Executive summary:

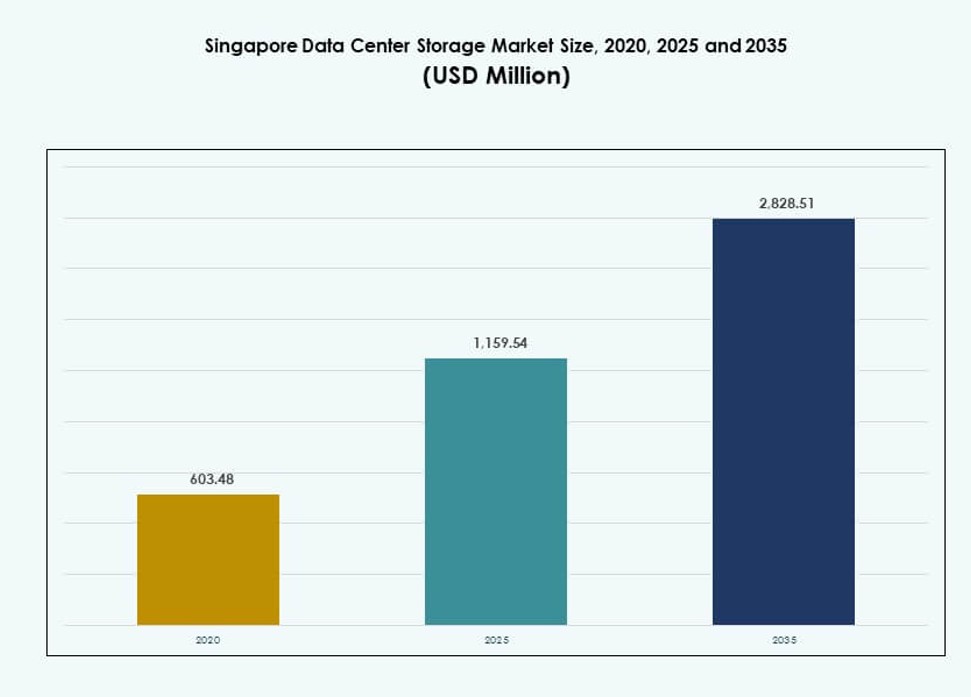

The Singapore Data Center Storage Market size was valued at USD 603.48 million in 2020 to USD 1,159.54 million in 2025 and is anticipated to reach USD 2,828.51 million by 2035, at a CAGR of 9.23% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Singapore Data Center Storage Market Size 2025 |

USD 1,159.54 Million |

| Singapore Data Center Storage Market, CAGR |

9.23% |

| Singapore Data Center Storage Market Size 2035 |

USD 2,828.51 Million |

The market is expanding rapidly due to accelerated adoption of AI workloads, hybrid cloud models, and software-defined storage systems. Government mandates and enterprise modernization initiatives are driving innovation in data infrastructure. Players invest in flash storage, NVMe architectures, and scalable platforms to support growing demand. The shift toward performance-driven storage design and regulatory compliance boosts investment in intelligent, efficient solutions. For businesses and investors, Singapore offers a digitally mature, policy-stable environment with high storage infrastructure returns.

Central Singapore leads the market, supported by hyperscale operators, colocation hubs, and financial data zones. Western Singapore is emerging with industrial and edge storage projects tied to smart logistics and IoT. Northern and eastern zones support backup and secondary deployments with smaller facilities. The country’s robust connectivity and regulatory clarity position it as Southeast Asia’s dominant storage hub. Surrounding countries rely on Singapore’s infrastructure for low-latency, compliant storage access.

Market Dynamics:

High Government Focus on Digital Economy and Cloud-First Initiatives

Singapore’s Smart Nation agenda encourages widespread digital adoption across sectors. Government mandates on cloud-first strategies increase demand for secure, compliant storage infrastructure. Public sector data workloads are migrating to sovereign cloud environments. Investments in AI, IoT, and 5G continue fueling large-scale data generation. This drives enterprises to adopt scalable and redundant storage platforms. The Singapore Data Center Storage Market supports real-time processing across public services, finance, and logistics. It also benefits from regulatory alignment with global data protection norms. These shifts make the country a testbed for advanced storage systems. Businesses and investors view Singapore as a launchpad for regional growth.

