Executive summary:

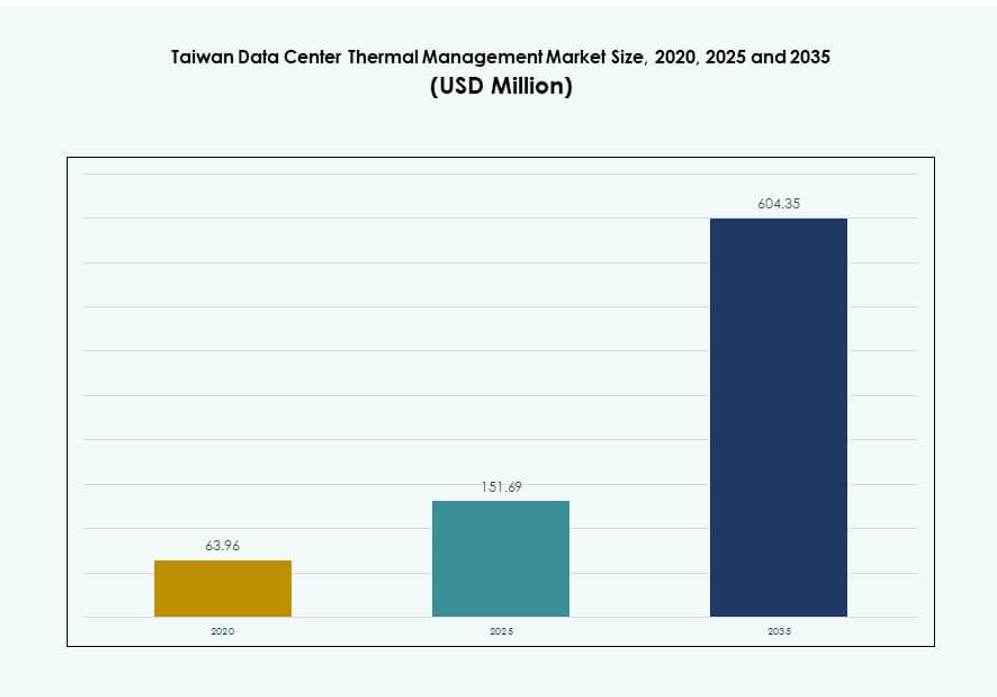

The Taiwan Data Center Thermal Management Market size was valued at USD 63.96 million in 2020 to USD 151.69 million in 2025 and is anticipated to reach USD 604.35 million by 2035, at a CAGR of 14.72% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Taiwan Data Center Thermal Management Market Size 2025 |

USD 151.69 Million |

| Taiwan Data Center Thermal Netherlands Market, CAGR |

14.72% |

| Taiwan Data Center Thermal Management Market Size 2035 |

USD 604.35 Million |

The market is growing due to rising AI workloads, high-density GPU servers, and demand for liquid cooling. Colocation and hyperscale operators are shifting from traditional air-based systems to hybrid and direct-to-chip setups. Companies focus on energy savings, automation, and predictive controls to manage thermal loads efficiently. Government incentives, sustainability mandates, and edge expansion drive further innovation. Strategic investments are helping Taiwan emerge as a thermal technology hub in Asia. Vendors are competing by offering modular and scalable cooling infrastructure. These developments create strong long-term value for investors and infrastructure builders.

Northern Taiwan leads the market due to dense hyperscale activity in Taipei, Hsinchu, and Taoyuan. These cities benefit from proximity to tech clusters, grid reliability, and skilled labor. Central Taiwan is growing with smart manufacturing zones and edge deployments in Taichung. Southern Taiwan is emerging, supported by smart city programs and telecom sites in Kaohsiung and Tainan. Each subregion reflects varied cooling needs shaped by compute density and available space.

Market Dynamics:

Market Drivers

Growing AI, GPU, and High-Density Workload Deployments Necessitate Advanced Thermal Management Systems

Taiwan’s rapid growth in AI and machine learning workloads demands more powerful servers, increasing heat output in data centers. These GPU-intensive environments need high-efficiency thermal management to maintain performance and prevent failure. Traditional air-based systems cannot support rack densities exceeding 30kW, pushing operators toward liquid cooling and hybrid solutions. Hyperscale and enterprise operators prioritize energy efficiency and cooling scalability to reduce operational costs. Strategic investments in AI infrastructure are reinforcing demand for thermal innovations. The Taiwan Data Center Thermal Management Market supports these shifts with purpose-built solutions. Equipment upgrades align with rising sustainability requirements. Companies seek energy savings, uptime protection, and future-ready cooling systems to remain competitive.

