Executive summary:

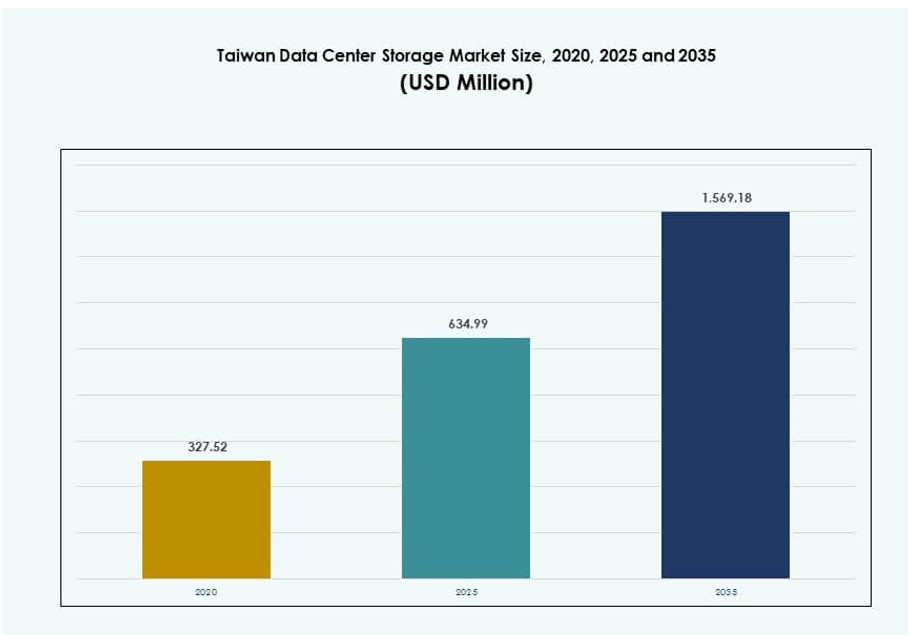

The Taiwan Data Center Storage Market size was valued at USD 327.52 million in 2020 to USD 634.99 million in 2025 and is anticipated to reach USD 1,569.18 million by 2035, at a CAGR of 9.37% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Taiwan Data Center Storage Market Size 2025 |

USD 634.99 Million |

| Taiwan Data Center Storage Market, CAGR |

9.37% |

| Taiwan Data Center Storage Market Size 2035 |

USD 1,569.18 Million |

The market is being driven by rising AI workloads, edge deployments, and smart manufacturing initiatives. Enterprises are adopting NVMe and all-flash systems to enhance data throughput and scalability. Hybrid cloud infrastructure and SDS adoption continue to grow as organizations prioritize agility and compliance. Government-backed digital programs and Taiwan’s leadership in electronics manufacturing further accelerate infrastructure investments. The market is strategically vital for firms aiming to scale digital operations and ensure secure, high-performance storage.

Taipei holds the largest share due to its dense IT ecosystem and network maturity, attracting hyperscale and colocation investments. Taoyuan and Hsinchu are emerging as strong secondary hubs, driven by tech manufacturing, R&D zones, and better land availability. Taichung and southern regions support enterprise and edge deployments. These areas are expanding as part of Taiwan’s effort to decentralize and diversify its data center footprint.

Market Dynamics:

Market Drivers

Strong Push for Cloud, AI, and HPC Workloads Demanding Fast, Scalable Storage Infrastructure

The Taiwan Data Center Storage Market is gaining momentum through the expansion of cloud-native architectures and AI-focused computing environments. Enterprises are adopting storage systems that support GPU-accelerated workloads and high-speed parallel processing. Strong demand comes from AI model training, machine vision, and smart manufacturing applications. Government-backed digital economy programs continue to fund research parks and tech innovation hubs. It aligns data storage priorities with Taiwan’s leadership in semiconductors and electronics. Growing workloads from hyperscalers, including edge nodes and backup systems, require fast, scalable storage layers. Enterprises seek latency optimization, data redundancy, and faster IOPS for critical workloads. The market drives adoption of modular systems that can be deployed across private, public, and hybrid environments.

- For instance, GMI Cloud is building an AI Factory in Taiwan equipped with 7,000 Nvidia GPUs across 96 high-density racks, using VAST Data’s architecture to support AI training at hyperscale. The deployment strengthens Taiwan’s AI infrastructure with next-generation storage systems.

