Executive summary:

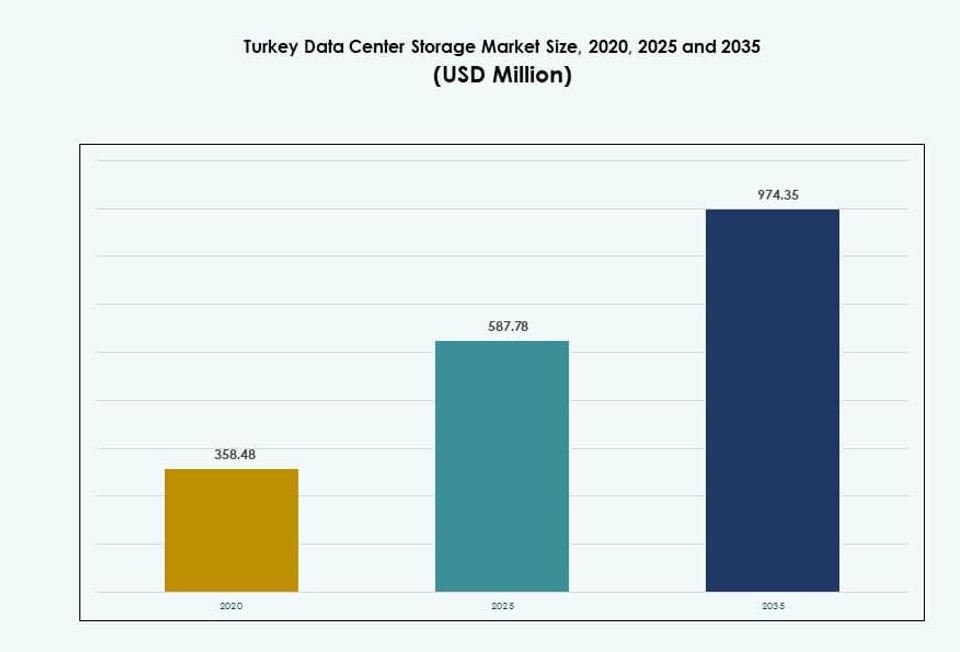

The Turkey Data Center Storage Market size was valued at USD 358.48 million in 2020 to USD 587.78 million in 2025 and is anticipated to reach USD 974.35 million by 2035, at a CAGR of 5.03% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Turkey Data Center Storage Market Size 2025 |

USD 587.78 Million |

| Turkey Data Center Storage Market, CAGR |

5.03% |

| Turkey Data Center Storage Market Size 2035 |

USD 974.35 Million |

Strong demand for AI workloads, 5G deployments, and data localization regulations are driving the market. Enterprises are adopting flash-based and software-defined storage to meet performance and compliance needs. Local data center operators are expanding infrastructure to support sovereign cloud and edge computing. Investors are targeting next-gen storage solutions to support high-growth sectors like BFSI, healthcare, and telecom. Businesses view storage as a foundation for secure, low-latency digital services. The market plays a central role in enabling Turkey’s broader digital economy goals.

Istanbul leads the market due to its dense network infrastructure, hyperscale activity, and proximity to major connectivity routes. Ankara follows with strong demand from public sector and regulatory-focused storage projects. Emerging regions like Izmir and Bursa are attracting cloud and colocation investments, driven by industrial expansion and digital transformation outside core zones. These cities are shaping the secondary growth frontier in the Turkey Data Center Storage Market.

Market Dynamics:

Market Drivers

Surge in Enterprise Digital Transformation and Demand for Agile Storage Infrastructure

Enterprises across Turkey are shifting to digital-first operations, requiring robust and agile storage systems. Cloud-native applications and big data workflows need fast, scalable storage that traditional systems cannot support. Businesses across BFSI, manufacturing, and government sectors are investing in high-availability storage infrastructure. The Turkey Data Center Storage Market benefits directly from this transition. Private and hybrid cloud adoption is increasing demand for storage that enables low-latency processing. Virtualization and AI are pushing enterprises toward tiered storage solutions. Fast backup and disaster recovery have become critical requirements. Enterprises view storage as a core enabler for business continuity. Investors see this shift as a structural driver for market growth.

- For instance, Turkcell partnered with Google Cloud in late 2025 to build Türkiye’s first hyperscale regional data center, expanding infrastructure and cloud services locally while supporting advanced workload needs including storage and analytics.

