Executive summary:

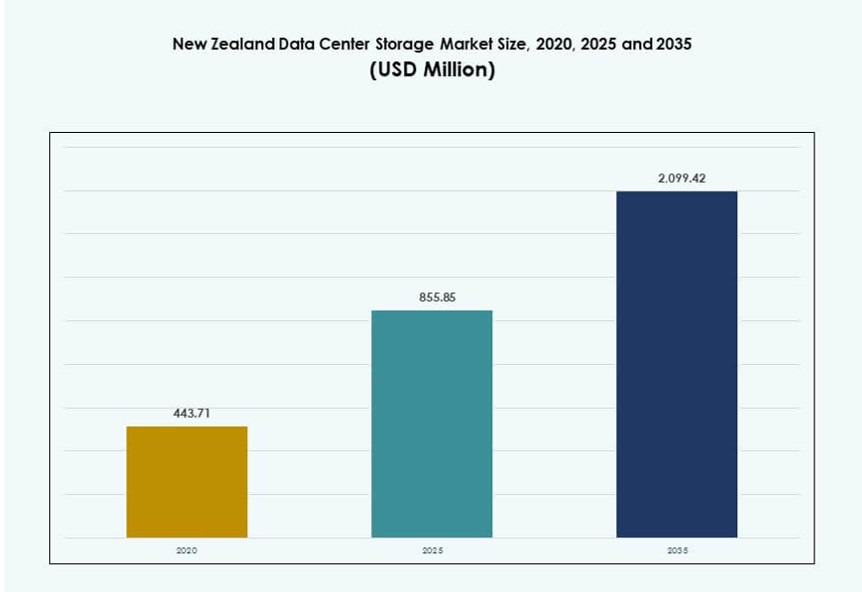

The New Zealand Data Center Storage Market size was valued at USD 443.71 million in 2020 to USD 855.85 million in 2025 and is anticipated to reach USD 2,099.42 million by 2035, at a CAGR of 9.29% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| New Zealand Data Center Storage Market Size 2025 |

USD 855.85 Million |

| New Zealand Data Center Storage Market, CAGR |

9.29% |

| New Zealand Data Center Storage Market Size 2035 |

USD 2,099.42 Million |

Demand for localized storage is rising due to national data residency laws, AI adoption, and cloud migration. Enterprises are modernizing infrastructure with all-flash arrays and software-defined storage to handle real-time workloads. The shift toward hybrid and edge models is reshaping deployment strategies. Government digital strategies and sustainability goals further push innovation in storage platforms. Service providers are investing in scalable, energy-efficient systems to meet low-latency demands. Investors are targeting sovereign infrastructure opportunities. The market holds strategic value for enterprise continuity and regulatory compliance. It is positioned as a growth hub for long-term digital infrastructure.

Auckland leads the market with advanced interconnection hubs, submarine cable access, and dense enterprise activity. It hosts most hyperscale and colocation facilities, making it the storage backbone of the country. Wellington and Christchurch are expanding steadily, supported by public sector modernization and regional tech investment. Secondary cities are emerging due to fiber rollout, smart city projects, and business continuity needs. The regional split reflects a balance between urban data density and distributed edge infrastructure. Geographic resilience remains a key priority across deployment strategies.

Market Dynamics:

Market Drivers

Rising Demand for Data Sovereignty and Compliance-Driven Storage Expansion

New Zealand enforces strict data sovereignty laws, pushing enterprises to localize storage infrastructure. The Privacy Act and data protection mandates fuel investment in secure, in-country storage platforms. Public and private entities adopt onshore solutions to comply with sector-specific regulations. Financial institutions, government agencies, and healthcare providers lead demand for compliant infrastructure. Local cloud players expand capacity to support audit-ready, low-latency storage. This regulatory environment boosts trust in domestic data centers. Investors view this as a stable opportunity for infrastructure growth. The New Zealand Data Center Storage Market benefits directly from this shift toward national data residency. It ensures storage services meet both legal and operational requirements.

- For instance, Spark New Zealand agreed in August 2025 to sell a 75% stake in its data center business to Pacific Equity Partners, valuing the asset at up to NZ$705 million to scale sovereign cloud and storage services in response to compliance-driven demand.

