Executive summary:

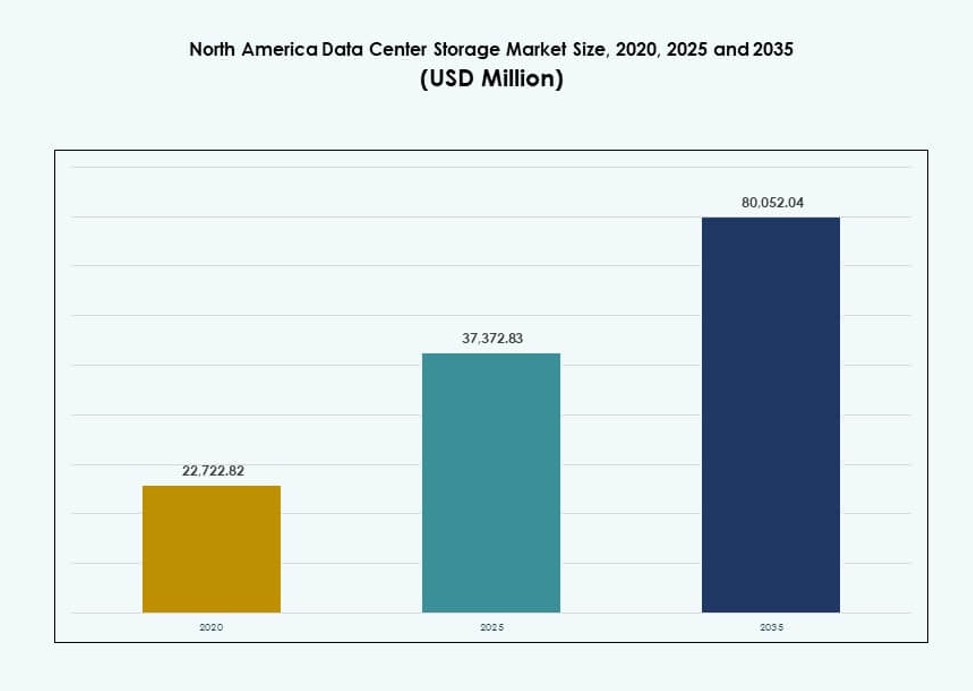

The North America Data Center Storage Market size was valued at USD 22,722.82 million in 2020 to USD 37,372.83 million in 2025 and is anticipated to reach USD 80,052.04 million by 2035, at a CAGR of 7.85% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| North America Data Center Storage Market Size 2025 |

USD 37,372.83 Million |

| North America Data Center Storage Market, CAGR |

7.85% |

| North America Data Center Storage Market Size 2035 |

USD 80,052.04 Million |

Growing enterprise focus on cloud transformation, AI workloads, and real-time analytics is driving significant upgrades in data center storage infrastructure. Organizations are replacing legacy systems with all-flash arrays and NVMe solutions for better performance and scalability. Software-defined and hybrid models are gaining traction across industries seeking agility and lower total cost of ownership. These changes make storage a critical layer in IT modernization, attracting investor interest and vendor innovation across the region.

The United States leads due to its hyperscale dominance, extensive cloud presence, and rapid enterprise adoption of high-performance storage. Canada is emerging through steady digitalization in banking, telecom, and healthcare sectors, supported by data privacy regulations. Mexico is gaining relevance as a strategic location for edge storage and regional cloud hubs, supported by infrastructure investments and growing enterprise demand.

Market Dynamics:

Market Drivers

Rising Demand for High-Performance and Low-Latency Storage Infrastructure

Enterprises require faster data access to support AI, analytics, and cloud workloads. Storage systems now prioritize low latency and high throughput. Organizations replace legacy systems with flash-based and NVMe architectures. This shift supports mission-critical applications and real-time processing needs. Hyperscale operators influence enterprise buying behavior across sectors. The North America Data Center Storage Market benefits from this performance-first mindset. Businesses view storage as a strategic asset rather than a backend utility. Investors see stable returns from long-term infrastructure upgrades.

- For instance, Pure Storage’s FlashArray//X achieves 150 microsecond latency with DirectFlash technology. Organizations replace legacy systems with flash-based and NVMe architectures.

