominence through public cloud projects and federal agency deployments. Lahore shows strong momentum, driven by SME digitization, startup activity, and education-led IT adoption. Emerging cities like Faisalabad and Peshawar are witnessing early investments in edge and hybrid infrastructure. This regional spread strengthens national data sovereignty and supports a balanced, multi-city storage ecosystem.

Market Dynamics:

Market Drivers

Government-Led Digital Transformation and Data Sovereignty Efforts Fueling Infrastructure Demand

The Pakistan Data Center Storage Market is growing due to government-backed digitalization. Programs such as “Digital Pakistan” are pushing agencies toward cloud-first strategies. Public sector reforms require secure and compliant data storage. New laws around data localization and sovereignty increase demand for in-country infrastructure. These regulations affect healthcare, banking, and defense sectors. The push for secure public service delivery platforms is transforming how storage is deployed. It drives both capacity expansion and modernization of legacy systems. Enterprises now prefer domestic cloud and hybrid setups for regulated workloads. This shift strengthens the storage market’s strategic importance.

- For instance, in November 2025, Telenor Pakistan entered a strategic partnership with Data Vault Pakistan to explore sovereign AI cloud infrastructure, aiming to host secure, onshore data services compliant with SBP and PTA regulations for sectors such as finance, telecom, and healthcare.

Enterprise Cloud Adoption Accelerating Storage Demand in Financial, Telecom, and Retail Sectors

Cloud transformation among large enterprises is a major storage driver. Telecom operators, fintech platforms, and digital-first retailers are scaling operations. AI-based analytics, e-commerce logistics, and financial transactions require high-throughput storage. Real-time data access and secure backups are now business-critical. Demand is shifting to all-flash arrays and SAN-based deployments for high availability. Pakistan’s growing digital economy expands the role of data centers across verticals. Enterprises see localized storage as essential for service delivery and latency control. Regulatory pressure on data compliance increases cloud investments. It makes the Pakistan Data Center Storage Market a strategic priority.

- For instance, PTCL partnered with DWP Technologies in 2025 to modernize its data centers using Dell’s enterprise storage solutions, supporting software-defined infrastructure upgrades across core telecom workloads.

Rise of OTT, E-Learning, and Streaming Platforms Driving Edge Storage and Content Caching

Streaming platforms and digital education tools contribute to rising data generation. Platforms require localized storage nodes to reduce latency and manage peak loads. OTT services are deploying content delivery networks across metro hubs. E-learning platforms store vast educational content across regional facilities. It pushes demand for hybrid storage and scalable NAS solutions. Cities like Karachi and Lahore lead in deployment of edge caching infrastructure. Content replication and disaster recovery become central to digital experience. Telecom operators are integrating storage with media delivery systems. It enables real-time access, making localized storage a high-growth need.

Startup Ecosystem, SME Digitization, and Local Hosting Mandates Encouraging Affordable Storage Solutions

The startup ecosystem and SME digitization create a distinct need for scalable, affordable storage. Small enterprises need secure, on-demand data access without high capex. This drives adoption of cloud-based, subscription-driven storage services. Local hosting mandates incentivize domestic deployment by service providers. The SME sector prefers hybrid storage linked to business management tools. Application performance depends on fast, secure access to customer and transaction data. Service providers bundle compute and storage into flexible packages. It supports business continuity and scalability without infrastructure burden. The Pakistan Data Center Storage Market benefits from this shift toward agile storage.

Market Trends

Growth of Tier III and Tier IV Certified Storage Facilities Across Major Urban and Industrial Zones

The Pakistan Data Center Storage Market is seeing an increase in Tier III and IV facilities. Urban centers are now home to high-availability data hubs supporting critical operations. These facilities include redundant storage arrays and modular systems. Karachi, Islamabad, and Lahore are witnessing dense facility clusters. Tier certifications help service finance, telecom, and government workloads. Uptime and compliance are central to deployment strategies. Businesses prefer certified storage environments for hosting regulated data. This trend is strengthening investment from local and international operators. It reshapes Pakistan’s digital infrastructure profile.