- For instance, GovTech’s Government on Commercial Cloud (GCC) platform “currently hosts over 600 government digital services,” including MyCareersFuture and MOE’s Student Learning Space, underscoring the scale of cloud-based workloads and storage managed under Singapore’s Smart Nation and cloud-first agenda.

Expansion of AI and High-Performance Workloads Driving Storage Innovation

The acceleration of AI-based applications is reshaping storage system architecture. Training models for language processing, autonomous systems, and surveillance requires high-throughput storage with low latency. Enterprises shift from traditional HDDs to flash and NVMe to meet AI demands. Data centers optimize infrastructure for GPU-based systems and parallel processing. The Singapore Data Center Storage Market adapts by integrating intelligent tiering and storage orchestration tools. This shift improves both performance and cost-efficiency. It also enables use cases such as predictive analytics and smart city deployments. Investors target hyperscale-ready storage platforms with strong uptime SLAs and green compliance features.

- For instance, NVIDIA and Singtel announced that Singtel’s AI Data Center at Tuas will be powered by NVIDIA H100 Tensor Core GPUs as part of a sovereign AI initiative, enabling high-performance AI training and inference infrastructure that supports GPU-accelerated workloads for enterprises in Singapore and the wider region.

Rising Cloud and Hybrid Storage Adoption Across Financial and Tech Verticals

Financial services, fintech startups, and health tech firms adopt hybrid and cloud storage models. These sectors require both data locality and scalability to manage compliance and transaction volumes. Providers deliver on-premises gateways paired with cloud-based object and block storage. This mix enables backup, disaster recovery, and cross-border access while maintaining latency control. The Singapore Data Center Storage Market reflects this trend by seeing increasing demand for hybrid architectures. Hardware-agnostic software platforms further help clients transition between vendors. Businesses gain flexibility while meeting MAS and PDPA data policies. The storage market becomes integral to financial resilience and innovation cycles.

Edge Computing and 5G Fueling Demand for Decentralized Storage Architecture

Smart infrastructure deployments create massive demand for real-time analytics. Edge computing environments need localized storage nodes to reduce response times. 5G rollouts extend coverage for applications such as autonomous transport and industrial automation. These require distributed storage that can handle bursts of high-volume data. The Singapore Data Center Storage Market supports this shift with micro data center integration. Operators deploy edge storage closer to IoT endpoints and smart buildings. AI-based storage management enhances fault tolerance and performance at the edge. These developments attract ecosystem partners building next-gen digital services across Southeast Asia.

Market Trends

Rise of Liquid Cooling and Densified Racks Enhancing Storage System Efficiency

Singapore’s energy constraints and land scarcity drive innovation in hardware design. Storage systems are being integrated into high-density server racks optimized with liquid cooling. This supports growing rack-level power demands without exceeding thermal limits. Cooling innovations lower operational costs and environmental impact. The Singapore Data Center Storage Market adopts liquid cooling in storage-heavy workloads. High-capacity SSDs and parallel access file systems are embedded in these dense architectures. Operators pursue data center design standards that align with sustainability goals. These setups increase rack-level utilization and reduce real estate requirements. The trend aligns with Singapore’s green data ambitions.

Integration of AI for Predictive Storage Maintenance and Workload Optimization

Operators increasingly use AI-based tools to monitor and manage storage lifecycles. These tools predict hardware failures, optimize tiering, and reduce redundancy. Storage solutions integrate telemetry systems for real-time performance diagnostics. The Singapore Data Center Storage Market sees AI-powered orchestration across object and file storage arrays. Enterprises benefit from reduced downtime and improved system efficiency. Predictive models also help optimize capacity planning. The trend supports proactive IT governance and better ROI. AI capabilities embedded in storage software enhance decision-making for CIOs and infrastructure leads.

Emergence of Sovereign Cloud and Zero Trust Models Impacting Storage Design

Singapore emphasizes data sovereignty to safeguard critical infrastructure and citizen information. Storage systems increasingly comply with zero trust security frameworks and local residency requirements. Encryption-at-rest, access segmentation, and audit logging become standard features. The Singapore Data Center Storage Market aligns with these changes through design-level policy integration. Storage vendors offer sovereign cloud solutions embedded within hyperscale frameworks. Government and regulated sectors prioritize such models for workload hosting. These shifts redefine vendor selection criteria and create demand for storage policy customization.