Expansion of Cloud Services and Hybrid IT Architectures

Cloud adoption reshapes how enterprises design storage environments. Firms deploy hybrid models to balance control, cost, and scalability. Storage platforms must integrate across on-premises and cloud systems. Vendors respond with cloud-compatible and software-defined solutions. This approach supports workload mobility and disaster recovery needs. The North America Data Center Storage Market gains relevance across cloud ecosystems. Enterprises value flexible architectures that reduce vendor lock-in. Investors favor providers aligned with hybrid cloud strategies.

Growth of Data-Intensive Applications Across Industries

Sectors like BFSI, healthcare, and telecom generate large data volumes. These industries demand secure, scalable, and resilient storage platforms. Compliance and data protection requirements raise storage complexity. Vendors focus on automation and intelligent management tools. Storage now supports business continuity and regulatory adherence. The North America Data Center Storage Market serves critical digital infrastructure roles. Enterprises depend on reliable storage to protect operational continuity. Capital flows favor vendors with strong enterprise penetration.

- For instance, Dell PowerStore 5000T delivers 2.4 million IOPS for database workloads in enterprise deployments.

Shift Toward Software-Defined and Disaggregated Storage Models

Organizations seek cost efficiency and deployment flexibility. Software-defined storage separates hardware from control layers. This model improves scalability and resource utilization. Disaggregated systems align with composable data center designs. Enterprises reduce capital intensity through modular expansion paths. The North America Data Center Storage Market reflects this architectural evolution. Businesses gain agility and better cost visibility. Investors track platforms that scale across diverse environments.

Market Trends

Adoption of Consumption-Based and Subscription Storage Models

Enterprises prefer predictable spending over large upfront purchases. Vendors offer storage through pay-as-you-use structures. This trend aligns storage costs with workload demand. Financial flexibility supports faster procurement decisions. Providers bundle software, support, and upgrades into unified plans. The North America Data Center Storage Market adapts to service-oriented buying patterns. Enterprises gain budget control and operational clarity. Vendors improve long-term customer retention.

Integration of Automation and AI-Driven Storage Management

Storage platforms adopt intelligent monitoring and analytics tools. Automation reduces manual intervention and human error. Predictive insights improve capacity planning and fault response. Operations teams manage complex environments with fewer resources. AI-driven tools enhance service reliability and uptime. The North America Data Center Storage Market evolves toward autonomous operations. Enterprises prioritize efficiency and resilience gains. Investors favor vendors with strong software capabilities.

Increased Focus on Data Security and Cyber Resilience

Cyber threats reshape storage design priorities. Vendors embed encryption, immutability, and secure snapshots. Enterprises treat storage as a frontline defense layer. Regulatory scrutiny increases demand for compliant architectures. Secure backup and recovery gain strategic importance. The North America Data Center Storage Market reflects heightened security awareness. Enterprises invest in protection-first storage solutions. Capital flows support vendors with strong security portfolios.

Optimization for Multi-Cloud and Edge Deployments

Enterprises distribute workloads across multiple cloud platforms. Storage systems must support portability and consistent performance. Edge deployments require compact and efficient storage designs. Vendors adapt products for distributed architectures. Unified management across locations gains importance. The North America Data Center Storage Market aligns with decentralized IT models. Enterprises seek seamless data mobility. Providers benefit from broad deployment support.

Market Challenges

High Capital Costs and Complex Migration Processes

Storage modernization requires significant financial commitment. Legacy system migration poses operational risks. Downtime concerns slow upgrade decisions. Integration complexity strains internal IT teams. Skills gaps increase reliance on external partners. The North America Data Center Storage Market faces adoption friction in cost-sensitive segments. Enterprises delay investments during economic uncertainty. Vendors must justify clear return profiles.

Rising Energy Consumption and Infrastructure Constraints

High-density storage increases power and cooling demands. Data centers face sustainability and capacity pressures. Energy costs affect total ownership economics. Operators balance performance with efficiency goals. Infrastructure limitations restrict rapid scale-up plans. The North America Data Center Storage Market encounters operational trade-offs. Enterprises seek efficient designs without performance loss. Providers face pressure to optimize energy profiles.

