Executive summary:

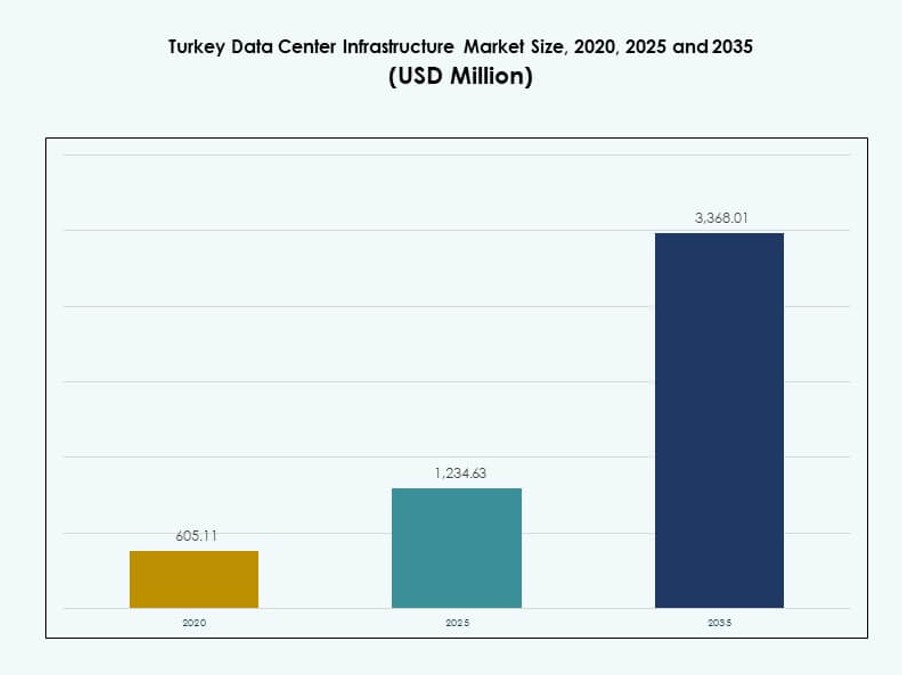

The Turkey Data Center Infrastructure Market size was valued at USD 605.11 million in 2020 to USD 1,234.63 million in 2025 and is anticipated to reach USD 3,368.01 million by 2035, at a CAGR of 10.47% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Turkey Data Center Infrastructure Market Size 2025 |

USD 1,234.63 Million |

| Turkey Data Center Infrastructure Market, CAGR |

10.47% |

| Turkey Data Center Infrastructure Market Size 2035 |

USD 3,368.01 Million |

Cloud service adoption, digital government programs, and AI workloads are key drivers of infrastructure demand in Turkey. Enterprises are shifting to scalable and hybrid IT environments, requiring upgrades in power, cooling, and network systems. High-performance computing, cybersecurity readiness, and data localization needs are transforming procurement strategies. These changes make Turkey a critical investment zone for technology providers and hyperscale developers targeting regional market expansion.

Istanbul remains the dominant hub due to its connectivity, economic influence, and access to enterprise customers. Ankara and Izmir are emerging as important growth corridors, supported by infrastructure incentives and growing tech ecosystems. Eastern and Southeastern regions show long-term potential, driven by digital inclusion policies and regional development plans aiming to decentralize capacity.

Market Dynamics:

Market Drivers

Expansion of Cloud Services and Enterprise Digital Transformation Fuel Infrastructure Growth

The Turkey Data Center Infrastructure Market is expanding as demand grows for high-performance computing, data security, and remote access. Cloud service providers are scaling operations to serve industries like banking, telecom, and logistics. Enterprises are shifting to hybrid IT models, adopting colocation and edge solutions for flexibility. Demand for real-time analytics and low-latency access is driving server upgrades and high-speed connectivity. Domestic cloud platforms are increasing in number to meet local data sovereignty requirements. The shift toward containerized applications and virtualized environments is redefining infrastructure needs. Government incentives and digital economy programs also support ecosystem growth. The Turkey Data Center Infrastructure Market continues to attract strategic investments from global and regional players. Its expansion aligns with national goals for tech modernization and competitiveness.