Enterprise Storage Requirements Evolving Through IoT Integration and Smart Manufacturing

Smart factory projects, led by semiconductor and electronics companies, continue to reshape the enterprise data environment. The rise of industrial IoT platforms generates massive volumes of real-time operational data. It demands storage systems that support uninterrupted availability and resilient backup. Companies invest in predictive maintenance analytics and digital twins, increasing the need for active data retrieval. Storage solutions embedded with AI-driven management improve resource allocation and uptime. The Taiwan Data Center Storage Market benefits from edge computing initiatives where localized storage reduces latency. Regulatory requirements for high-availability systems further promote hybrid storage systems. Industrial zones require secure, interoperable storage infrastructure to connect design, production, and logistics chains.

Strategic Role of Government-Led Digital Infrastructure and Cybersecurity Mandates

Taiwan’s Ministry of Digital Affairs and National Development Council have accelerated the digital transformation of public and enterprise systems. Initiatives like 5G expansion and national cloud frameworks demand new-generation storage technologies. Public cloud data centers are expected to complement sovereign cloud models in future government deployments. Data privacy and disaster recovery standards encourage more resilient and scalable storage solutions. It enables seamless failover capabilities, high-frequency backup, and cross-site replication. Cybersecurity protocols aligned with international benchmarks are becoming essential, especially for government and BFSI users. The Taiwan Data Center Storage Market benefits from the integration of secure storage technologies with government cloud systems. Storage vendors targeting this segment must offer encryption, access control, and recovery as default layers.

- For instance, Taiwan’s new cloud computing centre in Tainan hosts the ‘Nano 4’ supercomputer equipped with 1,760 Nvidia H200 GPUs and 144 Nvidia Blackwell chips, signaling strong investment in AI compute and associated storage infrastructure

Rising Hyperscale and Colocation Capacity Fueling Multi-Tenant Storage Adoption

Taiwan is experiencing fast-paced growth in colocation and hyperscale facilities across Taipei, Taoyuan, and Taichung. These deployments focus on dense compute clusters supported by high-speed, modular storage solutions. Multi-tenant environments require shared but isolated storage pools with dynamic resource allocation. Cloud providers, telecom operators, and managed service firms are scaling their infrastructure footprints to meet demand. Object-based and scale-out file storage systems are becoming central to high-volume service delivery. It creates opportunities for NVMe-over-Fabrics and software-defined storage platforms. The Taiwan Data Center Storage Market supports this trend through investment in low-latency, tiered, and redundant storage layers. This supports tenants across e-commerce, video streaming, gaming, and enterprise SaaS segments.

Market Trends

Adoption of Software-Defined Storage Solutions Transforming Storage Architectures Across Enterprises

The Taiwan Data Center Storage Market is witnessing a shift from hardware-centric models to software-defined storage (SDS). SDS platforms improve flexibility, enabling businesses to deploy unified systems across hybrid environments. It reduces vendor lock-in and provides automated tiering and provisioning. Organizations value the centralized control plane for managing heterogeneous workloads. The rise in containerization also demands persistent storage through SDS tools. Cloud-native platforms rely heavily on SDS for scalability and agility. Service providers adopt open-source frameworks like Ceph or GlusterFS to optimize TCO. Enterprises gain efficiency through data lifecycle policies and orchestration. The market is moving toward infrastructure-as-code in storage design.

Sustainability-Driven Storage Systems Using Energy-Efficient Hardware and Cooling Technologies

Taiwan’s data center operators focus on building green-certified infrastructure using energy-efficient systems. Storage devices with reduced power consumption, such as SSDs and hybrid flash systems, are prioritized. Organizations aim to lower their data center PUE (Power Usage Effectiveness) through advanced storage density. Circular economy practices like component reuse and recycling of drives gain traction. Cold storage strategies for archival workloads help reduce energy needs. The Taiwan Data Center Storage Market shows rising demand for heat-resistant, sealed HDDs and low-power tape libraries. Vendors integrate smart power control and automated sleep modes into storage systems. It ensures compliance with national carbon targets and ESG commitments.

Edge Storage Nodes Deployed for Smart Cities and 5G-Backed Infrastructure Projects

Edge computing is gaining traction in Taiwan, driven by 5G rollout and smart city programs. Storage systems are being placed closer to data sources like traffic cameras, sensors, and local analytics nodes. These deployments need rugged, compact, and autonomous systems with local failover capacity. Public projects in mobility, public safety, and urban IoT push edge storage demand. AI-powered surveillance and traffic analytics require real-time data caching at the edge. The Taiwan Data Center Storage Market adapts through micro data centers and containerized storage solutions. These support intermittent connectivity and allow seamless sync with core facilities. It enables faster decision-making in latency-sensitive environments.

