Executive summary:

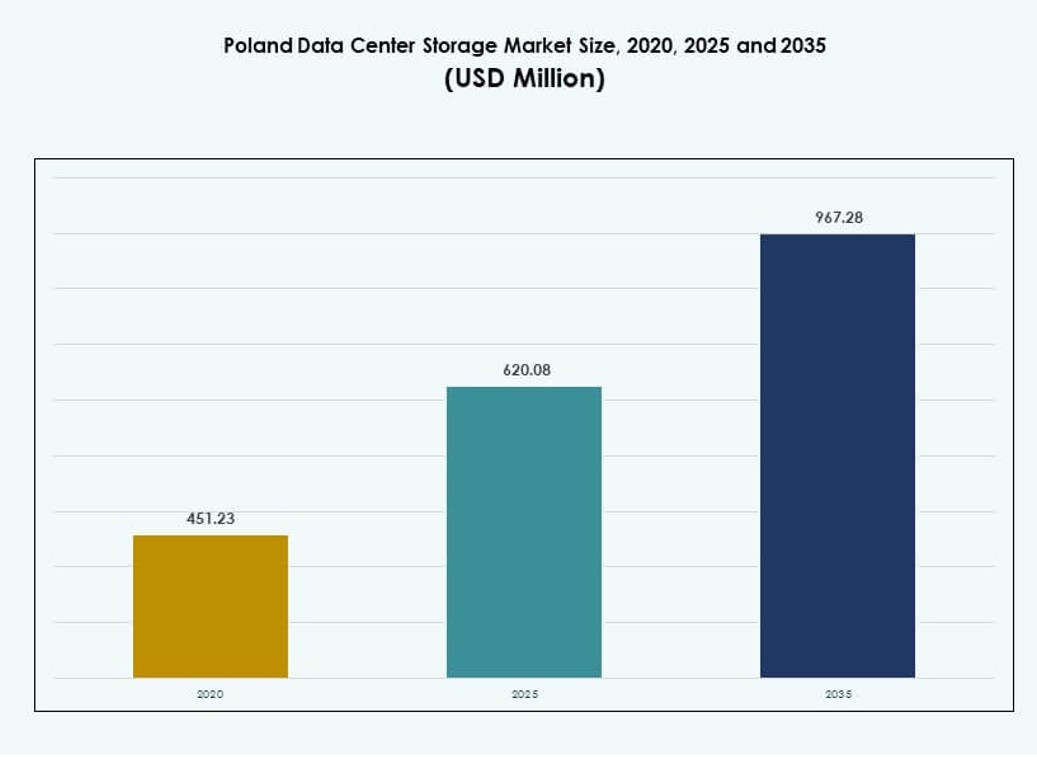

The Poland Data Center Storage Market size was valued at USD 451.23 million in 2020 to USD 620.08 million in 2025 and is anticipated to reach USD 967.28 million by 2035, at a CAGR of 4.48% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Poland Data Center Storage Market Size 2025 |

USD 620.08 Million |

| Poland Data Center Storage Market, CAGR |

4.48% |

| Poland Data Center Storage Market Size 2035 |

USD 967.28 Million |

The market is advancing due to strong demand for hybrid storage, growing cloud integration, and the rollout of AI-intensive workloads. Enterprises are prioritizing software-defined storage and scalable infrastructure that can support IoT and edge data. Increased digitalization across sectors is prompting investments in high-throughput, low-latency storage platforms. This transformation is strategic for businesses managing regulatory compliance and data-intensive operations. Investors are drawn by the country’s IT talent base and expanding hyperscale ecosystem.

Warsaw leads the market due to its dense network connectivity, hyperscale activity, and enterprise IT footprint. Kraków and Wrocław are emerging regions with rising demand from startups, research institutes, and industrial firms. Secondary cities like Gdańsk and Poznań are seeing edge-focused deployments that support local business continuity and real-time services. Regional expansion is vital for improving latency, resilience, and data sovereignty in distributed environments.