AI and Data Analytics Workloads Trigger Shift Toward High-Performance Flash and Object Storage

Emerging AI, machine learning, and analytics workloads are reshaping storage demands. Workloads require low-latency, high-speed access to structured and unstructured data. Enterprises adopt flash-based and object storage to manage large datasets efficiently. Edge AI deployments need distributed storage closer to data sources. Object storage supports scalability in data lakes and real-time processing. Startups and enterprises in health, retail, and logistics deploy AI-ready storage stacks. Cloud-native platforms integrate analytics and storage natively. The Pakistan Data Center Storage Market responds with customized storage tiers. It aligns performance with workload complexity.

Rising Demand for Storage-as-a-Service and Cloud-Native Platforms in Cost-Sensitive Deployments

Storage-as-a-Service models are gaining popularity among SMEs and startups. Businesses opt for opex models to avoid upfront hardware investment. Local cloud providers bundle compute, storage, and cybersecurity services. Cloud-native platforms offer scalability without complexity. Multitenant environments support small clients with secure data isolation. Subscription models help startups manage dynamic workloads. APIs simplify storage integration with business apps. This trend promotes agility and flexibility in infrastructure use. It makes the Pakistan Data Center Storage Market appealing for digital-native firms.

Disaster Recovery, Backup-as-a-Service, and Archival Solutions Expanding in BFSI and Public Sector

Disaster Recovery (DR) and backup services are rising in regulated sectors. BFSI and government institutions must meet strict data retention and recovery policies. Enterprises invest in backup-as-a-service to ensure business continuity. Tiered storage solutions support archival and quick recovery. Public cloud DR services support hybrid workloads with minimal downtime. Government agencies require secure storage for national records and digital identity. Cloud-based backup solutions reduce risk of ransomware and corruption. Compliance mandates enforce structured backup frameworks. This trend strengthens long-term demand in the Pakistan Data Center Storage Market.

Market Challenges

Limited Energy Reliability, Infrastructure Gaps, and Real Estate Constraints Affect Storage Expansion

The Pakistan Data Center Storage Market faces infrastructure-related bottlenecks. Power reliability remains a concern across metro and secondary regions. Storage facilities require continuous, stable power for uptime and data integrity. While backup systems are deployed, energy costs increase operational burden. Real estate availability in core zones like Karachi and Lahore is constrained. Rising property costs limit expansion for colocation and cloud providers. Network infrastructure in Tier-2 cities lacks redundancy and latency control. It hampers edge deployment and multi-zone failover planning. These gaps restrict national-level scalability in storage operations.

Shortage of Skilled Data Center Workforce and Cybersecurity Expertise Slows Technology Uptake

Human capital constraints present a challenge for the storage sector. Pakistan faces a shortfall in trained professionals for storage administration and data center operations. Specialized skills in SAN, NAS, and cloud-native storage management are in short supply. This limits the speed at which providers can deploy new architectures. Cybersecurity talent gaps impact deployment of secure storage environments. Enterprises delay migration to new platforms due to lack of technical support. Certification and training pipelines remain underdeveloped for critical storage technologies. It affects service quality and restricts confidence among enterprise customers. Workforce development must align with storage market growth.

Market Opportunities

National Data Hosting Regulations and Public Cloud Incentives Open Up New Storage Deployment Models

New regulations encouraging in-country data hosting open growth channels. Telecom and cloud providers can localize workloads for BFSI, public sector, and health. Government incentives promote local cloud stack development. Storage vendors expand services to meet compliance and data sovereignty needs. The Pakistan Data Center Storage Market supports flexible, scalable models for regulated sectors.

International Investment and Regional Interconnectivity Boost Cross-Border and Cloud Exchange Deployments

Cross-border data interconnectivity with Central and South Asia improves regional cloud access. Investments from Gulf and Chinese operators support hyperscale infrastructure. Pakistan becomes a hub for regional compute and storage spillover. This opens the door for carrier-neutral storage exchanges. Market players can build strategic peering and cloud exchange points.

