Executive summary:

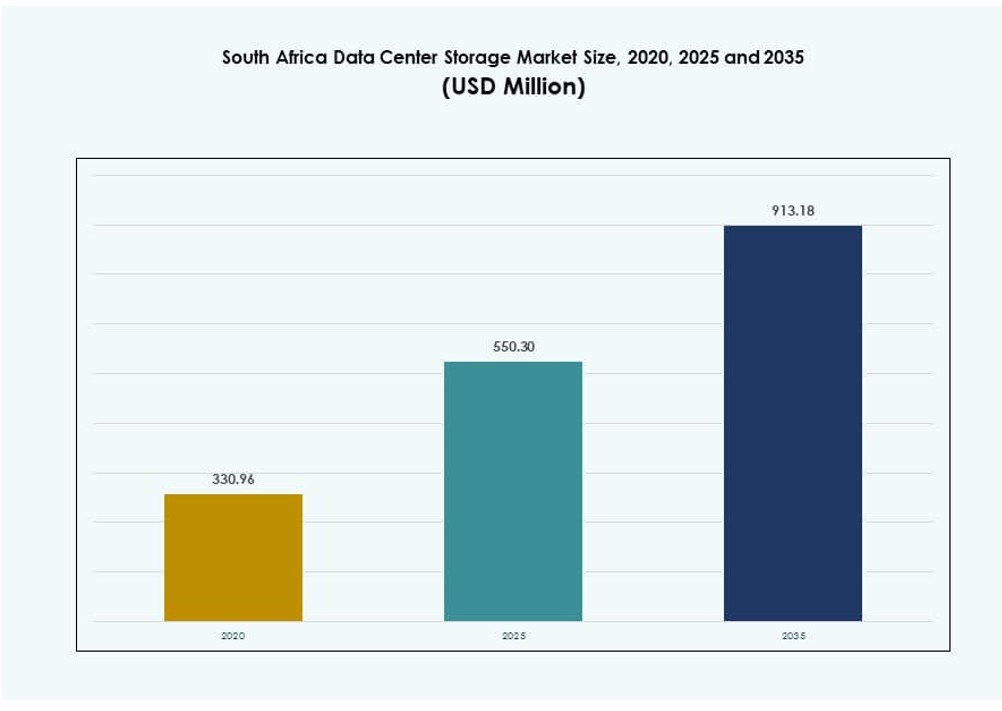

The South Africa Data Center Storage Market size was valued at USD 330.96 million in 2020 to USD 550.30 million in 2025 and is anticipated to reach USD 913.18 million by 2035, at a CAGR of 5.20% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| South Africa Data Center Storage Market Size 2025 |

USD 550.30 Million |

| South Africa Data Center Storage Market, CAGR |

5.20% |

| South Africa Data Center Storage Market Size 2035 |

USD 913.18 Million |

Growth in cloud adoption, edge computing, and AI workloads is driving demand for scalable and high-performance storage solutions. Enterprises are transitioning from legacy systems to hybrid cloud platforms, boosting the need for reliable, low-latency infrastructure. Regulatory push for data localization and rising data volumes from financial, telecom, and government sectors increase the market’s relevance. Storage innovation is critical for business continuity, digital transformation, and data-driven services, making this market strategically important for regional and global investors.

Gauteng province, led by Johannesburg and Pretoria, dominates the market due to its dense IT infrastructure and enterprise activity. Western Cape, especially Cape Town, is emerging with strong data center investments and sustainability initiatives. KwaZulu-Natal shows growing traction with regional hosting and public sector digitization. These regions vary in maturity, but together they shape the geographic spread and growth potential of South Africa’s data center storage landscape.

Market Dynamics:

Cloud Migration and Enterprise Digitalization Creating Strong Demand for Scalable Storage Solutions

South Africa is witnessing a rapid transition from legacy IT to cloud-centric models. Enterprises across finance, telecom, and government sectors are moving workloads to hybrid or private cloud setups. This shift fuels the demand for scalable, high-throughput data storage systems. Companies require both on-premises and cloud-compatible infrastructure to manage large volumes of structured and unstructured data. Many are adopting NVMe-based storage to support data-intensive workloads such as AI and analytics. The South Africa Data Center Storage Market is gaining momentum as data lifecycle management becomes mission-critical. It supports business continuity, compliance, and real-time access. For investors, this signals long-term revenue streams from infrastructure upgrades and platform services.

