Executive summary:

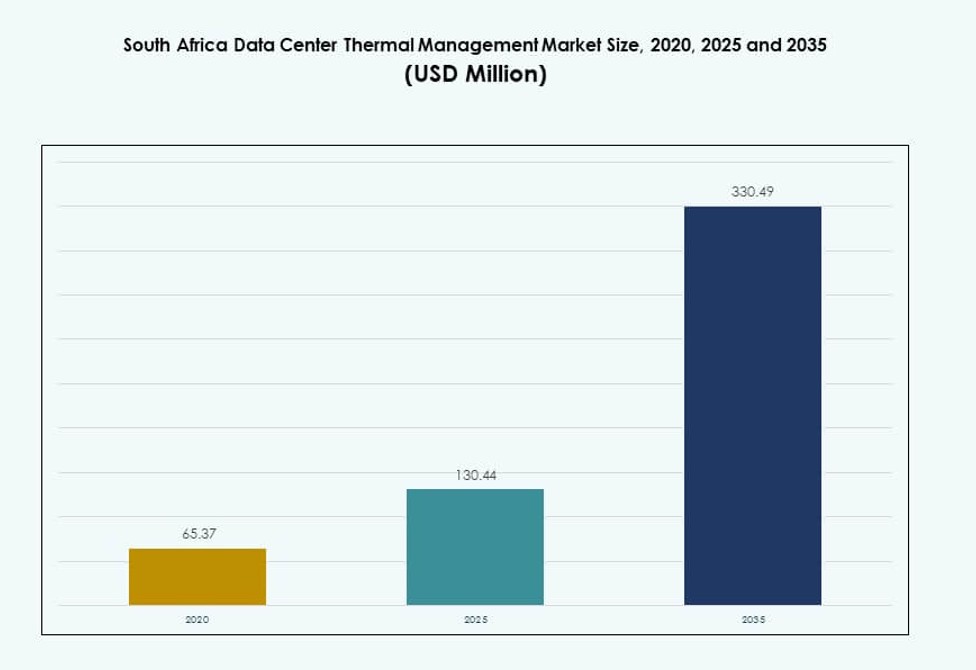

The South Africa Data Center Thermal Management Market size was valued at USD 65.37 million in 2020 to USD 130.44 million in 2025 and is anticipated to reach USD 330.49 million by 2035, at a CAGR of 9.75% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| South Africa Data Center Thermal Management Market Size 2025 |

USD 130.44 Million |

| South Africa Data Center Thermal Management Market, CAGR |

9.75% |

| South Africa Data Center Thermal Management Market Size 2035 |

USD 330.49 Million |

The market is driven by increasing demand for energy-efficient cooling systems in hyperscale and colocation data centers. Liquid cooling, hybrid thermal systems, and modular setups are gaining traction across enterprise and cloud deployments. Regulatory pressure and ESG goals are pushing facilities to adopt low-PUE solutions. Innovation in AI-powered thermal controls further enhances energy savings and system reliability. Businesses view thermal systems as critical to uptime, sustainability, and cost management. The market’s evolution aligns with broader digital infrastructure upgrades. Strategic investors favor facilities equipped with scalable, eco-efficient thermal technologies. This shift reflects a long-term vision for resilient digital operations.

Gauteng leads the market due to its dense concentration of data centers in Johannesburg and Pretoria, backed by power access and fiber infrastructure. Western Cape is emerging as a strong secondary hub with favorable climate conditions supporting efficient cooling. KwaZulu-Natal and Eastern Cape are witnessing rising edge deployments driven by telecom and logistics demand. Regional cooling strategies vary by climate, grid stability, and build density. Urban zones adopt hybrid and AI-based systems, while rural areas lean toward compact and efficient units. The market shows nationwide relevance with distinct regional priorities shaping thermal technology adoption.

Market Dynamics:

Market Drivers

Expansion of AI-Ready Infrastructure and High-Density Computing Demands Greater Cooling Efficiency

The South Africa Data Center Thermal Management Market is driven by surging demand for AI and GPU-intensive computing. Operators are building high-density data halls that require precise thermal control. Direct-to-chip and liquid cooling solutions help maintain operational efficiency under rising compute loads. Data center operators are under pressure to reduce PUE while handling 30–50 kW per rack deployments. These technologies improve uptime and hardware lifespan. AI workloads push thermal systems to adapt rapidly. The market supports strategic IT infrastructure transformation across sectors. It enables long-term investment confidence by enhancing thermal reliability. Businesses prioritize sustainability and performance, making thermal upgrades essential.

