Executive summary:

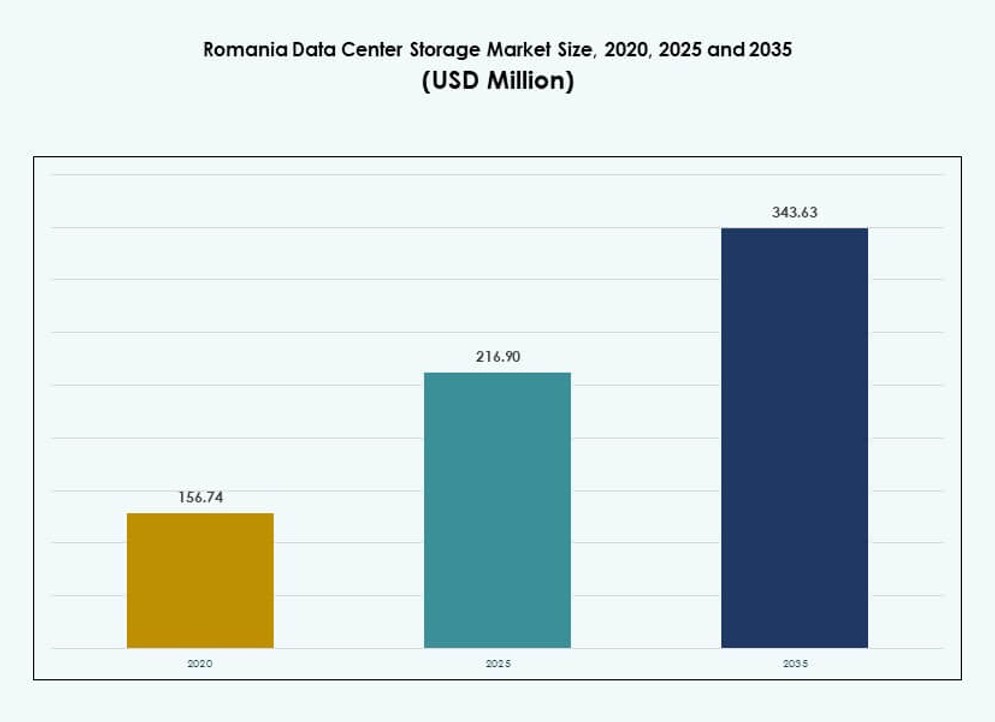

The Romania Data Center Storage Market size was valued at USD 156.74 million in 2020 to USD 216.90 million in 2025 and is anticipated to reach USD 343.63 million by 2035, at a CAGR of 4.65% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Romania Data Center Storage Market Size 2025 |

USD 216.90 Million |

| Romania Data Center Storage Market, CAGR |

4.65% |

| Romania Data Center Storage Market Size 2035 |

USD 343.63 Million |

The market is driven by strong momentum in digitalization across public and private sectors. Enterprises are modernizing IT environments, adopting hybrid and cloud-based storage solutions to support critical workloads. Software-defined storage and flash technologies are gaining traction due to performance and flexibility advantages. Regulatory alignment with EU data protection norms increases demand for secure, scalable infrastructure. Businesses view storage modernization as essential for operational agility, competitive edge, and long-term risk management. It enables faster response times, data-driven decision-making, and business continuity assurance.

Bucharest leads the market due to dense enterprise presence, superior fiber networks, and hyperscale facilities. Cities like Cluj-Napoca and Iași are emerging, supported by growing IT outsourcing, tech parks, and startup ecosystems. Timișoara gains traction due to proximity to western borders and cross-regional connectivity. These regions attract cloud and edge infrastructure investments due to rising digital service needs. Romania’s balanced regional ecosystem supports long-term demand for localized and interconnected storage.

Market Dynamics:

Market Drivers

Surge in Cloud Workloads and Modernization of Legacy Storage Infrastructure Across Enterprise IT Networks

The Romania Data Center Storage Market benefits from enterprise migration toward cloud-native platforms and digital ecosystems. Companies phase out legacy architectures to adopt modern, scalable, and secure storage models. The shift aligns with broader EU digitalization efforts and regional tech acceleration. Demand grows for virtualized and container-based storage to support microservices and remote workforce applications. Cloud interoperability and data mobility shape purchasing decisions across sectors. The public sector also expands digital infrastructure in healthcare and education. Growing fintech and e-commerce activity require flexible, low-latency storage to handle dynamic workloads. Businesses invest in hybrid setups for greater control and compliance assurance. The Romania Data Center Storage Market supports this digital leap with agile and adaptive infrastructure.

