Executive summary:

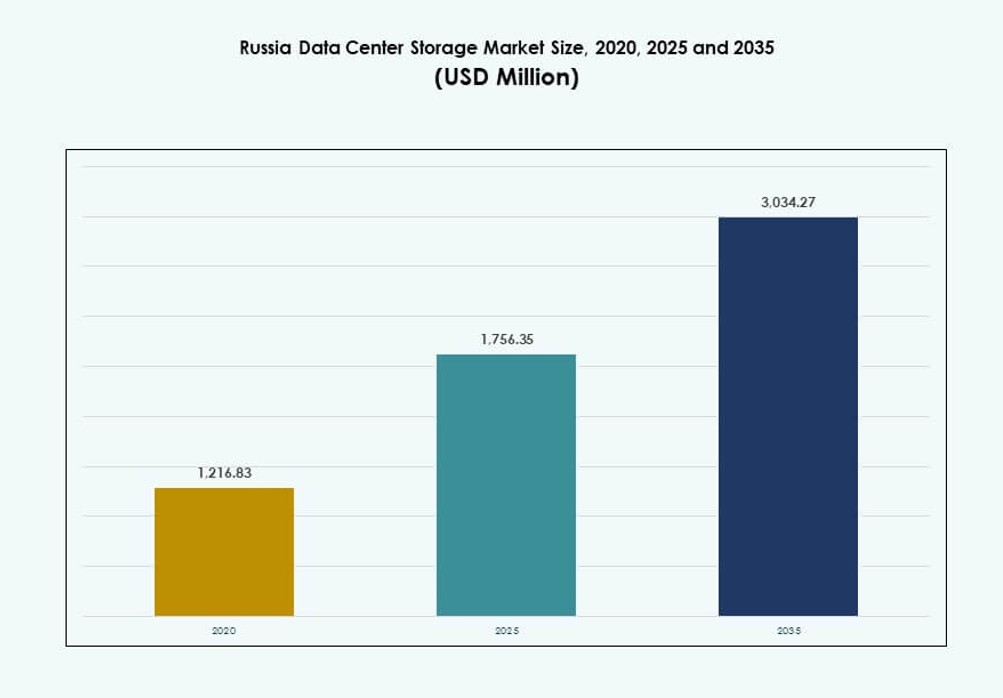

The Russia Data Center Storage Market size was valued at USD 1,216.83 million in 2020 to USD 1,756.35 million in 2025 and is anticipated to reach USD 3,034.27 million by 2035, at a CAGR of 5.56% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Russia Data Center Storage Market Size 2025 |

USD 1,756.35 Million |

| Russia Data Center Storage Market, CAGR |

5.56% |

| Russia Data Center Storage Market Size 2035 |

USD 3,034.27 Million |

Digital sovereignty laws, growing AI workloads, and cloud service expansion are reshaping the storage landscape in Russia. Enterprises are shifting toward hybrid and software-defined storage to improve flexibility, compliance, and cost efficiency. Increasing demand for high-throughput and low-latency solutions is driving flash storage adoption. State-backed projects and regulated industries are accelerating modernization. These trends position the Russia Data Center Storage Market as a strategic space for investment and infrastructure development.

Central Russia dominates due to the concentration of enterprises and digital services in Moscow. The Northwestern region, led by Saint Petersburg, is expanding through industrial digitization and tech investments. Emerging zones in Siberia and the Far East are gaining importance with growth in edge deployments and regional data hubs. These areas support industrial applications and help reduce data latency across vast geographies.

Market Dynamics:

Market Drivers

Digital Sovereignty Regulations Driving Domestic Storage Infrastructure Demand

Russia’s push for digital sovereignty continues to drive investments in local storage infrastructure. Regulations mandate the storage of Russian citizens’ data within national borders. This boosts demand for domestic data centers equipped with scalable storage systems. Enterprises in finance, healthcare, and telecom sectors lead this trend. Compliance pressures fuel upgrades from legacy infrastructure to software-defined and hybrid storage. The Russia Data Center Storage Market benefits from strong policy support and rising enterprise IT workloads. Local cloud providers scale operations to serve regulated sectors. Global sanctions limit external data transfers, making local storage essential. This regulatory push increases market resilience and long-term demand.

- For example, Sberbank broke ground in 2021 on a data center in Balakovo designed for at least 3,000 racks and up to 120,000 servers with 82 MW capacity to support local data processing under sovereignty rules, with first stage completion targeted for Q1 2023.

