Executive summary:

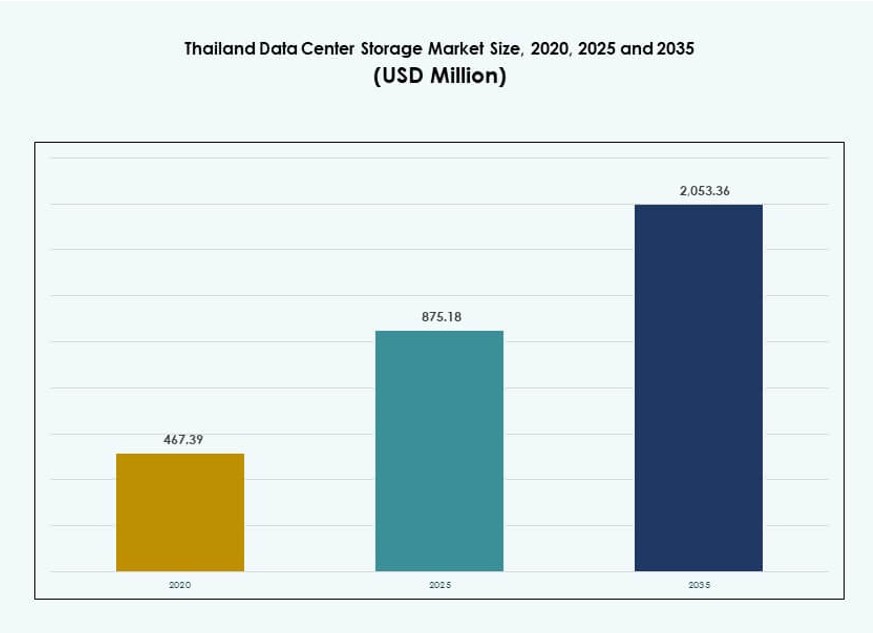

The Thailand Data Center Storage Market size was valued at USD 467.39 million in 2020 to USD 875.18 million in 2025 and is anticipated to reach USD 2,053.36 million by 2035, at a CAGR of 8.81% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Thailand Data Center Storage Market Size 2025 |

USD 875.18 Million |

| Thailand Data Center Storage Market, CAGR |

8.81% |

| Thailand Data Center Storage Market Size 2035 |

USD 2,053.36 Million |

Strong cloud adoption, digital-first enterprise models, and growing data generation are pushing demand for reliable storage infrastructure. Sectors like telecom, BFSI, and public services are upgrading to software-defined and high-performance storage. Investments in AI, edge computing, and hybrid environments are reshaping storage strategies. The market plays a vital role in enabling service agility, data protection, and operational continuity. Vendors focusing on automation and energy-efficient platforms gain significant traction in this environment.

The Bangkok Metropolitan Region holds the largest share due to its cloud hubs and enterprise density. The Eastern Economic Corridor is emerging with strong industrial demand and government support for digital infrastructure. Northern and Southern Thailand are gradually expanding, with edge deployments and smart city projects. These regions are supported by fiber connectivity, localized data policies, and growing cloud-native application adoption. Regional diversity enhances overall market resilience and reach.

Market Dynamics:

Market Drivers

Digital Transformation Across Sectors Drives Enterprise Storage Infrastructure Demand

Enterprises across Thailand are transitioning to digital-first models, which demands scalable and secure storage infrastructure. Sectors such as banking, government, healthcare, and retail are generating high volumes of unstructured data. This shift accelerates the need for faster processing, real-time analytics, and robust storage capabilities. The Thailand Data Center Storage Market supports this transition by offering flexible, high-performance storage systems. It is critical for business continuity, regulatory compliance, and digital competitiveness. Local firms invest in private cloud environments to control costs and improve data security. Storage upgrades remain key to enabling enterprise mobility and digital identity services. Government-led smart initiatives also rely heavily on advanced data infrastructure. Investors recognize the strategic value of scalable storage systems in this fast-evolving digital landscape.

- For instance, Siam Commercial Bank migrated its data lake to Microsoft Azure Thailand Region to improve scalability and manage unstructured data, enabling advanced analytics on over 12 million ATM transactions. This supported enhanced ATM performance and optimized storage efficiency.