Growth of AI-Centric Workloads Requiring Specialized High-Performance Storage Solutions

AI workloads, particularly in healthcare, robotics, and financial modeling, require high-throughput storage systems. Demand is growing for all-flash arrays with support for massive concurrency. NVMe interfaces, GPU memory hierarchies, and distributed storage backbones dominate deployment roadmaps. Taiwan’s research institutions and medical centers use these systems for genome sequencing, fraud analytics, and autonomous systems. AI-as-a-service offerings by local cloud firms drive need for scalable backend storage. The Taiwan Data Center Storage Market meets this demand with AI-ready architectures. Vendors provide tunable IOPS, data striping, and error-correction logic as key features. It enables complex inferencing, large-scale simulation, and secure model storage.

Market Challenges

Seismic Risk, Power Reliability, and Land Constraints Hindering High-Capacity Data Center Deployment

Taiwan’s geography introduces operational risks for hyperscale data center planning. Earthquake-prone zones increase the cost and complexity of resilient storage infrastructure. Facilities need anti-vibration systems, multi-zone replication, and hardened enclosures. Urban density in Taipei and limited land availability pose barriers to expansion. Developers face difficulties in securing power and water in high-demand districts. High costs of Tier IV certification and strict compliance increase CAPEX for new entrants. These issues impact ROI on large storage deployments. The Taiwan Data Center Storage Market must balance infrastructure resilience with cost optimization.

Talent Shortage and Dependence on Imports Affecting Storage System Integration and Support

The market faces skill shortages in cloud-native storage architecture and SDS platforms. Enterprises struggle to find local talent skilled in Kubernetes storage orchestration or data fabric management. Taiwan relies on imported storage hardware and software from the U.S., Japan, and Europe. Currency fluctuations and trade policies affect pricing stability. Long lead times for specialized storage components disrupt project schedules. Support services are often delayed due to limited local representation of global vendors. The Taiwan Data Center Storage Market needs more localized training, integration hubs, and partner ecosystems. Without these, growth may face delays in deployment and maintenance cycles.

Market Opportunities

High Demand for Digital Twin, Smart Manufacturing, and AI Training Accelerates Enterprise Storage Need

Smart manufacturing and digital twin solutions present strong opportunities for advanced storage deployments. These workloads require real-time ingestion, retrieval, and multi-format data handling. Enterprises seek scalable infrastructure that supports predictive modeling and analytics. The Taiwan Data Center Storage Market can grow by enabling industry-grade storage resilience and speed.

Strong Potential in Colocation, Edge, and Compliance-Based Storage Platforms

Edge deployments for surveillance, logistics, and fintech applications present a high-growth segment. Demand is also rising for compliant storage platforms for regulated industries. The Taiwan Data Center Storage Market benefits from tailored solutions with encryption, isolation, and redundancy built in. Growth opportunities exist in modular, low-latency systems optimized for urban and suburban zones.

Market Segmentation

By Storage Type

Traditional storage holds a declining but notable presence due to legacy applications. However, all-flash storage leads the Taiwan Data Center Storage Market in performance-intensive segments such as AI and fintech. Hybrid storage gains traction among mid-size enterprises looking for cost-to-performance balance. Other storage types like object storage continue expanding in cloud-native setups due to scalability.