Enterprise Cloud Migration Encouraging Hybrid Storage Deployments

Russian enterprises are accelerating their transition toward hybrid IT architectures. This shift drives demand for hybrid storage solutions that combine on-premises and cloud systems. Organizations prefer flexibility in managing data across distributed environments. The need to reduce latency, improve disaster recovery, and meet compliance boosts hybrid adoption. The Russia Data Center Storage Market reflects a growing interest in flexible and secure storage platforms. Public-private partnerships also support cloud infrastructure growth. Domestic players expand capabilities to offer reliable storage services for business continuity. AI workloads, video analytics, and virtual desktop infrastructure need faster storage throughput. These trends increase enterprise investment in modern storage deployments.

Increased AI and IoT Workloads Necessitating Scalable and High-Speed Storage

High-performance storage solutions are gaining demand due to rapid growth in AI and IoT applications. Edge computing, machine vision, and data-rich applications are rising in manufacturing, energy, and telecom sectors. These use cases require real-time data access and low-latency storage. The Russia Data Center Storage Market is witnessing upgrades toward NVMe-based and all-flash architectures. Enterprises prioritize faster IOPS and high endurance to support AI inference and training models. Industrial IoT adoption also increases bandwidth and storage capacity needs. Storage vendors localize their offerings to comply with security and performance requirements. Innovation in storage controllers and software optimization improves overall efficiency. Strategic digital projects push demand for storage with better analytics integration.

Public Sector Modernization and Smart City Projects Supporting Long-Term Growth

Government-backed digital transformation programs are transforming the public sector IT landscape. Initiatives such as e-Government, smart cities, and digital healthcare expand storage infrastructure demand. These projects involve massive data collection and analytics, pushing long-term storage investments. The Russia Data Center Storage Market sees increased participation from local system integrators and OEMs. Public institutions deploy cloud-compatible storage for scalability and data protection. Infrastructure spending includes upgrades for backup, disaster recovery, and high-availability storage. Smart traffic systems, surveillance networks, and health record digitization rely on robust storage backbones. Long-term vision for digital public infrastructure makes storage a key enabler. This environment strengthens market attractiveness for investors and service providers.

- For instances, Moscow faces land shortages for data centers as of November 2024, with Sberbank and T-bank planning facilities for over 100,000 servers each to support smart city and public digital projects.

Market Trends

Rising Demand for Liquid-Cooled Storage Servers in High-Density Racks

Thermal management in dense server environments is reshaping storage system design in Russia. Large data centers shift to liquid-cooled infrastructure to improve energy efficiency and increase rack density. These setups enable compact layouts while maintaining performance stability. The Russia Data Center Storage Market sees adoption of cold plate and rear-door heat exchanger solutions. Storage arrays for AI and HPC workloads integrate direct-to-chip cooling methods. Energy-saving benefits align with ESG targets set by local enterprises. OEMs offer modular storage servers optimized for thermal performance. Hyperscale facilities deploy these systems to reduce power usage effectiveness. Thermal-aware designs influence future procurement standards in modern Russian data centers.

Edge Storage Expansion to Support Industrial and Remote Applications

Growing digitization in remote industrial zones drives edge storage deployments across Russia. Sectors like oil & gas, mining, and utilities require localized data processing to ensure low latency and resilience. Edge facilities host modular storage units for real-time analytics and AI model inference. The Russia Data Center Storage Market supports use cases where unreliable connectivity limits cloud dependency. Portable storage units enable flexible operations in extreme environments. Edge deployments integrate solid-state drives for faster read/write cycles. Vendors develop compact form factors to support limited space and power budgets. Industrial automation drives demand for low-maintenance and ruggedized storage systems. This trend accelerates decentralized storage growth in rural and border regions.

Growing Popularity of Object Storage for Media, Backup, and Archival Use Cases

Object storage is becoming the preferred model for unstructured data management in Russia. Media firms, surveillance agencies, and cloud providers use it to manage high-volume, low-cost data repositories. The Russia Data Center Storage Market experiences increased adoption of S3-compatible platforms and open-source object storage software. Scalability and durability make it suitable for archival and backup needs. Data growth from video content, logs, and analytics pushes shift from file-based systems. Object storage also supports multi-tenant applications and content delivery networks. Startups and mid-sized enterprises value the pay-as-you-grow model. Integration with AI pipelines and metadata tagging enhances data accessibility. It provides long-term cost-efficiency over traditional block storage setups.