- For instance, Delta Electronics has deployed direct‑to‑chip liquid cooling systems in Taiwan capable of supporting rack densities above 80 kW for AI server clusters.

Rising Demand for Sustainable Infrastructure Drives Liquid and Hybrid Cooling Adoption

Taiwan’s government and data center industry are aligning with ESG frameworks that emphasize energy and water efficiency. Thermal management systems play a central role in sustainability strategies, especially in dense urban campuses. Liquid cooling systems offer better energy performance, lower water usage, and a smaller environmental footprint. Vendors are launching solutions that combine air and liquid systems, enabling phased upgrades for existing data centers. These developments support carbon neutrality targets for colocation and hyperscale facilities. Enterprises seek green certifications such as LEED and ISO 50001, influencing procurement decisions. The Taiwan Data Center Thermal Management Market addresses these needs with integrated, efficient systems. Energy credits and utility partnerships also incentivize upgrades.

Rising Edge and Micro Data Center Growth Fuel Regional Thermal Management Demand

Smart manufacturing, digital healthcare, and real-time analytics are expanding edge data center deployment across Taiwan. These smaller facilities often operate in limited-space environments, intensifying thermal challenges. Liquid cooling and modular cooling systems ensure high-density performance within space and power constraints. Thermal reliability becomes essential for telecom, surveillance, and autonomous vehicle infrastructure. Vendors develop compact thermal systems optimized for micro and edge sites. This growing edge footprint expands the Taiwan Data Center Thermal Management Market’s scope beyond urban core facilities. Integration with remote monitoring and AI-based controls enhances reliability. Businesses and investors recognize edge growth as a new cooling demand frontier.

Increased Hyperscale and Colocation Investments Accelerate Hardware and Software Cooling Innovation

Leading cloud and colocation providers continue to scale infrastructure in northern Taiwan. Hyperscale builds drive strong demand for efficient chillers, CRAH/CRAC units, and BMS-linked airflow systems. These large-scale campuses use AI tools for predictive thermal controls, enabling smarter resource management. Hardware cooling is complemented by software-defined energy optimization. New builds are designed for 100kW+ rack support and seamless integration of immersion and direct-to-chip cooling. The Taiwan Data Center Thermal Management Market benefits from global vendors entering partnerships with local players. These collaborations accelerate innovation and localization of advanced thermal systems. Investors view such developments as strong indicators of long-term digital infrastructure growth.

- For instance, Johnson Controls deployed Silent‑Aire cooling systems with integrated controls in hyperscale facilities supporting AI racks above 100 kW, improving thermal stability and response time under fluctuating loads.

Market Trends

Adoption of AI-Based Thermal Management Software and Intelligent Control Systems

Taiwan’s operators are deploying AI-based software to monitor, predict, and optimize thermal loads. These systems learn from historical data to preemptively adjust airflow and coolant distribution. DCIM platforms now integrate thermal analytics and visualization for real-time control. AI-based thermal engines reduce fan speed variation and manage hot spot formation, cutting energy use. Predictive maintenance reduces downtime and improves lifespan of cooling equipment. The Taiwan Data Center Thermal Management Market is seeing growth in intelligent BMS modules and AI-led simulation tools. Software automation helps meet rising SLA expectations. Vendors promote AI optimization for future-proof thermal management across enterprise and colocation spaces.

Design for Liquid Cooling Readiness Becomes a Standard in New Data Center Builds

Taiwan’s new data centers are increasingly being designed with infrastructure that supports liquid cooling from day one. Builders install rear-door heat exchangers, CDU loops, and direct-to-chip compatibility in anticipation of AI and HPC deployments. Though many sites still operate air-based systems, structural readiness allows seamless transition. Thermal vendors co-develop cooling plans with IT teams during design phases. Data centers in Hsinchu and Taoyuan are implementing hybrid-ready architecture to improve asset longevity. The Taiwan Data Center Thermal Management Market sees demand shift from retrofits to future-proof builds. Design readiness minimizes future disruption and accelerates deployment timelines. This trend reshapes thermal planning across hyperscale and colocation projects.

Integration of Sustainability Metrics and Energy Benchmarking in Cooling Procurement

Enterprises and colocation providers in Taiwan now evaluate cooling systems using PUE, WUE, and other sustainability indicators. Thermal systems must demonstrate energy and water savings over full operational life. Procurement teams favor vendors offering transparent metrics and compliance with global benchmarks. Certifications such as ISO 14001 and LEED now influence vendor selection. Governments promote these practices with incentives tied to environmental performance. The Taiwan Data Center Thermal Management Market is adjusting with greener refrigerants, waterless cooling, and solar-integrated chillers. Buyers expect full lifecycle analysis and ROI from energy savings. Vendors that deliver quantifiable impact on emissions gain competitive edge.