Shift Toward Consumption-Based and Software-Defined Storage Models

Clients demand flexibility in how they pay for storage capacity and performance. Consumption-based models offer predictable costs aligned to usage patterns. Software-defined storage platforms decouple software from proprietary hardware. The Singapore Data Center Storage Market responds by expanding offerings in software-defined and subscription-based models. Clients benefit from scalability without CAPEX-intensive commitments. Multi-cloud environments integrate easily with API-driven storage layers. This trend supports digital-native enterprises seeking cost control and operational agility. It also lowers vendor lock-in risks and enhances resilience strategies.

Market Challenges

Limited Land Availability and Energy Constraints Restrict Physical Expansion

Singapore’s small land footprint limits the ability to build new large-scale data centers. Government imposes moratoriums and green building standards to manage space and energy use. Operators must innovate within strict efficiency boundaries. The Singapore Data Center Storage Market faces constraints in adding storage-heavy infrastructure. This challenge pushes demand for higher density storage formats like all-flash and NVMe. Cooling limitations further impact how storage arrays can be deployed. It becomes harder for legacy hardware to meet current sustainability standards. Investors must weigh scalability plans against site-level capacity ceilings and power quotas.

Talent Shortage and Regulatory Complexity Slowing Advanced Storage Integration

While Singapore excels in policy clarity, it also maintains strict compliance regimes. Businesses managing financial or health data must comply with PDPA, MAS, and sectoral frameworks. These add complexity to hybrid and cross-border storage deployments. The Singapore Data Center Storage Market must ensure storage configurations meet multi-jurisdictional standards. Simultaneously, there is a shortfall in professionals trained in modern storage architecture, DevOps, and storage security. The skills gap delays innovation cycles and increases vendor dependency. High labor costs further complicate operating budgets for smaller data center players.

Market Opportunities

AI Workloads and Multicloud Environments Creating Scope for Storage Innovation

Singapore’s AI and analytics ecosystem drives demand for real-time, high-speed storage infrastructure. Cloud-native enterprises are adopting NVMe over Fabrics and intelligent caching systems. The Singapore Data Center Storage Market can leverage this shift by integrating performance-optimized storage stacks. Opportunities lie in vendor-neutral orchestration tools and low-latency data tiers. These enable data-heavy services such as fintech analytics, genomics, and smart mobility.

Sustainability-Driven Upgrades Opening Market for Next-Gen Storage Solutions

Green mandates are prompting legacy storage replacements with energy-efficient platforms. Operators seek SSD-based, low-power solutions with intelligent cooling and recycling features. The Singapore Data Center Storage Market opens opportunities for vendors offering high-density, eco-friendly storage. Certifications like BCA Green Mark create an advantage for storage suppliers supporting ESG goals.

Market Segmentation

By Storage Type

Traditional storage remains relevant for archival and backup use cases, but all-flash storage dominates in performance-critical environments. All-flash storage leads the Singapore Data Center Storage Market due to speed and power efficiency. Hybrid storage gains traction in mixed workload environments that need both capacity and performance. Emerging formats such as object-based and NVMe-tiered storage are reshaping architecture strategies. Enterprises select based on performance, latency, and energy metrics.

By Storage Deployment

Network-attached storage (NAS) systems dominate due to ease of scaling and shared access across enterprise networks. Storage area network (SAN) systems follow closely for high-performance, block-level storage needs in virtualized environments. Direct-attached storage (DAS) continues in use for smaller applications and edge locations. In the Singapore Data Center Storage Market, NAS leads in adoption by cloud-native and digital services firms. Hybrid deployment models blending NAS and SAN are also on the rise.

By Component

Hardware continues to hold a larger market share due to the foundational role of physical drives, enclosures, and racks. Software, however, grows faster due to the rise in virtualization, orchestration, and AI-based storage management tools. In the Singapore Data Center Storage Market, software adoption accelerates among cloud providers and hyperscalers. Software-defined storage drives innovation by separating control logic from physical infrastructure.

By Medium

Solid-state drives (SSD) dominate the market due to higher speed, lower latency, and energy efficiency. Hard disk drives (HDD) still hold ground in bulk archival and low-cost backup scenarios. Tape storage maintains a niche for long-term retention in compliance-sensitive applications. The Singapore Data Center Storage Market sees SSDs as the default choice for performance-oriented deployments. Their adoption is boosted by falling prices and growing NVMe integration.

