Executive summary:

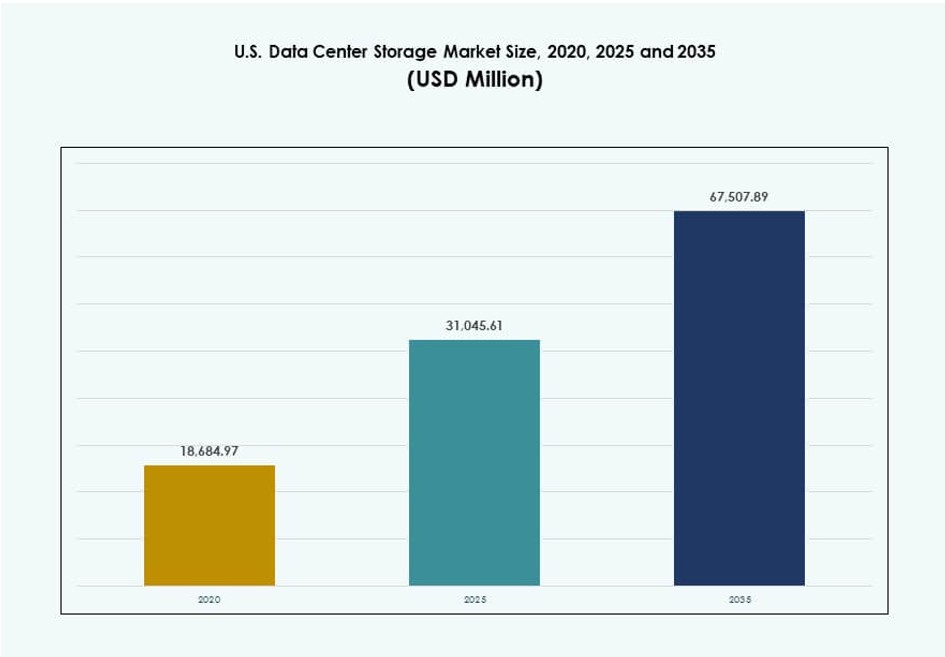

The U.S. Data Center Storage Market size was valued at USD 18,684.97 million in 2020 to USD 31,045.61 million in 2025 and is anticipated to reach USD 67,507.89 million by 2035, at a CAGR of 8.01% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| U.S. Data Center Storage Market Size 2025 |

USD 31,045.61 Million |

| U.S. Data Center Storage Market, CAGR |

8.01% |

| U.S. Data Center Storage Market Size 2035 |

USD 67,507.89 Million |

Rapid growth in cloud-native platforms, artificial intelligence workloads, and real-time data processing is driving demand for scalable storage solutions. Enterprises are shifting from legacy hardware to software-defined storage and flash-based systems for agility and performance. Major hyperscalers and colocation providers continue to invest in modernizing their storage architecture. This shift enables faster data access, secure backup, and greater operational efficiency. Businesses and investors view this market as a foundation for long-term infrastructure resilience and competitive advantage. It is closely tied to evolving enterprise demands, regulatory standards, and service-level expectations.

Northern Virginia remains the dominant region due to hyperscale concentration, government proximity, and strong network infrastructure. California and Texas follow, supported by cloud-native ecosystems and energy-efficient deployments. These regions lead in terms of capacity, storage modernization, and AI-readiness. States like Arizona, Ohio, and Oregon are emerging due to lower land and energy costs, favorable climate, and tax benefits. These markets attract new entrants looking to scale quickly while managing operational overheads. Growth in these zones reflects demand for distributed, edge-ready storage infrastructure. The geographic spread of investments supports the decentralization of storage capacity in the U.S. Data Center Storage Market.