Cross-Border Partnerships Accelerate Technology Transfer and System Localization

Taiwan’s data center market is attracting international thermal technology vendors through joint ventures and OEM deals. These collaborations improve access to advanced systems like immersion cooling and modular chillers. Local manufacturers adapt imported solutions for Taiwan’s climate and grid conditions. Thermal partnerships reduce procurement costs, shorten lead times, and support knowledge exchange. Localization ensures compliance with local regulations and grid constraints. The Taiwan Data Center Thermal Management Market benefits from these regional synergies. Global firms gain foothold, while local integrators scale deployment faster. These ties help Taiwan stay aligned with global thermal technology standards.

Market Challenges

Infrastructure Constraints and Limited Access to Renewable Energy for Sustainable Cooling

Taiwan’s data centers often operate in dense urban environments where grid constraints limit cooling flexibility. High power tariffs and limited renewable energy supply affect cost-efficiency of thermal systems. Data centers competing for electricity must balance thermal needs with IT performance and uptime. Water-based systems face opposition in areas with seasonal droughts or infrastructure gaps. Space limitations in existing facilities challenge large cooling unit retrofits. The Taiwan Data Center Thermal Management Market must overcome these physical constraints with compact, modular, and energy-flexible solutions. Government incentives for green infrastructure remain in early stages. These hurdles increase operational complexity for thermal planners.

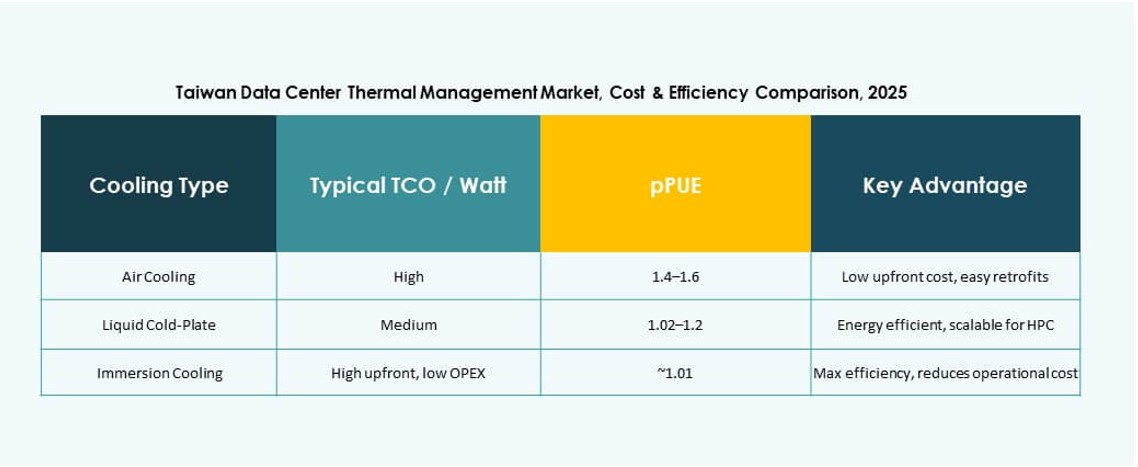

High Capital Costs and Uncertain ROI for Next-Generation Liquid Cooling Systems

While immersion and direct-to-chip cooling offer performance gains, their high upfront cost deters widespread adoption. Enterprises with limited budgets hesitate to replace functional air-based systems. Liquid cooling installations require plumbing, CDUs, and specialized maintenance, which increases project costs. Operators question the payback timeline, especially in mid-size and edge sites. Training requirements and limited expertise also slow integration. The Taiwan Data Center Thermal Management Market must address ROI clarity and lifecycle cost transparency. Vendors offering service-based models or leasing options see better traction. Long-term savings remain compelling, but short-term budgets limit speed of adoption.

Market Opportunities

Expansion of Edge, AI, and Smart Manufacturing Sites Across Taiwan’s Southern and Central Regions

Smart factories and edge computing nodes are proliferating across Taichung, Tainan, and Kaohsiung. These deployments require efficient and compact thermal systems for high-density racks. Vendors can target modular liquid and hybrid solutions suited for tight environments. The Taiwan Data Center Thermal Management Market supports this growth with scalable units, especially for telecom and healthcare edge sites. These zones offer greenfield opportunity for vendors to supply future-ready cooling.