- For instance, Turkcell operates eight core data centers totaling 41.5 MW IT load capacity across Tekirdag, Gebze, Ankara, and Izmir as of 2025, with plans to add 8.4 MW by year-end.

Rising Demand for AI, IoT, and Data Analytics Platforms Spurs IT Infrastructure Modernization

Enterprises in Turkey are deploying AI and machine learning workloads that require GPU-accelerated data center capacity. Industrial IoT deployments in manufacturing and energy sectors further drive edge infrastructure investments. To support these demands, operators are upgrading legacy systems with high-density servers, NVMe storage, and scalable network switches. IT transformation is also pushing for improved orchestration tools, SDN, and DCIM platforms. The Turkey Data Center Infrastructure Market supports this shift by offering modular designs and cloud-ready frameworks. Businesses prioritize performance, uptime, and compliance as they digitize their core operations. Multi-tenant data centers increasingly offer services tailored to high-compute environments. These changes reflect a shift from traditional storage to intelligent data processing infrastructure. The market helps position Turkey as a regional tech hub for next-gen applications.

Growth in E-Commerce, OTT, and Mobile Usage Boosts Demand for Scalable Data Center Capacity

Turkey’s rapidly growing digital economy, driven by e-commerce platforms and streaming services, puts pressure on IT infrastructure. Online transactions, personalized ads, and video streaming require robust back-end processing and storage. Telecom companies and content providers are expanding data center footprints to reduce latency. The Turkey Data Center Infrastructure Market plays a critical role in supporting this growth through power-dense and energy-efficient systems. Growing smartphone usage and 5G rollouts are creating new edge workloads, especially in urban areas. Businesses are also integrating CRM and ERP systems into cloud platforms to scale operations. These trends increase demand for regional availability zones and disaster recovery setups. Large enterprises and SMBs alike seek flexible hosting models. The market enables this digital acceleration while supporting compliance with evolving data regulations.

Government Digitization, Cybersecurity Priorities, and Infrastructure Localization Drive Strategic Investment

Turkey’s national digital transformation strategy encourages cloud-first adoption in public services, which increases demand for secure and localized data centers. New regulations mandating data localization and cybersecurity standards are pushing government and financial institutions to upgrade infrastructure. The Turkey Data Center Infrastructure Market facilitates this shift by offering secure and scalable deployment models. Investment incentives for tech parks and smart cities also create demand for Tier III and Tier IV certified facilities. Public-private partnerships are emerging to build sovereign cloud ecosystems. Local players expand their portfolio to meet regulatory and mission-critical workloads. International providers collaborate with Turkish firms to comply with local standards. The market strengthens digital sovereignty while enabling foreign investment and technology transfer.

- For instance, Turkcell powers its expansion with 63 MW solar capacity commissioned and an 18 MW wind plant in Izmir for sustainable, net-zero-aligned data centers by 2050.

Market Trends

Shift Toward Liquid Cooling and Energy-Efficient Infrastructure Designs in High-Density Data Centers

Operators in Turkey are adopting liquid cooling technologies to address the thermal challenges of AI workloads and high-performance computing clusters. Traditional air-cooled systems are being replaced with direct-to-chip and immersion cooling solutions. These systems reduce power usage effectiveness (PUE) while improving rack density. The Turkey Data Center Infrastructure Market sees growing preference for energy-efficient architectures. Green building certifications and renewable integration are key decision factors for hyperscale projects. Modular and containerized designs are helping reduce deployment time and improve scalability. Newer facilities increasingly feature aisle containment, variable-speed fans, and advanced thermal management. These changes support compliance with EU energy directives and global ESG benchmarks. Innovation in this area is enhancing operational sustainability for data center operators.

Rise in Edge Data Center Deployment Across Secondary Cities and Industrial Zones

The demand for low-latency processing is accelerating the rollout of edge data centers in regions beyond Istanbul. These facilities cater to localized content delivery, IoT processing, and industrial automation applications. Operators deploy compact, modular units near telecom towers, factories, and logistic hubs. The Turkey Data Center Infrastructure Market supports this trend by enabling rapid, factory-built installations. Businesses in regions like Izmir and Gaziantep seek to process data closer to the source to reduce transmission delays. This trend also aligns with the adoption of 5G networks and autonomous technologies. The market is evolving toward distributed infrastructure models to enhance network resilience. Vendors offering pre-integrated edge modules are gaining competitive advantage. Local governments also support this development to bridge the urban-rural digital divide.

