Executive summary:

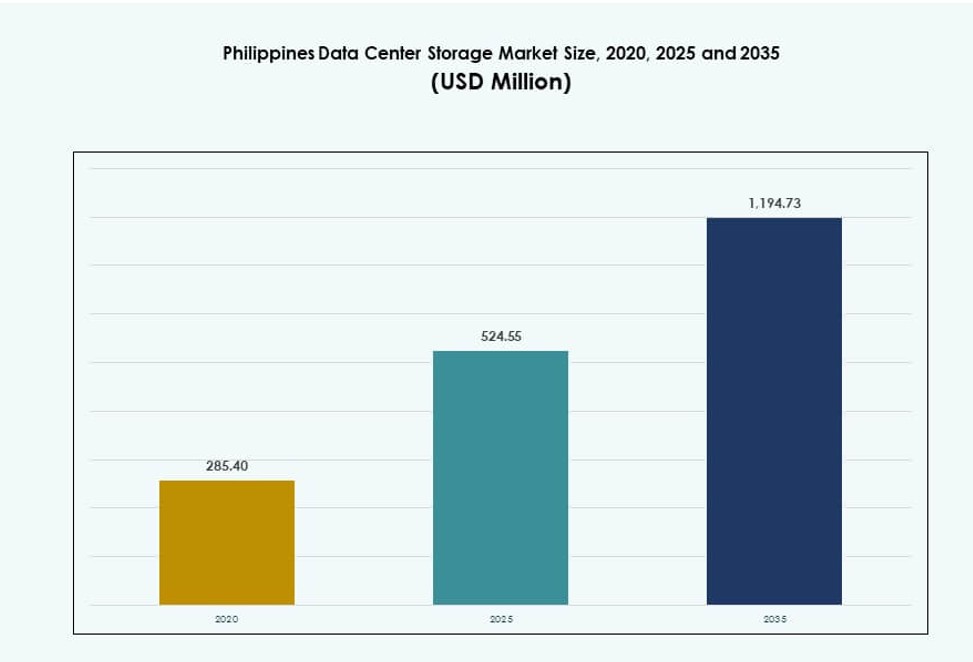

The Philippines Data Center Storage Market size was valued at USD 285.40 million in 2020 to USD 524.55 million in 2025 and is anticipated to reach USD 1,194.73 million by 2035, at a CAGR of 8.49% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Philippines Data Center Storage Market Size 2025 |

USD 524.55 Million |

| Philippines Data Center Storage Market, CAGR |

8.49% |

| Philippines Data Center Storage Market Size 2035 |

USD 1,194.73 Million |

The market is advancing due to rapid digitalization, strong enterprise cloud migration, and demand for low-latency, high-capacity storage systems. AI workloads, smart city programs, and growing fintech platforms are driving storage infrastructure modernization. Liquid-cooled and high-density deployments are increasing across colocation and hyperscale facilities. Businesses are investing in scalable, energy-efficient storage to meet evolving compliance and performance standards. Storage is now a strategic enabler of operational resilience and digital competitiveness.

Metro Manila leads with the highest share due to its advanced connectivity, skilled workforce, and concentration of enterprise and government demand. Cebu and Davao are emerging as secondary hubs, supported by improved fiber networks and localized infrastructure initiatives. Regional expansion aligns with smart city rollouts and increased digital activity in tier-two urban zones. These locations are gaining importance in supporting national storage capacity and enterprise continuity.

Market Dynamics:

Market Drivers

Digital Transformation and Rising Enterprise Workloads Across Key Sectors

The Philippines Data Center Storage Market is expanding due to rising demand from BFSI, e-commerce, telecom, and government sectors. Enterprises are upgrading legacy systems to handle larger datasets and meet compliance. High-volume storage is critical to support digital transactions, identity management, and data-driven decision-making. Edge computing initiatives are increasing localized storage needs in retail, healthcare, and logistics. Cloud service providers are enhancing storage scalability and latency performance. The market plays a central role in supporting long-term national ICT development. It supports disaster recovery, business continuity, and real-time analytics at enterprise scale. Growing public-private partnerships are also improving data infrastructure deployment across regions. Storage demand is further driven by regulatory mandates for data protection and localization.

- For instance, PLDT’s VITRO Sta. Rosa hyperscale facility, energized in July 2024 and officially launched in April 2025, features 50 MW of capacity and NVIDIA-powered GPU servers. It supports AI-ready centralized storage infrastructure for banking, fintech, healthcare, logistics, and government workloads, including analytics and disaster recovery.

