Executive summary:

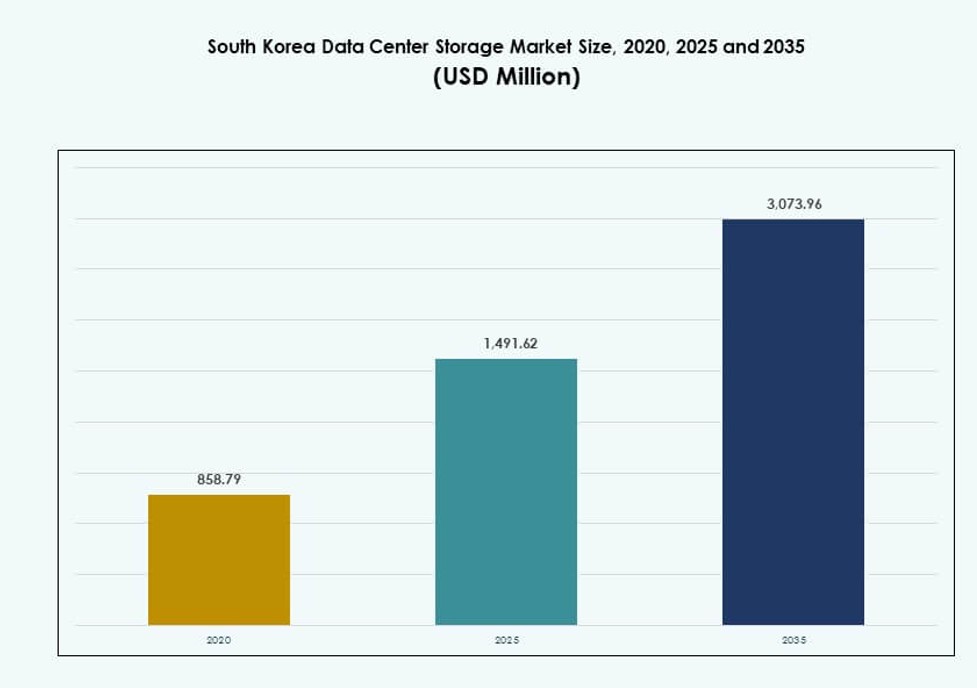

The South Korea Data Center Storage Market size was valued at USD 858.79 million in 2020 to USD 1,491.62 million in 2025 and is anticipated to reach USD 3,073.96 million by 2035, at a CAGR of 7.42% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| South Korea Data Center Storage Market Size 2025 |

USD 1,491.62 Million |

| South Korea Data Center Storage Market, CAGR |

7.42% |

| South Korea Data Center Storage Market Size 2035 |

USD 3,073.96 Million |

Strong 5G infrastructure, growing AI deployment, and the rise of cloud-native applications are driving demand for advanced storage systems in South Korea. Enterprises are adopting flash-based, hybrid, and software-defined storage to handle real-time data needs and reduce latency. Innovation in NVMe, AI-based orchestration, and regulatory-driven data localization is shaping purchasing decisions. This environment makes the market strategically valuable for hyperscale operators, telecom firms, and tech service providers looking to expand storage capabilities and meet compliance.

The Seoul Metropolitan Area leads the market due to high data density, colocation capacity, and cloud region presence. Gyeonggi-do and Incheon are emerging as alternative zones, supported by new land availability and industrial demand. Ulsan and Busan are seeing growth tied to hyperscale expansion and edge deployment for logistics and smart port operations. This distribution reflects a balanced trend between core and regional zones for data center storage development.

Market Dynamics:

Market Drivers

Strong Digital Infrastructure and 5G Deployment Are Accelerating the Need for Storage Solutions

South Korea’s advanced telecom ecosystem supports high-volume data generation. The widespread rollout of 5G accelerates edge computing and real-time analytics. Enterprises are upgrading their legacy systems to support modern digital services. This transformation drives demand for high-performance and scalable storage systems. Public cloud providers are also expanding operations to handle growing workloads. Government support for digitalization strengthens long-term infrastructure development. Regulatory compliance for data localization promotes local storage expansion. The South Korea Data Center Storage Market benefits from these aligned developments. It reflects strong public-private coordination in building resilient digital frameworks.