Expansion of Cloud Adoption Accelerates Need for Scalable Storage Systems

Thailand’s rising cloud adoption, led by both public and hybrid models, pushes demand for advanced storage technologies. Cloud providers, including AWS and Huawei Cloud, are enhancing in-country availability zones, enabling data localization. Enterprises migrating workloads to cloud require storage that supports high availability and data redundancy. It gives rise to tiered storage strategies for balancing cost and performance. The Thailand Data Center Storage Market supports this evolution by integrating cloud-native and software-defined storage platforms. It enables seamless scaling, centralized management, and operational efficiency. This shift allows faster deployment of services such as virtual desktops and disaster recovery. Managed storage solutions see rising interest among SMEs seeking simplicity and cost control. The market gains strategic relevance as cloud-native transformation accelerates.

Smart City Projects and E-Governance Fuel Edge Storage and Data Centralization

The government’s push for smart city initiatives and digital public services demands robust backend infrastructure. National projects such as Thailand 4.0 and Digital ID systems drive multi-source data generation. These require secure and high-speed storage environments with regional accessibility. Edge storage becomes critical in cities like Phuket, Chiang Mai, and Bangkok to ensure low-latency access. Centralized data lakes improve analytics and decision-making for public service optimization. The Thailand Data Center Storage Market facilitates this integration of edge and core infrastructure. It enables dynamic data migration, security compliance, and workload flexibility. Multisector collaboration on digital infrastructure boosts the case for sustainable and intelligent storage models. These initiatives create opportunities for colocation providers and hardware vendors.

- For instance, the Phuket Smart City initiative, led by Thailand’s Digital Economy Promotion Agency, deployed sensor and video surveillance systems for traffic, tourism, and safety analytics. These systems rely on centralized government data platforms to store and process multi-agency data under the Thailand 4.0 strategy.

Rising AI, IoT, and Video Analytics Adoption Spurs Need for High-Performance Storage

Use cases like AI model training, IoT telemetry, and surveillance analytics demand low-latency, high-throughput storage solutions. Enterprises require systems that can process petabytes of data across edge, core, and cloud environments. NVMe-based flash storage, parallel file systems, and intelligent caching are gaining prominence. The Thailand Data Center Storage Market enables these applications by offering performance-optimized architectures. It supports real-time inference, content delivery, and device telemetry across urban and industrial zones. AI adoption in finance, logistics, and agriculture adds pressure to upgrade legacy storage setups. Industry players seek agile systems that support containerized environments and GPU workloads. These technical drivers elevate storage from a support system to a business-critical enabler.

Market Trends

Shift Toward Software-Defined Storage Platforms Across Enterprise and Cloud Environments

Organizations are increasingly deploying software-defined storage (SDS) to separate hardware from storage services. This trend enables cost reduction, centralized management, and improved scalability for hybrid IT models. SDS also supports integration with virtualization tools and orchestration platforms. The Thailand Data Center Storage Market sees strong uptake of SDS among telecom, BFSI, and managed service providers. It improves infrastructure agility by supporting multicloud and workload mobility. Vendors offer SDS packages that include deduplication, snapshotting, and replication features. This trend reshapes procurement from hardware-focused to subscription-based models. It aligns well with cloud-first and automation-led strategies in enterprise IT roadmaps. Investment shifts from CapEx-heavy legacy systems to OpEx-optimized storage models.

Growing Interest in Green Storage Infrastructure and Energy-Efficient Solutions

Energy efficiency is becoming a major buying factor for storage infrastructure in Thailand. Enterprises seek to reduce power consumption and thermal output while maintaining performance. This fuels demand for solid-state drives (SSDs), advanced cooling systems, and intelligent energy management. The Thailand Data Center Storage Market reflects this shift as colocation providers adopt green building certifications and power-efficient hardware. Vendors launch storage systems with power-saving modes and predictive maintenance to extend lifespan. Renewable-powered data centers also seek storage with reduced carbon footprint. This trend supports ESG compliance and corporate sustainability goals. Storage planning now includes lifecycle cost analysis and environmental benchmarking. It influences both procurement decisions and infrastructure design.

Integration of AI-Driven Storage Management and Predictive Analytics Capabilities

Storage platforms now embed AI-based monitoring tools for predictive capacity planning and performance optimization. These systems identify bottlenecks, automate tiering, and prevent hardware failures. The Thailand Data Center Storage Market benefits from AI-based insights for large-scale deployments across government and telecom sectors. AI-powered analytics also enhance cybersecurity by detecting abnormal patterns and enabling quick recovery. Vendors bundle AI engines with storage software for real-time intelligence. This trend reduces admin workload and improves uptime metrics. Enterprises deploy these features to support mission-critical applications without compromising performance. It reinforces a shift toward self-healing, autonomous storage environments. Integration with AI workflows makes storage an active part of decision intelligence.