- For instance, Teraco’s JB4 expansion in Johannesburg completed in 2025 features liquid-to-liquid cooling across six data halls, each supporting 5 MW of critical IT power for high-density AI workloads.

Adoption of Liquid Cooling and Sustainable Technologies Amid Power and Water Constraints

Enterprises seek lower energy and water usage amid rising sustainability regulations. Liquid cooling systems outperform traditional air cooling in efficiency and adaptability. Technologies like rear-door heat exchangers and immersion cooling support dense server setups. New builds incorporate hybrid systems combining liquid and air for optimized loads. Investors prefer facilities that integrate low PUE and WUE metrics. The South Africa Data Center Thermal Management Market attracts funding by showcasing measurable environmental impact. Water-scarce areas like Gauteng push data centers toward dry and semi-liquid options. Modular cooling adds flexibility to varied compute environments. Adoption of sustainable cooling helps meet ESG and compliance goals.

Digital Infrastructure Push Supported by Government and Private Sector Investments

The national drive for digital transformation includes rapid expansion of cloud zones and enterprise facilities. Government initiatives promote data sovereignty and localized processing capacity. Telecom and energy sectors are partnering with global hyperscalers to deploy edge and core data centers. These sites need reliable and scalable thermal systems. Strategic zones like Johannesburg host large-scale data hubs demanding next-gen cooling. It supports national goals to become a regional digital gateway. Thermal management is central to operational stability in these initiatives. The market aligns with broader ICT development goals. South Africa’s digital economy roadmap reinforces long-term thermal infrastructure demand.

Growing Preference for Smart Cooling Management and AI-Powered Optimization Tools

Enterprises are adopting advanced thermal monitoring powered by AI and analytics. Data center infrastructure management (DCIM) tools offer real-time insights into thermal behavior. AI-driven control systems dynamically adjust cooling loads based on server activity. These platforms reduce overcooling and improve energy cost savings. Predictive analytics help avoid downtime by identifying thermal anomalies. Smart dashboards support better decision-making for facility operators. The South Africa Data Center Thermal Management Market benefits from this integration of hardware with software intelligence. It reduces manual intervention while increasing responsiveness. Businesses see these systems as vital for long-term cost control and sustainability targets.

- For instance, Schneider Electric’s EcoStruxure Data Center Solutions integrate power systems, cooling infrastructure, racks, and management software within a unified architecture. This approach supports coordinated thermal control and improves overall operational efficiency across different data center environments.

Market Trends

Edge Data Centers and Micro Facilities Driving Shift in Cooling Strategies

Edge deployments near urban and remote zones require compact and efficient cooling setups. Smaller footprints call for localized systems like rack-based liquid modules. Telecom-led edge builds favor air-to-liquid hybrid systems for latency-sensitive zones. Energy use must be minimal, given load distribution across multiple sites. It pushes demand for modular and flexible thermal components. Edge growth aligns with 5G rollout and IoT data processing. This trend influences buyer preference toward mobile, scalable thermal units. The South Africa Data Center Thermal Management Market is shaped by these distributed architectures. It is triggering demand for intelligent, low-maintenance thermal designs.

Increased Role of AI and Digital Twins in Cooling Design and Forecasting

Design optimization is shifting from static models to digital twins and CFD simulations. Operators use predictive modeling to simulate airflow and heat distribution before deployment. AI tools offer recommendations to reduce hot spots and increase airflow balance. These systems optimize thermal efficiency without overcooling. Real-time adjustments support variable workloads. Digital twin models enhance ROI by refining equipment placement. The market increasingly values integrated software during planning and retrofitting stages. The South Africa Data Center Thermal Management Market benefits from this trend through better resource planning. It creates a performance-based approach to facility thermal design.

Colocation Growth Accelerating Demand for Adaptive and Multi-Tenant Cooling Solutions

Colocation providers require cooling systems that accommodate diverse IT loads from multiple tenants. Variable workloads and density levels complicate thermal management needs. Adaptive cooling technologies support zoned temperature control within shared spaces. Facilities invest in modular systems that can scale and reconfigure quickly. AI platforms track usage patterns and fine-tune cooling accordingly. Multi-tenant SLAs often require minimum thresholds of thermal uptime. The South Africa Data Center Thermal Management Market aligns with this trend by promoting agile and SLA-compliant cooling architectures. Colocation operators gain competitive advantage with efficient and reliable thermal infrastructure.

