Executive summary:

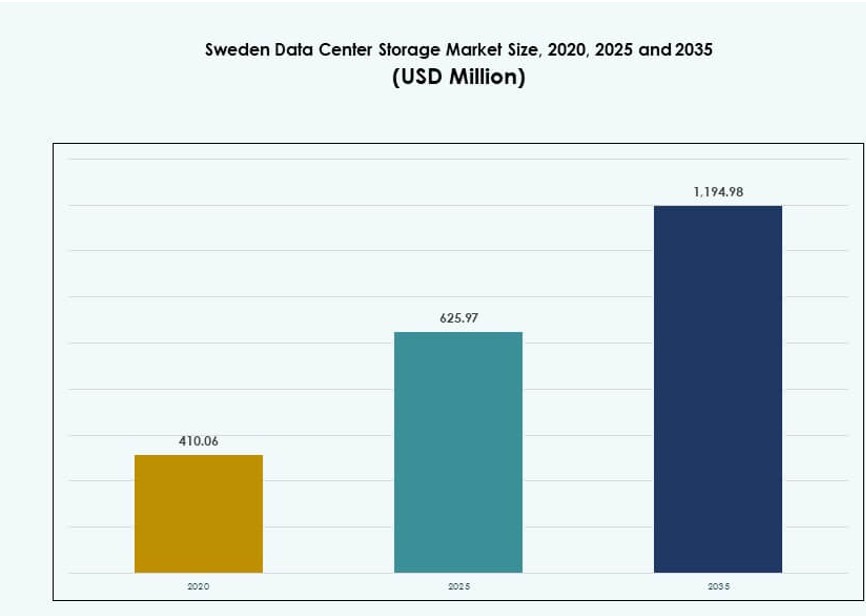

The Sweden Data Center Storage Market size was valued at USD 410.06 million in 2020 to USD 625.97 million in 2025 and is anticipated to reach USD 1,194.98 million by 2035, at a CAGR of 6.62% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Sweden Data Center Storage Market Size 2025 |

USD 625.97 Million |

| Sweden Data Center Storage Market, CAGR |

6.62% |

| Sweden Data Center Storage Market Size 2035 |

USD 1,194.98 Million |

The market is driven by rapid digitalization, strong cloud adoption, and growing AI and IoT workloads across enterprises. Organizations seek scalable, high-performance storage systems that align with evolving regulatory and security standards. The shift toward software-defined storage, flash infrastructure, and hybrid deployments reflects a need for agility and operational efficiency. Data sovereignty laws and sustainability goals further shape infrastructure investments. The Sweden Data Center Storage Market plays a vital role in enabling enterprise innovation and supporting digital transformation across sectors.

Stockholm leads the market due to its dense connectivity, hyperscale presence, and strong enterprise demand. Gothenburg and Malmö are emerging regions supported by industrial growth and data localization efforts. Northern Sweden offers potential through energy-efficient greenfield developments using abundant renewable energy. Together, these regions enable geographically distributed, high-performance infrastructure, making the Sweden Data Center Storage Market increasingly resilient and future-ready.

Market Dynamics:

Market Drivers

Enterprise Demand for Scalable Storage Amid Rapid Digital Transformation in Sweden

The Sweden Data Center Storage Market is growing due to increased digital transformation across sectors. Enterprises are shifting workloads to cloud and hybrid models, raising demand for scalable and secure storage. Data-intensive workloads such as AI, big data analytics, and IoT require high-throughput, low-latency systems. Companies seek flexible, software-defined infrastructure that adapts to business needs. Rising cloud adoption boosts interest in storage virtualization and hyperconverged systems. Regulatory compliance reinforces onshore storage growth. Sweden’s data privacy frameworks favor localized infrastructure. The market holds strategic value for firms optimizing IT. Investors find growth potential in evolving infrastructure platforms.