Rising Deployment of Hyperconverged Infrastructure with Integrated Storage Functions

Hyperconverged infrastructure (HCI) is gaining traction for its ability to unify compute, storage, and networking in one appliance. It streamlines operations and simplifies deployment in edge and branch office environments. The Thailand Data Center Storage Market supports this trend by offering HCI-based solutions for BFSI, retail, and education sectors. HCI allows flexible scaling, centralized control, and faster provisioning of resources. Storage in HCI setups benefits from redundancy, deduplication, and compression. Organizations implement HCI for disaster recovery, virtual desktop infrastructure, and private cloud. Vendors such as Nutanix and Dell EMC drive market adoption through preconfigured systems. This trend reduces IT complexity and accelerates digital transformation timelines.

Market Challenges

High Capital Costs and Technology Fragmentation Limit Storage Modernization in Mid-Market Enterprises

Many mid-sized enterprises in Thailand face budget limitations that delay modernization of storage infrastructure. Legacy systems often remain in use due to high upfront costs for flash, NVMe, and SDS deployments. Inconsistent IT standards and fragmented technology stacks further complicate upgrades. The Thailand Data Center Storage Market experiences slow uptake in cost-sensitive verticals such as manufacturing and logistics. Firms lack in-house expertise to evaluate, integrate, and manage modern storage technologies. Vendor lock-in risks, compatibility issues, and migration complexity also hinder adoption. Limited government incentives for mid-market IT upgrades add to this hesitation. This challenge leaves segments exposed to data risks and performance bottlenecks.

Data Sovereignty Regulations and Compliance Complexity Affect Storage Architecture Decisions

Data protection laws in Thailand are becoming stricter, requiring data localization and sector-specific compliance. These rules impact how and where enterprises store personal, financial, and health-related data. Storage architecture must comply with both national and cross-border standards. The Thailand Data Center Storage Market must adapt to this environment by offering compliant and auditable systems. Multinational firms face challenges in aligning global infrastructure with local regulations. Small providers struggle to maintain data classification and retention protocols. This complexity adds legal risk and slows infrastructure planning cycles. Organizations must carefully balance performance, cost, and legal adherence in designing storage environments.

Market Opportunities

Rising Edge Data Storage Demand in Smart Cities and Industrial Zones Unlocks Growth Avenues

Thailand’s smart city projects, logistics hubs, and industrial corridors generate opportunities for edge-based storage infrastructure. Edge deployments reduce latency, enable real-time analytics, and support autonomous systems. The Thailand Data Center Storage Market benefits from this shift as providers develop micro data centers and edge appliances. Energy-efficient, ruggedized storage systems gain popularity in outdoor and industrial settings. Tailored solutions for video surveillance, traffic systems, and IoT gateways support market growth. Vendors targeting provincial cities and border zones capture new revenue streams.

Cross-Border Data Connectivity Projects and ASEAN Digital Integration Boost Regional Demand

Thailand’s role in ASEAN digital connectivity plans creates opportunities for cross-border storage solutions. High-capacity fiber and submarine cable expansions enable low-latency, high-throughput data transfers. The Thailand Data Center Storage Market aligns with this demand by supporting content delivery networks, regional SaaS providers, and cross-border e-commerce. Hybrid and multicloud storage services find growing adoption across regional enterprises. Integration with Malaysia, Vietnam, and Singapore data corridors strengthens Thailand’s positioning as a digital hub.