Market Segmentation

By Storage Type

Traditional storage dominates in legacy deployments but is declining in favor of hybrid and all-flash solutions. All-flash storage is gaining traction for mission-critical workloads in finance and telecom. Hybrid storage balances performance and cost and sees broad adoption across SMEs. The Pakistan Data Center Storage Market shows growing demand for low-latency flash solutions.

By Storage Deployment

Storage Area Network (SAN) systems lead in performance-centric deployments, especially in BFSI and telecom. Network-attached Storage (NAS) systems are widely used in SMEs for scalability and ease of use. Direct-attached Storage (DAS) sees use in small private servers. SAN remains dominant in the Pakistan Data Center Storage Market due to reliability.

By Component

Hardware holds the largest share, driven by increasing deployment of physical storage arrays. Software-defined storage is gaining momentum in cloud-native environments. Vendors bundle storage software with hybrid infrastructure offerings. The Pakistan Data Center Storage Market reflects a shift toward intelligent, software-managed platform for scalability.

By Medium

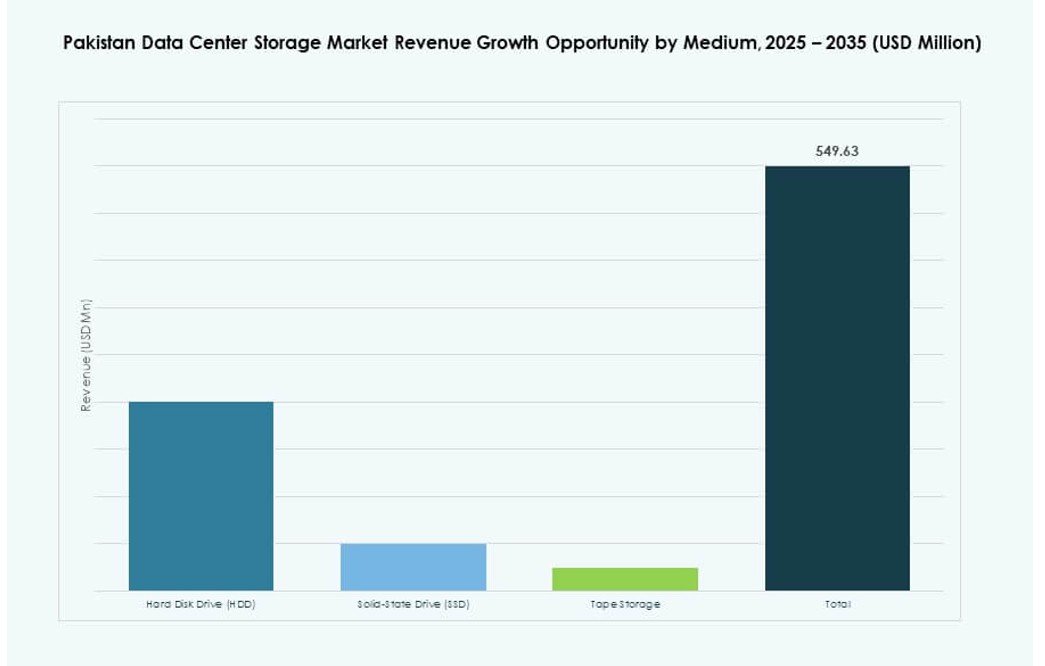

Hard Disk Drives (HDDs) still account for most deployments due to cost efficiency in bulk storage. Solid-State Drives (SSDs) gain share in performance-driven applications. Tape storage persists in archival use cases for compliance and cost-saving. SSD adoption is expected to rise in the Pakistan Data Center Storage Market.

By Deployment Model

On-premises deployment remains strong across public institutions and financial enterprises. Cloud-based deployment is rising among startups and agile enterprises. Hybrid models dominate where compliance meets scalability needs. The Pakistan Data Center Storage Market supports a mix of all three, with hybrid models growing fastest.

By Application

IT and telecom lead storage adoption due to high data throughput and SLA requirements. BFSI follows closely with secure storage needs for financial records and transactions. Government agencies drive sovereign storage mandates. Healthcare sees rising use of EMR and imaging solutions. The Pakistan Data Center Storage Market also supports retail, logistics, and education under the ‘others’ category.