Market Opportunities

Expansion of AI, Analytics, and Data Monetization Use Cases

AI workloads require fast and scalable storage backends. Enterprises extract value from large datasets. Advanced storage supports data-driven decision models. Vendors tailor solutions for AI pipelines and analytics engines. Demand grows across enterprise and research environments. The North America Data Center Storage Market benefits from data-centric strategies. Businesses invest to unlock new revenue streams. Investors favor AI-aligned storage platforms.

Growth of Edge Computing and Regional Data Localization

Edge sites require compact and resilient storage systems. Regulatory rules encourage local data processing. Enterprises deploy regional facilities closer to users. Vendors design storage for constrained environments. This shift opens new deployment scenarios. The North America Data Center Storage Market expands beyond core hubs. Enterprises gain latency and compliance advantages. Providers access untapped regional demand.

Market Segmentation

By Storage Type

Traditional storage maintains presence in legacy workloads. All-flash storage dominates performance-critical environments. Hybrid storage balances cost and speed for mixed workloads. Enterprises favor flash for databases and analytics. Hybrid systems support gradual modernization paths. The North America Data Center Storage Market reflects this mix. Flash adoption drives premium revenue share. Growth aligns with enterprise modernization cycles.

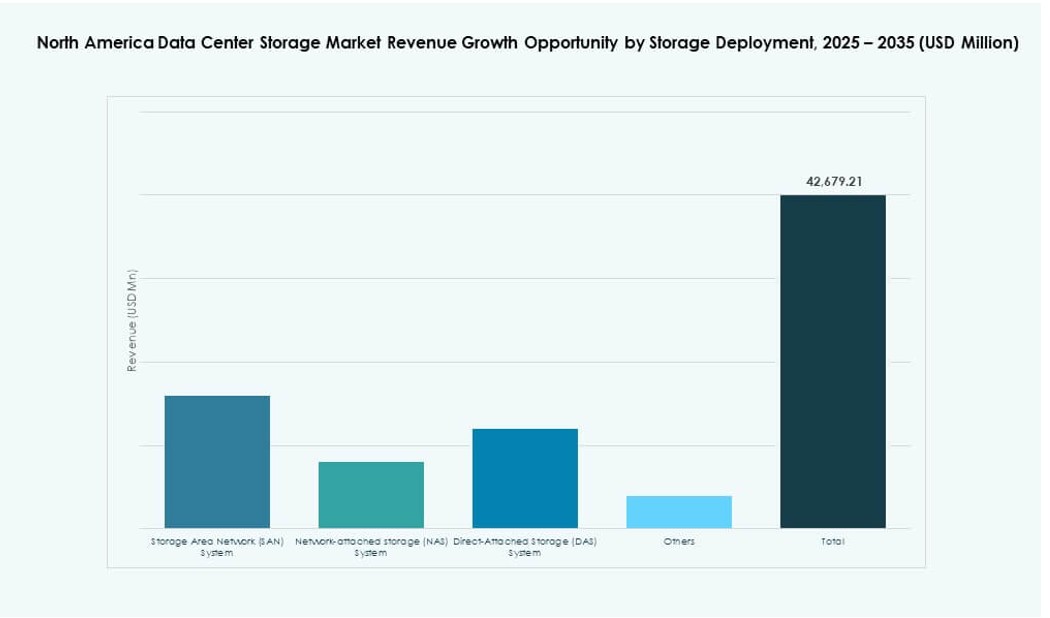

By Storage Deployment

SAN systems lead large enterprise environments. NAS systems support file-based and collaboration workloads. DAS serves localized and edge use cases. SAN benefits from scalability and control features. Enterprises select deployment based on workload type. The North America Data Center Storage Market shows strong SAN penetration. NAS gains traction in unstructured data growth. Deployment diversity supports broad vendor participation.

By Component

Hardware accounts for a major revenue share. Software grows faster due to management and security needs. Enterprises invest in orchestration and analytics layers. Software enhances hardware utilization rates. Vendors bundle components into integrated offerings. The North America Data Center Storage Market shifts toward software value. Enterprises seek intelligence over raw capacity. Software margins attract investor interest.