- For instance, South Korea achieved nationwide 5G coverage by April 2024 through SK Telecom, KT, and LG Uplus, with average download speeds reaching 1,025.52 Mbps across carriers in 2024.

Rapid Adoption of AI and Big Data Applications Is Fueling Storage Innovation

AI-driven analytics and machine learning systems require low-latency, high-throughput storage. South Korea’s tech firms are deploying AI-specific infrastructure with flash-based storage at scale. Enterprises in finance, e-commerce, and manufacturing now generate complex datasets. These datasets demand real-time access and secure backups. Innovation in NVMe-over-Fabrics and AI-powered storage management tools is advancing operational efficiency. Companies are integrating hybrid systems to balance performance and cost. New workloads are shifting storage architecture from centralized to distributed. This evolution drives continued investment in high-speed storage. The South Korea Data Center Storage Market is adapting rapidly to these computational needs.

Strategic Government Initiatives Support Data Sovereignty and Local Storage Mandates

Regulatory changes push enterprises to retain data within national boundaries. This creates steady demand for on-premises and localized cloud storage. Initiatives like the “K-Digital” program promote digital service expansion. Financial subsidies and land allocation for data parks help foreign and local players. Government mandates on disaster recovery boost backup infrastructure. Public institutions increasingly move to hybrid storage for compliance and resilience. Local governments are also enabling smart city data hubs. The South Korea Data Center Storage Market reflects this policy-driven expansion. It benefits from strong digital sovereignty and national security concerns.

- For instance, the Ministry of Science and ICT allocated private 5G frequencies in the 4.7GHz and 28GHz bands to 56 locations across 35 companies by February 2024 to support digital transformation.

Rising Enterprise Digitalization and E-Commerce Growth Amplify Storage Infrastructure

Enterprises in South Korea are accelerating digital adoption to remain competitive. Sectors like BFSI, healthcare, and media demand robust data storage systems. The rapid shift to e-commerce increases unstructured data volumes. User data, video content, and transactions require scalable object storage systems. SaaS-based platforms expand, driving storage for cloud-native applications. SMEs are investing in flexible and secure storage models. Organizations prefer modular deployments to control costs. The South Korea Data Center Storage Market tracks closely with enterprise modernization. It continues to scale with evolving commercial needs.

Market Trends

All-Flash Arrays and NVMe Interfaces Are Gaining Ground in Performance-Critical Environments

Enterprises seek faster access to data for analytics and workload processing. All-flash arrays dominate new deployments in financial and AI applications. NVMe-based architectures enhance throughput, reducing latency in transactional systems. Cloud providers integrate NVMe-over-Fabrics for seamless virtualization. Traditional HDD systems lose share in latency-sensitive applications. Flash cost per GB continues to fall, encouraging faster migration. Government data centers deploy flash to manage AI and IoT workloads. The South Korea Data Center Storage Market shows a clear move toward performance optimization. It reflects growing focus on mission-critical uptime and agility.

Growth of Colocation and Hyperscale Facilities Is Redefining Storage Demand

Rising cloud adoption fuels hyperscale buildouts in Seoul and surrounding areas. Colocation providers offer storage-as-a-service tailored to hybrid workloads. Cross-connectivity demands drive unified storage for diverse tenants. AI, edge, and gaming workloads influence storage configuration in hyperscale sites. DCIM tools now integrate storage resource management. Operators invest in energy-efficient and scalable storage modules. High-density storage becomes crucial for space optimization. The South Korea Data Center Storage Market is evolving with hyperscale architecture. It supports diversified, software-defined storage configurations.

Increased Focus on Cybersecurity Drives Secure Storage Solutions and Air-Gapped Systems

Enterprises emphasize ransomware protection and regulatory compliance. Demand grows for immutable storage and WORM (write once read many) configurations. Organizations deploy air-gapped and encrypted storage layers for sensitive data. Financial institutions adopt blockchain-based storage logs for auditability. Sovereign cloud models support compliance with Korean privacy regulations. Security certifications for storage platforms gain relevance in procurement. Storage vendors offer tiered security models integrated with backup systems. The South Korea Data Center Storage Market integrates advanced security layers. It aligns with growing national and sector-specific compliance requirements.