Strategic Importance of Data Localization Mandates and Regulatory Compliance

Turkey’s data localization laws are compelling enterprises to store and process data within national borders. These regulations are driving demand for domestic data center storage infrastructure. Critical sectors such as banking, healthcare, and telecom must comply with local data residency requirements. This regulatory shift expands infrastructure investments by both public and private entities. The Turkey Data Center Storage Market is gaining strategic value from its role in national digital sovereignty. Companies are modernizing storage with encrypted and role-based access controls. Regulatory frameworks are reshaping how data is archived, retrieved, and protected. Advanced storage is now a compliance necessity. Government support adds momentum to local infrastructure deployment.

Acceleration of 5G Rollout and Its Impact on Edge and Distributed Storage

The rollout of 5G networks is expanding edge computing demand in Turkey, fueling need for localized data storage. Low-latency use cases like autonomous systems, video analytics, and IoT require real-time processing. Telecom operators are scaling out distributed storage nodes near base stations. The Turkey Data Center Storage Market gains relevance by enabling these edge deployments. 5G’s impact is visible in the growing need for NVMe-based, high-throughput storage. Distributed storage helps reduce core network loads and ensures performance consistency. Equipment vendors are aligning offerings with 5G-ready storage configurations. Data gravity is shifting toward edge locations. Businesses adopting 5G need robust storage ecosystems to function efficiently.

- For instance, telecom operators including Turkcell, Vodafone Turkey, and Türk Telekom secured key 5G spectrum blocks in October 2025, preparing networks for 5G services that will drive localized data processing and storage needs in cities nationwide.

Surge in AI and Analytics Workloads Driving NVMe and All-Flash Deployments

AI-powered applications and real-time analytics are transforming how data is consumed and stored. Workloads in genomics, fraud detection, and smart surveillance require low-latency, high-bandwidth storage. Enterprises are adopting NVMe and all-flash arrays to support high IOPS and microsecond response times. The Turkey Data Center Storage Market plays a vital role in supporting these compute-heavy tasks. New workloads are incompatible with legacy storage and demand faster data retrieval. Flash-based systems offer reliability and consistent throughput for AI pipelines. Organizations prioritize performance and scalability over capacity alone. This shift supports the transition from HDD to SSD infrastructure. Storage innovation is central to the next phase of enterprise digitalization.

Market Trends

Rising Use of Object Storage for Unstructured Data Management Across Vertical Markets

Unstructured data volumes are increasing rapidly across industries like media, education, and healthcare. Object-based storage enables scalable and flexible management of this unstructured data. Organizations in Turkey are deploying object storage to support data lakes, archiving, and media workflows. The Turkey Data Center Storage Market is evolving to include high-capacity, S3-compatible platforms. Cloud-native applications are better aligned with object-based models than traditional file or block systems. The need for fast retrieval and efficient backup is fueling adoption. Object storage supports metadata indexing, making it valuable for AI-based analytics. Vendors are integrating object storage into hybrid architectures. It is becoming a critical layer in modern storage stacks.

Expansion of Tiered Storage Strategies to Optimize Performance and Cost Balance

Companies are increasingly using tiered storage systems to manage performance and budget trade-offs. High-speed SSDs handle active workloads, while low-cost HDDs manage archive data. This strategic layering helps optimize IT spending and reduce latency bottlenecks. In the Turkey Data Center Storage Market, tiered architectures are becoming standard. Enterprises prioritize fast access for mission-critical apps while allocating bulk data to slower tiers. Tiering also improves backup and restore efficiency. Vendors are bundling automation tools to manage data placement dynamically. The move helps reduce total cost of ownership. Tiered storage aligns with evolving workload diversity across sectors.

Software-Defined Storage (SDS) Adoption for Infrastructure Flexibility and Scalability

Businesses in Turkey are adopting software-defined storage to gain agility and hardware independence. SDS platforms allow organizations to manage diverse storage assets through a centralized interface. Enterprises benefit from automation, scalability, and vendor-agnostic infrastructure. The Turkey Data Center Storage Market is shifting toward software-first models that decouple storage software from physical hardware. SDS supports hybrid deployments and rapid scaling, which suits evolving enterprise needs. It also simplifies storage provisioning and monitoring. Organizations implementing SDS report improved operational efficiency. Service providers are using SDS to offer flexible storage-as-a-service. It is reshaping long-term storage architecture decisions.