Adoption of AI, 5G, and IoT Technologies Across Core Business Applications

AI adoption is pushing businesses to implement storage systems that handle unstructured and training data efficiently. Real-time analytics, machine learning, and natural language processing require faster and higher-capacity infrastructure. The 5G rollout across urban centers boosts IoT devices and sensors, generating large volumes of localized data. Secure, low-latency storage is now a critical enabler for smart manufacturing, autonomous systems, and intelligent transport. Cloud storage providers are offering AI-ready solutions tailored for verticals like fintech and healthtech. The Philippines Data Center Storage Market benefits from this convergence by providing next-gen storage platforms. These platforms allow rapid scaling and dynamic resource allocation. Enterprises and investors see long-term value in storage services that support AI lifecycle workloads. The market now acts as a core digital enabler for future technologies.

Shift Toward Hybrid Cloud Models and Software-Defined Storage Environments

Hybrid cloud strategies are gaining momentum among large corporations and mid-market enterprises. These models offer flexibility to balance data residency, cost-efficiency, and scalability. Storage environments now include software-defined layers for virtualization, automation, and orchestration. Vendors are deploying container-friendly and multi-tenant storage solutions for dynamic workloads. This shift improves manageability, security, and integration with DevOps environments. Businesses are investing in cloud-native storage to support continuous deployment pipelines. The Philippines Data Center Storage Market supports hybrid and edge-to-core workflows, driving CAPEX and OPEX efficiency. It improves adaptability to changing compliance, workload, and performance requirements. Storage vendors are building platforms that simplify control across public and private clouds. This evolution supports digital resilience for enterprises.

Government Policy, Infrastructure Incentives, and Local Manufacturing Integration

The government has introduced fiscal incentives, PEZA accreditation, and fast-track permitting for data infrastructure. These initiatives attract global hyperscale players and regional colocation providers. Special Economic Zones are offering access to power, land, and connectivity at reduced costs. The Philippines Data Center Storage Market benefits from these location-based advantages and national digital priorities. Emerging integration with electronics manufacturing boosts availability of localized storage components. Storage vendors are forming alliances with telcos and ICT firms to build joint ventures. Infrastructure is evolving to align with data protection and national cybersecurity frameworks. Investor confidence is rising due to policy consistency and demand visibility. These drivers make the market a strategic growth zone for digital infrastructure players.

- For instance, under the CREATE MORE Act, data center projects registered in economic zones are eligible for four to seven years of income tax holiday, followed by a 5% special corporate income tax or enhanced deductions, along with duty-free importation of capital equipment and zero-rated VAT on local purchases. These incentives directly support new investments in storage and digital infrastructure.

Market Trends

Rising Hyperscale Activity and Investment from Global Cloud Providers

Global cloud platforms are entering the market through direct builds or partnerships with local firms. These projects include hyperscale campuses, carrier-neutral facilities, and modular storage systems. Providers prioritize locations near metro hubs for connectivity and power access. Hyperscale investment drives demand for large-scale storage clusters with high fault tolerance. The Philippines Data Center Storage Market is attracting strategic investment for regional data hubs. It aligns with APAC data sovereignty and latency reduction goals. Cloud-native storage tools and advanced data lifecycle management are being deployed. These setups enable multitenancy, automation, and integration with analytics services. Hyperscale presence is reshaping capacity planning and pricing in the market.

Deployment of Edge Storage Systems to Support Digital Inclusion Initiatives

Edge computing projects are expanding to remote islands, rural towns, and second-tier cities. Telecom operators and ISPs install micro data centers with distributed storage layers. These systems help process content locally for e-learning, telemedicine, and e-governance. Edge storage reduces reliance on distant core infrastructure and lowers latency for critical apps. The Philippines Data Center Storage Market supports this edge transition through compact, scalable units. Portable storage platforms are being introduced for field operations and disaster resilience. Local governments and NGOs adopt edge setups for continuity in emergencies. Growth in satellite broadband and 5G further strengthens edge storage use cases. The market is seeing demand for rugged, containerized storage hardware.

Greater Emphasis on Green Storage Infrastructure and Power Optimization

Energy-efficient storage is gaining traction in response to rising electricity costs and sustainability targets. Vendors offer systems with high-density drives, power-saving modes, and thermal monitoring. Colocation providers now evaluate power usage effectiveness (PUE) in storage procurement. The Philippines Data Center Storage Market integrates green cooling and SSD-heavy architecture to optimize loads. Enterprises are migrating to storage with deduplication, tiering, and intelligent data placement. These features reduce physical footprint and cooling needs. Facilities leverage renewable power and energy credits where available. Environmental certification is influencing storage vendor selection. The shift supports ESG reporting and green financing for large buyers.