By Medium

HDD remains relevant for archival storage. SSD leads performance-driven deployments. Tape storage supports long-term data retention. Enterprises optimize cost through tiered media use. SSD adoption rises in mission-critical systems. The North America Data Center Storage Market favors SSD growth. HDD and tape retain niche roles. Media diversity supports lifecycle management.

By Deployment Model

On-premises remains vital for regulated sectors. Cloud-based models grow across enterprises. Hybrid deployments dominate strategic planning. Firms balance control with scalability. Vendors align offerings with hybrid demand. The North America Data Center Storage Market centers on hybrid models. Enterprises gain flexibility and resilience. Providers capture recurring revenue streams.

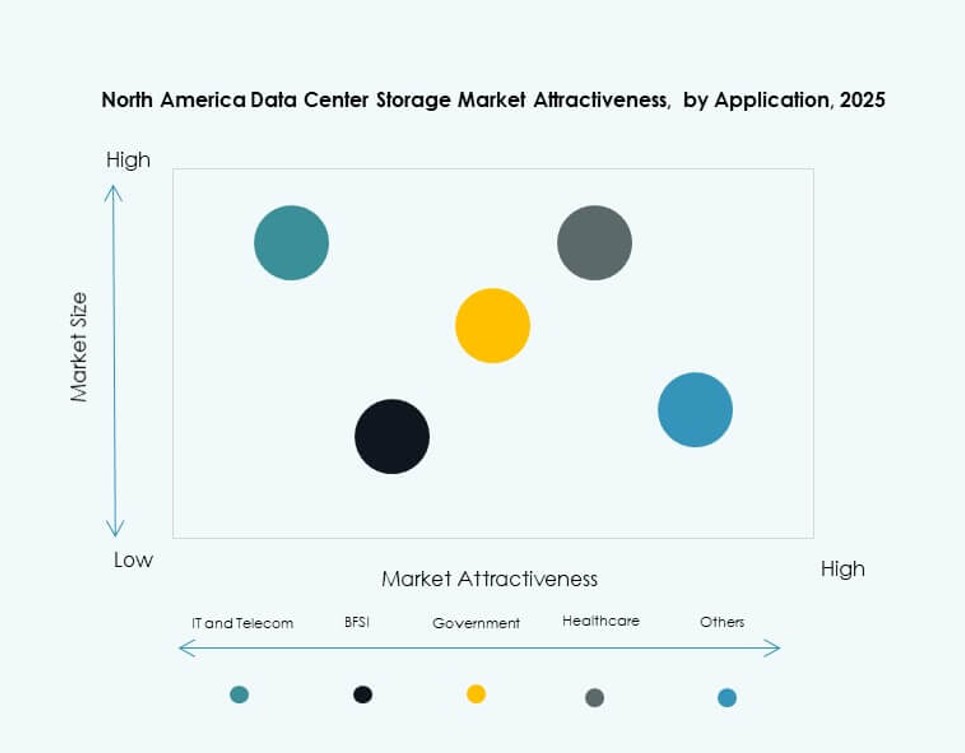

By Application

IT and telecom lead storage demand. BFSI prioritizes security and uptime. Healthcare drives growth through data compliance needs. Government adopts secure and sovereign storage. Other sectors expand digital operations. The North America Data Center Storage Market serves diverse applications. Demand links closely to digital maturity. Sector diversity stabilizes market growth.