Integration of AI-Powered Storage Management and Predictive Analytics

Storage solutions with built-in AI and machine learning capabilities are gaining traction. Predictive maintenance, auto-tiering, and intelligent data placement improve storage efficiency. The Russia Data Center Storage Market features smart storage systems that monitor workloads and optimize performance in real time. AI tools help detect anomalies, forecast usage, and reduce downtime. Enterprises benefit from better SLA adherence and operational transparency. These capabilities are embedded into software-defined storage platforms. ML-driven dashboards enhance IT administrators’ decision-making in complex environments. Government-funded digital labs also explore AI-enhanced storage for research. This integration aligns storage performance with evolving business intelligence demands.

Market Challenges

Geopolitical Sanctions and Restricted Access to International Storage Technologies

Ongoing geopolitical tensions limit Russia’s access to advanced international storage technologies and vendors. Many Western suppliers have withdrawn from the market, disrupting existing vendor relationships. Enterprises face constraints in sourcing high-end flash systems, storage controllers, and software updates. This hampers modernization efforts in large-scale data centers. The Russia Data Center Storage Market must rely on domestic or Asian alternatives, some of which lag in performance benchmarks. Compatibility issues arise with legacy infrastructure when switching suppliers. Investment risk increases due to uncertainty in global tech supply chains. System integrators must redesign solutions based on available hardware, affecting lead times. Skill gaps in deploying new platforms further slow implementation cycles.

Rising Cybersecurity Threats and Compliance Barriers for Data-Centric Infrastructure

With growing digitization and cloud adoption, Russian enterprises face escalating risks from cyberattacks and data breaches. Storage environments become prime targets due to the high volume of critical data. The Russia Data Center Storage Market must align with evolving data protection laws and sector-specific compliance frameworks. Encryption, access control, and audit logging requirements raise operational complexity. Domestic developers need to enhance cybersecurity features in storage software. Financial institutions and government bodies demand certified and secure storage platforms. Limited availability of mature local solutions presents gaps in incident response and disaster recovery. These factors increase infrastructure cost and hinder adoption timelines.

Market Opportunities

Development of Sovereign Cloud Ecosystems with Localized Storage Infrastructure

Russia’s focus on building sovereign cloud platforms opens new avenues for localized storage investments. National providers are expanding capacity with fully Russian-hosted storage infrastructure. The Russia Data Center Storage Market benefits from this ecosystem shift that reduces reliance on foreign services. Local governments and regulated sectors prefer in-country hosted data to meet compliance. OEM partnerships with state-backed cloud operators create new channels for growth.

Strategic Investments in AI Research Facilities and Data-Intensive Innovation Hubs

Growth of AI innovation centers and academic supercomputing labs increases demand for high-performance storage. These facilities prioritize flash-based systems with parallel data access and real-time throughput. The Russia Data Center Storage Market can expand by supporting these data-centric innovation clusters. Government funding and grants encourage participation from local storage vendors. Startups working on image processing, NLP, and genomics further drive demand.

Market Segmentation

By Storage Type

The Russia Data Center Storage Market is segmented into traditional storage, all-flash storage, hybrid storage, and others. All-flash storage is gaining traction due to faster performance and support for latency-sensitive applications like AI and VDI. Hybrid storage remains dominant for balancing cost-efficiency and speed. Traditional storage still sees limited use in backup and archival environments. The shift toward flash-based arrays is more visible in financial and cloud sectors.