Market Dynamics:

Market Drivers

Enterprise Digitization and Rising Data Volumes Fuel Strong Demand for Storage Expansion

Enterprises across Poland are accelerating digital transformation, pushing demand for scalable and secure storage. Data from ERP, CRM, AI analytics, and IoT systems requires robust infrastructure that ensures performance and availability. The Poland Data Center Storage Market is gaining traction as local firms replace aging storage with hybrid and cloud-native systems. Storage modernization aligns with the growing need for business continuity, faster data access, and disaster recovery capabilities. Vendors are introducing modular platforms for flexible deployment and improved lifecycle management. Industries like retail, logistics, and healthcare rely on secure data infrastructure to meet compliance and performance targets. Edge data volumes are rising with the spread of smart devices and remote operations. Storage architectures now need to support distributed data environments while ensuring speed and data sovereignty. Businesses view storage as a strategic asset that supports innovation and operational efficiency.

- For instance, Orange Polska deployed 15 backbone links with 400 Gbps capacity across major cities including Warsaw and Krakow in December 2023, handling 40% of its total traffic for IoT and enterprise data flows.

Cloud Adoption Driving Shift Toward Flexible and Software-Defined Storage Models

Cloud adoption continues to grow across enterprise and public sectors in Poland, reshaping storage infrastructure needs. Many organizations are shifting to hybrid models that blend on-premises security with cloud scalability. Software-defined storage (SDS) has gained popularity for reducing vendor lock-in and improving control. The Poland Data Center Storage Market reflects these transitions with growing investment in SDS platforms and cloud-integrated appliances. Enterprises want to scale capacity on-demand while optimizing total cost of ownership. Storage systems must now deliver seamless performance across private and public clouds. Government cloud initiatives and digital public services further expand this trend. Innovation in orchestration tools enables intelligent storage tiering and policy-based automation. Storage has become a critical enabler of cloud agility and responsiveness in a competitive digital environment.

Artificial Intelligence and Data-Intensive Workloads Elevate the Need for High-Performance Storage

Adoption of AI, big data analytics, and machine learning is creating a new class of storage demand. These workloads require low-latency access, rapid throughput, and advanced data management capabilities. The Poland Data Center Storage Market supports this shift with all-flash and hybrid systems optimized for performance. AI-driven businesses need systems that ensure real-time data delivery, support parallel processing, and handle large volumes efficiently. Enterprises are investing in NVMe-based flash storage, GPU-compatible platforms, and integrated caching to meet these needs. Storage providers are responding with purpose-built solutions for AI training, inferencing, and analytics. HPC workloads in sectors like pharma, finance, and manufacturing drive adoption of scalable, high-speed storage solutions. This demand reshapes procurement patterns, favoring innovation-driven vendors and custom deployment strategies. Performance now plays a larger role in storage decisions than traditional capacity metrics.

- For instance, NetApp AFF A900 systems deliver up to 14.4 million IOPS at 1ms latency in clustered deployments, as verified for high-performance AI workloads in European enterprise settings including Poland.

Compliance, Data Sovereignty, and Edge Computing Needs Reinforce Investment in Local Infrastructure

Organizations must comply with strict data protection and cybersecurity regulations across sectors in Poland. Local data storage is often mandated by laws around financial records, health data, and citizen information. The Poland Data Center Storage Market responds with solutions that offer secure, compliant, and location-specific deployment options. This trend increases demand for localized data center expansions and backup systems near the point of use. Edge computing is also rising, driving growth in micro data centers and regional storage nodes. Companies operating in logistics, energy, and manufacturing require edge storage that supports real-time decision-making. Regulatory pressure further drives adoption of encryption, secure access controls, and audit-ready data management features. Businesses invest in systems that balance performance, compliance, and cost. Data localization requirements support long-term growth for storage vendors with regional footprint and sector-specific expertise.