Adoption of Virtualization and Software-Defined Storage to Improve Scalability and Efficiency

Virtualized environments are becoming standard in Romania’s mid-size and enterprise-level IT deployments. Software-defined storage (SDS) allows organizations to scale efficiently across multi-tenant and multi-cloud ecosystems. It reduces hardware dependence and centralizes control for heterogeneous data sources. SDS solutions support rapid provisioning and dynamic scaling for high-volume analytics, AI, and IoT use cases. Telecom providers integrate SDS for network resiliency and 5G edge enablement. Startups and SMEs adopt these models due to lower upfront CAPEX and faster go-to-market time. Software-led frameworks help avoid vendor lock-in while optimizing performance. The Romania Data Center Storage Market captures this shift toward agile and open infrastructure. It ensures operators meet unpredictable demand with minimal disruption.

Enterprise Backup, Disaster Recovery, and Security Compliance Demands Shape Storage Investments

Romanian enterprises prioritize resilience, redundancy, and compliance in choosing data storage systems. Cloud-based backup-as-a-service (BaaS) and disaster recovery-as-a-service (DRaaS) solutions are widely adopted. These support ransomware protection, rollback capabilities, and data encryption under regulatory compliance. GDPR enforcement drives localization of data assets and stricter access control policies. BFSI and government sectors invest in high-availability storage architectures with continuous mirroring and automated failover. Multi-zone replication and secure object storage dominate procurement preferences. DR drills and business continuity protocols demand robust, distributed storage. The Romania Data Center Storage Market responds with solutions balancing cost, performance, and risk mitigation.

- For instance, NAV Communications delivers 99.99% uptime via N+1 power and dual-feed fiber in Tier III facilities, meeting ERP and banking compliance needs. These support ransomware protection, rollback capabilities, and data encryption under regulatory compliance.

Strategic Role of Edge Storage in Expanding Real-Time Applications Across Connected Urban Hubs

Edge computing adoption fuels localized storage growth across Romania’s connected cities and industrial zones. Smart infrastructure, real-time analytics, and AI-driven platforms demand faster data processing close to the source. Edge storage enhances latency-sensitive operations in mobility, manufacturing, and utilities. 5G rollout and IoT sensor networks require agile micro data centers with embedded storage layers. Municipal governments deploy edge nodes for surveillance, traffic control, and energy monitoring. Retailers use edge caching to support immersive consumer experiences and fast checkout. Telecom providers build edge POPs integrated with storage to improve regional coverage. The Romania Data Center Storage Market enables these real-time architectures across edge-tier layers.

- For instance, 5G rollout drives edge demand in Romania, contributing a +2.8% growth impact in urban centers by enabling micro data centers that support IoT workloads and real-time analytics applications.

Market Trends

Expansion of Green Storage Infrastructure Aligned with Energy Efficiency and Carbon Goals

Sustainability is shaping procurement in the Romania Data Center Storage Market, with a shift toward energy-efficient infrastructure. Enterprises demand low-power storage components that meet thermal performance standards. SSDs and flash arrays replace legacy HDDs to reduce power consumption per terabyte. Operators integrate cold aisle containment, liquid cooling, and energy reuse systems across facilities. Green-certified storage modules are prioritized in public sector tenders. Hyperscale and colocation providers aim to meet ESG goals via renewable-powered facilities. Demand for sustainable storage will rise as EU green targets tighten. It is driving operational shifts and vendor realignment in the market.

Rise in Demand for AI-Ready and High-Throughput Storage for Data-Centric Workloads

The increasing adoption of AI/ML, big data, and video analytics drives demand for faster and denser storage infrastructure. Organizations in Romania invest in high-throughput systems to process massive unstructured datasets. NVMe-based storage and GPU-optimized storage nodes are deployed across cloud and colocation centers. Financial and public sectors explore real-time fraud detection and surveillance tools needing ultra-low-latency storage. AI model training workloads create bottlenecks on legacy systems, prompting upgrades. Hyperscalers and national cloud platforms deploy scalable object storage for petabyte-scale training. The Romania Data Center Storage Market supports AI-readiness with specialized infrastructure layers.

Storage-as-a-Service (STaaS) Gains Adoption Across Enterprises Seeking Flexible and Cost-Efficient Models

STaaS adoption is rising across Romanian SMEs and mid-market players aiming to reduce infrastructure costs. STaaS enables subscription-based access to enterprise-grade storage without CAPEX burden. It also offers scalability and performance tuning without hardware replacement cycles. MSPs provide tailored STaaS bundles for backup, compliance, and tiered storage needs. Integration with DRaaS and SaaS applications enhances value proposition. STaaS contracts include SLAs around uptime, data durability, and regional data residency. It simplifies infrastructure planning and supports hybrid cloud strategies. The Romania Data Center Storage Market benefits from this subscription-based model adoption.