Free Cooling Integration and Climate-Responsive Cooling Deployment

South Africa’s climate allows partial use of ambient air and evaporative cooling in select seasons. Facilities are integrating free-air and indirect evaporative methods to cut energy costs. Temperature-controlled fresh air systems improve cooling capacity in cooler regions. Cooling systems adapt to regional temperature ranges, reducing compressor reliance. Sites optimize intake temperatures without compromising IT performance. Use of thermal walls and smart louvers is growing. The South Africa Data Center Thermal Management Market tracks these installations as facilities prioritize eco-efficiency. This trend supports growing awareness of climate-integrated infrastructure planning.

Market Challenges

Power Instability, Load Shedding, and High Energy Costs Limit Efficient Cooling Operations

Power supply constraints in South Africa affect data center thermal system reliability. Frequent load shedding disrupts airflow patterns and risks server overheating. Backup systems increase capital and operating costs for cooling redundancy. Power-hungry cooling units struggle with efficiency during generator operation. Facilities rely on diesel-based backup, adding emissions and costs. Hybrid systems are hard to sustain without consistent power flow. High energy tariffs further raise operational expense, impacting ROI. The South Africa Data Center Thermal Management Market faces significant friction from this challenge. Long-term sustainability of thermal systems depends on grid improvements.

Limited Local Supply Chain for Advanced Thermal Components and Expertise

Access to specialized cooling technologies is constrained by a weak local supply base. Import dependence for high-end chillers and immersion units increases lead times. Currency volatility and customs delays affect pricing stability. Technical expertise for liquid cooling installation and maintenance is limited. Workforce skill gaps slow the adoption of innovative thermal systems. Vendor support for remote facilities is often inadequate. This gap affects edge deployment scalability. The South Africa Data Center Thermal Management Market must build a stronger ecosystem of local integration and service partners. Strengthening domestic capabilities will reduce total lifecycle costs and risk.

Market Opportunities

Strategic Role in Regional Hyperscale and AI Infrastructure Expansion

South Africa’s leadership in regional connectivity attracts hyperscale and AI-led infrastructure investments. These facilities need thermal solutions capable of supporting 30–100 kW rack densities. Demand for smart liquid-based and modular cooling units will increase. Efficient cooling will be a key competitive differentiator for attracting cloud zones. The South Africa Data Center Thermal Management Market holds strategic potential as a thermal technology hub. Exporting expertise and retrofitting services to neighboring countries can further expand value.

Growing Adoption of ESG-Focused Thermal Design and Monitoring Standards

Sustainability goals drive demand for PUE and WUE-compliant cooling systems. ESG-aligned investors prioritize eco-efficient thermal management. Facilities are adding DCIM and AI modules to meet compliance benchmarks. Water-efficient designs like dry coolers and adiabatic systems are gaining traction. The South Africa Data Center Thermal Management Market will benefit from offering solutions aligned with ESG certifications. It opens opportunities for green finance and international investment partnerships.

Market Segmentation

By Data Center Size

Large data centers dominate the South Africa Data Center Thermal Management Market due to their hyperscale and colocation presence. These sites often exceed 20 MW capacity and require robust thermal systems with multiple redundancies. Medium-sized facilities are growing fast, driven by regional enterprise and public sector deployments. Small data centers serve edge and branch-level functions with compact cooling units. The large segment remains most lucrative due to investment volume, while medium centers are vital for localized service delivery.