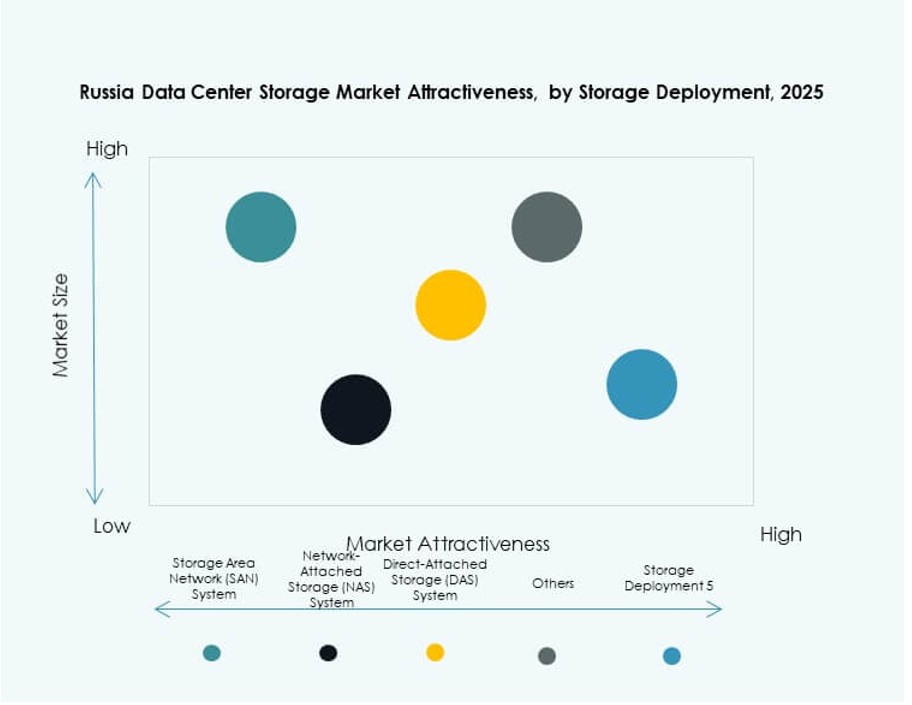

By Storage Deployment

Storage Area Network (SAN) systems lead in high-performance workloads and enterprise databases. Network-Attached Storage (NAS) gains popularity for file sharing, especially in media and government sectors. Direct-Attached Storage (DAS) serves SMBs and edge environments due to simplicity. The Russia Data Center Storage Market sees SAN adoption rise in Tier III and Tier IV data centers. Hybrid deployments mixing NAS and SAN offer flexible integration.

By Component

Hardware dominates the Russia Data Center Storage Market due to ongoing infrastructure expansion. Storage arrays, enclosures, and high-capacity drives drive hardware sales. Software is growing with the adoption of software-defined storage, backup platforms, and storage virtualization tools. Vendors bundle software with hardware to enhance value. Enterprises focus on integrated solutions with monitoring and automation features.

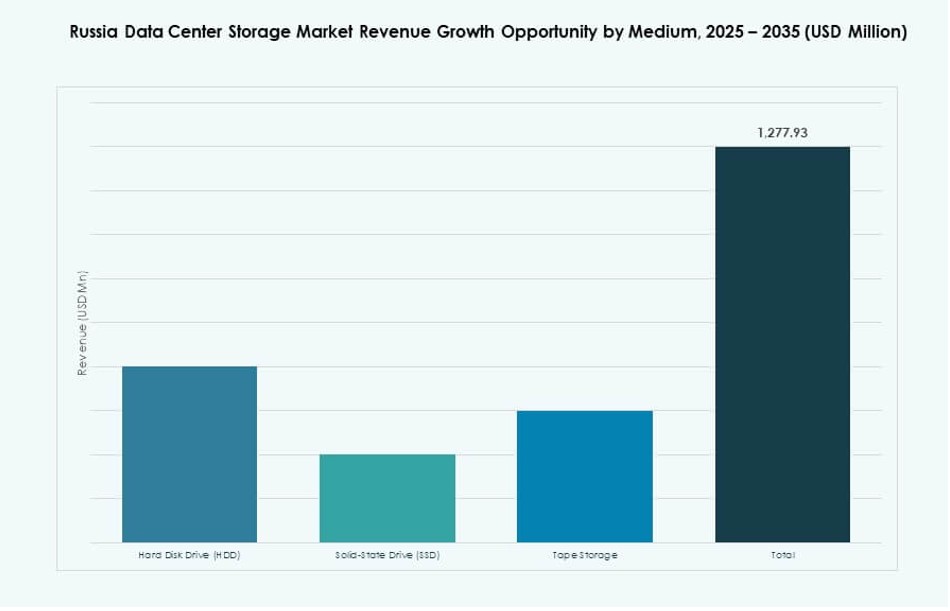

By Medium

Solid-State Drives (SSDs) are outpacing Hard Disk Drives (HDDs) due to their performance advantages. SSDs support AI, analytics, and database workloads needing low latency. HDDs remain in use for archival and video surveillance. Tape storage has a niche in long-term backup due to durability and low cost. The Russia Data Center Storage Market sees SSDs gaining share in Tier I and II facilities.