Acceleration of Cloud Migration and Edge Infrastructure Deployment

Businesses across New Zealand are transitioning from legacy systems to hybrid and multi-cloud models. Cloud storage adoption increases as firms seek agility, scalability, and cost efficiency. Edge computing deployments grow in response to rising latency-sensitive workloads. Smart city initiatives, IoT adoption, and AI workloads demand real-time data processing closer to users. These changes require advanced storage with high throughput and low latency. Enterprises invest in modular storage systems that adapt to dynamic application needs. This decentralization trend reshapes how storage is deployed nationwide. The New Zealand Data Center Storage Market evolves to support both centralized and edge use cases. It supports rapid transformation across digital-first sectors.

- For instance, AWS launched its Asia Pacific (New Zealand) Region in August 2025, committing over NZ$7.5 billion to build local data centers that support edge computing and low-latency hybrid storage solutions across the country.

Strategic Government Investment in Digital Infrastructure Modernization

The New Zealand Government’s Digital Strategy 2030 outlines cloud-first policies and infrastructure funding. Investments target modernizing legacy IT systems across public sector departments. This includes secure storage platforms, automated backup systems, and disaster recovery solutions. Education, health, and justice sectors upgrade digital infrastructure to ensure continuity and compliance. The strategy boosts demand for local cloud capacity with integrated storage. Public-private partnerships support regional infrastructure projects, enhancing resilience. This push encourages adoption of private and sovereign cloud deployments. The New Zealand Data Center Storage Market aligns with national digital goals. It becomes a key pillar in the broader digital transformation roadmap.

Surging Enterprise Data Volumes Driven by E-Commerce, AI, and Remote Workflows

Digital business models in retail, fintech, and logistics generate massive unstructured data. AI training, real-time analytics, and remote collaboration tools require high-performance storage. Enterprises need scalable systems to manage unpredictable data spikes. Cloud-native apps, video conferencing, and file sharing drive sustained storage growth. Organizations prioritize backup, archiving, and high-availability systems. AI workloads, in particular, require parallel processing and distributed storage layers. Flexible deployment models become critical for scalability and cost control. The New Zealand Data Center Storage Market supports this scale-up through elastic and intelligent storage platforms. It helps businesses stay agile while managing complex digital ecosystems.

Market Trends

Growth in Green Storage Infrastructure to Meet National Sustainability Targets

Energy-efficient data center designs gain traction to align with New Zealand’s low-emission goals. Operators prioritize low-PUE systems and storage with reduced energy draw. Liquid cooling and AI-powered storage resource management support sustainability. Many providers now seek carbon-neutral certifications to boost investor confidence. Renewable power sourcing from hydro and wind further strengthens green credentials. Enterprises prefer vendors offering lifecycle-efficient storage systems. Long-term retention solutions favor high-density but low-power technologies. The New Zealand Data Center Storage Market integrates these changes into long-term infrastructure plans. It sets new standards for climate-aligned data management.

Proliferation of AI-Ready Storage Architectures Across Enterprise Deployments

AI use cases in sectors like agriculture, healthcare, and finance require real-time, GPU-compatible storage systems. Enterprises deploy NVMe and high IOPS storage to handle AI training and inferencing. Hybrid storage models optimize cost and performance for these workloads. New architectures prioritize data locality and fast read/write speeds. Edge AI deployments drive need for compact, ruggedized storage units. The New Zealand Data Center Storage Market integrates AI support into core platform designs. It enhances workload performance while maintaining data compliance. AI-readiness becomes a key differentiator in storage vendor selection.

Increased Adoption of Software-Defined Storage for Infrastructure Flexibility

Organizations adopt software-defined storage (SDS) to decouple hardware and scale easily. SDS offers unified management of block, file, and object storage under one interface. Enterprises benefit from automation, reduced vendor lock-in, and cost efficiency. SDS platforms integrate seamlessly with hybrid cloud environments. These solutions improve fault tolerance and disaster recovery capabilities. Use cases include media storage, financial reporting, and compliance archiving. Vendors develop SDS tailored to sector-specific needs like healthcare or education. The New Zealand Data Center Storage Market sees rising SDS deployment among SMBs and enterprises. It reflects the demand for flexible, future-ready storage strategies.