Edge Storage Deployment Expands in Support of Industrial and Urban IoT Infrastructure

Smart cities and factory automation projects generate real-time data at the edge. Regional nodes require micro data centers with fast local storage. Edge-specific SSD systems are now standard in logistics and industrial sectors. Healthcare and surveillance systems adopt edge storage for latency-sensitive video. Telcos partner with storage providers to offer managed edge platforms. Newer designs prioritize energy-efficient and rugged storage media. Real-time decision-making drives investment in intelligent caching systems. The South Korea Data Center Storage Market adapts to edge workloads. It supports distributed intelligence in urban and industrial zones.

Market Challenges

High Energy Costs and Limited Renewable Integration Restrain Storage Expansion

South Korea faces rising energy prices and limited land for green energy generation. Data centers depend on power-intensive infrastructure, including high-capacity storage arrays. Lack of widespread renewable energy usage raises operational costs. This affects TCO for long-term storage expansion, especially in urban zones. ESG compliance pressure pushes operators to upgrade cooling and efficiency. Some enterprises delay upgrades due to sustainability targets. Regional policy gaps exist for incentivizing clean power integration in storage. The South Korea Data Center Storage Market absorbs these cost-driven challenges. It must balance growth with sustainability and energy constraints.

Complex Regulatory Environment and Land Shortage Delay New Storage Projects

Securing permits and land for new storage sites in Seoul remains difficult. Zoning laws and environmental clearances slow hyperscale expansion. Regulatory compliance adds complexity for cross-border storage use. Foreign operators face longer onboarding timelines for colocation offerings. Municipal limits on power usage affect rack density and modular storage design. The absence of standardized procurement policy complicates public sector tenders. Delays in fiber infrastructure outside metro zones hinder edge storage growth. The South Korea Data Center Storage Market must navigate fragmented regulations. It requires multi-level alignment for faster infrastructure rollout.

Market Opportunities

Growing Investment from Global Cloud Providers Boosts Storage Innovation and Localization

Amazon Web Services, Microsoft Azure, and Google Cloud expand their Korean footprint. These players bring advanced storage solutions aligned with AI and analytics demand. Local partnerships drive integration of Korean language NLP datasets. Colocation firms adapt their storage services to meet global compliance standards. Public-private collaboration encourages regional data availability zones. The South Korea Data Center Storage Market benefits from localized innovation. It reflects global investment and indigenous technology synergies.

Surging AI and Quantum Research Opens Doors for Specialized Storage Infrastructure

Government-funded research centers drive quantum and neuromorphic computing development. These programs demand new forms of ultra-low latency and high-resilience storage. Startups are innovating in AI training data warehousing and GPU-optimized storage. Sector-specific data lakes emerge in healthcare and manufacturing. The South Korea Data Center Storage Market supports experimental and high-throughput platforms. It positions the country as a leader in advanced compute-storage integration.

Market Segmentation

By Storage Type

Traditional storage holds a declining share, with enterprises shifting to All-Flash and Hybrid systems. All-Flash Storage is gaining ground due to fast data access, especially in BFSI and cloud operations. Hybrid Storage solutions balance cost and performance, favored by government and mid-tier firms. Others include object-based and software-defined storage tailored for AI workloads. In the South Korea Data Center Storage Market, All-Flash leads with performance-centric deployments.

By Storage Deployment

Network-attached Storage (NAS) dominates due to ease of integration and scalability. SAN systems are used by high-end applications requiring low-latency and structured access. DAS systems are preferred in edge and standalone setups. Others include hyper-converged infrastructure in SMEs. In the South Korea Data Center Storage Market, NAS is the dominant format due to multi-tenant and hybrid cloud environments.

By Component

Hardware leads in revenue due to physical storage unit purchases and renewals. High-capacity SSD and NVMe drives account for the largest share. Software includes backup, data replication, storage virtualization, and orchestration. In the South Korea Data Center Storage Market, hardware maintains a majority share, but software demand is growing fast.