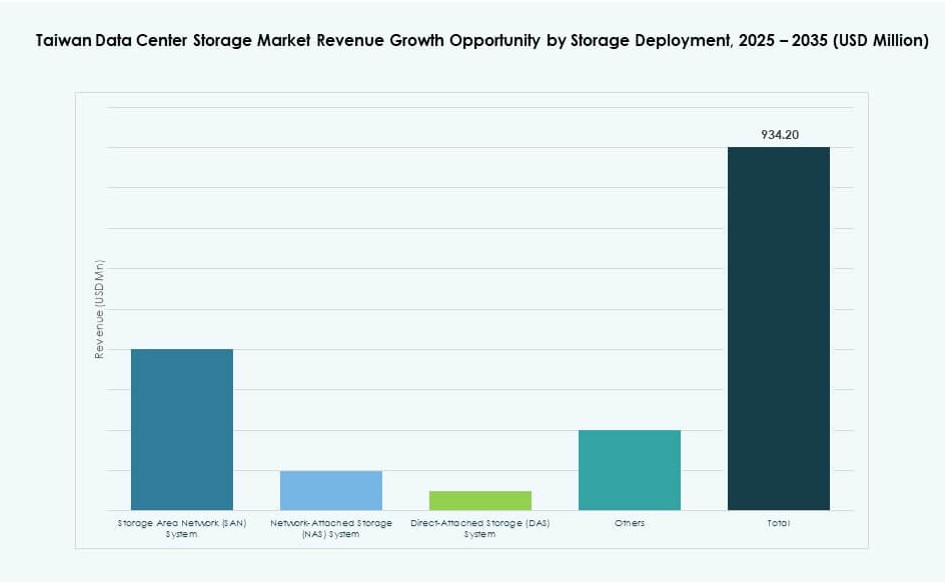

By Storage Deployment

Storage Area Network (SAN) systems dominate high-speed compute environments, particularly in financial institutions and government agencies. Network-attached Storage (NAS) is widely used for content-heavy operations like media and education. Direct-attached Storage (DAS) remains relevant for SMBs and edge deployments. Other advanced models like hyperconverged storage are gaining traction across hybrid cloud use cases.

By Component

Hardware leads the segment, driven by investments in SSDs, controllers, and backup systems. Software, however, is growing faster due to the rise of SDS and data orchestration platforms. Enterprises require integrated monitoring, access control, and data lifecycle tools. The Taiwan Data Center Storage Market is seeing bundling of hardware-software packages across mid- to large-scale deployments.

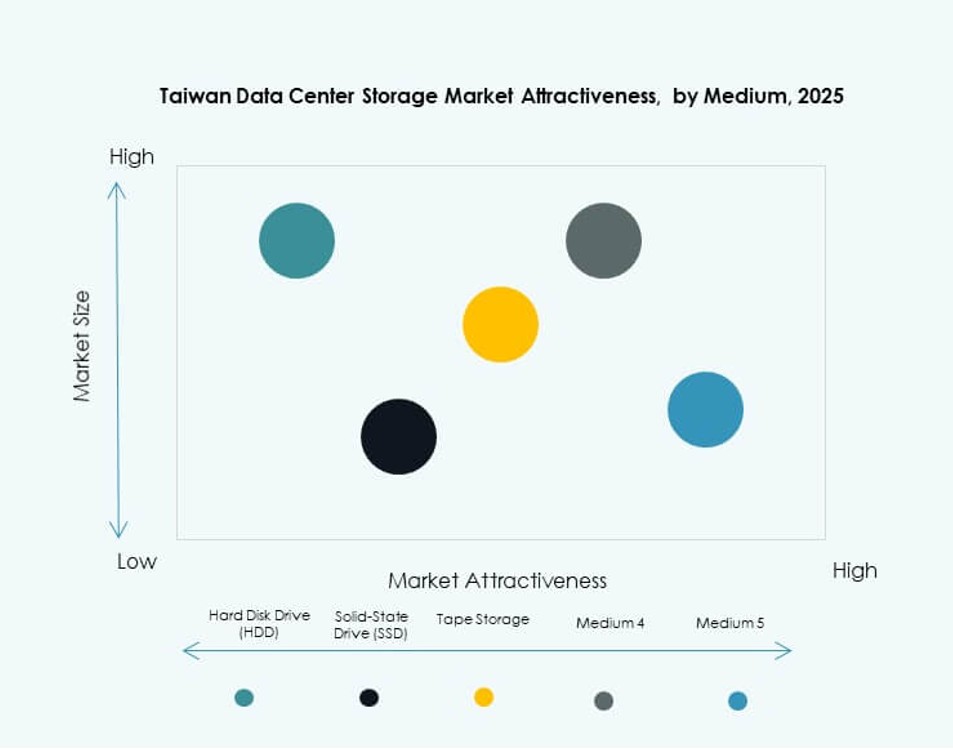

By Medium

Solid-State Drives (SSD) dominate in performance-oriented environments, including AI, analytics, and VDI. Hard Disk Drives (HDD) still command volume in backup and cold storage applications. Tape storage is used selectively in long-term archival systems and government repositories. The shift toward SSD is clear in latency-sensitive workloads across urban data centers.