Rise of Cloud-Native Backup and Disaster Recovery-as-a-Service (DRaaS)

Organizations shift from physical backup systems to cloud-native DRaaS platforms. Ransomware threats, natural disaster risks, and regulatory requirements drive the shift. DRaaS ensures business continuity with minimal downtime and fast recovery. Providers offer multi-zone and cross-region data replication to meet SLA needs. Integration with virtualization platforms improves recovery automation. Subscription models lower the entry barrier for SMBs and startups. DRaaS adoption rises in telecom, education, and legal sectors. The New Zealand Data Center Storage Market responds with localized DRaaS offerings. It meets growing demand for scalable and secure business continuity solutions.

Market Challenges

High Infrastructure Costs and Limited Economies of Scale in a Small Market

New Zealand’s limited population base restricts economies of scale for large-scale storage deployments. Data center construction and operational costs remain high due to import dependency and geographic isolation. Skilled labor shortages increase staffing costs across storage and IT operations. Hardware and advanced storage systems face longer lead times and higher shipping expenses. This drives up total cost of ownership for enterprise deployments. Many smaller providers struggle to match global pricing benchmarks. Limited hyperscale presence reduces bulk procurement advantages. The New Zealand Data Center Storage Market must balance innovation with economic viability. It requires targeted investments to overcome size-related inefficiencies.

Network Latency Constraints and Limited Submarine Cable Redundancy

Despite improved connectivity, international bandwidth still relies on limited submarine cables. Any disruption can impact cloud storage access and latency-sensitive workloads. Data-intensive applications suffer from inconsistent international performance. Redundancy and peering limitations constrain cross-border data movement. Domestic fiber coverage outside major metros remains patchy. Edge storage rollouts in remote areas face logistical delays. These factors restrict deployment flexibility and regional expansion. The New Zealand Data Center Storage Market needs enhanced network resilience. It depends on continuous upgrades to support scalable, low-latency services.

Market Opportunities

Public Sector Cloud Initiatives and Smart Infrastructure Projects

Smart city rollouts, e-governance platforms, and health digitization create demand for localized, scalable storage. Government-backed digital twin projects and real-time urban analytics require cloud-based platforms. The New Zealand Data Center Storage Market can support these initiatives with robust, compliance-ready infrastructure. It enables sector-specific innovation while securing sensitive data.

Partnerships with Global Cloud Providers and Regional Expansion

Strategic alliances with AWS, Microsoft, and Google Cloud support hybrid deployments across the country. These partnerships reduce latency and boost resilience. Regional operators gain capacity-building support and access to broader ecosystems. The New Zealand Data Center Storage Market benefits from such collaborations by extending capabilities into underserved regions.

Market Segmentation

By Storage Type

Traditional storage systems continue to serve legacy applications but lose share to modern alternatives. All-flash storage is the fastest-growing segment due to its high performance and reliability. Hybrid storage balances cost and speed, making it popular for mid-size enterprises. Others include object-based systems for unstructured data. In the New Zealand Data Center Storage Market, all-flash solutions gain traction in AI and analytics-heavy workloads.