Integration of DCIM, AI-Based Monitoring, and Remote Infrastructure Management Tools

The need for enhanced uptime, proactive maintenance, and efficient resource usage is driving DCIM adoption in Turkey. Data center operators increasingly integrate AI-driven tools to monitor thermal loads, equipment health, and power usage trends. These systems enable predictive maintenance and automated response to faults. The Turkey Data Center Infrastructure Market is responding by offering cloud-based and API-enabled management platforms. These tools improve SLA compliance while reducing manual intervention. Enterprises and colocation providers deploy smart sensors and digital twins to simulate asset performance. Remote management has become a standard feature post-COVID, especially for distributed infrastructure. These trends promote visibility, cost optimization, and agility across data center operations. Software-defined infrastructure is now embedded in most new project bids.

Increased Activity in Greenfield Developments and Strategic Expansion by Colocation Providers

New players and existing colocation firms are actively acquiring land and securing energy supply for future-ready facilities. Turkey’s strategic location between Europe and Asia makes it ideal for interconnectivity and regional expansion. The Turkey Data Center Infrastructure Market benefits from this as hyperscale and wholesale providers enter long-term leases and power purchase agreements. Developers now prefer greenfield sites with renewable energy potential and fiber proximity. M&A activity is rising, with foreign firms partnering with local players. These expansions include purpose-built campuses with phased deployment plans. Operators are targeting finance, cloud, and public sectors as anchor tenants. Neutral-host models and carrier-agnostic facilities are gaining preference. These trends reflect a maturing and globally relevant infrastructure ecosystem.

Market Challenges

Grid Instability, Power Supply Constraints, and Limited Access to Renewable Energy Impact Facility Expansion

Power availability and energy pricing remain top concerns for data center operators in Turkey. Frequent outages in certain regions and rising electricity costs add complexity to capacity planning. Access to stable and redundant power sources becomes critical for Tier III and IV projects. The Turkey Data Center Infrastructure Market faces obstacles from aging grid infrastructure and limited utility cooperation. Backup systems increase CAPEX and operating complexity. Renewable energy options like solar and wind are underutilized due to permitting and storage limitations. Lack of a standardized green energy policy slows adoption among hyperscale developers. These constraints hinder the pace of greenfield projects and impact cost competitiveness.

Talent Shortages, Regulatory Delays, and Permitting Barriers Affect Construction Timelines

Qualified professionals in data center design, network engineering, and facilities operations are in short supply. Skill gaps delay project execution and affect long-term maintenance planning. The Turkey Data Center Infrastructure Market also faces hurdles from lengthy permitting processes and unclear zoning rules. Data localization laws lack standard implementation frameworks, creating ambiguity for international operators. Environmental and seismic regulations add complexity to civil infrastructure work. Delays in fiber deployment and interconnection licensing limit flexibility in site selection. These challenges raise risks for foreign investors and increase time-to-market. Addressing these issues is essential to sustain infrastructure momentum.

Market Opportunities

Growth Potential in Public Cloud Adoption and Digital Government Services Creates New Infrastructure Demand

Public cloud demand is rising across Turkey’s banking, retail, and public sectors. Digital government programs are expanding e-services and citizen platforms, needing secure and scalable backend infrastructure. The Turkey Data Center Infrastructure Market supports this transition through regional cloud availability zones. Cloud-native platforms and hybrid models open opportunities for colocation and enterprise players. Investment in smart cities and e-health projects further amplifies demand for localized storage and compute capacity.

Increased Interest from International Hyperscale and Telecom Firms Expands Investment Scope

Turkey’s geographic advantage and EU-adjacent status attract major global players to invest in new campuses. Telecom operators seek new routes and interconnectivity hubs, opening space for regional IXPs. The Turkey Data Center Infrastructure Market enables such expansions with favorable location, fiber routes, and a young digital economy. Partnerships between local and global firms can unlock capital, technology, and expertise. These trends offer strong ROI prospects for strategic investors.