Interconnect-Centric Storage Clusters Drive Growth in Carrier-Neutral and Edge-Centric Facilities

The need for low-latency, interconnected storage clusters is growing across Romania’s neutral colocation and edge sites. Enterprises increasingly rely on direct interconnects between storage and compute nodes across multiple tenants. Carrier-neutral data centers provide dense interconnect fabrics linking ISPs, content providers, and enterprises. Edge locations offer metro-level redundancy with direct fiber to key business zones. Multi-access edge computing (MEC) frameworks integrate storage for smart grid, retail, and telemedicine. Cloud adjacency and localized caching reduce data hops and support fast content delivery. The Romania Data Center Storage Market grows through these interconnected deployments in regional cities.

Market Challenges

Limited Domestic Manufacturing and Heavy Dependence on External Supply Chains for Storage Hardware

The Romania Data Center Storage Market faces structural constraints due to minimal domestic hardware manufacturing. Data center operators rely on imports for SSDs, HDDs, storage servers, and enclosures. Fluctuating global semiconductor supply and geopolitical risks affect delivery timelines and pricing. Import dependencies create bottlenecks in project execution and hinder scale-out agility. SMEs lack bargaining power to absorb price hikes from OEMs. Delays in customs clearance and logistics strain time-sensitive deployments. Local channel partners face constraints in securing volume discounts or specialized SKUs. The absence of regional storage R&D hubs slows down customization and innovation.

Gaps in Tier Certification, Skilled Workforce, and Interconnect Infrastructure in Secondary Cities

While Bucharest hosts Tier III/IV facilities, Romania’s Tier II cities lag in certified infrastructure and workforce availability. The market outside the capital faces latency issues due to poor fiber penetration and limited interconnection options. Local operators often struggle to secure redundant power, fire suppression, and security protocols matching global norms. Hiring skilled engineers and certified technicians remains a challenge. Vendors hesitate to expand without government incentives or anchor tenants. Regional colocation markets stay fragmented, restricting scale and national coverage. The Romania Data Center Storage Market must bridge this disparity to ensure even growth and infrastructure parity.

Market Opportunities

Expansion of Government Digitalization Programs and EU-Funded Infrastructure Grants

Romania’s National Recovery and Resilience Plan (NRRP) allocates funding for digital public services, cloud infrastructure, and cybersecurity. These initiatives create demand for robust and compliant storage infrastructure across sectors. EU structural funds support greenfield and brownfield data center development with advanced storage modules. Municipal and central government deployments will drive long-term consumption. The Romania Data Center Storage Market benefits from policy alignment and grant-backed infrastructure acceleration.

Emergence of AI Startups, IT Hubs, and Outsourcing Operations in Tier II Cities

Tech hubs in Cluj-Napoca, Iași, and Timișoara attract AI startups and BPOs needing scalable, secure storage. These cities host innovation parks and cross-border digital services. Demand rises for low-latency, localized storage to support multi-client workloads. SMEs prefer flexible leasing models and STaaS to manage costs. The Romania Data Center Storage Market gains momentum from this decentralized, innovation-driven demand.

Market Segmentation

By Storage Type

Traditional storage still holds a significant share, especially in public sector and legacy applications. However, all-flash storage is growing rapidly due to demand for performance, efficiency, and lower latency. Hybrid storage systems are adopted widely across enterprises balancing cost and performance. All-flash leads the Romania Data Center Storage Market in revenue growth, driven by AI workloads and real-time data processing.

By Storage Deployment

Storage Area Network (SAN) systems dominate the Romania Data Center Storage Market, particularly in enterprise and BFSI use cases. Network-attached Storage (NAS) systems are growing due to demand in SMEs and content-heavy industries. Direct-attached Storage (DAS) remains relevant in edge deployments and modular server environments. SAN leads due to its performance, scalability, and centralized management features.

By Component

Hardware components represent the bulk of investment, with increasing demand for NVMe SSDs, high-capacity drives, and controllers. Software segment grows due to adoption of SDS and analytics-driven storage orchestration. Vendors bundle both to offer integrated storage solutions. Hardware leads the Romania Data Center Storage Market, but software’s share increases with virtualization and hybrid cloud trends.