Market Trends

Growth in Colocation Storage Demand Due to Rising IT Outsourcing by Enterprises

Poland’s mid-sized enterprises increasingly prefer colocation services to reduce operational complexity and focus on core business. This shift drives strong demand for shared storage platforms with enterprise-grade security and performance. The Poland Data Center Storage Market benefits from partnerships between colocation providers and storage vendors. Colocation facilities now offer integrated storage bundles, including SAN, NAS, and flash arrays, tailored to hosted environments. These services meet growing requirements for compliance, scalability, and multi-site backup. Enterprises rely on service-level agreements to ensure uptime and access. Hyperscale colocation deployments push adoption of centralized storage control and remote orchestration. Colocation also supports green IT goals by consolidating infrastructure and optimizing energy usage. This trend shapes the way storage is provisioned, accessed, and managed in modern hybrid environments.

Emergence of Cyber Resilience and Immutable Storage Architectures for Ransomware Defense

Cyber threats have become more sophisticated, with ransomware attacks targeting critical data assets across sectors. To counter this, businesses are deploying immutable storage systems that prevent tampering, deletion, or rollback of backups. The Poland Data Center Storage Market reflects this trend with growing adoption of WORM (Write-Once, Read-Many) technology and air-gapped backup appliances. These solutions ensure business continuity by isolating and securing data copies from external threats. Immutable storage also supports audit requirements and long-term record retention policies. Managed service providers offer cyber-resilient storage bundles with built-in recovery workflows. Enterprises prioritize solutions that combine active monitoring, automated failover, and secure versioning. Adoption of these architectures improves recovery time objectives and enhances board-level confidence in digital risk management.

Integration of AI and Predictive Analytics into Storage for Optimization and Self-Healing

Storage platforms now integrate AI to automate provisioning, capacity planning, and failure prediction. These features help IT teams reduce manual effort and increase system reliability. The Poland Data Center Storage Market is shifting toward intelligent storage with built-in analytics dashboards and usage trend forecasts. Vendors offer solutions with machine learning engines that fine-tune workload performance and detect anomalies. Self-healing capabilities are embedded into controllers for dynamic tuning and faster issue resolution. Businesses gain visibility across multi-tier environments and optimize resources based on usage patterns. These smart platforms reduce downtime and improve service quality. Storage becomes a more agile and autonomous layer in the overall IT stack. Enterprises value this intelligence for both cost savings and better user experiences.

Adoption of Cold Storage and Archival Systems for Cost-Optimized Long-Term Retention

With rising data volumes, organizations are segmenting active and passive datasets more clearly. Cold storage solutions offer cost-efficient retention for infrequently accessed data like records, logs, and legal files. The Poland Data Center Storage Market sees growth in tape storage, archival SSDs, and object-based systems that support long-term preservation. Financial institutions and public sector agencies lead adoption due to regulatory and recordkeeping needs. Cloud-based archival solutions with tiered pricing models also gain traction. Businesses integrate cold storage into hybrid models to optimize performance and cost. This tiering helps reduce energy use and carbon footprint, supporting sustainability goals. Storage providers respond with flexible retention policies, encryption, and compliance features. Long-term storage becomes a strategic component of digital governance and enterprise continuity planning.

Market Challenges

Legacy Infrastructure and Budget Constraints Limit the Pace of Storage Modernization Across Enterprises

Many Polish enterprises still rely on aging storage systems that lack scalability and security features. These legacy environments limit integration with modern workloads and cloud-native applications. The Poland Data Center Storage Market faces hurdles as businesses struggle to justify high upfront investments in newer platforms. Budget constraints in SMEs, particularly outside major cities, hinder upgrades and long-term planning. Vendors face challenges in demonstrating ROI and aligning value propositions with immediate business outcomes. System migration risks, including data loss and downtime, also slow modernization. Firms with tight IT teams delay transition to avoid disrupting ongoing operations. Limited awareness of total cost benefits from hybrid and software-defined storage models adds to resistance. These factors create an uneven adoption curve that impacts national digital competitiveness.