- For instance, in November 2025, Vodacom Group announced a multi‑year collaboration with Google Cloud to migrate critical data platforms to Google Cloud’s data cloud, including BigQuery, unifying vast data assets for real‑time insights and AI model deployment across its South African operations.

Rising Edge Computing Adoption Driving Demand for Decentralized and Low-Latency Storage Infrastructure

Edge computing is expanding across key verticals such as mining, manufacturing, and smart retail. These industries demand real-time data processing near operational zones. Localized storage solutions reduce latency and bandwidth strain, making them essential to edge environments. Portable modular data centers and micro edge nodes are integrating storage components with high IOPS. AI-based decision-making at the edge is driving growth in all-flash storage and hybrid platforms. The South Africa Data Center Storage Market benefits from this push toward decentralized IT architecture. It provides faster, safer data access for remote operations. Businesses gain from increased responsiveness, better insights, and cost-efficiency at the network edge.

- For instance, in August 2025, Vodacom invested R400 million in Free State and Northern Cape to expand 4G and 5G sites, driving a 66.2 % year‑on‑year growth in 5G adoption and supporting edge data processing with data traffic up 42 % year‑on‑year in remote operational areas.

Government Policy on Data Sovereignty Reinforcing Investment in Localized Storage Systems

Regulatory mandates requiring local data residency are reshaping IT strategies across sectors. Government institutions, banks, and telecom firms must now store sensitive data within national borders. This policy drives the demand for domestic storage infrastructure, particularly in secure colocation and sovereign cloud environments. Vendors are offering compliant systems with encryption and access controls tailored to local standards. The South Africa Data Center Storage Market is aligning with cybersecurity frameworks, ensuring trust among public and private clients. It enables secure storage for national digital IDs, health records, and public services data. This trend attracts investment from both domestic firms and global players establishing regional nodes.

AI and Big Data Workloads Requiring High-Performance, Energy-Efficient Storage Architectures

The rise of AI, IoT, and big data analytics is transforming how data centers approach storage. These workloads generate continuous data streams that must be ingested, processed, and retrieved in real time. Traditional storage often fails to meet the speed and volume demands of AI-driven applications. To address this, operators deploy high-performance flash arrays, object storage, and tiered systems. The South Africa Data Center Storage Market evolves to support GPUs, ML models, and real-time insights. It helps optimize resources, reduce TCO, and unlock new service offerings. For businesses and hyperscalers, storage upgrades enable faster innovation, better user experiences, and competitive differentiation.

Market Trends

Adoption of Software-Defined Storage for Infrastructure Agility and Cost Efficiency

Software-defined storage (SDS) is gaining ground as organizations prioritize flexibility over rigid hardware dependencies. SDS platforms allow seamless scaling, hardware abstraction, and integration with existing IT stacks. These solutions lower operational costs by supporting multi-vendor environments. Enterprises across banking, government, and telecom adopt SDS to improve automation and policy-driven management. Open-source solutions are also expanding market access. The South Africa Data Center Storage Market sees rising deployment of SDS to support hybrid cloud workflows and container-based environments. It empowers IT teams to scale storage on demand while ensuring better control and visibility. Vendors are offering pay-as-you-grow models that appeal to medium-sized businesses.

Integration of Storage with AI-Powered Data Management and Predictive Analytics Tools

AI is being embedded into storage systems to automate data classification, optimize tiering, and forecast capacity usage. Predictive analytics enables proactive maintenance and load balancing. Smart storage reduces latency, power consumption, and risk of outages. Vendors introduce systems with built-in AI engines for performance tuning and anomaly detection. The South Africa Data Center Storage Market benefits from this transition toward intelligent, self-managing storage. It enables enterprises to handle complex workloads with minimal human intervention. AI-ready storage also supports compliance reporting and data lifecycle tracking. Enterprises gain insights to improve cost control, performance, and security posture.

Surge in Demand for Cold Storage and Archival Solutions Across Regulated Sectors

Sectors such as healthcare, public administration, and legal services require long-term storage of large data volumes. Cold storage platforms offer low-cost, energy-efficient options for infrequently accessed data. Tape libraries, object storage, and cloud archival systems are in high demand. These are often used for backup, disaster recovery, and compliance mandates. The South Africa Data Center Storage Market is expanding its footprint in archival segments. It allows organizations to separate active and passive data layers, optimizing resources. Providers offer integrated data retention platforms with automated tiering. This helps businesses reduce costs and meet regulatory needs without compromising data integrity.