Market Dynamics:

Market Drivers

Expansion of Cloud Infrastructure and High-Density Workloads Across Enterprise IT Ecosystems

The rapid expansion of cloud platforms, AI, and data-heavy applications is pushing enterprises to upgrade storage capacities. Demand for scalable and cost-efficient storage infrastructure drives the adoption of advanced storage solutions across hybrid and multi-cloud environments. Hyperscalers and tech giants prioritize modular and software-defined storage to manage expanding digital workloads. The U.S. Data Center Storage Market is benefiting from strong enterprise migration to cloud-native services and real-time computing. Organizations require robust infrastructure to support big data, analytics, IoT, and streaming media platforms. High-density workloads in financial services, government, and healthcare fuel demand for low-latency and high-throughput storage systems. Rapid virtualization and edge computing adoption increase storage demand across distributed networks. Data center modernization initiatives reinforce strategic investment across storage tiers and platforms.

Shift Toward Flash-Based Storage and Intelligent Tiering for Data Performance Optimization

The increasing preference for all-flash arrays and NVMe-based architecture improves performance and lowers latency for data-intensive workloads. Organizations prioritize agility and responsiveness, driving demand for flash storage in primary and secondary storage environments. Automated tiering solutions help manage active and cold data efficiently, reducing storage costs while improving speed. AI and ML-based management systems optimize workload placement and streamline data lifecycle control. The U.S. Data Center Storage Market is seeing robust activity from companies seeking to modernize their storage stack for high-availability needs. Investment in intelligent caching, deduplication, and compression enhances cost-performance ratios. These advancements make flash storage accessible beyond high-end applications. Enterprises adopt flash for mission-critical tasks while leveraging hybrid models for backup and archival.

- For instance, Microsoft expanded Azure Premium SSD v2 adoption across high‑performance workloads, while Mbv3 VM series support up to 650,000 disk IOPS to handle database peak traffic. These capabilities significantly improve storage throughput and latency for large‑scale enterprise deployments within the U.S. Data Center Storage Market.

Rising Role of Software-Defined Storage in Hybrid and Multi-Cloud Deployments

Software-defined storage (SDS) enables enterprises to decouple hardware from storage management, offering improved flexibility, scalability, and cost control. It allows organizations to use commodity hardware while achieving enterprise-grade performance. The U.S. Data Center Storage Market is increasingly influenced by SDS frameworks that simplify storage operations across cloud and on-premise environments. Policy-based automation and real-time analytics enable efficient resource allocation. This shift also reduces vendor lock-in and allows storage customization as per workload needs. The market sees strong growth from cloud service providers and large enterprises adopting SDS for data mobility. SDS enables centralized control over distributed data resources while ensuring data integrity and compliance. Growth in containerization and DevOps accelerates SDS adoption across edge and core infrastructure.

- For instance, Azure NetApp Files released large volumes in 2025 scaling to 2 PiB with over 700,000 IOPS and 12.5 GiBps throughput for mission-critical workloads like EDA and HPC.

Data Sovereignty, Security, And Compliance Pressures Driving Private and Hybrid Storage Demand

Stricter data protection laws and privacy regulations such as HIPAA, CCPA, and sector-specific mandates are shaping storage decisions. Enterprises prefer storage solutions that provide control over data locality, retention, and access. The U.S. Data Center Storage Market gains momentum from organizations integrating secure, encrypted, and access-controlled storage systems. Hybrid and private cloud storage allow enterprises to balance regulatory compliance with performance and scalability. Encrypted backups, WORM (write-once-read-many) storage, and secure replication play a key role in industries handling sensitive data. Businesses invest in security-enhanced storage appliances and audit-ready software to meet governance goals. Demand rises for compliance-aware storage workflows in healthcare, BFSI, and defense sectors. Long-term archival solutions must now integrate security by design across infrastructure.

Market Trends

Edge-Centric Storage Infrastructure Gaining Relevance for Decentralized Data Workflows

With edge computing adoption growing, organizations deploy storage closer to data sources to reduce latency. Edge data centers process large volumes of time-sensitive data, requiring fast, compact, and reliable storage systems. The U.S. Data Center Storage Market is witnessing rising investments in edge-optimized flash storage and hyperconverged systems. Compact designs with local caching, auto-tiering, and simplified deployment models are gaining traction. Industrial IoT, smart cities, and retail analytics are key edge use cases. Storage devices with low power consumption and ruggedized designs fit edge environments. Integration of lightweight software-defined storage platforms supports flexible management. Enterprises aim to reduce bandwidth usage and network dependence with localized data processing.