Skilled Workforce Shortage and Vendor Fragmentation Create Barriers to Scalable Deployment

There is a shortage of professionals skilled in managing next-generation storage systems, particularly outside major tech hubs. This talent gap slows deployment of complex storage configurations and reduces reliability. The Poland Data Center Storage Market must address the need for certified specialists in SAN, NAS, SDS, and AI-integrated platforms. Vendor fragmentation also creates integration challenges as enterprises adopt multi-vendor solutions with varying standards. Lack of interoperability increases costs and reduces performance consistency. Enterprises struggle to manage vendor relationships and unify support across products. Training, documentation, and long-term maintenance become bottlenecks for scaling infrastructure. These operational difficulties weaken customer satisfaction and slow the broader transition to resilient, high-performance storage.

Market Opportunities

Demand for Edge Storage and Regional Micro Data Centers Offers New Growth Potential

Edge computing is expanding in Poland with demand from sectors like logistics, retail, and manufacturing. These industries require localized storage for real-time analytics, IoT data, and latency-sensitive applications. The Poland Data Center Storage Market benefits from rising investments in micro data centers that serve regional and sector-specific needs. Vendors offering rugged, scalable edge storage solutions gain a competitive advantage. It opens up opportunities for partnerships with smart city projects and industrial automation hubs.

Growing Hyperscale Investments and 5G Rollouts to Drive Next-Gen Storage Demand

New hyperscale developments in Warsaw and secondary cities bring large-scale demand for unified, high-performance storage platforms. These deployments integrate with national 5G rollouts, enabling advanced cloud, AI, and remote operations. The Poland Data Center Storage Market is positioned to benefit from increased need for NVMe, SDS, and container-native storage. Vendors focusing on 5G-compatible architecture, automation, and orchestration tools can capture market share from global entrants and local players.

Market Segmentation

By Storage Type

Traditional storage holds a notable share, driven by legacy systems in government and banking sectors. However, all-flash storage is gaining momentum due to performance and energy efficiency. Hybrid storage leads in flexibility, offering a balanced approach for businesses transitioning to modern systems. The Poland Data Center Storage Market shows rising adoption of hybrid storage across mid-sized enterprises managing structured and unstructured data.

By Storage Deployment

Storage Area Network (SAN) systems dominate due to their enterprise-grade speed and centralized management. SANs are favored in financial and telecom sectors requiring consistent throughput. Network-attached Storage (NAS) is rising among SMEs and content-driven applications. Direct-attached Storage (DAS) remains relevant in edge deployments where simplicity and low cost matter. The market is gradually shifting toward flexible, software-managed models.

By Component

Hardware accounts for the bulk of spending, led by investment in flash arrays, racks, and controllers. Software is growing steadily with demand for SDS, analytics, and backup management platforms. The Poland Data Center Storage Market reflects a clear shift toward integrated software-hardware bundles that ensure interoperability and scalability across hybrid environments.