Expansion of Green Data Centers Supporting Sustainable Storage Investments

Sustainability is influencing investment in energy-efficient storage solutions. Operators now seek systems with low power draw, compact footprints, and minimal cooling needs. Flash storage, deduplication, and power-aware controllers play a central role. Green certifications and ESG compliance drive purchasing decisions in the public and private sectors. The South Africa Data Center Storage Market is responding to this by aligning with global efficiency standards. Providers integrate carbon reporting and energy optimization features into their platforms. This allows users to reduce environmental impact while achieving long-term cost savings. Sustainable storage also strengthens bids for public contracts and global partnerships.

Market Challenges

High Capital Expenditure and Import Dependency Limiting Infrastructure Modernization

Building modern data center storage infrastructure requires substantial investment in hardware, software, and skilled personnel. Many organizations struggle to justify the upfront costs for high-performance systems. Imports dominate the storage supply chain, leading to high costs due to currency fluctuations, shipping fees, and duties. This dependency also causes delays during global supply disruptions. The South Africa Data Center Storage Market faces slow project rollouts in regions outside Gauteng. It impacts nationwide digital infrastructure goals and weakens rural access to enterprise-class IT services. Operators must balance performance needs with budget limitations and vendor lock-in risks.

Limited Domestic Expertise and Regulatory Complexity Slowing Storage Innovation

Technical expertise in managing advanced storage systems is concentrated in a few urban centers. Shortages of certified professionals make deployment and maintenance more difficult, especially in edge locations. Training programs are limited, leading to dependence on foreign consultants or system integrators. At the same time, regulatory frameworks around data privacy, cross-border data flows, and localization are becoming more stringent. The South Africa Data Center Storage Market must align with these evolving standards without stalling innovation. This creates compliance challenges for businesses and delays product rollouts. It also raises risks for international firms seeking to invest in local infrastructure.

Market Opportunities

Growing SME Digitization and Regional Business Expansion Fuels New Demand for Mid-Tier Storage

Small and medium enterprises are digitizing operations to compete with large firms. Many require reliable, affordable storage platforms for ERP systems, remote work, and customer management. Vendors offering scalable solutions tailored to SMEs are gaining traction. The South Africa Data Center Storage Market benefits from this trend through volume-driven adoption. It opens revenue streams for modular and subscription-based offerings. Local partners can deliver managed services bundled with storage for regional businesses expanding into new markets.

Public Cloud and AI Collaboration Driving Demand for Agile, Multi-Tenant Storage Platforms

Public cloud providers are expanding footprint in South Africa through data center partnerships. These firms require agile storage with multi-tenant capabilities to support diverse customer workloads. AI-driven workloads further boost demand for real-time, scalable infrastructure. The South Africa Data Center Storage Market can leverage these collaborations to build platforms supporting analytics, security, and hybrid deployment. It creates opportunities for system integrators and OEMs to co-develop vertical-specific solutions.

Market Segmentation

By Storage Type

Traditional storage dominates in legacy enterprise setups, but all-flash storage is gaining traction rapidly. It offers superior performance for real-time applications and analytics workloads. Hybrid storage is also expanding among mid-sized businesses due to cost-performance balance. The South Africa Data Center Storage Market is seeing gradual transition toward all-flash arrays in newer deployments. Emerging categories such as object storage are also being adopted for unstructured data growth.

By Storage Deployment

Storage Area Network (SAN) systems lead due to their use in high-performance environments like BFSI and government. NAS systems follow closely, preferred for file-sharing and enterprise collaboration platforms. DAS systems are still common in remote or small-scale deployments. The South Africa Data Center Storage Market benefits from SAN expansion tied to private cloud infrastructure. Others include object storage and distributed setups catering to modern edge needs.

By Component

Hardware holds the major share, driven by demand for high-density drives, controllers, and rack systems. Software is gaining ground with virtualization, automation, and software-defined storage platforms. The South Africa Data Center Storage Market is increasingly software-centric in design philosophy. Growth in analytics and hybrid cloud boosts the role of smart software layers for orchestration, monitoring, and security.