Emergence of AI-Optimized Thermal Software and Retrofit Demand in Urban Data Centers

Data centers in Taipei and New Taipei face rising thermal loads without expansion room. AI-based retrofits improve airflow, reduce PUE, and extend hardware life. Software vendors can deploy plug-in modules for existing BMS platforms. The Taiwan Data Center Thermal Management Market is opening up service-led opportunities through upgrades and predictive analytics. These offerings address thermal needs without major infrastructure changes.

Market Segmentation

By Data Center Size

Large data centers dominate the Taiwan Data Center Thermal Management Market due to hyperscale and colocation builds. These facilities require robust, multi-layered cooling systems to support high-density racks. Small and medium centers follow, serving edge computing and enterprise needs. Demand for scalable cooling is growing across all size categories. Large facilities benefit from economies of scale and full-system integration, driving their share upward.

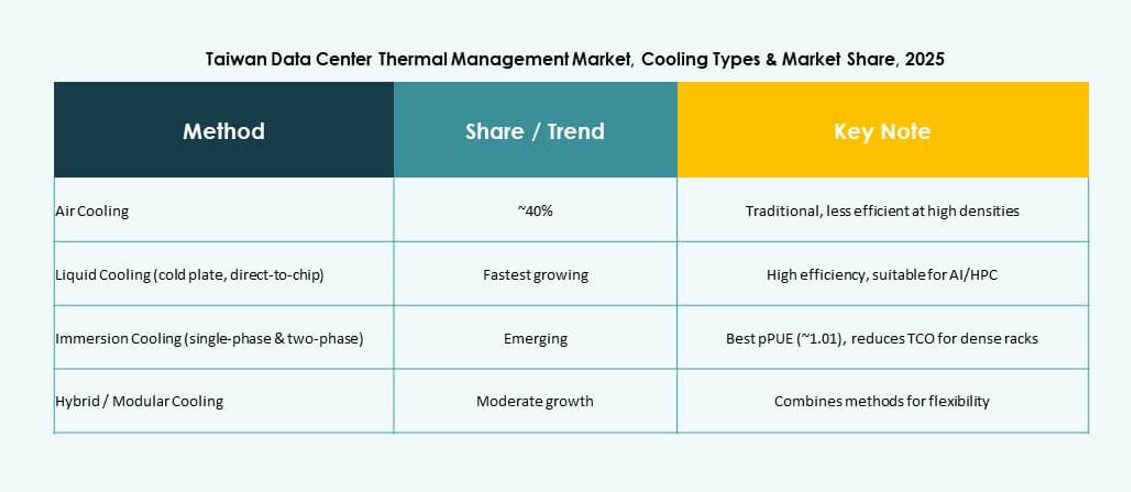

By Cooling Technology

Air-based cooling continues to hold a major share, with hot/cold aisle and direct air systems widely adopted. However, liquid-based technologies like direct-to-chip and immersion are gaining ground. Hybrid solutions are preferred in new builds that plan for gradual migration. The Taiwan Data Center Thermal Management Market sees a growing shift toward high-efficiency hybrid setups. Phase-change and thermoelectric methods remain niche but attract R&D focus.

By Component

Hardware remains the largest component segment, driven by demand for chillers, fans, and heat exchangers. Software is rising fast due to AI-based optimization and energy control modules. Services including retrofits and remote monitoring add value in operational efficiency. The Taiwan Data Center Thermal Management Market integrates these components across lifecycle stages. Full-stack thermal packages are favored by hyperscale buyers.

By Hardware

Cooling units and chillers account for the largest hardware revenue due to their use in all thermal systems. Heat exchangers and airflow devices follow, supporting airflow dynamics and liquid transfer. Piping and distribution infrastructure grows with liquid cooling adoption. The Taiwan Data Center Thermal Management Market reflects demand across core and edge deployments. Vendors focus on reliability and modular scalability in hardware supply.

By Software

DCIM dashboards lead the software segment, helping monitor energy use and thermal efficiency. AI optimization tools are rapidly gaining share due to their ROI and energy-saving potential. CFD simulations and BMS modules help in advanced thermal modeling and real-time control. The Taiwan Data Center Thermal Management Market emphasizes predictive thermal tools in high-density environments. Software integration supports uptime and cost reduction.

By Services

Installation and preventive maintenance are dominant, especially for large-scale deployments. Retrofit and monitoring-as-a-service models are expanding among enterprise and edge facilities. Vendors offer full-service contracts including upgrades, audits, and optimization. The Taiwan Data Center Thermal Management Market sees services driving long-term performance. Comprehensive support packages enhance adoption of advanced cooling systems.