By Medium

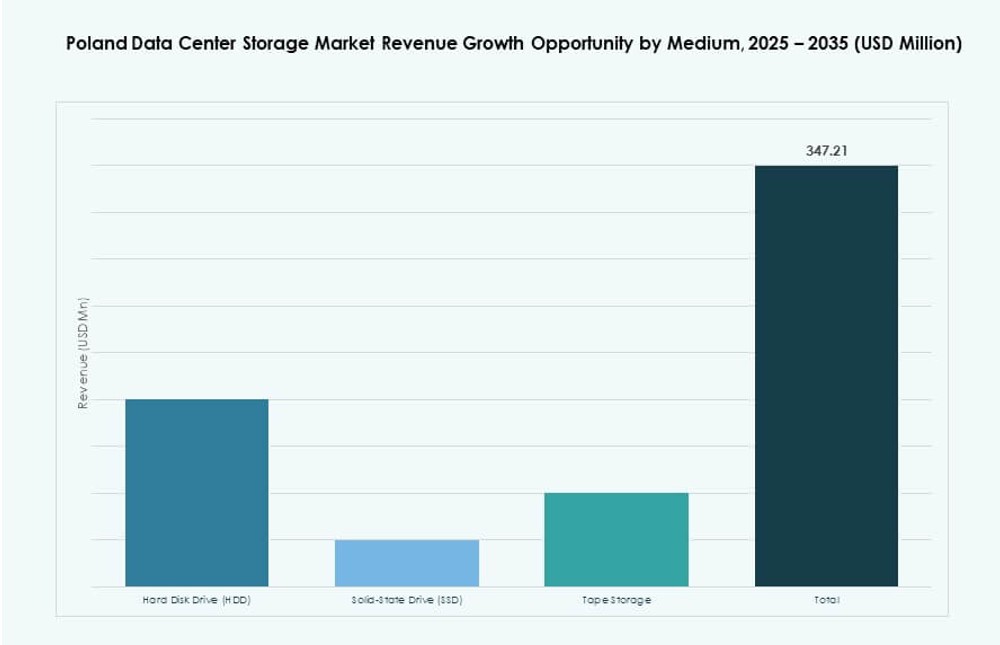

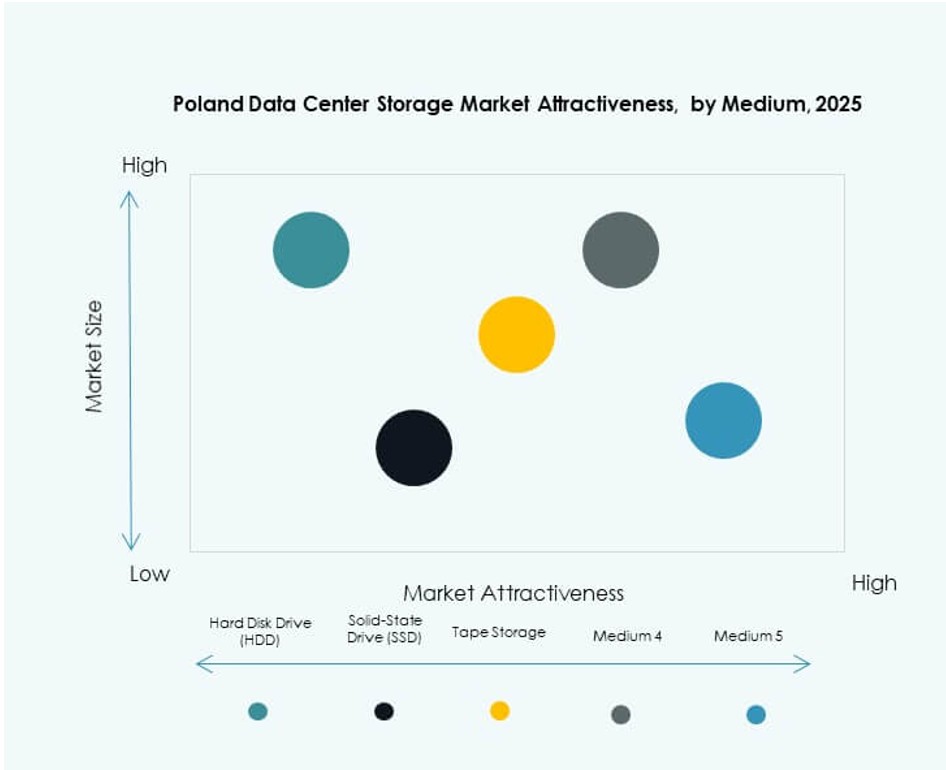

Hard Disk Drives (HDD) are still widely used for cost-effective bulk storage, especially in archival systems. Solid-State Drives (SSD) are expanding fast in applications demanding speed and energy efficiency. Tape storage continues to serve long-term backup needs in government and healthcare. The market is seeing growing deployment of SSDs in AI, video surveillance, and transactional workloads.