By Deployment Model

Cloud-based deployment leads the market, driven by hybrid work trends, application modernization, and reduced CAPEX. On-premises models persist among sectors needing strict data control, such as BFSI and healthcare. Hybrid models are preferred for balancing security, cost, and scalability. The Singapore Data Center Storage Market sees hybrid deployment rising across SMEs and multinationals. Vendor ecosystems support seamless transitions between on-prem and public cloud.

By Application

IT and telecommunications dominate demand due to high data throughput needs and content delivery services. BFSI follows with strong demand for secure, compliant, and low-latency storage infrastructure. Government and healthcare increasingly shift to cloud storage for digital services and health data integration. In the Singapore Data Center Storage Market, IT and telecom firms drive innovation in architecture and scale. Application-specific storage configurations improve ROI across verticals.

Regional Insights

Central Singapore Leads with Over 55% Market Share Due to Digital Hub Concentration

The Downtown Core and One-North regions dominate storage demand. These areas host hyperscale facilities, cloud zones, and fintech clusters. The Singapore Data Center Storage Market centers its storage infrastructure around these hubs. High-density real estate and fiber backbone support low-latency services. Major hyperscalers and colocation players maintain presence here to meet enterprise and cross-border needs. The proximity to submarine cables enhances international traffic flow.

- For instance, Equinix’s SG1 facility in the Downtown Core is one of the most network‑dense colocation sites in the region, offering access to major Internet exchange points and being part of an ecosystem with over 225 network providers, boosting low‑latency connectivity and broad interconnection opportunities.

Western Singapore Holds 30% Share with Industrial and Edge Deployments

Jurong and Tuas regions are emerging as secondary zones for data center expansion. These areas offer more affordable land and industrial zoning support. The Singapore Data Center Storage Market gains capacity from purpose-built sites in these locations. Operators focus on edge deployments for smart manufacturing, port logistics, and industrial IoT. Government incentives support power optimization and green certification in this zone.

- For instance, Google’s Singapore data centers operate at an average temperature of 27°C with recycled water cooling systems reused multiple times, contributing to quarterly Power Usage Effectiveness (PUE) matching global fleet averages.

Northern and Eastern Singapore Capture 15% Share Through Satellite and Backup Infrastructure

Tampines and Woodlands host smaller data centers for redundancy, backups, and business continuity. These zones play a supporting role in storage replication and failover strategies. The Singapore Data Center Storage Market ensures service continuity by balancing workloads across regions. These facilities attract healthcare and SME clients seeking compliance and uptime. Future expansions in these zones focus on modular and containerized storage units.

Competitive Insights:

- ST Telemedia Global Data Centres

- Keppel Data Centres

- Princeton Digital Group

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- NetApp

- IBM Corporation

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Hitachi Vantara

The Singapore Data Center Storage Market features intense competition between domestic data center operators and global technology vendors. Local players like ST Telemedia and Keppel leverage geographic advantage, land access, and sustainability alignment. Global firms such as Dell, HPE, and IBM offer high-performance, scalable storage systems integrated with hybrid and cloud infrastructure. Many companies form alliances or joint ventures to serve BFSI, telecom, and government workloads. Demand for NVMe, SDS, and sovereign cloud solutions shapes product portfolios. It supports both hyperscale and edge deployments, pushing vendors to innovate across density, latency, and energy efficiency. The market rewards agility, regulatory readiness, and service-level guarantees.

Recent Developments:

- In April 2025, PureStorage, together with Singapore-based technology services firm NCS, implemented a major storage modernization project for a Singapore government ministry, deploying all-flash storage systems that cut the ministry’s physical data center storage footprint by about 94% while simultaneously increasing AI workload performance.

- In March 2025, Kioxia launched its LC9 Series 122.88 TB NVMe solid-state drives, designed for high-capacity, high-performance environments such as AI and data center storage workloads, a product line that is directly relevant for operators and customers.

- In February 2025, Singapore’s Infocomm Media Development Authority (IMDA) issued new advisory guidelines on cloud and data center resilience, requiring more stringent risk assessment and business continuity planning for operators, which is prompting data center storage buyers in Singapore to prioritize resilient, compliant storage architectures and solutions.