By Medium

Solid-State Drives (SSD) dominate due to superior speed, durability, and energy efficiency. HDDs continue to serve cold storage and archival needs in backup scenarios. Tape storage remains limited to compliance-driven sectors and long-term data retention. SSDs hold the leading share in the Romania Data Center Storage Market, supported by declining price per GB and cloud deployments.

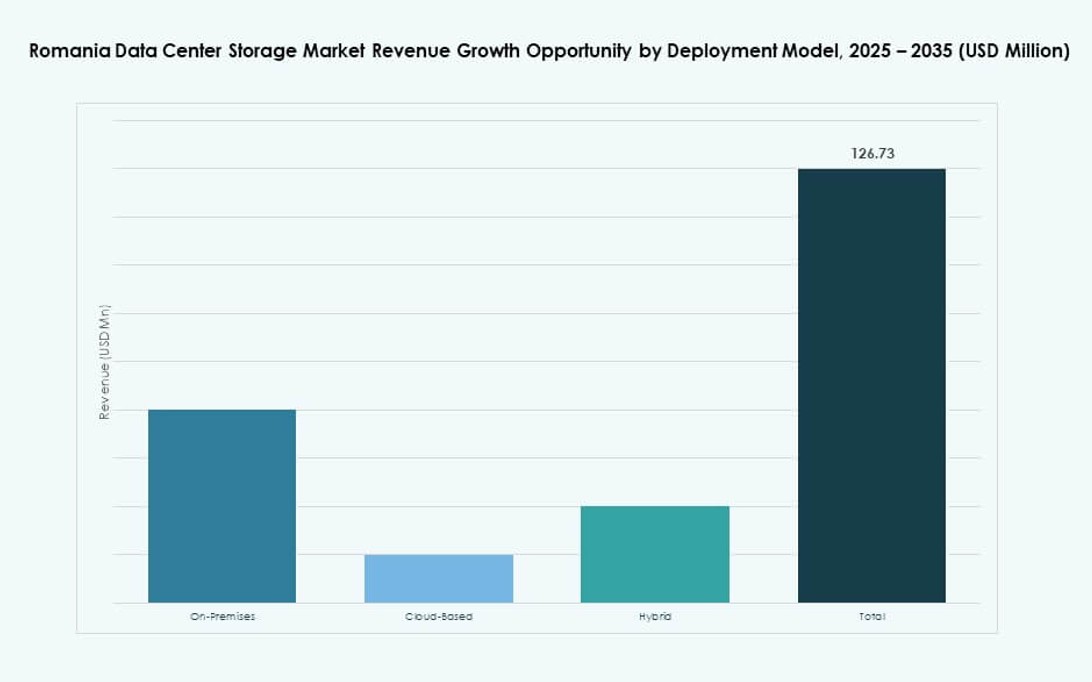

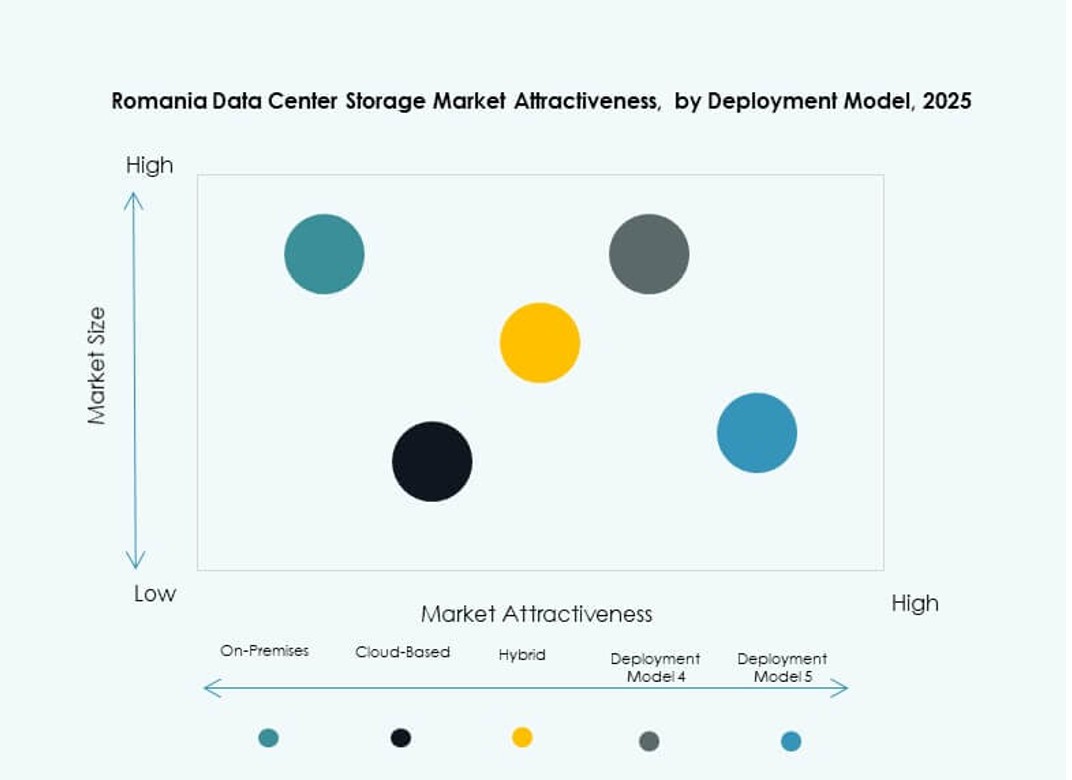

By Deployment Model

On-premises storage still accounts for a large share, especially in sectors with data sovereignty needs. Cloud-based models grow rapidly, with hyperscalers and local cloud providers expanding offerings. Hybrid models attract enterprises seeking flexibility, control, and cost-efficiency. Hybrid deployment holds the highest momentum in the Romania Data Center Storage Market due to regulatory balancing and operational agility.

By Application

IT and telecommunications lead storage consumption in Romania, supported by cloud, 5G, and content services. BFSI sector follows with strong demand for secure, compliant storage platforms. Government and healthcare segments expand due to digital transformation and EU mandates. IT & telecom lead the Romania Data Center Storage Market due to scale and continuous demand.

Regional Insights

Bucharest Metropolitan Area Leads with Over 60% Market Share Due to Infrastructure Density and Enterprise Demand

Bucharest hosts the highest concentration of Tier III/IV data centers, fiber interconnects, and hyperscale-ready campuses. The region attracts multinationals, telecom operators, and cloud providers who need reliable, low-latency storage. Carrier-neutral facilities offer dense interconnect ecosystems and multi-cloud support. Real estate availability and strong power grid access support expansion. The Romania Data Center Storage Market sees Bucharest contributing over 60% of national capacity.

- For instance, NXDATA operates Romania’s first neutral colocation data centers, NXDATA-1 and NXDATA-2. NXDATA-1 offers 4,138 square meters of space and hosts nodes for Balkan-IX and Interlan, supporting over 100 regional and international networks across its carrier-neutral ecosystem.

Cluj-Napoca, Iași, and Timișoara Emergent Hubs with 25% Combined Market Share