Technology Shifts and Storage Modernization Led by Cloud and AI Integration

Storage modernization plays a key role in infrastructure refresh cycles. AI and machine learning tools demand persistent, high-bandwidth storage to process unstructured data. Storage solutions evolve toward high IOPS systems with intelligent data management. Organizations integrate flash and tiered storage systems to optimize workloads. Sweden’s mature ICT landscape accelerates the adoption of storage platforms that support AI inference and analytics. On-premises to hybrid migration increases traction for cloud-aligned architectures. Storage vendors offer AI-ready products tailored for enterprise AI use cases. Investors monitor deployment cycles linked to AI integration. The Sweden Data Center Storage Market benefits from AI-fueled digital upgrades.

- For instance, Ericsson supplied 5G core network technology to MSB for Sweden’s Rakel G2, enabling secure data sharing with voice, images, and video across mission-critical operations starting 2024.

Shift to Sustainable Infrastructure Fueling Storage Efficiency and Innovation

Sweden’s commitment to sustainability influences storage procurement decisions. Energy-efficient storage plays a vital role in green data center initiatives. Liquid cooling, low-power SSDs, and advanced airflow designs reduce environmental footprint. Cloud providers deploy storage optimized for low-carbon operations. Regulatory incentives drive the adoption of sustainable components and power management software. Innovation centers around green IT infrastructure that balances performance with carbon goals. Storage vendors invest in designs compliant with Sweden’s energy standards. IT buyers prioritize hardware lifecycle optimization. The Sweden Data Center Storage Market aligns with long-term sustainability goals while supporting digital infrastructure expansion.

High Regulatory Standards and Data Sovereignty Shaping Infrastructure Investments

Sweden enforces strict data localization and GDPR-aligned regulations that impact storage strategies. Enterprises prioritize secure, compliant storage options that meet jurisdictional controls. Multinational firms establish regional storage hubs to meet audit and reporting standards. Regulatory-driven design shifts include increased encryption, backup systems, and immutable storage layers. Government and BFSI sectors invest in infrastructure with strong data control capabilities. This environment increases demand for hybrid cloud systems that ensure location-based governance. Storage architecture decisions align with long-term risk management strategies. Investors target vendors addressing data sovereignty needs. The Sweden Data Center Storage Market responds actively to evolving legal frameworks.

- For instance, atNorth’s Swedish facilities provide GDPR-compliant colocation with 99.99% uptime guarantees and encrypted storage for data sovereignty.

Market Trends

AI-Driven Storage Management Systems Transforming Data Infrastructure Efficiency

AI and ML tools are now embedded into storage infrastructure to optimize performance and cost. These platforms automatically tier data, monitor usage patterns, and predict capacity needs. Smart storage orchestration reduces downtime and enhances speed. Sweden’s enterprises use predictive analytics to manage storage across hybrid and multi-cloud environments. AI-based anomaly detection improves data protection. This trend supports operational efficiency and faster deployment cycles. Vendors bundle AI tools with storage management software. Energy efficiency improves with intelligent resource utilization. The Sweden Data Center Storage Market supports innovation through AI-led automation frameworks.

Increased Adoption of NVMe and Flash Storage for Latency-Sensitive Workloads

Organizations demand faster storage throughput to support AI, edge, and analytics workloads. NVMe and all-flash storage deliver low latency and high-speed access. Enterprises replace traditional HDDs with SSDs to handle real-time applications. Vendors scale NVMe offerings to support mixed enterprise workloads. Sweden’s tech ecosystem benefits from rapid flash adoption due to demand from telecom and finance sectors. NVMe-over-Fabrics further extends high-speed storage across distributed architectures. Storage optimization for critical workloads drives product differentiation. All-flash arrays become central to Tier III and Tier IV facilities. The Sweden Data Center Storage Market shifts toward performance-intensive flash solutions.

Expansion of Edge Data Storage in Industrial and Smart City Deployments

Sweden’s industrial sector and urban development projects need localized, edge-based storage. Edge data centers require compact, high-performance storage systems that operate in remote or constrained spaces. Industrial automation and sensor-based systems generate large volumes of decentralized data. Storage systems with rugged design and edge-optimized software support these environments. Telecom operators deploy micro data centers with storage near cell towers. Edge deployments use flash storage to handle latency-sensitive tasks. Vendors integrate data synchronization tools for centralized analytics. This decentralization trend diversifies storage demand. The Sweden Data Center Storage Market grows with edge computing expansion.