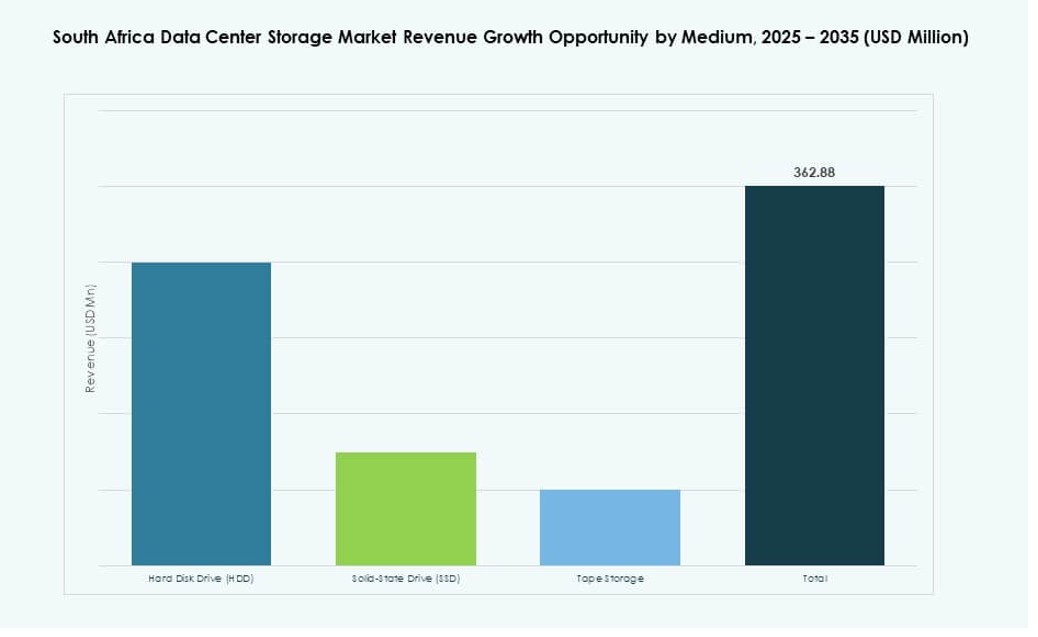

By Medium

Hard Disk Drives (HDDs) continue to be used for backup and archival needs. Solid-State Drives (SSDs) are expanding due to faster performance and falling prices. Tape storage still plays a role in cold storage and regulatory compliance in public institutions. The South Africa Data Center Storage Market sees increased SSD adoption for workloads requiring fast throughput. Power efficiency and reduced latency make SSDs a preferred choice in critical environments.

By Deployment Model

On-premises remains strong across finance and public sectors, where security and compliance matter most. Cloud-based deployment is rising fast among startups and SMEs with limited IT teams. Hybrid models are preferred in mid-to-large firms managing multiple data types and compliance needs. The South Africa Data Center Storage Market is transitioning toward hybrid frameworks with seamless data mobility. These models help balance control, cost, and scalability.