Cluj-Napoca and Iași lead among Tier II cities with growing demand from IT outsourcing, startups, and academia. These regions benefit from tech parks, high-skilled workforce, and cross-border digital service hubs. Timișoara is rising due to its proximity to Serbia and Hungary, enabling cross-regional data flows. Combined, these cities contribute around 25% market share to the Romania Data Center Storage Market.

Rest of Romania Accounts for 15% Share, With Demand Driven by Edge and Government Programs

Smaller cities and rural areas see moderate storage demand through smart city projects and public digitization efforts. Edge deployments support logistics, agriculture, and utility applications. Inter-city fiber rollout and regional STaaS offerings boost accessibility. Market penetration is low, but targeted initiatives and decentralization efforts are changing the landscape. The Romania Data Center Storage Market gains nationwide depth through such tier-balanced expansion.

- For instance, ClusterPower is developing a hyperscale data center campus in Mișchii, Dolj County, with planned Tier III+ certification, 200 MW capacity, and support for up to 4,500 racks across multiple phases.

Competitive Insights:

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- IBM Corporation

- Cisco Systems, Inc.

- NetApp

- Huawei Technologies Co., Ltd.

- Hitachi Vantara

- Bitdefender

- Endava Romania

- Lenovo Group

The Romania Data Center Storage Market hosts a mix of global technology giants and strong domestic IT players. Dell Technologies, HPE, and IBM dominate enterprise deployments with end-to-end infrastructure and hybrid cloud storage solutions. Cisco and NetApp strengthen their edge through high-performance network-attached and software-defined storage platforms. Huawei and Lenovo hold a presence in mid-range and hyperscale-ready environments. Romanian companies like Bitdefender and Endava contribute through cybersecurity integration and localized managed services. Vendors compete on latency, modularity, support models, and cloud-native compatibility. It evolves through partnerships, software-defined innovation, and government digitalization mandates driving long-term storage demand.

Recent Developments:

- In November 2025, Premier Energy Group acquired a construction-ready battery energy storage system (BESS) project near Iași. The facility features 200 MW charging/discharging power and 400 MWh storage capacity.