By Cooling Technology

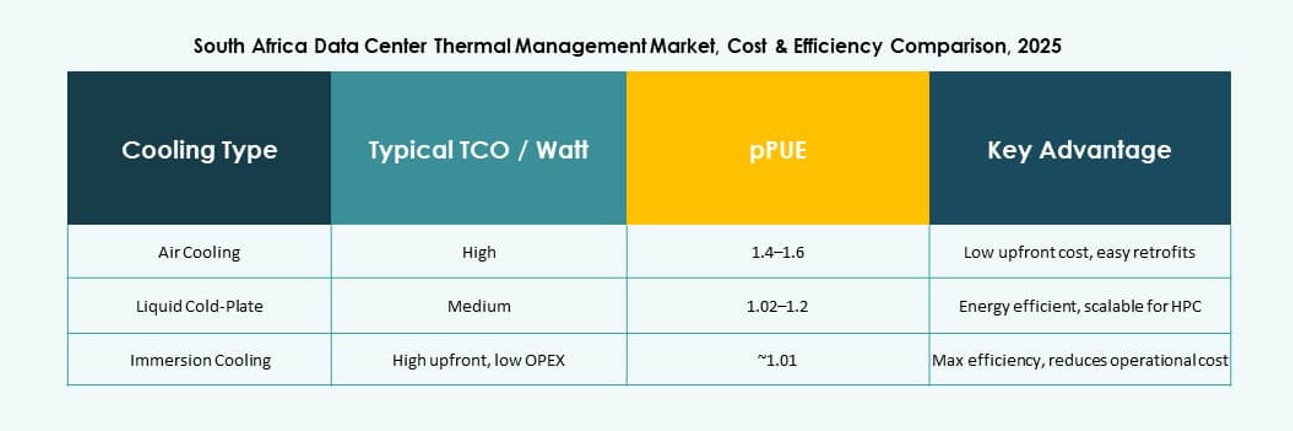

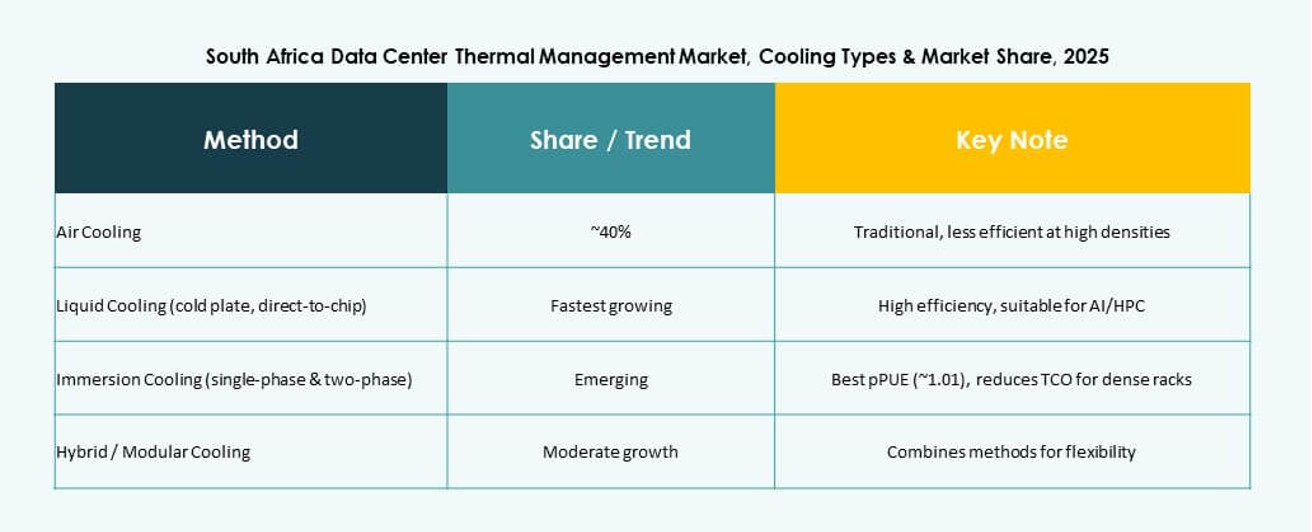

Air-based cooling holds the largest market share, favored for its affordability and ease of deployment. Direct air and hot/cold aisle containment remain widely used across standard-density facilities. However, liquid-based cooling is growing rapidly, especially in high-density environments with AI workloads. Direct-to-chip and immersion cooling are key technologies in this segment. Hybrid systems combining air and liquid ensure flexibility and energy efficiency. The shift toward liquid and hybrid reflects a broader move toward sustainable, high-performance cooling.

By Component

Hardware forms the largest share of the market due to ongoing deployments of chillers, fans, and heat exchangers. Software, particularly DCIM and AI optimization tools, is expanding rapidly as data centers prioritize automation. Services like retrofits, commissioning, and maintenance are essential for lifecycle support. Hardware remains foundational, but software integration enhances performance monitoring. The services segment ensures continuous uptime and adapts systems to evolving workloads.

By Hardware

Cooling units and chillers account for the bulk of spending in the hardware segment. Piping and heat exchangers follow, forming the backbone of both air and liquid systems. Fans, distribution systems, and airflow devices are critical in precision airflow management. Rear door heat exchangers are gaining demand in high-density server zones. The South Africa Data Center Thermal Management Market sees consistent upgrades across hardware categories. The drive for modularity and reliability shapes procurement priorities.