Growing Investment in Cyber-Resilient and Immutable Storage for Ransomware Protection

Cybersecurity concerns fuel demand for tamper-proof, resilient storage. Enterprises in Sweden implement immutable backups and air-gapped storage solutions. Ransomware threats push organizations toward zero-trust storage architectures. Immutable file systems preserve critical datasets against alteration or deletion. Cyber-resilient storage includes AI-based monitoring, automatic failover, and quick restore functions. BFSI and public sector users demand audit-compliant storage infrastructure. Vendors build hardened systems with integrated threat detection. Cyber insurance mandates influence storage design parameters. The Sweden Data Center Storage Market evolves with heightened focus on secure-by-design storage platforms.

Market Challenges

Energy Consumption Pressures Amid Storage Growth and Sustainability Demands

Energy use remains a concern with expanding data storage capacity. High-density storage racks demand significant power and cooling. Despite Sweden’s clean energy mix, power costs and grid capacity constraints present planning hurdles. Storage deployments must balance performance with efficiency. SSDs offer lower power draw but higher acquisition costs. Regulatory expectations for green infrastructure intensify pressure on data center operators. Cooling innovation helps but adds capital cost burdens. Investors expect sustainable returns tied to long-term energy savings. The Sweden Data Center Storage Market must reconcile demand growth with sustainability targets.

Rising Complexity in Storage Management Across Hybrid and Multicloud Environments

The shift toward hybrid and multicloud storage creates integration complexity. Enterprises need unified visibility, control, and compliance across multiple systems. Managing data mobility, latency, and security becomes harder without standardization. Interoperability issues slow adoption of new storage platforms. Skilled professionals with hybrid storage experience remain limited. Misaligned policies increase risk of data loss or regulatory non-compliance. Storage vendors must support API-based integration and multi-platform tools. Complex deployment cycles delay time-to-value. The Sweden Data Center Storage Market faces operational friction in scaling hybrid cloud storage solutions.

Market Opportunities

Growth in AI, Life Sciences, and IoT Driving Demand for High-Performance Storage

Sweden’s innovation economy drives demand for specialized data storage. AI labs, biotech firms, and IoT deployments require systems supporting massive, fast-moving datasets. Verticalized solutions built for scientific workloads create strong storage opportunities. Flash-based arrays, object storage, and software-defined platforms suit high-throughput use cases. Edge data gathering from IoT expands localized storage needs. Vendors can tailor offerings by vertical. The Sweden Data Center Storage Market benefits from sector-specific digital acceleration.

Expansion of Hyperscale and Greenfield Data Centers Across Sweden’s Key Zones

New builds and hyperscale expansions fuel demand for large-scale storage. Stockholm remains central, but other regions attract colocation and cloud storage investment. Sweden’s renewable power capacity makes it attractive for sustainable infrastructure. Investors target greenfield facilities with scalable storage zones. Opportunities emerge for hardware, software, and hybrid deployments. The Sweden Data Center Storage Market gains momentum from infrastructure investment cycles.

Market Segmentation

By Storage Type

Traditional storage continues to serve legacy applications, but hybrid and all-flash storage lead growth. All-flash systems dominate Tier III and hyperscale facilities due to performance advantages. Hybrid storage balances cost and speed, gaining traction in mid-size enterprises. The Sweden Data Center Storage Market sees increasing preference for flash-enabled and adaptive storage configurations across regulated sectors.

By Storage Deployment

Storage Area Network (SAN) systems lead, supporting large-scale virtualization and high-availability workloads. Network-attached Storage (NAS) suits file-heavy applications and SMEs. Direct-attached Storage (DAS) is declining but remains in smaller setups. Hybrid deployments integrate SAN/NAS in cloud-aligned use cases. The Sweden Data Center Storage Market is driven by SAN-based architectures for mission-critical operations.