Market Segmentation

By Infrastructure Type

The Turkey Data Center Infrastructure Market is dominated by IT & network infrastructure due to increasing server, storage, and networking demands. Electrical infrastructure follows closely, driven by UPS and power distribution upgrades to support uptime. Mechanical and civil components are growing with new greenfield and retrofitting projects. Modular and prefabricated systems see rising adoption for speed and cost efficiency.

By Electrical Infrastructure

Uninterruptible power supply (UPS) systems hold the largest share due to demand for Tier III/IV readiness and reliability. Battery energy storage systems (BESS) are gaining ground as operators look to offset energy instability. Power distribution units (PDUs) and transfer switches see growing investment to enable redundancy and flexible power routing.

By Mechanical Infrastructure

Cooling units such as CRAC/CRAH systems remain key investments, especially in high-density deployments. Chillers and containment systems are gaining share as liquid cooling expands. Modular piping and thermal automation tools improve energy efficiency and maintain uptime. This segment reflects the need for adaptable, low-PUE systems.

By Civil / Structural & Architectural

Superstructure development leads this segment, particularly in new hyperscale builds with steel/concrete frames. Raised floors and suspended ceilings follow, supporting airflow management. Modular and prefabricated buildings reduce construction time. Building envelopes and site preparation are essential for seismic resilience and thermal regulation.

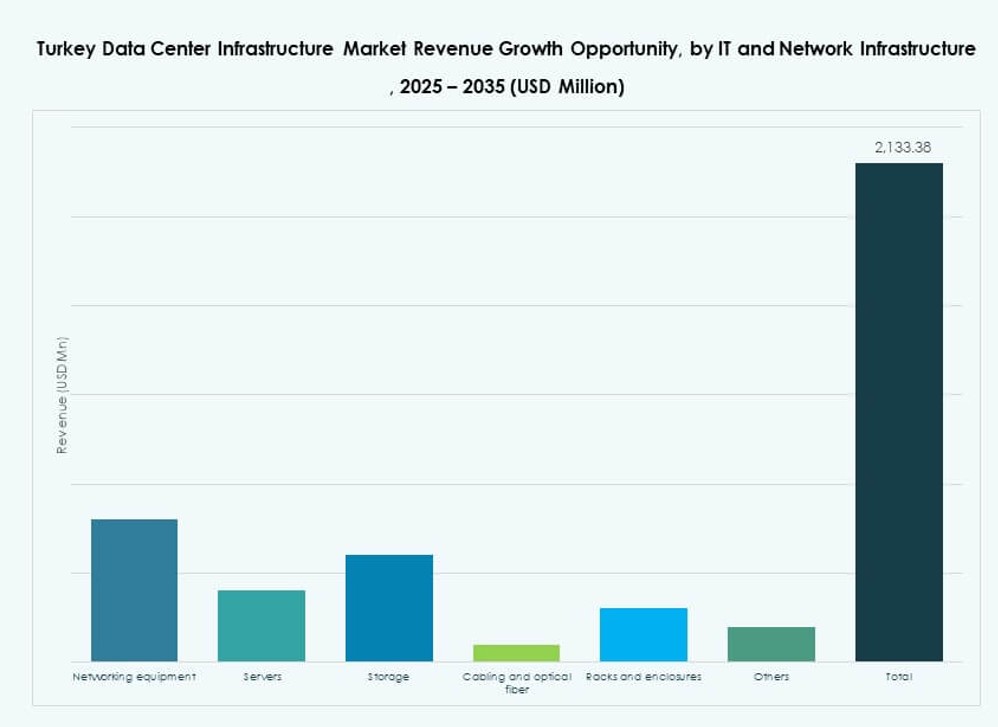

By IT & Network Infrastructure

Servers and racks dominate the IT segment due to growing demand for high-density computing. Storage solutions are expanding with cloud and analytics workloads. Networking gear and fiber cabling support scalable and redundant connectivity. Vendors focus on rack-ready solutions and software-defined integration.