Expansion of Security-Driven Storage Solutions Amid Cyber Risk Growth

Cyber threats have increased enterprise focus on data security and backup solutions. Demand is rising for immutable storage, ransomware protection, and air-gapped systems. Compliance with data privacy laws pushes firms to upgrade backup and disaster recovery infrastructure. The Philippines Data Center Storage Market is seeing growth in secure storage appliances. These solutions include encrypted drives, tokenized access, and behavioral monitoring. Enterprises prefer vendors with strong SLAs on data integrity and breach response. Multi-layer security and AI-based anomaly detection are becoming standard. This trend supports market growth in sectors like BFSI and public services.

Market Challenges

Infrastructure Gaps and Power Supply Concerns Limit Storage System Deployment

Limited Tier III+ facilities in secondary regions slow down large-scale storage deployments. Metro Manila hosts most advanced infrastructure, but congestion and land scarcity raise operating costs. Reliable power supply and backup systems remain a challenge for edge locations. The Philippines Data Center Storage Market faces delays from permitting, zoning, and fiber rollout bottlenecks. Storage projects in provincial areas require heavy CAPEX for supporting utilities. Grid instability in some regions raises downtime and storage system risk. Shortages in qualified infrastructure contractors delay hyperscale timelines. Facilities must overinvest in power redundancy to meet enterprise SLAs. This barrier affects profitability for new entrants.

High Import Dependence and Limited Local Supply Chain Maturity

The market heavily depends on imported drives, controllers, and racks, increasing project costs and timelines. Local sourcing for storage hardware remains limited, and distribution channels lack scale. Currency fluctuations and shipping delays affect pricing and availability. The Philippines Data Center Storage Market struggles to build a resilient storage hardware ecosystem. Vendor support and RMA processes face delays due to offshore dependencies. Skills shortage in software-defined storage and maintenance also affects adoption. Logistics costs are higher compared to regional peers like Singapore and Malaysia. Limited data center component warehousing increases lead times for urgent replacements. These issues slow market competitiveness.

Market Opportunities

Cloud-Native and AI-Optimized Storage Demand from Digital Enterprises

Enterprises in fintech, healthcare, and e-commerce are scaling data analytics and AI platforms. They require storage solutions with low latency, high throughput, and intelligent tiering. The Philippines Data Center Storage Market can capitalize on this shift by offering AI-ready, cloud-integrated platforms. Demand for S3-compatible object storage and GPU-aligned storage is rising. Startups and large firms both explore pay-as-you-go models for flexibility.

Public Sector Digitalization and E-Government Systems Boosting Storage Needs

National ICT programs such as eGOV and digital ID systems require secure, scalable storage. Government agencies are adopting on-prem and hybrid models to meet compliance. The Philippines Data Center Storage Market is seeing public procurement for long-term archival and citizen data platforms. Opportunities lie in tiered storage, automated backups, and secure vaults for defense and healthcare sectors.

Market Segmentation

By Storage Type

Traditional storage remains widely used for structured workloads and low-cost archiving. All-flash storage is gaining share due to its speed and reliability, especially in banking and telecom. Hybrid storage leads the [Philippines Data Center Storage Market] due to its balance of performance and cost. Many enterprises combine HDD with SSD in hybrid arrays. All-flash adoption will grow fastest due to digital banking, AI, and cloud-native apps.

By Storage Deployment

Storage Area Network (SAN) systems dominate large-scale data centers due to high performance and centralized management. Network-attached Storage (NAS) is common in mid-sized enterprise and government setups. Direct-attached Storage (DAS) sees use in edge sites and legacy systems. SAN leads the [Philippines Data Center Storage Market] because of its scalability and speed. Future demand for NAS will grow in healthcare and retail sectors.

By Component

Hardware accounts for the largest share, driven by demand for SSDs, controllers, and enclosures. Software is gaining traction as more organizations deploy storage virtualization and automation tools. Storage management and monitoring tools are being bundled with hardware. The [Philippines Data Center Storage Market] shows strong investment in high-performance storage appliances. Software-defined storage is expected to increase as cloud and edge models grow.