By Software

DCIM dashboards dominate the software segment, enabling centralized thermal monitoring. AI optimization tools help reduce energy consumption by adjusting cooling parameters in real time. CFD simulation software supports facility design and airflow analysis. BMS integration aligns thermal systems with broader building control. The software segment sees strong traction in greenfield and retrofit projects. These tools improve responsiveness, reduce costs, and support ESG targets. Their rising relevance marks a shift toward intelligent thermal operations.

By Services

Installation and commissioning services lead the segment, driven by new data center builds. Preventive maintenance ensures uptime and minimizes risk of equipment failure. Monitoring as a service gains traction, especially for multi-tenant or edge facilities. Retrofits and upgrades address older systems unable to meet new efficiency standards. Services provide essential value in ensuring lifecycle performance. The market values bundled offerings combining installation with long-term monitoring. Growth in third-party service providers expands accessibility and support coverage.

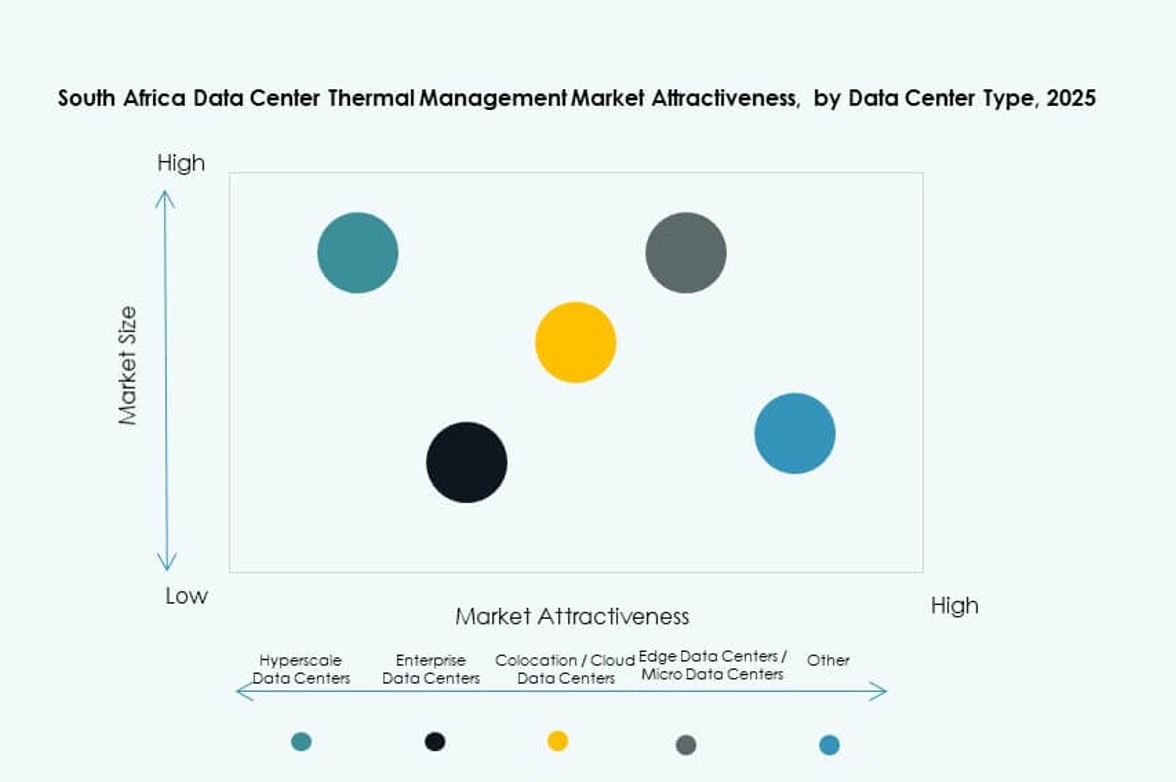

By Data Center Type

Colocation and cloud data centers lead the market due to their rapid expansion across South Africa. Enterprise data centers follow, with firms enhancing on-premise capacity. Hyperscale centers invest heavily in thermal infrastructure for AI and cloud services. Edge and micro data centers serve last-mile computing, demanding compact and efficient cooling. Colocation remains the most dynamic due to diverse tenant needs and uptime SLAs. Each type requires tailored cooling strategies to match operational scale and density.