By Data Center Type

Hyperscale data centers lead the market, driven by cloud growth and AI computing loads. Colocation and cloud facilities follow due to tenant-driven demand for efficient cooling. Enterprise and edge centers expand thermal needs in industrial and telecom sectors. The Taiwan Data Center Thermal Management Market is diversifying by facility type. Thermal solutions cater to workload-specific and spatial needs.

By Structure

Room-based systems remain widely used in older and mid-scale data centers. Rack- and row-based systems are gaining traction for density control and modular builds. Row-based systems support airflow optimization and targeted cooling. The Taiwan Data Center Thermal Management Market is gradually shifting toward rack and row formats. Structural design influences cooling configuration and retrofitting flexibility.

Regional Insights

Northern Taiwan Leads with Over 55% Market Share Due to Hyperscale Concentration

Taipei, Taoyuan, and Hsinchu dominate the Taiwan Data Center Thermal Management Market with over 55% share. These regions house hyperscale, cloud, and semiconductor-related data center investments. Operators focus on high-density cooling for AI workloads and 5G infrastructure. Proximity to talent, tech zones, and grid capacity supports thermal innovation. Northern Taiwan continues to attract global vendors and investors in data infrastructure.

- For instance, in June 2025, Delta Electronics launched a direct-to-chip liquid cooling line in Taoyuan aimed at hyperscale deployments exceeding 80kW rack densities.

Central Taiwan Holds Around 25% Share, Driven by Industrial and Edge Deployments

Taichung and surrounding regions account for roughly 25% of the thermal market. Smart manufacturing and industrial digitalization increase demand for edge and enterprise cooling. Central Taiwan’s industrial clusters host micro data centers that need compact cooling solutions. Vendors deploy modular systems with energy-efficient airflow units. Growth stems from integration of IT and OT in Industry 4.0 zones.

- For instance, Vertiv installed adaptive CRAC and CRAH units in a micro data center supporting a smart mobility project near Changhua, maintaining sub-1.3 PUE during variable workloads.

Southern Taiwan Emerges with 20% Market Share Backed by Smart Cities and Telecom Hubs

Kaohsiung and Tainan contribute nearly 20% of the Taiwan Data Center Thermal Management Market. Government-led smart city programs and regional telecom data centers fuel growth. Edge and micro facilities are common, supporting real-time applications and IoT networks. Liquid and hybrid cooling systems are gaining traction due to limited space and rising compute loads. Southern Taiwan represents strong future opportunity for thermal innovation.

Competitive Insights:

- Vertiv Group Corp.

- Schneider Electric

- Delta Electronics, Inc.

- Daikin Industries Ltd.

- Mitsubishi Electric Corporation

- NTT Facilities

- LG Electronics

- Johnson Controls International plc

- Trane Technologies plc

- Fujitsu Limited

The Taiwan Data Center Thermal Management Market features intense competition among global and regional players offering advanced hardware, software, and service-based cooling solutions. Vertiv and Schneider Electric lead with comprehensive portfolios across rack, row, and room cooling, along with AI-based thermal software. Delta Electronics leverages local manufacturing strength and custom designs for Taiwan’s hyperscale and colocation needs. Mitsubishi Electric, LG, and Daikin focus on efficient chillers and CRAC systems. NTT Facilities and Fujitsu provide integrated thermal design and facility management expertise. The market sees increasing focus on modular systems and hybrid cooling adoption. Competitive strategies center on energy savings, high-density readiness, and retrofittable systems that align with Taiwan’s edge and AI-driven infrastructure growth.

Recent Developments:

- In October 2025, Delta Electronics showcased advanced energy-saving power, cooling, and infrastructure solutions at Data Centre World Asia, including a 20-foot containerized data center with liquid-to-air coolant distribution units (CDUs) offering up to 80kW capacity and scalable power trains up to 2,400kW for AI workloads.

- In September 2025, Johnson Controls launched the Silent-Aire Coolant Distribution Unit (CDU), a scalable liquid cooling solution for high-density AI data centers, expanding its thermal management offerings from chip to chiller levels.

- In September 2025, NTT Facilities partnered with GF Piping Systems to supply pre-insulated piping for its ‘Products Engineering Hub for Data Center Cooling’ testbed in Japan, advancing sustainable direct liquid cooling technologies applicable to data centers.

- In January 2025, Daikin established a joint venture in Taiwan with Hotai Development and LEADING to produce large-sized air handling units (AHUs) tailored for semiconductor and data center applications, leveraging Daikin’s chiller expertise.