AI-Driven Predictive Storage Management Transforming Operational Efficiency and Cost Control

AI and machine learning algorithms are reshaping data center operations by enabling predictive storage management. These technologies detect performance anomalies, forecast capacity needs, and recommend optimization strategies in real-time. The U.S. Data Center Storage Market is shifting toward intelligent storage solutions that reduce manual interventions. Vendors offer AI-powered platforms that track data movement, usage patterns, and workload behavior. Predictive analytics help minimize unplanned outages and reduce over-provisioning costs. Such systems support dynamic scaling to adapt to evolving data volumes. Businesses gain from lower operational expenses, better asset utilization, and improved SLA adherence. Predictive intelligence also plays a growing role in cybersecurity and risk mitigation.

Energy-Efficient Storage Hardware and Cooling Design Becoming Priority in Sustainable Data Centers

Rising focus on environmental sustainability compels data centers to adopt energy-efficient storage systems. New-generation drives consume less power per IOPS and require minimal active cooling. The U.S. Data Center Storage Market is aligning with energy efficiency standards and green building certifications. Storage vendors develop eco-friendly enclosures, intelligent cooling layouts, and power-throttling algorithms. Cold storage solutions with low energy consumption attract interest for archival applications. Infrastructure designs now incorporate airflow optimization and liquid-cooled enclosures for dense flash setups. Operators monitor energy consumption at storage node level using real-time metrics. Demand grows for low-carbon footprint storage systems backed by renewable energy.

Storage Virtualization and Unified Storage Platforms Gaining Momentum Across IT Ecosystems

Virtualized storage abstracts physical devices into software-defined pools that can be centrally managed and provisioned. This flexibility enables better resource sharing and utilization. The U.S. Data Center Storage Market benefits from rising enterprise preference for unified storage combining file, block, and object protocols. Unified platforms simplify operations, reduce complexity, and improve scalability. Enterprises consolidate workloads across different environments using centralized dashboards. Storage virtualization also enhances disaster recovery and failover capabilities. It supports flexible allocation across public cloud, private cloud, and on-premises assets. Enterprises seeking agile storage models increasingly adopt virtualized environments. Centralized management also enables easier automation and compliance control.

Market Challenges

Scalability Issues and Legacy System Constraints Limiting Enterprise Agility and Storage Efficiency

Many enterprises face performance bottlenecks and storage inefficiencies due to legacy architecture. Traditional systems lack compatibility with modern virtualization tools and cloud-native applications. Upgrading legacy infrastructure requires significant investment and operational downtime. The U.S. Data Center Storage Market encounters resistance from businesses hesitant to disrupt critical services. Storage expansion across hybrid deployments becomes complex without standardized protocols. Integration with AI, real-time analytics, and edge workflows remains limited for older systems. Inefficient data tiering leads to cost overruns and underutilized resources. Maintaining legacy platforms increases OPEX, limiting IT budgets for modernization.

High Capital Investment and Skills Gap In Managing Evolving Storage Ecosystems

Building scalable and resilient storage infrastructure involves significant capital investment in both hardware and software. Enterprises need trained personnel to deploy, manage, and secure storage ecosystems across cloud, edge, and on-premises environments. The U.S. Data Center Storage Market faces skilled workforce shortages in SDS, cybersecurity, and automation. Complex deployment models require continuous staff training and certifications. SMEs struggle with limited resources to match evolving standards. Vendor-specific platforms create steep learning curves and integration risks. Maintenance costs rise with new technology adoption cycles, further increasing TCO. Cost-to-performance balancing remains a top barrier for many IT leaders.