By Component

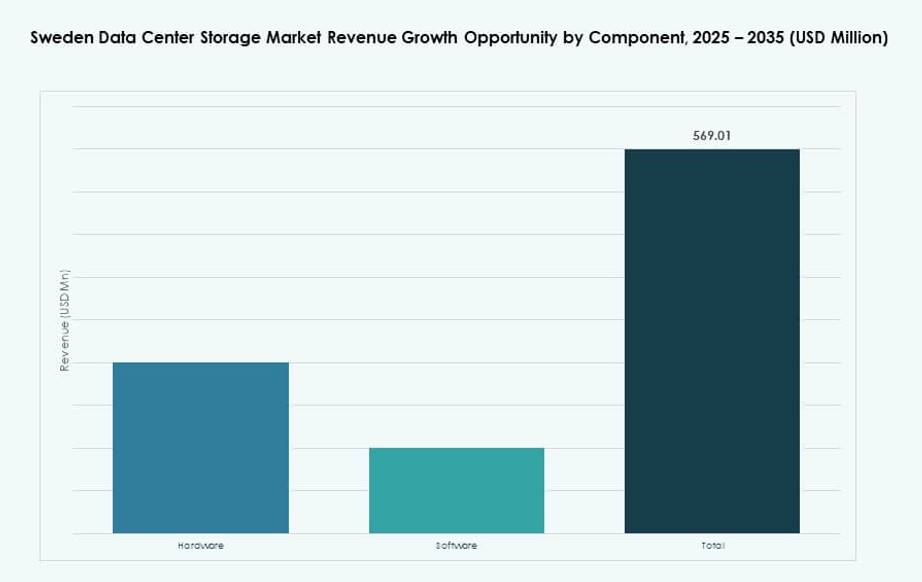

Hardware dominates in revenue due to large infrastructure deployments and recurring upgrades. Software solutions are rising with demand for virtualized storage control, orchestration, and analytics. Vendors bundle software in software-defined storage products. Growth is faster in software, but hardware still contributes majority share. The Sweden Data Center Storage Market sees hardware-led investments supported by advanced software platforms.

By Medium

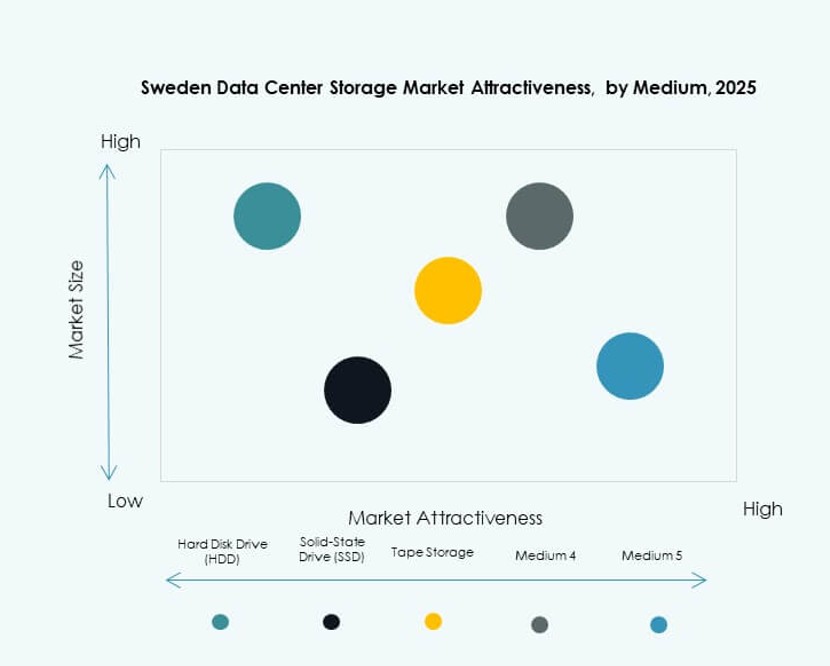

Solid-State Drives (SSD) hold major share due to performance, energy efficiency, and falling prices. HDDs continue to serve cold storage and backup workloads. Tape storage has niche use in archival systems within public institutions. SSD adoption is accelerating across enterprise and hyperscale deployments. The Sweden Data Center Storage Market reflects a shift toward flash-first infrastructure.

By Deployment Model

Cloud-based storage sees strong growth driven by SaaS, PaaS, and hybrid cloud models. On-premises storage remains critical for sectors with data sovereignty concerns. Hybrid deployment models are gaining favor for combining scalability and control. Enterprise IT strategies increasingly align with hybrid-first approaches. The Sweden Data Center Storage Market supports flexible deployments matching compliance and agility needs.