Growing Adoption of Green Storage Solutions in Response to Energy and ESG Mandates

Energy efficiency is now a major consideration for storage procurement decisions. Enterprises are adopting energy-aware storage solutions to meet sustainability targets. The Turkey Data Center Storage Market is seeing demand for drives with low power consumption and advanced cooling integration. Green data centers prioritize SSDs over spinning disks due to lower heat output and energy usage. ESG policies are guiding technology refresh cycles in large enterprises. Vendors are launching storage products with carbon footprint reporting features. Environmental certifications are influencing storage investment decisions. Efficient storage contributes to reduced total power usage effectiveness (PUE). Companies view it as a step toward long-term sustainability.

Market Challenges

Dependence on Imported Storage Hardware and Fluctuations in Global Supply Chains

Turkey relies heavily on international vendors for key storage components and systems. Import dependency exposes the market to currency volatility, trade restrictions, and global supply disruptions. The Turkey Data Center Storage Market faces challenges from rising costs and unpredictable lead times. Procurement delays affect deployment timelines and scalability plans for local operators. Global chip shortages and freight issues have impacted flash and controller availability. Enterprises often struggle to source high-end systems on demand. Limited local manufacturing limits flexibility during geopolitical or economic shocks. This dependency creates risks that can delay infrastructure growth and modernization. Stakeholders are exploring diversification, but progress remains slow.

Skilled Workforce Gaps in Advanced Storage Technologies and System Integration

Despite strong infrastructure demand, Turkey faces a shortage of professionals skilled in storage system design and management. Many enterprises lack in-house expertise to deploy and maintain advanced storage like SDS, NVMe, or cloud-native platforms. The Turkey Data Center Storage Market must overcome this talent deficit to ensure sustained adoption. Complexities in hybrid and multi-cloud environments require trained architects and system integrators. Limited local training programs and certifications hinder talent availability. Businesses depend on international consultants, increasing costs and reducing long-term resilience. Workforce gaps also slow down innovation and customization. Upskilling programs and academic partnerships are urgently needed to bridge this gap.

Market Opportunities

Rising Role of Regional Cloud Providers and Edge Storage Deployments

Regional cloud service providers in Turkey are expanding rapidly and localizing storage offerings. These providers support compliance, latency, and pricing demands of local businesses. The Turkey Data Center Storage Market has a strong opportunity in enabling edge deployments through modular and scalable storage platforms. Growth in smart city and industrial IoT projects will drive localized data processing needs. Vendors offering flexible, low-latency edge storage can capture niche opportunities.

Growing Investor Interest in Hyperscale and AI-Ready Storage Infrastructure

Global and regional investors are eyeing Turkey’s growing digital infrastructure space. Hyperscale data centers, AI clusters, and sovereign cloud zones demand performance-centric storage solutions. The Turkey Data Center Storage Market can benefit from capital inflows that fund high-performance, scalable, and efficient storage ecosystems. Investments are shifting toward AI-ready flash storage, backup automation, and regulatory-compliant storage-as-a-service.

Market Segmentation

By Storage Type

Hybrid storage dominates the Turkey Data Center Storage Market, offering a balance between performance and cost. Organizations prefer a mix of HDD and SSD to handle varied workloads and archival needs. All-flash storage adoption is rising in BFSI and AI-driven sectors that demand high IOPS and low latency. Traditional storage still exists in legacy applications but is declining. The market is expected to shift steadily toward all-flash and hybrid formats for flexibility.

By Storage Deployment

Storage Area Network (SAN) systems hold a dominant position due to their use in large-scale enterprise environments. SAN delivers high-speed, block-level access for transactional workloads in financial and telecom sectors. NAS systems are growing in content-heavy sectors like media and education. DAS remains limited to smaller enterprises with single-server setups. The Turkey Data Center Storage Market is shifting toward network-based storage for scalability and remote accessibility.

By Component

Hardware remains the leading segment in the Turkey Data Center Storage Market due to demand for physical drives, enclosures, and servers. Growth in SSDs, controllers, and NVMe arrays fuels hardware investments. Software is gaining traction through SDS and virtualization layers that enhance storage management. Enterprises increasingly seek automation, analytics, and cloud integration tools. Software’s share is rising steadily due to its role in flexible and intelligent storage systems.