Market Opportunities

Rising Cloud-Native Application Development Unlocks Demand For Scalable Storage Solutions

Cloud-native app deployment is growing across sectors such as healthcare, BFSI, retail, and media. These applications need low-latency, high-availability storage capable of scaling dynamically. The U.S. Data Center Storage Market offers growth opportunities for vendors delivering container-integrated and Kubernetes-friendly storage solutions. Object-based storage for unstructured data and backup use cases also sees rising demand. Cloud-native data protection and snapshot tools are gaining interest from DevOps teams.

5G Rollout And Edge AI Expanding The Scope Of Storage Infrastructure In Distributed Networks

5G deployment across U.S. metros is accelerating adoption of edge AI, video analytics, and connected devices. These use cases require storage systems that can handle real-time data generation across edge locations. The U.S. Data Center Storage Market benefits from rising demand for distributed storage platforms with local compute integration. Compact, energy-efficient storage for mobile base stations, retail nodes, and smart factories offers long-term growth.

Market Segmentation

By Storage Type

Traditional storage holds a significant base but is steadily losing share to all-flash and hybrid systems. All-flash storage dominates high-performance workloads due to low latency and fast IOPS delivery. Hybrid storage gains traction for combining speed and cost-efficiency. The U.S. Data Center Storage Market reflects growing replacement of legacy systems with intelligent flash-based solutions. Niche segments such as object storage and disaggregated storage are also expanding.

By Storage Deployment

SAN systems lead in enterprise environments needing high availability and robust data throughput. NAS systems dominate content-heavy applications like video and file sharing due to easier scalability. DAS systems remain common in edge and departmental setups. The U.S. Data Center Storage Market also includes emerging models like storage over IP and cloud-integrated SAN. Custom configurations for industry-specific deployments increase demand diversity.

By Component

Hardware contributes the largest revenue share due to server-attached storage drives, enclosures, and networking components. However, software is growing fast with SDS, virtualization, backup automation, and performance monitoring. The U.S. Data Center Storage Market favors modular, license-based storage platforms enabling better asset use. Vendors offering integrated software-hardware solutions gain preference in large enterprise contracts.

By Medium

HDD continues to dominate archival and backup storage, driven by cost per TB. SSD adoption is surging in primary storage workloads due to performance gains. Tape storage remains relevant for compliance-driven industries and cold storage. The U.S. Data Center Storage Market sees mixed-use environments combining SSD for performance and HDD for bulk retention. Cloud-native SSD solutions gain interest in fast-access use cases.