Regional Insights

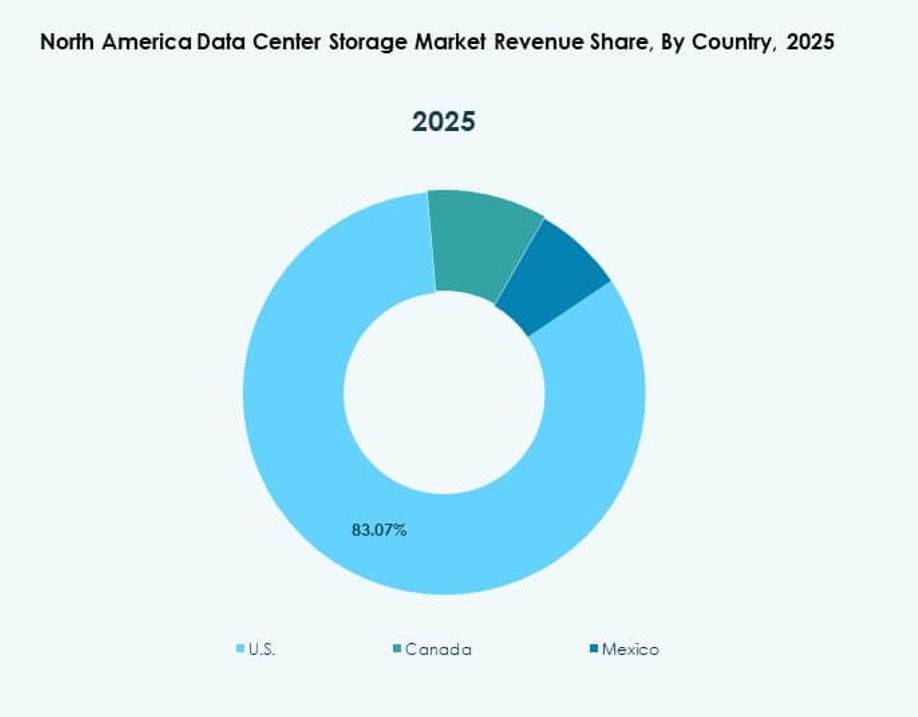

United States

The United States holds about 70% market share. Hyperscale cloud providers drive large-scale deployments. Enterprise digital transformation sustains steady demand. Advanced infrastructure supports high-density storage. Innovation adoption remains strong across sectors. The North America Data Center Storage Market centers on this subregion. Vendor competition stays intense. Investment activity remains high.

Canada

Canada accounts for nearly 20% market share. Banking and telecom sectors fuel storage demand. AI research and cloud adoption gain pace. Data sovereignty supports local deployments. Enterprises modernize legacy infrastructure steadily. The North America Data Center Storage Market sees stable Canadian growth. Policy support strengthens investor confidence.

- For instance, AWS Canada Central region includes 3 Availability Zones for sovereign data storage and AI compute. Data sovereignty supports local deployments.

Mexico

Mexico holds close to 10% market share. New data center builds support regional demand. Nearshoring trends encourage digital infrastructure growth. Enterprises adopt storage to support cloud services. Cost advantages attract regional investments. The North America Data Center Storage Market expands southward. Growth potential remains strong.

- For instance, KIO Data Centers operates hyperscale facilities in Querétaro that support cloud and enterprise storage deployments. Nearshoring trends continue to accelerate digital infrastructure investment in the region.

Competitive Insights:

- Hewlett Packard Enterprise Development LP (HPE)

- Dell Technologies

- IBM Corporation

- NetApp

- Cisco Systems, Inc.

- Lenovo Group

- Seagate Technology

- Veeam Software

- Cohesity, Inc.

- Hitachi Vantara

The North America Data Center Storage Market features intense competition among global technology leaders and specialized storage providers. Companies like HPE, Dell, IBM, and NetApp offer broad portfolios covering all-flash arrays, hybrid storage, and software-defined platforms. It benefits from aggressive investments in innovation, cloud integration, and AI-optimized storage solutions. Vendors differentiate through performance, automation, security features, and support services. Strategic partnerships, mergers, and cloud-aligned product launches shape market dynamics. Software-centric players gain ground by delivering flexibility, scalability, and reduced total cost of ownership. Customer retention strategies center around hybrid cloud compatibility, subscription pricing, and workload-aware orchestration. Emerging players focus on edge-ready solutions and autonomous storage operations. Market consolidation continues as enterprises demand end-to-end platforms with strong service reliability.

Recent Developments:

- In September 2025, Data Storage Corporation (DTST) closed the sale of its CloudFirst business to Performive. The transaction generated about $40 million in gross proceeds, enabling targeted acquisitions in AI, GPU technologies, and cybersecurity within the data storage sector.

- In March 2025, Hewlett Packard Enterprise (HPE) introduced its latest storageplatform for AI‑ready data centers in North America, expanding its GreenLake‑based block and file services to support higher performance and cyber‑resilient workloads for enterprise and cloud providers.