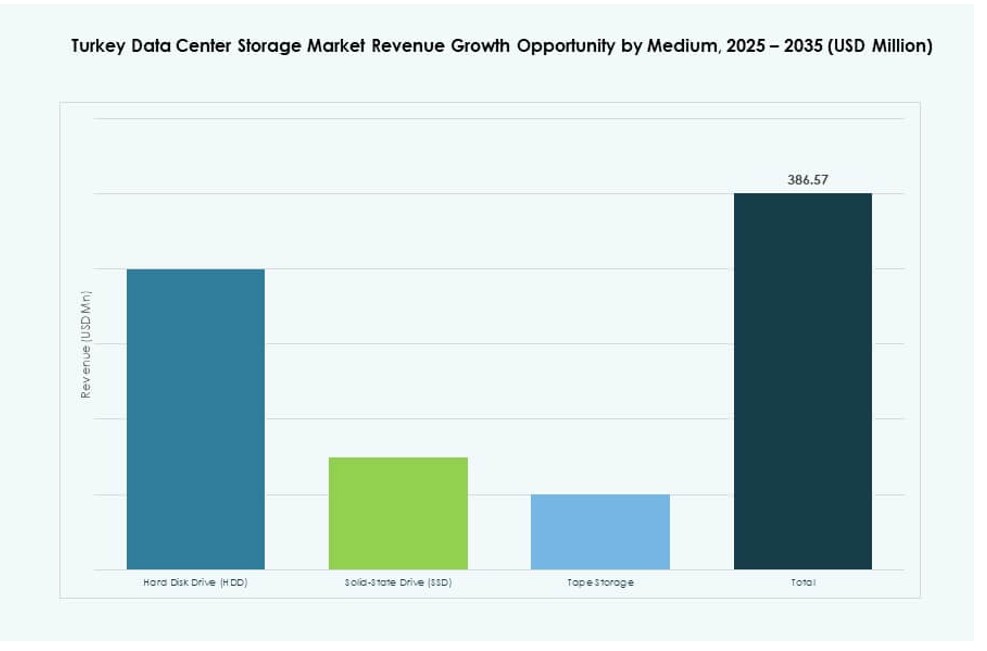

By Medium

Solid-State Drives (SSD) are the fastest-growing segment due to their speed, durability, and lower power usage. SSDs support AI, analytics, and high-performance computing, making them ideal for data center workloads. Hard Disk Drives (HDD) still hold share for bulk storage and archiving needs. Tape storage, though niche, remains relevant for compliance and cold backup scenarios. The Turkey Data Center Storage Market favors SSDs in modern deployments while retaining HDDs for cost-sensitive applications.

By Deployment Model

Cloud-based storage is gaining fast adoption among enterprises and SMEs seeking scalability and cost-efficiency. On-premises storage holds a strong base in regulated sectors like government and banking. Hybrid deployments are becoming common as companies adopt multi-cloud strategies. The Turkey Data Center Storage Market reflects this shift toward flexible and distributed deployment models. Organizations want control and agility in their storage infrastructure to match evolving business needs.