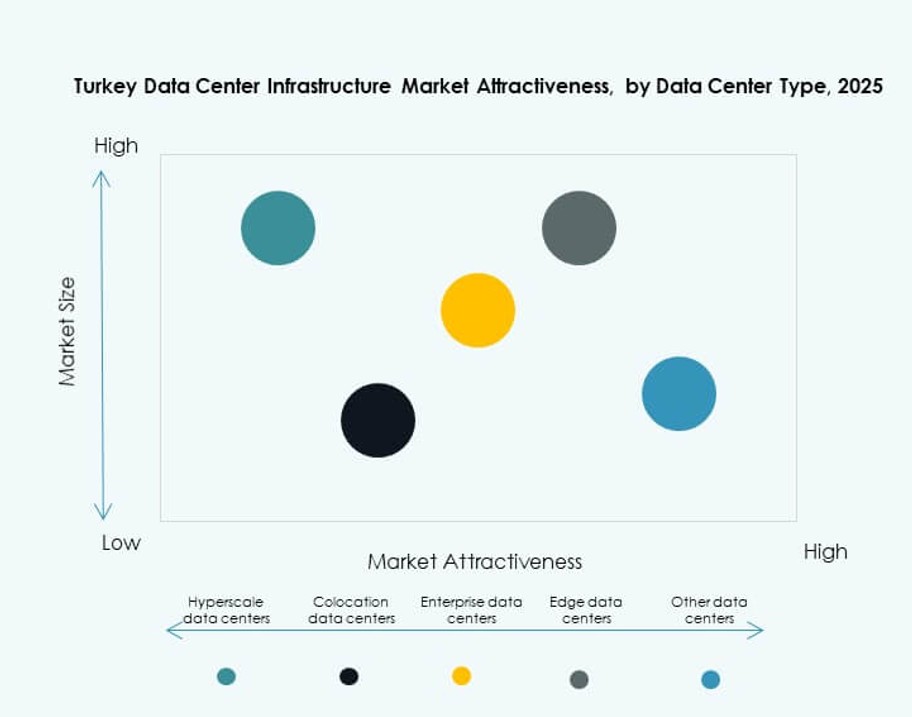

By Data Center Type

Colocation data centers hold the largest share due to growing demand from enterprises seeking shared infrastructure. Hyperscale and edge data centers are emerging fast with AI and content delivery needs. Enterprise data centers still exist but are declining as firms move to cloud and hybrid models.

By Delivery Model

Turnkey and design-build/EPC models dominate due to their speed and reliability. Retrofit and upgrade projects are increasing, especially among government and telecom players. Modular factory-built deployments are gaining traction in remote and edge locations.

By Tier Type

Tier III facilities dominate due to balanced cost and performance, while Tier IV is gaining traction among financial and public sectors. Tier I and II are limited to small and non-critical applications. Compliance and service level expectations push operators toward Tier III+ certification.

Regional Insights

Marmara Region Leads with Istanbul as the Central Data Hub Holding 58% Market Share

Istanbul dominates the Turkey Data Center Infrastructure Market, benefiting from dense population, fiber connectivity, and enterprise presence. The Marmara region accounts for 58% of the market, hosting colocation and hyperscale projects. Proximity to Europe supports regional cloud availability zones and interconnection hubs. Istanbul also offers robust power and telco infrastructure, making it the top destination for data center investments.

Anatolian and Aegean Regions Witness Emerging Growth and Edge Infrastructure Deployment

The Anatolian region, including Ankara, contributes 22% market share, driven by government, telecom, and enterprise demand. Government digitization efforts and cloud-first policies support infrastructure growth. The Aegean region (12%) sees demand from industrial zones and growing technology parks, particularly in Izmir. Edge and modular data centers are emerging in these regions to support localized processing.

- For instance, Turkcell and Google Cloud announced a partnership for Turkey’s first hyperscale cloud region in Ankara, featuring a 3-site architecture with construction starting in Q1 2026 and full capacity by 2028.

Eastern and Southeastern Regions Remain Nascent but Strategic for Future Expansion

Eastern and Southeastern Turkey collectively represent 8% of the market but offer future growth potential. Infrastructure remains underdeveloped, but 5G, smart city, and digital inclusion initiatives are creating interest. Logistics corridors and cross-border trade routes enhance the strategic relevance of these regions for edge deployments. Government subsidies and land availability further support expansion prospects.