By Structure

Room-based cooling structures dominate legacy and large data center setups. Row-based and rack-based systems gain demand in high-density and modular environments. Rack-based cooling enables fine-grained control and supports advanced liquid integration. Row-based systems offer flexibility in medium-sized deployments. The structure mix reflects a growing shift toward zone-based thermal control. The South Africa Data Center Thermal Management Market supports this shift by offering diverse deployment options.

Regional Insights

Gauteng Leads with Over 45% Market Share Due to Data Center Density and Connectivity

Gauteng dominates the South Africa Data Center Thermal Management Market, holding more than 45% share. Johannesburg and Pretoria host the majority of hyperscale and colocation facilities. This region offers robust power access, fiber routes, and proximity to enterprise users. Gauteng’s leadership stems from its economic base and digital ecosystem. It also benefits from multiple submarine cable landing links and cloud zones. The market sees strong investment in next-gen cooling to support expansion plans. Thermal innovations here often set national benchmarks.

- For instance, Teraco’s JB7 facility in Johannesburg is designed with closed‑loop chilled water cooling and advanced thermal infrastructure to support high‑density workloads. The campus also aligns with Teraco’s broader renewable energy strategy, including large‑scale solar projects that supply power to its data center portfolio.

Western Cape Emerges as a Key Secondary Hub with Over 25% Share

Western Cape, led by Cape Town, accounts for more than 25% market share. Colder climate conditions improve the feasibility of free cooling and air-based systems. It supports both enterprise and edge facilities catering to the southern corridor. Cloud adoption in the public sector and tech startups drives data center demand. Availability of skilled workforce and academic research enhances cooling innovation. Cape Town benefits from its international business presence and oceanic climate advantage. Energy-efficient cooling solutions see quicker adoption here.

- For instance, Africa Data Centres at its CPT1 facility in Cape Town deployed a self-cooling rack solution from Gold Synergy, enabling high-density hosting without extensive infrastructure upgrades.

KwaZulu-Natal and Eastern Cape Hold Emerging Potential with Around 15% Share

KwaZulu-Natal and Eastern Cape jointly account for about 15% of the market. Durban leads in edge deployments supporting logistics and port operations. These regions require adaptive cooling due to variable temperatures and energy supply. Local enterprises and ISPs are investing in scalable micro data centers. State-backed digital transformation projects are likely to improve thermal infrastructure demand. While still emerging, these subregions represent growth frontiers. The South Africa Data Center Thermal Management Market will benefit from targeted capacity additions here.

Competitive Insights:

- Vertiv Group Corp

- Schneider Electric

- Johnson Controls

- Stulz GmbH

- Rittal GmbH & Co. KG

- Airedale International

- Huawei Technologies Co., Ltd.

- Delta Electronics, Inc.

- Eaton Corporation

- Trane Technologies

The South Africa Data Center Thermal Management Market features a competitive landscape led by global and regional cooling infrastructure providers. Vertiv, Schneider Electric, and Johnson Controls dominate due to their scalable liquid and air-based systems designed for hyperscale and colocation sites. Rittal and Stulz offer efficient modular cooling suited for enterprise and edge deployments. Airedale focuses on precision air conditioning with energy optimization features. Huawei and Delta leverage integrated smart cooling with data center IT systems, increasing competitiveness in hybrid builds. Domestic integrators and engineering firms support installation and services, expanding reach into tier-2 regions. It is evolving with a mix of high-efficiency product innovation, ESG-compliant solutions, and strategic partnerships that align with rising digital infrastructure and sustainability priorities in the country.

Recent Developments:

- In November 2025, Teraco (Digital Realty) completed the expansion of its CT2 data centre in Cape Town. The upgrade incorporates free air cooling with AI-enhanced technology for real-time data hall cooling configuration based on IT load and heat dispersion, achieving industry-leading power usage effectiveness (PUE) and zero water usage.

- In October 2025, Mitsubishi Electric Hydronics & IT Cooling Systems invested in South African sales and services company Intramech The partnership enhances one-stop services for applied HVAC and IT cooling systems, including design, sales, installation, operation, and maintenance, to meet growing data center demands in southern Africa.

- In November 2024, Teraco, a Digital Realty subsidiary, partnered with JUWI and Subsolar to start construction on a 120MW solar PV plant in Free State, South Africa, to power its data centers. JUWI handles design, procurement, construction, and commissioning, with operations expected by late 2026 to support low-carbon energy for cloud and AI workloads.