By Application

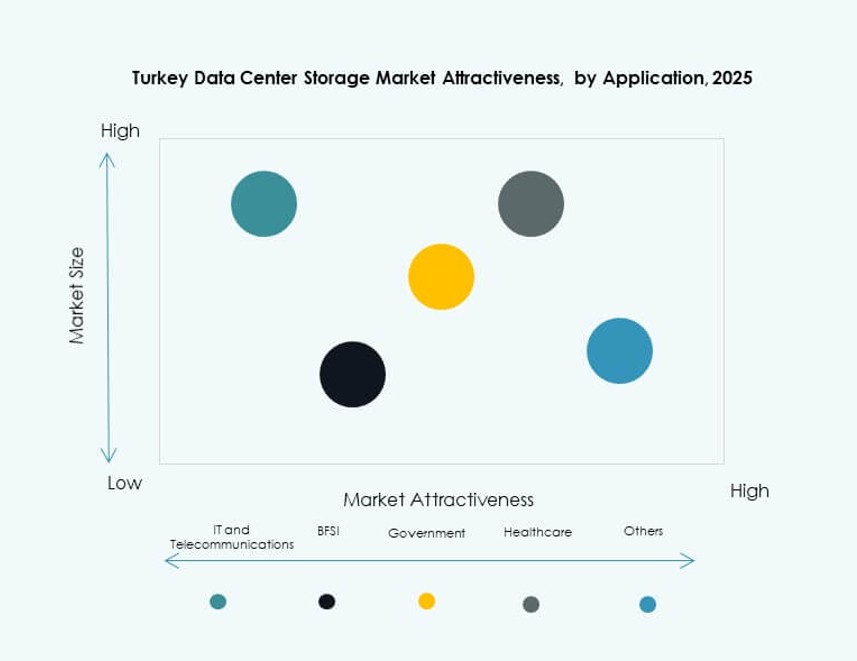

IT and telecommunications lead the market due to massive data generation, low-latency demands, and 5G rollout. BFSI is another dominant sector investing in secure, high-speed storage to support transactions and analytics. Government agencies are expanding cloud and sovereign data infrastructure. Healthcare is emerging with demand for imaging and patient record storage. The Turkey Data Center Storage Market supports varied vertical needs through sector-specific infrastructure.

Regional Insights

Istanbul Holds the Largest Market Share Due to Infrastructure Maturity and Cloud Hubs

Istanbul dominates the Turkey Data Center Storage Market, contributing over 50% of the total share. The city hosts major data centers, colocation providers, and telecom infrastructure. High enterprise density, strong fiber backbone, and proximity to submarine cable routes support growth. Cloud availability zones and digital hubs are concentrated in Istanbul. It serves as the country’s digital core and interconnection gateway. Demand for low-latency services continues to rise, attracting both local and foreign investment.

- For instance, Equinix operates multiple data centers in Istanbul, positioning the city as a key interconnection hub between Europe, Asia, and the Middle East. These facilities support carrier‑dense connectivity and enable low‑latency data exchange for enterprises and cloud service providers operating in Turkey.

Ankara Drives Public Sector Storage Expansion with 20% Market Share

Ankara holds approximately 20% share, fueled by its status as the administrative capital. The city supports storage demand from government cloud programs and regulatory bodies. Public institutions are modernizing data infrastructure for compliance and service digitization. Data localization and e-governance initiatives add momentum to infrastructure upgrades. Ankara is also home to research institutes driving secure data storage projects. It is a priority zone for sovereign cloud investments and secure backup systems.

Izmir, Bursa, and Antalya Are Emerging with a Combined 30% Share

Secondary regions including Izmir, Bursa, and Antalya jointly account for around 30% of the market. These cities are experiencing industrial growth, digital startups, and backup site expansion. Izmir is attracting technology investments due to port proximity and business parks. Bursa is developing data resilience capacity for its manufacturing base. Antalya is becoming a hub for regional enterprises seeking cost-effective hosting. The Turkey Data Center Storage Market is expanding beyond core cities as infrastructure demand decentralizes.

- For instance, Vodafone Turkey and Edgnex Data Centres by DAMAC announced a joint venture to build a Tier III‑standard data centre in Izmir with 6 megawatts of capacity, planned to start operations in the first quarter of 2025 and support regional digital infrastructure.

Competitive Insights:

- Turkcell Data Center

- Vodafone Turkey Data Center

- Radore Data Center

- Equinix Turkey

- Dell Technologies

- IBM Corporation

- Hewlett Packard Enterprise (HPE)

- Cisco Systems, Inc.

- NetApp

- Huawei Technologies Co., Ltd.

The Turkey Data Center Storage Market features a competitive mix of local data center operators and global storage technology vendors. Companies like Turkcell, Vodafone, and Radore lead domestic infrastructure expansion, focusing on compliance, low latency, and localized services. Global players such as Dell, IBM, and HPE dominate the hardware and software-defined storage segments. Vendors compete on performance, energy efficiency, and integration with hybrid and cloud-native platforms. Flash-based solutions, SDS offerings, and NVMe innovations are key areas of differentiation. M&A activity and strategic alliances are shaping the market, especially for AI-ready and regulatory-compliant solutions. Local providers continue investing in Tier III and IV facilities, while global vendors focus on advanced storage architecture, creating layered competition across deployment models.

Recent Developments:

- In November 2025, Turkcell announced a $1 billion investment commitment through 2032 to more than double its data center capacity and became an authorized reseller for Google Cloud in Turkey, enhancing national cloud and AI infrastructure.

- In May 2025, Turkcell secured €100 million in financing from Emirates NBD to expand its TDC data center unit, supporting long-term investments in Turkey’s digital infrastructure and localized storage services.

- In February 2024, Edgnex Data Centres (Damac) and Vodafone Turkey revealed plans to build a $100 million, 6MW data center in Izmir, with a scheduled launch in Q1 2025, aimed at strengthening regional cloud and computing capacity.