By Deployment Model

Hybrid models are becoming the preferred deployment choice, offering flexibility in combining cloud and on-premises storage. Cloud-based storage adoption grows with local cloud service providers expanding presence. On-premises systems remain relevant in government and defense sectors. The Russia Data Center Storage Market reflects balanced demand across deployment types. Businesses opt for models aligned with compliance and workload patterns.

By Application

IT and telecom sectors dominate storage consumption due to constant data processing needs. BFSI sector invests in encrypted and high-availability storage to meet security regulations. Government and healthcare drive growth through digital records and e-governance. The Russia Data Center Storage Market benefits from increasing data intensity in these sectors. Other sectors include education, retail, and logistics, each with growing digital footprints.

Regional Insights

Central Russia Leads with Over 40% Market Share Due to Dense Digital Ecosystem

Central Russia, especially Moscow and surrounding areas, holds more than 40% share in the Russia Data Center Storage Market. This region benefits from the concentration of large enterprises, government agencies, and hyperscale data centers. High internet penetration and established fiber networks enable large-scale storage deployments. Domestic cloud providers focus on Moscow for initial rollouts. Financial and telecom sectors headquartered in this region further drive demand.

- For instance, Rostelecom’s Moscow-III data center supports 900 racks across 3,500 square meters with 10 MW power capacity and Tier III reliability standards.

Northwestern Russia Accounts for 20–25% Due to Industrial Hubs and Proximity to Europe

Northwestern Russia, with Saint Petersburg as a key center, contributes 20–25% of market share. The region supports data-heavy applications in manufacturing, logistics, and maritime sectors. Proximity to European networks improves cross-border latency and redundancy. Data center operators in this zone invest in high-availability and energy-efficient storage. Local government initiatives support smart infrastructure and digitalization programs. Growth here is sustained by enterprise and state modernization.

- For instance, AtomData’s Xelent data center in Saint Petersburg offers 1,476 rack spaces with 10 MW power, expandable to 14 MW. Proximity to European networks improves cross-border latency and redundancy.

Siberia and Far East Regions Emerge with 15–18% Share Driven by Edge and Industrial Use Cases

Siberia and the Russian Far East are emerging regions, together contributing around 15–18% of the total market. These regions see rising demand for edge and modular storage systems due to remote industrial zones. Energy, mining, and transportation sectors require localized data processing. Storage vendors deploy rugged systems optimized for harsh climates and power-limited setups. New data center developments near Irkutsk and Vladivostok aim to serve regional workloads. Investment in energy-efficient cooling and local cloud hubs supports ongoing expansion.

Competitive Insights:

- Kaspersky

- Yandex Cloud

- Rostelecom

- IBS Group

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- Cisco Systems, Inc.

- Lenovo Group

- NetApp

- Huawei Technologies Co., Ltd.

The Russia Data Center Storage Market is shaped by a combination of global OEMs and strong domestic players. Local firms like Kaspersky, Yandex Cloud, and Rostelecom capitalize on regulatory mandates for data localization and sovereign infrastructure. Global leaders such as Dell, HPE, and NetApp offer high-performance systems but face restrictions from import limitations and geopolitical tensions. Chinese players like Huawei and Lenovo gain ground due to strategic partnerships and supply availability. It reflects a shift toward hybrid, cloud-based, and software-defined platforms. Vendors focus on enterprise, telecom, and public sectors with customized solutions. Product diversification, service integration, and regional alliances define growth strategies. Players emphasize cybersecurity, scalability, and compliance to remain competitive in an evolving storage environment.

Recent Developments:

- In October 2025, MegaFon launched a new data center in St. Petersburg featuring domestically manufactured equipment to support enhanced storage and processing needs amid Russia’s focus on self-reliant tech infrastructure.

- In October 2025, Rostelecom began construction of a data center for PhosAgro Group at the Volkhov branch of Apatit JSC, aiming to meet industrial-scale data storage demands, with completion targeted for 2026.

- In January 2025, Lenovo Group entered into a definitive agreement to acquire Infinidat Ltd., a provider of high-end enterprise storage systems, enhancing its global and regional data center storage portfolio.

- In July 2025, Seagate Technology started global shipments of its 30TB Exos M and IronWolf Pro hard drives, powered by HAMR technology, to meet increasing AI-driven storage requirements, including demand from Russian data centers aligned with national data sovereignty goals.