Regional Insights

Karachi Leads with Over 40% Share Due to Submarine Cable Access and Financial Sector Demand

Karachi accounts for over 40% of the Pakistan Data Center Storage Market. The city benefits from proximity to international submarine cables and Tier III facilities. It serves banking, insurance, and enterprise clients needing low-latency and redundant storage. The commercial and telecom sectors drive storage deployments. Karachi’s industrial zones also use edge and hybrid setups. Strategic investments position it as the storage backbone of the country.

- For instance, PTCL’s Tier III-certified data center in Karachi offers hosting and disaster recovery services to major financial institutions, supported by direct connectivity to submarine cables like PEACE and SEA-ME-WE 5/6, which provide scalable international bandwidth infrastructure for Pakistan.

Islamabad Holds 30% Share Driven by Government Cloud and Public Sector Digitization

Islamabad contributes around 30% to the national market, led by e-governance programs and federal digital services. Sovereign cloud initiatives require secure, in-country storage solutions. Government agencies use compliant platforms with on-prem and hybrid infrastructure. Tier II and III facilities are expanding in Islamabad’s tech zones. Public sector demand ensures stable growth for localized storage. It plays a crucial role in digital public service delivery.

Lahore and Emerging Cities Account for 30% Market Share with SME and Startup Activity

Lahore and cities like Faisalabad and Peshawar together represent 30% of the market. Lahore’s startup ecosystem and SME base drive demand for flexible cloud storage. Local hosting and data analytics needs support infrastructure growth. Education and health digitization projects fuel backup and archival services. Faisalabad’s textile sector is investing in IT infrastructure. These cities contribute to decentralizing storage demand across Pakistan. The trend supports national-scale digital inclusion.

- For instance, the Punjab Information Technology Board deployed hyper-converged infrastructure in Lahore to power provincial digital services, integrating private cloud capacity to support platforms like e-governance portals, health systems, and citizen facilitation centers.

Competitive Insights:

- Pakistan Data Management Services

- Netsol Cloud

- Hewlett Packard Enterprise (HPE)

- NEC Corporation

- NetApp

- IBM Corporation

- Cisco Systems, Inc.

- Lenovo Group

- Toshiba Corporation

- Huawei Technologies Co., Ltd.

The Pakistan Data Center Storage Market features a mix of global technology providers and local players. Multinational companies like HPE, NetApp, IBM, and Cisco offer enterprise-grade solutions for SAN, NAS, and hybrid cloud storage. Their dominance is driven by partnerships with telecom, BFSI, and government clients. Local firms such as Netsol Cloud and Pakistan Data Management Services support demand for sovereign storage and localized hosting. Vendors focus on service bundling, workload-specific customization, and regulatory compliance. Product differentiation is increasing in NVMe, software-defined storage, and flash-based arrays. Competition remains intense, with ongoing upgrades in performance, security, and scalability across all deployments. The Pakistan Data Center Storage Market continues evolving as businesses adopt hybrid and AI-ready infrastructure.

Recent Developments:

- In December 2025, US-based data center operator Datarocx partnered with Pakistan’s Data Vault to establish advanced computing facilities in Karachi, enhancing the country’s data storage and AI infrastructure capabilities.

- In December 2025, Data Vault Pakistan announced a strategic partnership with Rafay Systems to launch Pakistan’s first Sovereign AI Cloud, providing a managed Kubernetes platform for local AI workloads in storage and high-performance computing.

- In October 2025, XDS DATACENTRE and Al Nahal IT Park & Data Center signed an agreement to develop Pakistan’s first AI Liquid Immersion Data Centre in Karachi, featuring a containerized solution for rapid deployment and disaster recovery.

- In December 2024, IBM Corporation partnered with Pakistan Telecommunication Company Limited (PTCL) and GBM Pakistan to modernize PTCL’s IT infrastructure, deploying IBM Power10 servers across production, high availability, and disaster recovery environments to enhance data management and scalability in Pakistan’s telecom data centers.