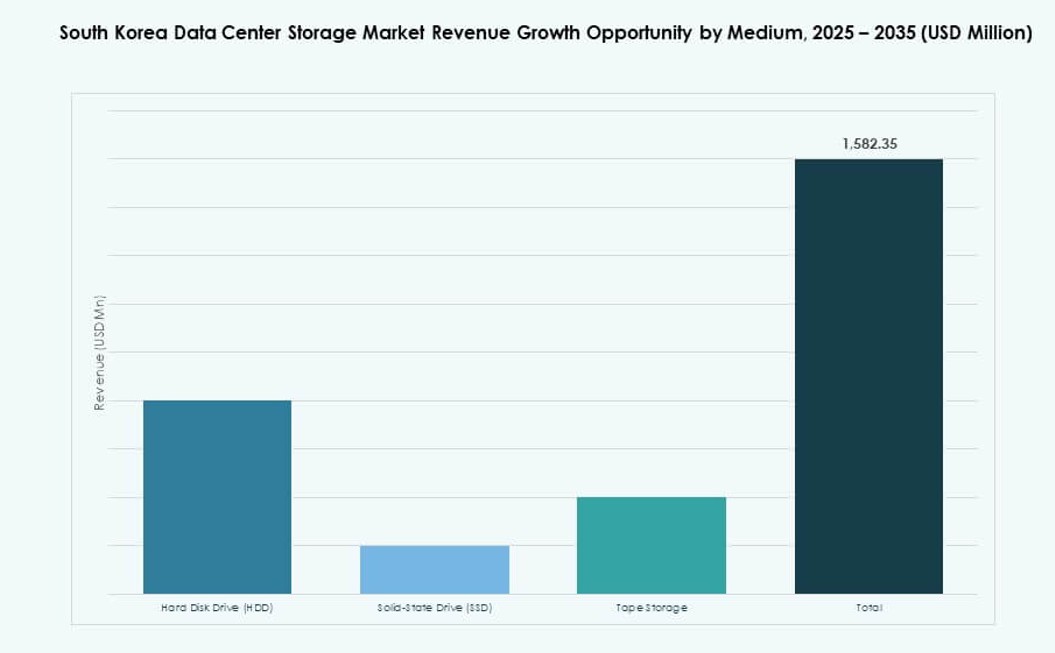

By Medium

Solid-State Drives (SSD) are dominant due to better performance and dropping prices. Hard Disk Drives (HDD) are still used in archival and cold storage applications. Tape storage is limited to government and archival mandates. The South Korea Data Center Storage Market reflects SSD-driven innovation with emphasis on NVMe formats.

By Deployment Model

Cloud-based deployment leads due to rapid digital service adoption. On-premises setups remain strong in sectors with compliance needs. Hybrid deployment is rising, offering flexibility and resilience. The South Korea Data Center Storage Market supports cloud-first but increasingly hybrid infrastructure preferences.

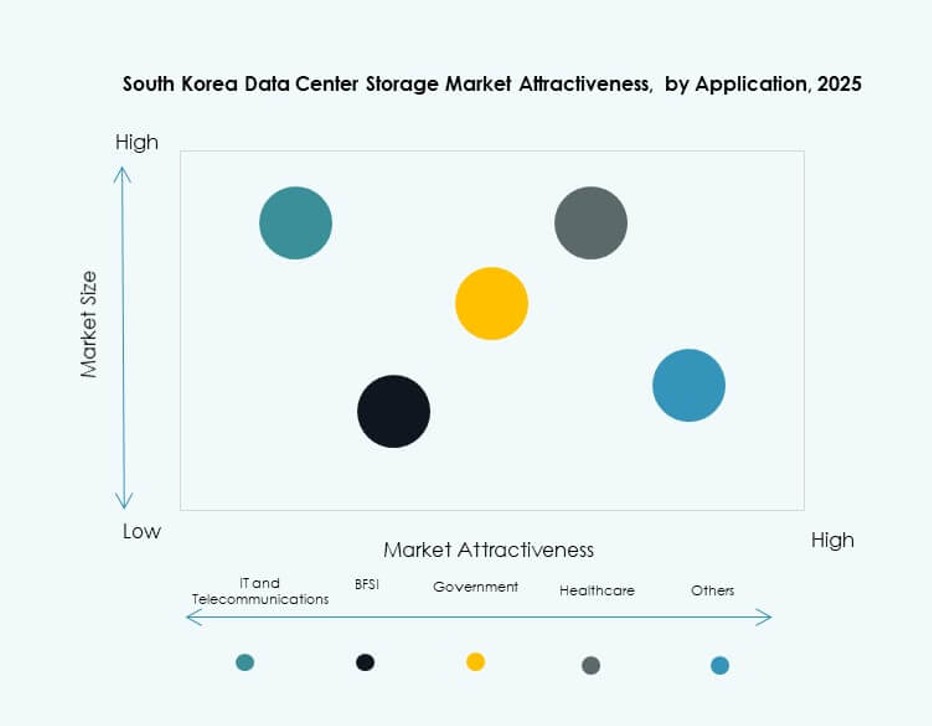

By Application

IT and Telecommunications dominate usage, driven by high data throughput and uptime needs. BFSI follows due to transaction-heavy workloads and backup needs. Government applications focus on secure and sovereign storage. Healthcare and others use storage for imaging, records, and analytics. In the South Korea Data Center Storage Market, IT and Telecom hold the largest segmental share.