By Deployment Model

Cloud-based models are expanding, driven by digital transformation and flexible cost structures. On-premises deployment holds strong in regulated industries requiring data control. Hybrid models are gaining most traction in the Poland Data Center Storage Market, balancing control, cost, and scalability. Enterprises prefer hybrid setups that combine public cloud elasticity with private storage security.

By Application

IT and telecom lead in storage demand due to high transaction volumes and fast data processing needs. BFSI is another major segment, driven by regulatory compliance and secure customer data handling. Government projects add significant demand, especially for archival and citizen data systems. Healthcare and others contribute through digital imaging, records management, and telemedicine growth.

Regional Insights

Warsaw Metropolitan Area Dominates with Over 60% Share Due to Hyperscale Activity

Warsaw leads the Poland Data Center Storage Market with more than 60% share due to hyperscale growth. The region offers the highest density of network providers, cloud platforms, and colocation hubs. Global firms select Warsaw for primary infrastructure deployments, citing strong power availability and carrier-neutral data centers. Storage demand here is driven by hybrid cloud integration, banking digitalization, and public cloud expansion.

- For instance, Microsoft announced a PLN 2.8 billion ($700 million) investment in February 2025 to expand its existing data center campuses near Warsaw through mid-2026, enhancing cloud and AI computing capacity across three physical complexes launched in 2023.

Emerging Growth Seen in Kraków and Wrocław from Enterprise and Academic Expansion

Kraków and Wrocław are growing storage hubs with increasing enterprise and academic demand. These cities benefit from skilled IT labor, lower operating costs, and innovation-focused economies. Storage infrastructure is expanding in support of local startups, R&D centers, and smart campus projects. Enterprises in these regions invest in hybrid storage to support agile development and remote collaboration models.

Tier 2 and Tier 3 Cities See Edge Deployment Driven by Industry 4.0 and Retail IT

Cities like Łódź, Poznań, and Gdańsk are emerging as targets for edge data center expansion. These markets show rising demand for localized storage in retail, logistics, and manufacturing sectors. The Poland Data Center Storage Market gains traction in these areas through regional deployments, supporting real-time decision systems. Industrial automation and e-commerce drive low-latency storage needs in these locations.

- For instance, Poland’s PIAST-AI Factory, hosted at the Poznań Supercomputing and Networking Center (PCSS), received approximately $125 million (PLN 540 million) in combined funding from the Polish government and the European Commission in 2024–2025.

Competitive Insights:

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- IBM Corporation

- Cisco Systems, Inc.

- NetApp

- Huawei Technologies Co., Ltd.

- Lenovo Group

- Comarch

- Asseco

- Fujitsu Limited

The Poland Data Center Storage Market features a mix of global OEMs and local IT firms competing across storage layers, deployment models, and service integration. Dell Technologies, HPE, and IBM lead in enterprise-grade deployments with hybrid, flash, and cloud-integrated offerings. NetApp and Cisco provide advanced storage networking and SDS platforms tailored to hyperscale and colocation demand. Huawei and Lenovo supply scalable systems optimized for performance and cost. Local players like Asseco and Comarch deliver custom storage solutions aligned with public sector and SME requirements. It shows rising investment in NVMe, cyber-resilience, and storage analytics to address AI, cloud, and edge workload demands. The market rewards vendors that combine infrastructure reliability, software integration, and regulatory compliance with regional service support.

Recent Developments:

- In September 2025, Poland’s Atman launched the first phase of its new Warsaw data center campus. The 14.4MW building went live, marking a significant boost to local storage infrastructure, with two additional data centers planned to follow.

- In February 2025, TSS invested in Asseco Poland shares, establishing a strategic partnership through a shareholder agreement that supports Asseco’s strategy of developing proprietary software and pursuing acquisitions while remaining headquartered in Poland.