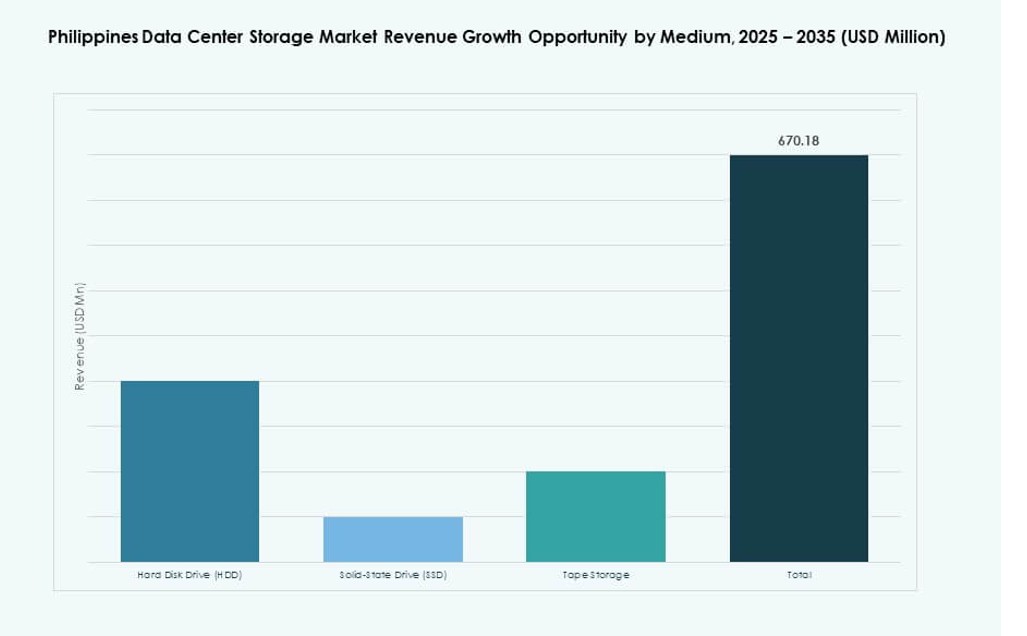

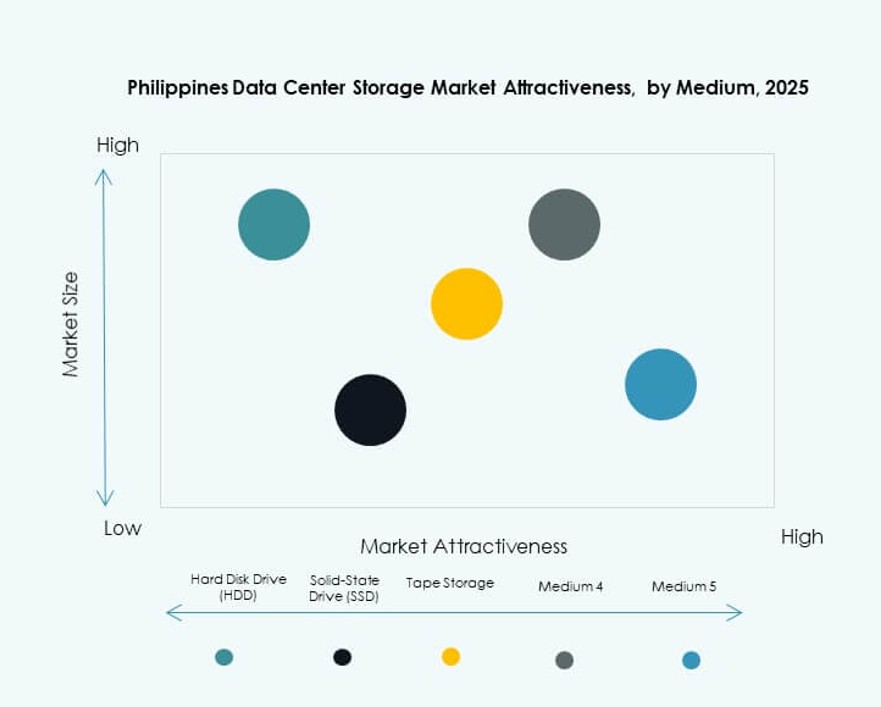

By Medium

Hard Disk Drives (HDDs) still hold the majority due to lower cost per TB for cold storage. Solid-State Drives (SSDs) are rapidly growing for mission-critical applications requiring fast access and durability. Tape storage maintains a niche role in archival and backup solutions. SSDs are preferred in flash arrays and tiered systems in the [Philippines Data Center Storage Market]. Hybrid deployments using HDD and SSD combinations are also expanding.