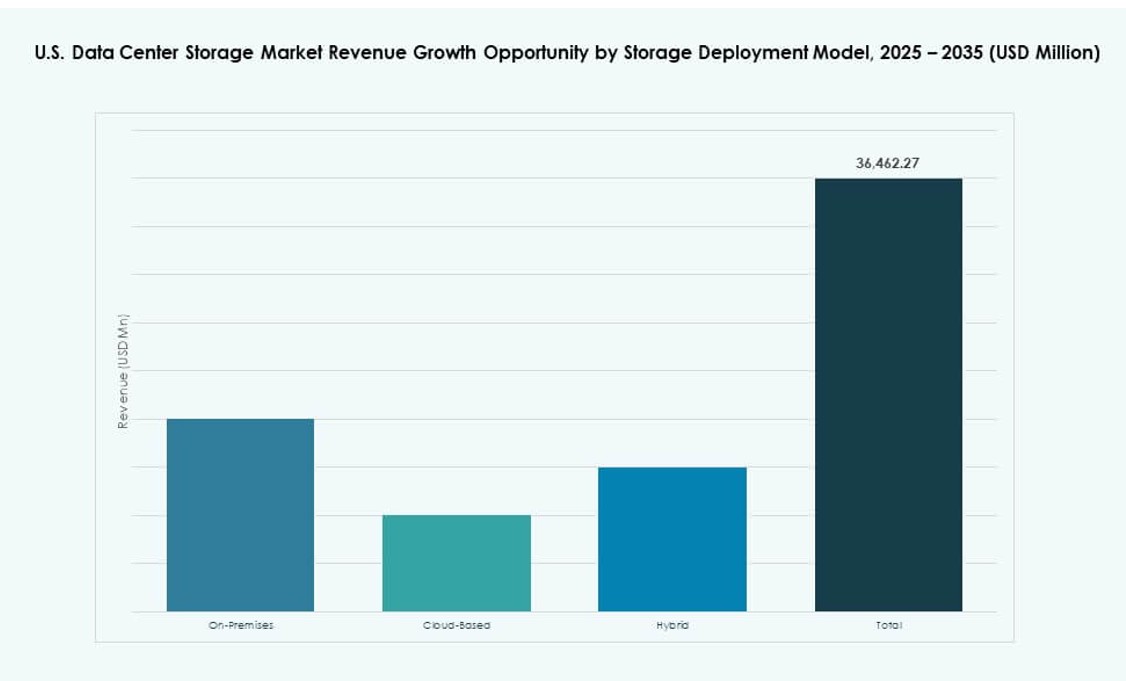

By Deployment Model

Cloud-based storage models are growing rapidly due to scalability, cost predictability, and minimal management overhead. On-premises deployments remain relevant in industries with data control requirements. Hybrid models dominate the landscape, enabling flexibility and workload optimization. The U.S. Data Center Storage Market supports both public cloud-native services and private cloud extensions. Data gravity concerns and regulatory policies shape deployment preferences.

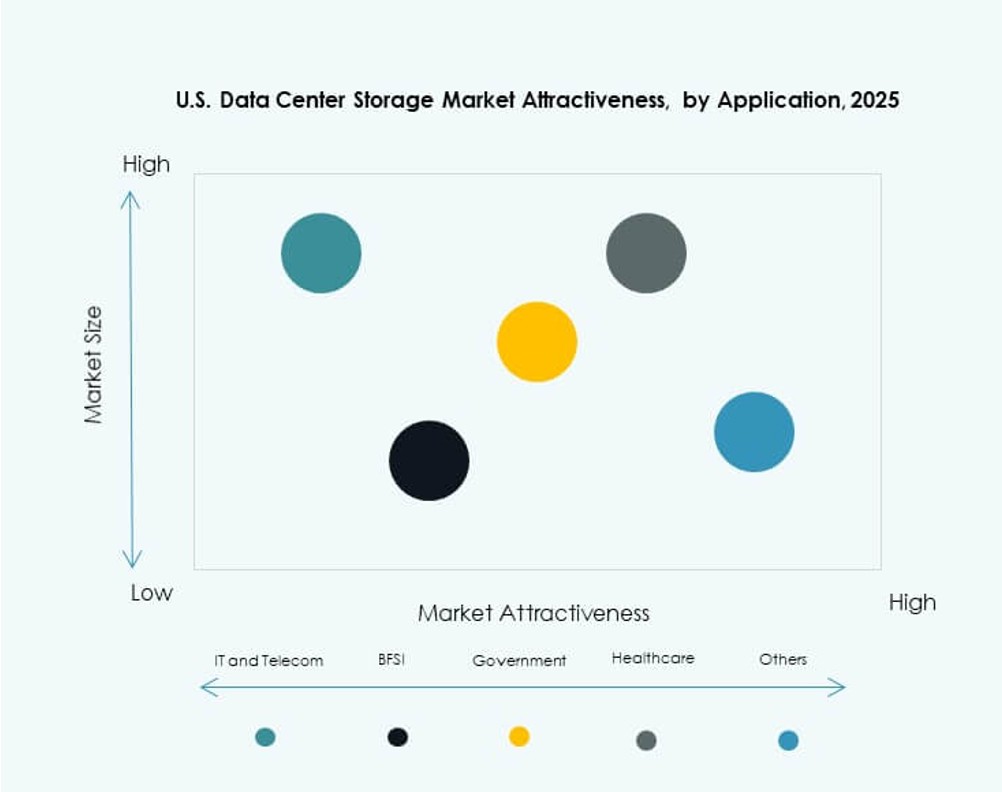

By Application

IT and telecom lead the market due to high data usage, large infrastructure footprint, and SLA sensitivity. BFSI and government sectors follow, driven by secure storage needs and compliance mandates. Healthcare grows fast due to EHRs, PACS, and diagnostic imaging. The U.S. Data Center Storage Market also serves retail, manufacturing, and media with scalable storage for structured and unstructured data.