By Storage Deployment

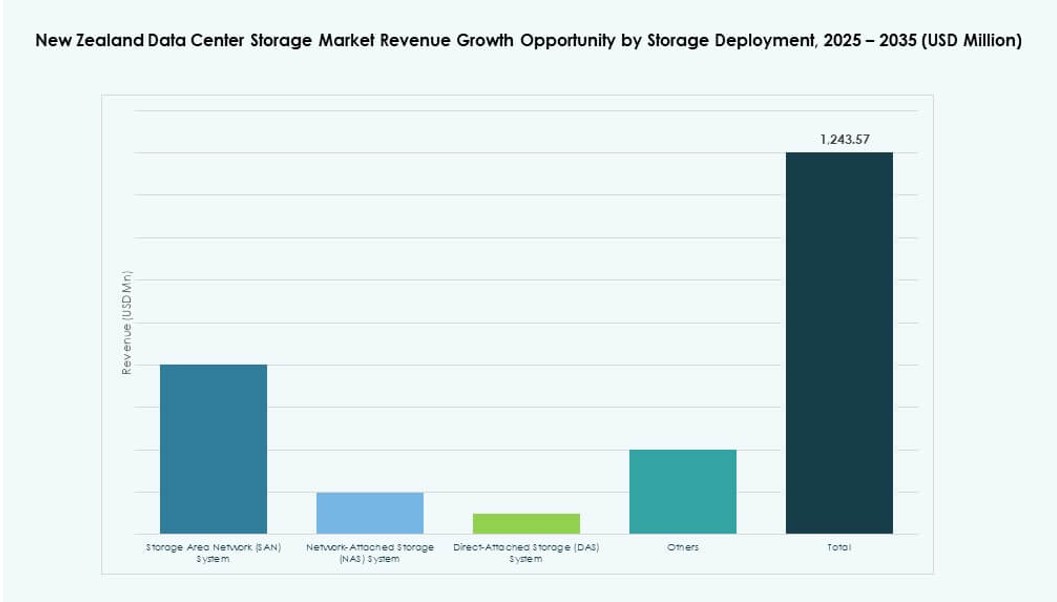

Storage Area Network (SAN) systems dominate, offering high-speed, low-latency connectivity ideal for enterprise workloads. NAS systems are widely adopted in media and collaboration platforms. Direct-Attached Storage (DAS) finds use in smaller deployments or as edge storage. Others include hyper-converged platforms for scale-out environments. The New Zealand Data Center Storage Market sees SAN as the backbone of large-scale infrastructure.

By Component

Hardware remains the dominant revenue contributor, driven by server racks, SSD arrays, and switches. Software, however, shows faster growth through SDS and analytics-driven management tools. Advanced storage controllers, deduplication software, and encryption modules lead innovation. The New Zealand Data Center Storage Market adopts integrated software-hardware stacks for operational efficiency.

By Medium

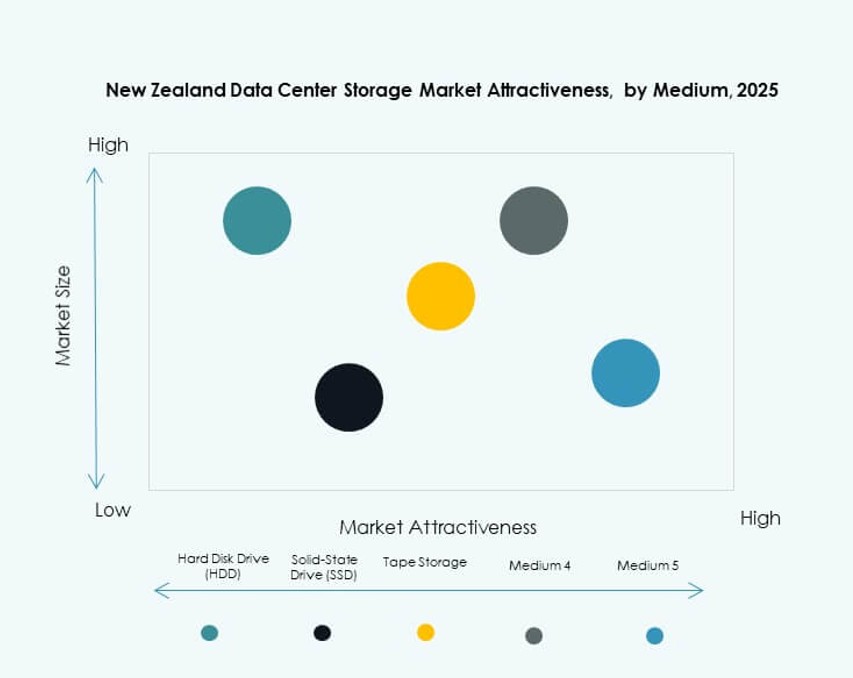

Solid-State Drives (SSD) lead in speed-sensitive workloads, offering better IOPS and energy efficiency. HDDs retain use in archival and bulk storage scenarios. Tape storage is used in regulated industries with long-term retention needs. SSD’s performance advantage makes it the top choice in newer deployments. The New Zealand Data Center Storage Market aligns storage medium with workload characteristics.