By Deployment Model

On-premises deployment leads due to regulatory compliance and enterprise control needs. Cloud-based storage adoption is growing across SMBs and startups. Hybrid deployment is emerging as the most flexible model across government and large enterprises. The [Philippines Data Center Storage Market] supports hybrid setups that blend local security with cloud scalability. This model is ideal for firms balancing cost, control, and compliance.

By Application

IT and Telecommunications lead storage demand due to 5G, mobile data growth, and cloud adoption. BFSI follows closely with demand for secure, high-speed transaction data handling. Government and healthcare are increasing digital workloads, boosting localized storage needs. The [Philippines Data Center Storage Market] sees rising activity in e-commerce, logistics, and education. Application-based demand is shifting toward performance, scale, and resilience.

Regional Insights

Metro Manila Holds 60% Share, Driving Core Infrastructure and Hyperscale Projects

Metro Manila is the primary hub for the Philippines Data Center Storage Market, holding 60% share. It offers connectivity, power availability, and enterprise concentration. Quezon City, Makati, and Pasig lead in Tier III+ deployments. Multinational firms prefer the region for compliance, talent, and uptime. Colocation and cloud providers base their regional nodes here. Storage investment is driven by banking, government, and tech sectors.

- For instance, VITRO, the data center arm of PLDT, operates 11 data centers nationwide including large sites in Metro Manila, and its flagship VITRO Sta.

Central Visayas and Davao Region Account for 25% with Growing Edge Deployments

Central Visayas, particularly Cebu, and Davao Region hold a combined 25% market share. These areas attract edge data center builds due to rising internet traffic and business activity. The storage systems here support regional education, healthcare, and BPO ecosystems. Fiber connectivity expansion and IT parks attract new investments. The market here benefits from supportive local policies and skilled labor.

Remaining Luzon, Mindanao, and Other Islands Capture 15% Through Niche and Government Demand

Smaller cities and remote provinces account for 15% of the storage market. Government-led digital inclusion and smart city projects are key drivers. Storage systems are deployed in disaster recovery centers, digital health units, and local offices. The [Philippines Data Center Storage Market] expands into these zones through rugged edge deployments. These regions rely on cloud and satellite-linked storage due to connectivity constraints. Growth potential exists in logistics, defense, and public services.

- For instance, PLDT and other operators connect multiple VITRO facilities, regional data centers, and cable landing stations in locations such as La Union, Batangas, and Digos to support government e‑services, disaster‑recovery sites, and public‑service platforms, enabling storage of critical data outside Metro Manila as part of a distributed national infrastructure.

Competitive Insights:

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- Huawei Technologies Co., Ltd.

- IBM Corporation

- NetApp

- Cisco Systems, Inc.

- ePLDT

- ST Telemedia Global Data Centres

- Beeinfotech PH

- Hitachi Vantara

The Philippines Data Center Storage Market features a mix of global technology vendors and leading domestic operators. It is shaped by aggressive cloud expansion, enterprise digitization, and public sector modernization. Global firms such as Dell, HPE, Huawei, and IBM offer end-to-end storage infrastructure across flash, hybrid, and software-defined environments. Local players like ePLDT and Beeinfotech PH dominate in service-led colocation, integrating storage-as-a-service into bundled offerings. The market is competitive on metrics such as latency, energy efficiency, data security, and total cost of ownership. Partnerships, edge storage innovation, and government-backed ICT initiatives are key differentiation drivers. Vendors actively localize solutions to match data sovereignty laws and support localized workloads.

Recent Developments:

- In March 2025, ST Telemedia Global Data Centres Philippines, in collaboration with Vertiv, Dell Technologies, and Novare Technologies, inaugurated the country’s first liquid-cooling technology showroom. The facility showcases advanced infrastructure designed to support high-density and AI workloads, marking a step toward localized deployment of next-generation storage and thermal solutions.

- In June 2025, Equinix confirmed the completion of its acquisition of the Manila-based MN1, MN2, and MN3 facilities. The launch of MN2 alone added approximately 500 cabinets, significantly increasing local storage capacity for both domestic and international customers operating in the Philippines.

- In March 2025, Dell Technologies participated as a technology partner in the STT GDC Philippines liquid-cooling showroom. Through this collaboration, Dell positioned its server and storage platforms for high-density, liquid-cooled deployments to meet growing demand from local enterprises and hyperscalers.

- In December 2024, ST Telemedia Global Data Centres Philippines completed the structural framework of its STT Fairview 1 campus in Quezon City. Projected to reach 124 MW IT capacity on full build-out, it is expected to become the country’s largest data center and a key driver of future demand for hyperscale-grade servers and storage systems.