- For instance, Turkcell contributes to Türkiye’s innovation ecosystem through its dedicated R&D operations, employing over 1,200 researchers across advanced ICT, AI, and 5G technologies. The company plays a key role in national digital transformation, supporting smart city and edge infrastructure projects through its technology subsidiary, Turkcell Teknoloji.

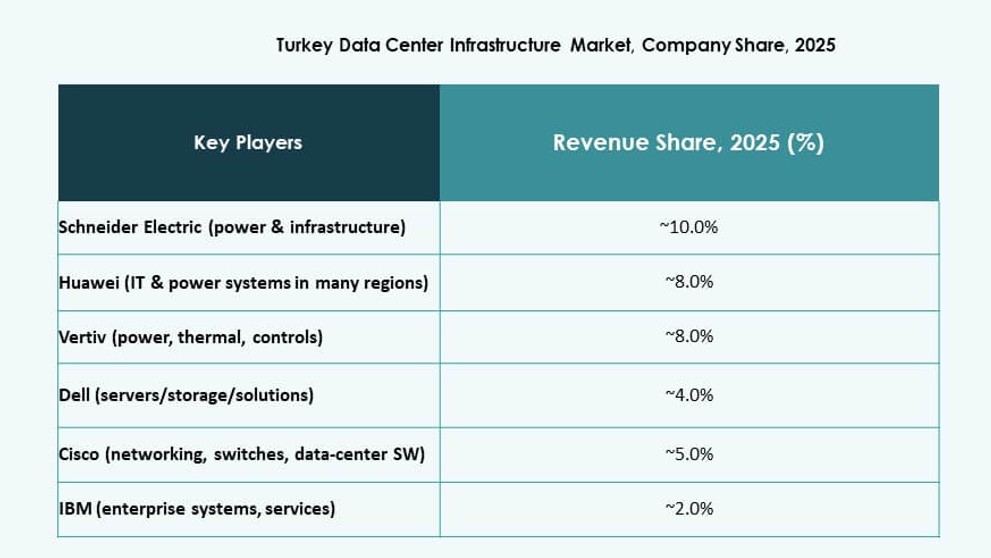

Competitive Insights:

- Khazna Data Centers

- Gulf Data Hub

- ABB

- Cisco Systems, Inc.

- Dell Inc.

- Equinix, Inc.

- Fujitsu

- Hitachi, Ltd.

- IBM

- Schneider Electric

The Turkey Data Center Infrastructure Market features a mix of global technology giants and emerging regional operators. It is shaped by aggressive investments in power systems, cooling units, IT hardware, and modular infrastructure solutions. Schneider Electric and Vertiv lead in power and thermal management, offering turnkey solutions tailored for Tier III and Tier IV facilities. Cisco and Dell dominate in IT and networking equipment, enabling scalable cloud infrastructure. Equinix and Khazna are expanding colocation and hyperscale footprints, often collaborating with local entities. Gulf Data Hub and IBM contribute to the growth of sovereign and hybrid cloud ecosystems. The market remains competitive with strong focus on energy efficiency, compliance, and localized service delivery. Strategic alliances, EPC partnerships, and modular deployments define the current growth landscape. Turkey’s position between Europe and Asia makes it a priority market for global expansion and regional data traffic consolidation.

Recent Developments:

- In November 2025, Turkcell partnered with Google Cloud to build the infrastructure for a new Google Cloud region in Türkiye, set to operate between 2028 and 2029, enhancing cloud services like AI, data storage, and cybersecurity.

- In November 2025, EngageLab Email officially launched its new data center facility in Istanbul, Turkey, expanding its global footprint and enhancing email communication services for enterprises in Europe, Middle East, and Africa. This launch reflects growth in the Turkey Data Center Infrastructure Market, improving service speed, stability, and localized data hosting for international clients

- In May 2025, Trendyol, a leading Turkish e-commerce firm, announced a partnership with Castle Investments to develop a 48MW data center in Ankara, Turkey.