Regional Insights

Seoul Metropolitan Region Leads with Over 65% Market Share in Storage Infrastructure

Seoul remains the dominant hub due to high data demand from telecom, finance, and tech. The capital city concentrates hyperscale cloud zones, colocation hubs, and enterprise data centers. Government agencies and digital service platforms drive localized data storage requirements. Strong network connectivity and skilled labor further enhance Seoul’s dominance. The South Korea Data Center Storage Market benefits from this centralized capacity. It reflects both domestic and foreign investment in the capital region.

Gyeonggi-do and Incheon Show Rising Demand with New Data Park Developments

The surrounding Gyeonggi-do region and Incheon account for nearly 20% market share. Industrial corridors in Pangyo and Suwon attract logistics, e-commerce, and smart factory investments. New data park developments support both colocation and enterprise storage expansion. Improved fiber and road connectivity ease multi-site deployments. These regions offer better land availability and lower costs than Seoul. The South Korea Data Center Storage Market sees accelerated growth in these suburban zones.

- For instance, Kakao signed an MOU for a 92,000 sqm AI data center in Namyangju, Gyeonggi-do, with construction starting 2026.

Southern and Eastern Regions Contribute 15% Share Through Government and Edge Use Cases

Busan, Daegu, and Ulsan form the emerging cluster in southern Korea. These regions support edge storage for port logistics, manufacturing, and public administration. Public sector agencies deploy backup systems to enhance disaster recovery. Energy-efficient micro data centers rise in regional campuses. Industrial parks and national security sites demand localized infrastructure. The South Korea Data Center Storage Market records steady growth across these areas. It aligns with the government’s balanced regional development strategy.

- For instance, Digital Edge acquired a site in Busan from Sejong Telecom, expanding its platform with integrated connectivity for edge applications.

Competitive Insights:

- Samsung SDS

- Samsung Electronics

- SK hynix

- LG CNS

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- NetApp

- IBM Corporation

- Hitachi Vantara

- Huawei Technologies Co., Ltd.

The South Korea Data Center Storage Market features a blend of domestic tech giants and global infrastructure providers. Samsung SDS and Samsung Electronics lead with deep integration across data infrastructure, semiconductor storage, and enterprise IT services. SK hynix supports the supply of high-density DRAM and NAND flash components. LG CNS and HPE focus on hybrid and software-defined solutions. Global players like Dell, NetApp, and IBM deliver scalable systems for hyperscale and enterprise clients. Huawei and Hitachi Vantara are expanding edge and modular storage offerings. The market remains highly competitive, with players investing in NVMe, AI-driven storage, and composable infrastructure to differentiate their portfolios. It shows increasing collaboration between telecom, cloud, and IT sectors to address Korea’s high-speed, high-volume storage demand.

Recent Developments:

- In October 2025, Samsung SDS signed a partnership with OpenAI to jointly develop AI data centers, provide enterprise AI services like ChatGPT Enterprise, and offer reseller support for OpenAI solutions in Korea.

- In June 2025, SK Group partnered with Amazon Web Services (AWS) on a $5.1 billion investment for a hyperscale AI data center in Ulsan, expanding cloud storage infrastructure with plans for 1 GW capacity to support advanced storage needs.

- In May 2025, Pure Storage and SK Hynix announced a strategic partnership to co-develop QLC flash modules optimized for hyperscale AI clusters, integrating SK Hynix’s 232-layer QLC NAND with Pure Storage’s DirectFlash software for enhanced data center storage performance.

- In January 2025, Penguin Solutions, SK Telecom, and SK Hynix formed a venture to deliver integrated AI data-center racks globally, focusing on storage-efficient solutions for high-density workloads.