Market Segmentation

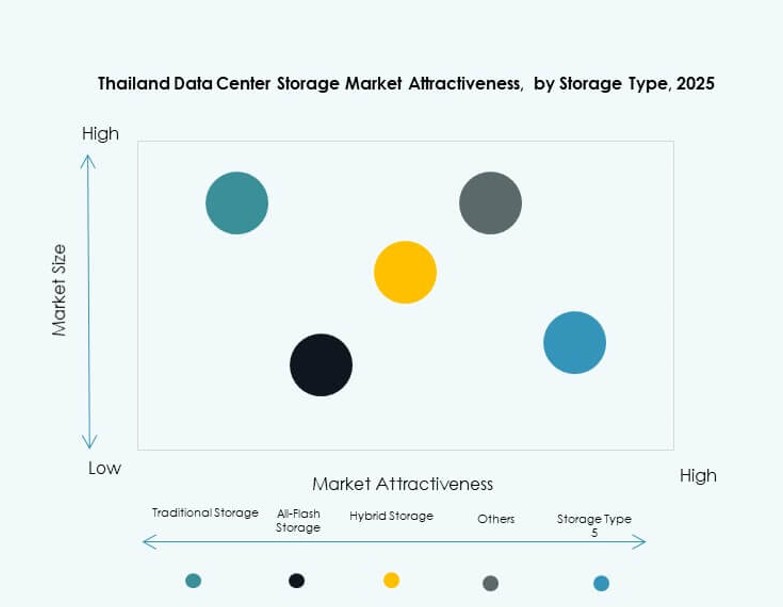

By Storage Type

Traditional storage systems currently dominate due to long-established infrastructure among telecom, banking, and government entities. However, all-flash storage is gaining share due to lower latency and higher throughput requirements in new applications. Hybrid storage solutions attract enterprises looking for a balance between cost and performance. The Thailand Data Center Storage Market sees traditional storage holding over 50% share, while all-flash is expanding quickly with AI and real-time analytics demand. Hybrid systems are popular for phased digital transitions.

By Storage Deployment

Storage Area Network (SAN) systems hold the largest share, preferred by organizations with mission-critical workloads requiring high-speed block-level storage. Network-attached storage (NAS) systems are widely used for file-sharing and collaborative platforms. Direct-attached storage (DAS) is mostly found in edge deployments or budget-constrained setups. The Thailand Data Center Storage Market favors SAN for core enterprise environments, while NAS is expanding in mid-market and educational institutions. Flexible hybrid deployments blend SAN and NAS for workload agility.

By Component

Hardware accounts for the largest share in the Thailand Data Center Storage Market, with demand for high-density racks, enclosures, and scalable servers. Storage software, while smaller in revenue, is growing faster due to rising demand for SDS, backup, deduplication, and analytics features. Software solutions enable flexibility and automation across on-premises and hybrid models. Vendors bundle management platforms with storage hardware to boost adoption. Security and data mobility features drive software investments.

By Medium

Hard Disk Drive (HDD) remains dominant for archival and high-capacity needs due to its cost-effectiveness. Solid-State Drive (SSD) adoption is rising due to faster read-write speeds, especially in performance-critical applications. Tape storage holds a niche for backup and compliance-related storage, especially in government and finance. The Thailand Data Center Storage Market sees increasing SSD deployment in AI, financial, and e-commerce workloads. Enterprises adopt tiered strategies combining SSD for speed and HDD for capacity.

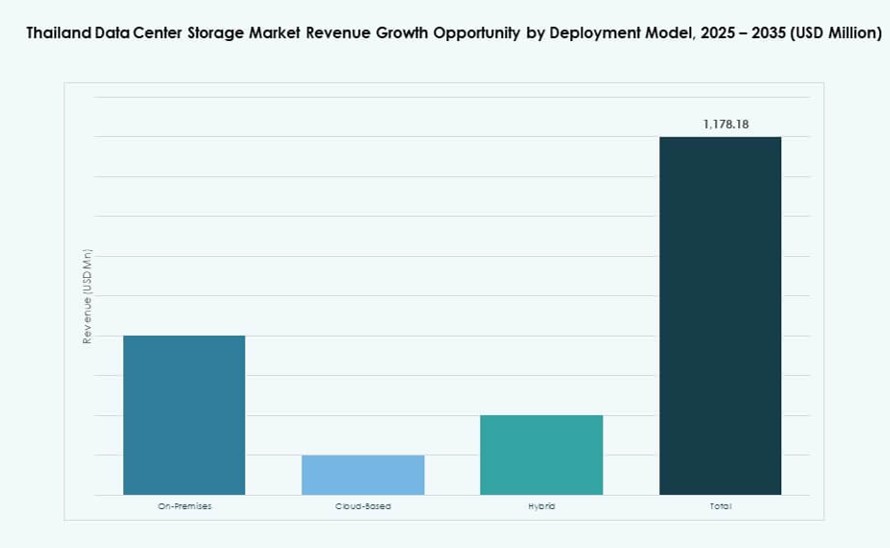

By Deployment Model

Cloud-based deployment is growing rapidly with Thailand’s cloud-first government policy and enterprise adoption of SaaS platforms. On-premises deployments remain strong in highly regulated sectors like banking and defense. Hybrid deployments are increasingly preferred for combining control with scalability. The Thailand Data Center Storage Market reflects this shift, with hybrid models gaining share through flexible architecture and improved data orchestration. Workload-specific deployment models allow cost optimization and performance tuning.