Regional Insights

Northern Virginia Leads with Over 25% Share Due to Hyperscale Presence and Fiber Infrastructure

Northern Virginia remains the dominant subregion, hosting the largest concentration of hyperscale data centers. It accounts for more than 25% of the U.S. Data Center Storage Market share. Proximity to Washington D.C., advanced fiber connectivity, and favorable energy pricing attract operators. Loudoun County, known as “Data Center Alley,” supports extensive deployments by AWS, Microsoft, and Meta. The region sees continued investments in new storage capacity, especially for AI and cloud services.

- For instance, Northern Virginia saw under-construction data center capacity reach 2,078.2 MW in H1 2025, an 80% increase from prior periods, driven by hyperscale expansions.

California and Texas Account for 15–20% Each, Driven by Tech Ecosystems and Enterprise Demand

California benefits from Silicon Valley’s tech ecosystem, strong R&D presence, and early cloud adoption. It holds around 18% share of the U.S. Data Center Storage Market. Enterprises deploy storage across both colocation and on-premise models. Texas, with nearly 15% market share, offers strategic advantages in terms of land, energy, and tax incentives. Cities like Dallas and Austin witness growing enterprise cloud deployments and storage upgrades.

Emerging Hubs Like Ohio, Arizona, and Oregon Capture Rising Share from Cost-Efficient Expansions

Secondary markets such as Arizona, Ohio, and Oregon are attracting investment due to lower operational costs and renewable energy availability. These states offer cooling-friendly climates and land availability for hyperscale builds. Their collective share in the U.S. Data Center Storage Market is rising steadily beyond 10%. Enterprise and colocation providers expand into these zones to reduce TCO while meeting latency and compliance needs. These hubs also benefit from state-level incentives and skilled labor pipelines.

- For instance, Microsoft Azure Storage processes over 100 exabytes of data monthly across global regions, supporting rising enterprise demand. In 2025, Microsoft expanded its U.S. data center capacity by over 2 gigawatts, including growth in East US 2 and South Central US.

Competitive Insights:

- Hewlett Packard Enterprise (HPE)

- Dell Technologies

- IBM Corporation

- Cisco Systems, Inc.

- NetApp

- Seagate Technology

- Lenovo Group

- Veeam Software

- Huawei Technologies

- Hitachi Vantara

The U.S. Data Center Storage Market features strong competition between multinational hardware vendors, software-defined storage providers, and cloud-integrated solution developers. It is shaped by large players like Dell Technologies, HPE, and IBM that offer comprehensive portfolios across flash, hybrid, and object storage. Vendors such as NetApp and Seagate specialize in scalable solutions for cloud-native and enterprise workloads. The competitive dynamic is also influenced by rising demand for AI-ready, high-density storage systems and SDS platforms. Strategic focus on sustainability, NVMe integration, and workload optimization defines current product roadmaps. Companies actively engage in partnerships, product innovations, and acquisitions to expand customer base across BFSI, IT, and government sectors. The market rewards vendors that deliver low-latency, high-resilience systems with flexible deployment models.

Recent Developments:

- In October 2025, Pure Storage expanded its collaboration with Cisco and NVIDIA to deliver AI infrastructure solutions for enterprise customers. The initiative integrates high‑performance storage with AI‑optimized networking and compute resources.

- In January 2025, Google Cloud launched Anthos Filestore, a fully managed file storage service designed for Kubernetes-based, stateful workloads. The solution supports high-performance file systems and improves container-native storage for U.S. data center operators.