By Application

IT and telecommunications dominate storage use, supporting digital services, 5G, and software platforms. BFSI follows, driven by high compliance and data integrity needs. Government and healthcare sectors contribute due to secure storage mandates. Others include retail, media, and energy sectors. The Sweden Data Center Storage Market finds diverse application growth aligned with digital transformation in key sectors.

Regional Insights

Stockholm Metropolitan Area Leading with Over 50% Market Share

Stockholm holds more than 50% of the Sweden Data Center Storage Market due to strong connectivity, power availability, and demand density. The region hosts several hyperscale and colocation facilities, supporting enterprise, government, and financial clients. Availability of renewable power and skilled workforce make it attractive for global providers. Many cloud service providers use Stockholm as a regional hub. Storage systems deployed here support AI, SaaS, and IoT infrastructure. The region will remain a strategic storage location in coming years.

Southern and Western Sweden Emerging with New Infrastructure Projects

Regions like Gothenburg and Malmö are gaining storage market share, contributing nearly 25% collectively. These cities benefit from proximity to industrial clusters, port infrastructure, and local enterprise demand. Investment in digital infrastructure and cloud services accelerates deployment of new data centers. Storage expansion includes hybrid and edge-ready systems. Enterprises in manufacturing and logistics drive storage needs. These areas are targeted for regional expansion strategies by cloud and colocation providers.

- For instance, in June 2024, Microsoft announced a 33.7 billion SEK investment to expand its data centers in Sandviken, Gävle, and Staffanstorp, deploying over 20,000 GPUs to boost AI and cloud capabilities. Azure’s Zone Redundant Storage offers up to 99.9999999999% durability, supporting Sweden’s enterprise-grade storage needs.

Northern and Central Sweden Offering Growth Potential through Renewable Power and Edge Needs

Northern and central parts of Sweden hold about 25% of the market share. These regions are emerging with projects using excess hydropower capacity. Lower energy costs attract greenfield hyperscale deployments. Edge data centers are deployed to support remote mining, energy, and telecom operations. Cold climate and sustainable power sources reduce operational costs. The Sweden Data Center Storage Market finds growth in rural zones driven by infrastructure balance and sustainability goals.

- For instance, Meta’s Luleå data center has operated on 100% renewable hydropower since 2013, expanding beyond 100 MW IT capacity by 2024. As Meta’s first hyperscale facility outside the U.S., it supports efficient large-scale storage with a PUE of 1.07, setting global sustainability benchmarks in Sweden.

Competitive Insights:

- Ericsson

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- NetApp

- IBM Corporation

- Cisco Systems, Inc.

- Seagate Technology

- Veeam Software

- Hitachi Vantara

- Fujitsu Limited

The Sweden Data Center Storage Market is led by global technology vendors and regional specialists offering high-performance storage solutions. Ericsson and HPE support enterprise and telecom workloads with hybrid storage systems. IBM and Dell focus on modular, AI-ready storage platforms for hyperscale and colocation deployments. NetApp and Seagate drive demand in cloud and flash storage with scalable configurations. Cisco integrates networking with storage for unified infrastructure delivery. Veeam and Fujitsu enhance market presence through data protection and software-defined storage offerings. It remains competitive as firms innovate in flash, NVMe, and hybrid storage technologies to meet rising demand from government, BFSI, and healthcare sectors. Product customization, sustainability alignment, and Sweden-based deployments shape long-term positioning strategies.

Recent Developments:

- In May 2025, Ericsson joined a consortium with AstraZeneca, SAAB, SEB, and Wallenberg Investments AB to establish a Swedish AI Factory, offering secure sovereign compute infrastructure. The initiative supports advanced data and storage needs critical for AI models and high-performance workloads in Sweden’s data center storage environments.

- In March 2025, Google Cloud launched its 42nd cloud region in Sweden, partnering with firms like IKEA and Spotify. The region provides local infrastructure for data-intensive workloads, boosting demand for secure, high-performance storage within the Sweden Data Center Storage Market.