By Application

IT and Telecommunications dominate the application landscape due to large-scale data handling and service provisioning. BFSI follows closely, driven by transaction processing and regulatory compliance needs. Government sector investments in digital identity and public service systems boost demand. Healthcare and education sectors also contribute as they digitalize patient records and academic content. The Thailand Data Center Storage Market supports these varied needs with tailored storage configurations and secure management platforms.

Regional Insights

Central Thailand (Bangkok Metropolitan Region) Holds the Largest Market Share at Over 60%

Bangkok remains the country’s primary data infrastructure hub, hosting most hyperscale and colocation data centers. It accounts for over 60% of the Thailand Data Center Storage Market due to strong enterprise density and telecom backbone. This region benefits from established connectivity, cloud service availability, and digital ecosystem maturity. Storage deployment is diverse, ranging from government-grade data vaults to multi-tenant SSD clusters. Colocation providers expand capacity to serve cloud and AI workloads.

- For instance, Beijing Haoyang Cloud & Data Technology is building a 300 MW hyperscale data center at WHA Eastern Seaboard Industrial Estate 4 in Rayong province, set to begin operations around 2026. This project positions the Bangkok–Eastern Seaboard corridor as Thailand’s key hub for high-capacity compute and data storage infrastructure.

Eastern Economic Corridor (EEC) Emerges as a Strategic Secondary Storage Cluster with 20% Share

The EEC region, which includes Chonburi, Rayong, and Chachoengsao, is rising as a key location for data-intensive industries. It captures nearly 20% of the Thailand Data Center Storage Market through government incentives and infrastructure upgrades. Industrial parks, smart logistics, and tech-driven manufacturing drive demand for localized storage. Edge deployments are gaining ground to support real-time industrial control and surveillance. The region attracts investment from both local and foreign cloud providers.

- For instance, Thailand’s Board of Investment approved three major data center and cloud projects in Bangkok, Chonburi, and Rayong, totaling nearly 350 MW of IT load. The Chonburi and Rayong sites, located in the Eastern Economic Corridor, represent a significant portion of this upcoming hyperscale storage and compute capacity.

Northern and Southern Thailand Show Growing Storage Demand, Together Accounting for 15% Share

Regions such as Chiang Mai and Songkhla are seeing gradual adoption of regional data centers and cloud storage services. Together, they account for approximately 15% of the Thailand Data Center Storage Market. Growth is supported by local government digitization programs, university research initiatives, and emerging smart city pilots. Providers deploy modular and containerized data centers to serve these regions efficiently. Regional diversity in workloads pushes tailored storage models suited to localized use cases.

Competitive Insights:

- Dell Technologies

- Hewlett Packard Enterprise Development LP (HPE)

- IBM Corporation

- NetApp

- Huawei Technologies Co., Ltd.

- Cisco Systems, Inc.

- Nutanix, Inc.

- Hitachi Vantara

- True IDC

- SUPERNAP Thailand

The Thailand Data Center Storage Market features a mix of global technology vendors and regional infrastructure leaders. Dell Technologies, HPE, and IBM dominate with integrated hardware-software storage portfolios tailored for enterprise and hybrid deployments. NetApp and Hitachi Vantara serve performance-intensive workloads, while Cisco and Huawei target cloud-ready storage through network convergence. Local players such as True IDC and SUPERNAP Thailand expand edge capabilities and colocation-linked storage services. It remains competitive due to rapid tech evolution, public cloud integration, and edge storage demand. Vendors focus on NVMe solutions, software-defined platforms, and energy-efficient systems to maintain market presence. Strategic alliances and service diversification strengthen their foothold across BFSI, telecom, and government applications.

Recent Developments:

- In September 2025, Amazon Web Services expanded Amazon MSK Connect into the Thailand region, enhancing data streaming services for analytics and real‑time workloads.

- In June 2025, True IDC launched Thailand’s first AI hyperscale data center. This new facility offers over 20 MW of power capacity and advanced cooling systems tailored for high‑performance compute and storage workloads, reinforcing Thailand’s infrastructure for AI and cloud applications.

- In February 2025, Alibaba Cloud established its second data center in Thailand, expanding local capacity and product support for generative AI and industry‑specific solutions to meet rising enterprise demand.

- In January 2025, Amazon Web Services (AWS) launched the AWS Asia Pacific (Thailand) Region with three availability zones. This infrastructure supports local cloud services and enables in‑country storage under data residency requirements.