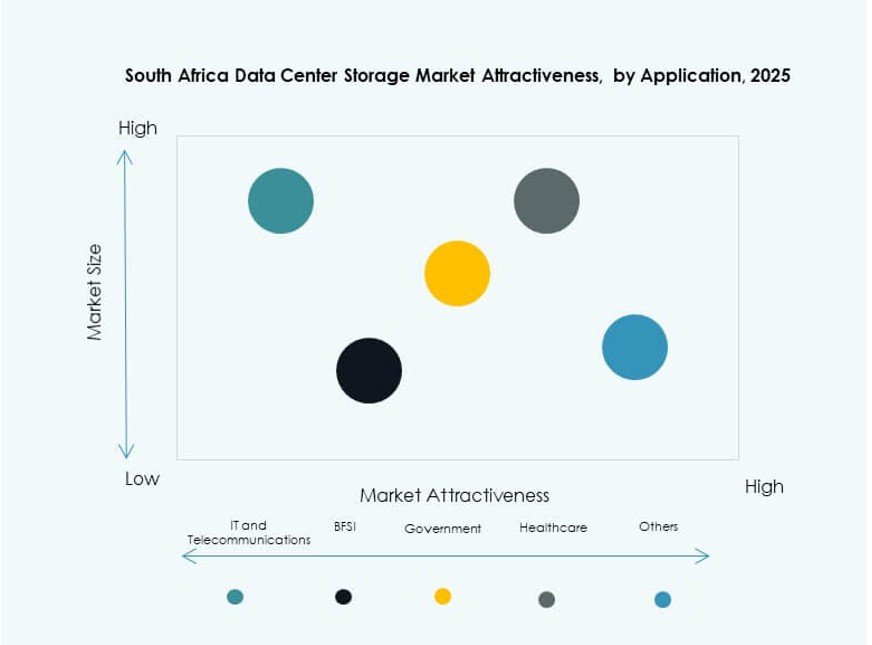

By Application

IT and Telecommunications dominate due to high storage volume and uptime needs. BFSI is another major sector, driven by real-time transactions and regulatory data archiving. Government use is expanding for smart city, e-governance, and surveillance applications. Healthcare is adopting data storage for patient records, diagnostics, and telemedicine. The South Africa Data Center Storage Market sees cross-sector demand, with customized storage stacks for each vertical’s workload profile.

Regional Insights

Gauteng Province Dominates with Over 50% Market Share Due to Dense Enterprise and Hyperscaler Presence

Gauteng leads the South Africa Data Center Storage Market with more than 50% market share. Johannesburg and Pretoria serve as the primary hubs for enterprise IT, financial institutions, and telecom providers. These cities house most of the country’s large-scale data centers and network interconnection zones. High bandwidth, stable power, and skilled labor support this concentration. Gauteng also attracts international cloud providers and colocation firms, reinforcing its dominant position. It remains the most mature market for high-density storage infrastructure and innovation.

- For instance, Teraco’s JB1 facility in Johannesburg provides 10.5 MW of power capacity with N+1 redundancy across UPS, cooling, and standby systems. High bandwidth, stable power, and skilled labor support this concentration.

Western Cape Emerging as a Secondary Hub Focused on Startups and Sustainable Infrastructure

Western Cape holds around 20% of the South Africa Data Center Storage Market share. Cape Town is evolving into a key location for digital startups, research institutions, and creative industries. Its reliable power grid and growing fiber connectivity attract new investments. The region is also leading in green data center initiatives with a focus on sustainability. It supports moderate-density storage deployments for edge computing, media workloads, and academic networks. Western Cape’s policy push toward digital economy enhances its relevance in the national storage landscape.

KwaZulu-Natal and Other Provinces Expanding Through Public Projects and Regional Hosting Services

KwaZulu-Natal accounts for roughly 15% market share and is emerging as a regional player. Durban is seeing new infrastructure projects backed by public-private partnerships. Regional data centers support provincial government, healthcare, and retail applications. The rest of the provinces, including Eastern Cape and North West, share the remaining 15%. They host low-density facilities primarily for local hosting, surveillance, and educational institutions. The South Africa Data Center Storage Market sees growth opportunities in these areas through mobile edge and rural connectivity initiatives.

- For instance, Teraco’s regional facilities maintain 47U racks at 1200 mm depth with perforated doors for 86 % airflow efficiency. The South Africa Data Center Storage Market sees growth opportunities in these areas through mobile edge deployments and rural connectivity initiatives.

Competitive Insights:

- Teraco Data Environments

- Open Access Data Centres

- BCX Data Centres

- Dell Technologies

- IBM Corporation

- Hewlett Packard Enterprise (HPE)

- Huawei Technologies Co., Ltd.

- NetApp

- Cisco Systems, Inc.

- Nutanix, Inc.

The South Africa Data Center Storage Market is shaped by a mix of global technology vendors and regional infrastructure providers. Teraco and Open Access Data Centres dominate colocation and hyperscale storage services, while BCX serves enterprise and public sector clients with managed solutions. Global OEMs like Dell, HPE, and Huawei drive innovation through flash storage, hyperconverged systems, and hybrid cloud platforms. NetApp, IBM, and Nutanix lead in software-defined storage and data orchestration capabilities. It remains competitive due to rising demand across BFSI, telecom, and healthcare. Vendors differentiate through data sovereignty compliance, energy-efficient storage designs, and edge-ready infrastructure. Partnerships and acquisitions continue to define strategic positioning.

Recent Developments:

- In January 2026, Open Access Data Centres (OADC) secured approval from South Africa’s Competition Commission to acquire a portfolio of seven NTT Data centers across key cities including Cape Town, Johannesburg, Bloemfontein, and East London.

- In November 2025, Teraco Data Environments completed the expansion of its CT2 hyperscale data center in Cape Town, bringing the facility’s total critical IT load to 50 MW. This expansion boosts local storage capacity and interconnection infrastructure, reinforcing Teraco’s role in supporting cloud, AI, and high-density storage workloads across the South African market.