By Deployment Model

Cloud-based storage models are rising fast due to demand for elasticity and remote access. On-premises deployments continue to lead in sectors with compliance needs like healthcare and government. Hybrid deployments are increasing in popularity due to flexibility in cost and control. The Taiwan Data Center Storage Market is leaning toward hybrid models as default enterprise architecture.

By Application

IT and telecom sectors dominate storage demand, driven by SaaS, content delivery, and cloud backup. BFSI uses high-performance storage for real-time transactions and compliance logging. Government bodies demand secure, redundant systems for public cloud initiatives. Healthcare and others use scalable storage for imaging, diagnostics, and digital records. The Taiwan Data Center Storage Market sees rising vertical-specific customization.

Regional Insights

Taipei Metropolitan Region Leading with 42% Share Driven by Hyperscale and Cloud Deployments

Taipei remains the dominant region for data center storage, capturing 42% of the Taiwan Data Center Storage Market. Strong fiber connectivity, colocation hubs, and government offices support this dominance. Major telecom and cloud vendors anchor their operations here. The area has dense urban infrastructure, stable power, and mature IT ecosystems. Enterprise data centers and AI labs also prefer Taipei due to talent availability. Demand for premium storage with low latency is highest in this zone.

- For instance, Google opened its largest AI infrastructure hardware engineering centre outside the U.S. in Taipei, employing hundreds of engineers to develop AI and cloud hardware technologies for deployment across its global data center network.

Taoyuan and Hsinchu Emerging with Combined 33% Market Share Through Industrial and Research Expansion

Taoyuan and Hsinchu together hold 33% of the market, supported by tech manufacturing and R&D zones. Hsinchu Science Park drives edge deployments for chip design and industrial simulation. Taoyuan supports smart logistics, AI training, and backup storage nodes. Both zones benefit from growing real estate availability and renewable power integration. These regions attract hyperscale projects and government cloud platforms. They are evolving into secondary data center corridors.

- For instance, Hsinchu Science Park hosts over 500 high‑tech firms and more than 170,000 employees in computing and semiconductor industries, providing a strong technology ecosystem that attracts support services including enterprise IT and storage infrastructure around the region.

Taichung and Southern Taiwan Capturing 25% Share from Enterprise and Edge Use Cases

Taichung and cities in southern Taiwan account for the remaining 25% share. These areas support local enterprise storage, disaster recovery zones, and industrial IoT edge deployments. Taichung’s industrial base and availability of land make it ideal for modular data centers. Southern zones see growing demand from logistics, healthcare, and regional government offices. Connectivity projects aim to improve their viability as future data center nodes. The Taiwan Data Center Storage Market diversifies its footprint through these emerging clusters.

Competitive Insights:

- Quanta Cloud Technology

- Wiwynn

- Inventec

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- NetApp

- IBM Corporation

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Micron Technology, Inc.

The Taiwan Data Center Storage Market features a mix of global and domestic players competing across hardware, software, and hybrid storage platforms. Quanta, Wiwynn, and Inventec hold strong local advantage through integrated server-storage solutions tailored for hyperscale and ODM segments. Global leaders like Dell Technologies, HPE, and IBM provide advanced storage arrays and hybrid cloud offerings. Companies such as NetApp and Cisco focus on data fabric and edge storage capabilities. Huawei and Micron support regional cloud and memory demands with AI-optimized solutions. The market reflects a technology-driven rivalry, with innovation in flash, NVMe, SDS, and power-efficient systems driving competition. It continues to shift toward vendor partnerships, colocation service integration, and multi-tenant orchestration platforms.

Recent Developments:

- In October 2025, Quanta Cloud Technology announced a strategic collaboration with networking software company Arrcus to deliver AI‑optimized rack solutions that bundle high‑bandwidth switching with QCT’s rack‑level systems for next‑generation data centers, targeting workloads such as AI and cloud that drive high‑performance compute and storage demand in markets including Taiwan.

- In October 2025, Quantum Corporation entered a strategic partnership with Entanglement to develop post‑quantum encrypted, regionalized data protection capabilities, a move aimed at enhancing secure data storage and backup offerings for data centers and enterprises, including those in Asia‑Pacific regions such as Taiwan that must comply with tightening data‑sovereignty and security requirements.

- In May 2025, Wiwynn showcased next‑generation AI servers and advanced direct liquid cooling solutions at Computex 2025 in Taipei, positioning these high‑density systems as infrastructure for modern and legacy data centers and explicitly highlighting applications that include AI workloads and associated storage expansion for cloud and hyperscale operators.