By Deployment Model

Cloud-based models dominate new deployments due to flexibility and scalability. On-premises storage persists in regulated and latency-sensitive sectors. Hybrid models gain traction, blending local control with cloud elasticity. Enterprises seek seamless integration across environments. The New Zealand Data Center Storage Market sees hybrid storage as the model of choice for digital transformation.

By Application

IT and Telecom lead market share, driven by 5G, streaming, and edge computing. BFSI follows closely with high-security requirements and fast transactional data needs. Government initiatives increase public sector storage spending. Healthcare sees growth due to telemedicine and EMR adoption. The New Zealand Data Center Storage Market serves these sectors with customized, regulation-compliant platforms.

Regional Insights

Auckland Leads with Over 50% Share Due to Data Density and Network Strength

Auckland dominates the New Zealand Data Center Storage Market, holding more than 50% share. It hosts the largest data centers and the most advanced network interconnections. High enterprise concentration, carrier hotels, and submarine cable landings drive growth. The city supports hyperscale facilities, colocation hubs, and financial sector storage. Strong talent pool and reliable energy supply enable continuous expansion. It remains the national epicenter for mission-critical infrastructure.

- For instance, NEXTDC is developing a Tier IV data center in Auckland designed for enterprise-grade resilience and low-latency interconnection.

Wellington and Christchurch Jointly Contribute Around 35% Market Share

Wellington and Christchurch together account for about 35% of the market. Wellington’s government focus drives demand for compliant, sovereign storage. Cloud-first mandates and digital archiving in public agencies fuel local deployments. Christchurch contributes through education and regional enterprise activity. These cities benefit from recent investments in resilient digital infrastructure. Both regions see expanding backup and DRaaS demand in education and health.

- For instance, Spark Digital operates a Wellington data centre aligned to TIA 942 Tier III standards and a Christchurch facility offering resilient colocation and managed services, serving government and enterprise storage needs.

Smaller Regions Account for 15% but Show Future Growth Potential

Smaller towns and regional zones hold around 15% share. Rural healthcare, education digitization, and remote office workflows support gradual storage adoption. Fiber rollouts and local IT upgrades boost regional storage capacity. Edge deployments address latency gaps in isolated areas. Though growth is slower, long-term upside remains strong. The New Zealand Data Center Storage Market expands cautiously in these zones through targeted public-private partnerships.

Competitive Insights:

- Datacom

- Spark Digital

- Revera

- Hewlett Packard Enterprise (HPE)

- Dell Technologies

- IBM Corporation

- NetApp

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Fujitsu Limited

The New Zealand Data Center Storage Market is marked by a mix of local and global players competing across traditional, cloud-based, and hybrid storage platforms. Local firms like Datacom, Spark Digital, and Revera hold strong positions due to their in-country infrastructure, government partnerships, and compliance offerings. Global vendors such as Dell Technologies, HPE, and IBM strengthen their presence through all-flash systems, AI-ready storage, and hyperconverged platforms. These companies leverage channel partnerships and regional alliances to reach public sector and BFSI clients. Huawei and Cisco focus on high-density storage, while NetApp and Fujitsu push for hybrid cloud and data lifecycle solutions. Product innovation, service localization, and regulatory alignment drive market competition. It remains highly fragmented but shows clear consolidation around sovereign cloud services and enterprise-grade performance.

Recent Developments:

- In September 2025, Amazon Web Services (AWS) launched its Asia Pacific (New Zealand) Region, committing over NZ$7.5 billion ($4.4 billion) to data center infrastructure that bolsters local storage and cloud services for digital transformation.

- In August 2025, Spark New Zealand announced that it entered an agreement to sell a 75% interest in its data centre business to Pacific Equity Partners (PEP), valuing the business at up to $705 million and supporting expansion amid rising cloud and AI demand for storage capacity.