Executive summary:

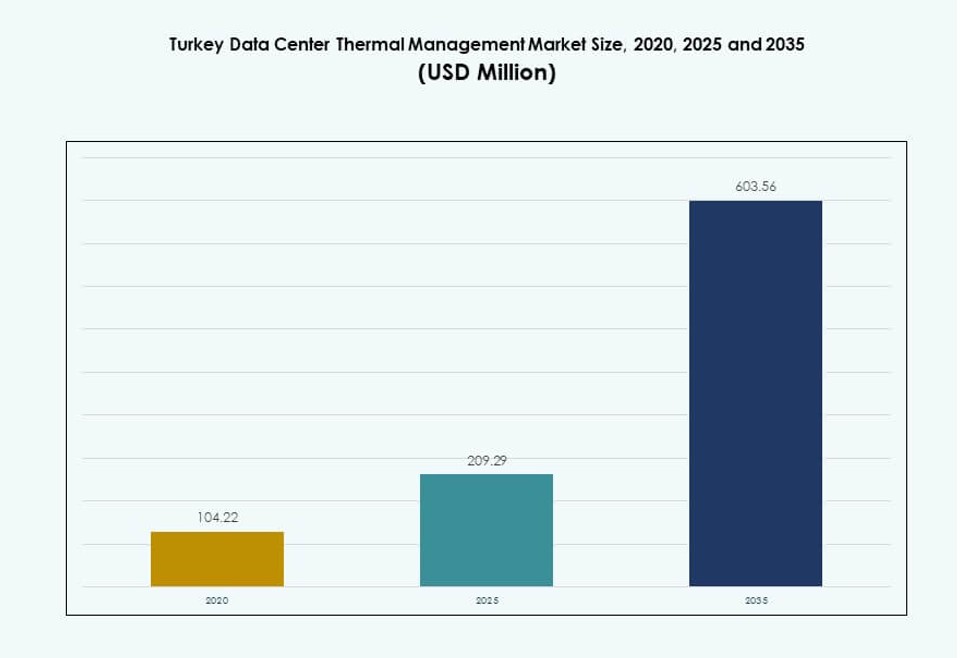

The Turkey Data Center Thermal Management Market size was valued at USD 104.22 million in 2020 to USD 209.29 million in 2025 and is anticipated to reach USD 603.56 million by 2035, at a CAGR of 11.04% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Turkey Data Center Thermal Management Market Size 2025 |

USD 209.29 Million |

| Turkey Data Center Thermal Netherlands Market, CAGR |

11.04% |

| Turkey Data Center Thermal Management Market Size 2035 |

USD 603.56 Million |

Growth in Turkey’s digital economy, along with rising data consumption and cloud demand, is driving investment in data center thermal infrastructure. Operators are adopting liquid cooling, AI-driven thermal optimization, and modular systems to manage dense computing loads. Regulatory focus on energy efficiency and sustainability also fuels the shift toward advanced cooling designs. These factors create strong strategic value for investors and businesses looking to scale secure and green data infrastructure in the region.

Istanbul leads the market due to its dense connectivity, colocation footprint, and hyperscale development pipeline. Ankara is emerging as a new hub with large-scale projects backed by telecom partnerships. Other cities like Izmir and Bursa are gaining momentum through enterprise and edge deployments. The market reflects a shift toward broader regional coverage supported by digital transformation beyond major metros.

Market Dynamics:

Market Drivers

Rising Demand for Digital Infrastructure and Hyperscale Data Center Growth

The Turkey Data Center Thermal Management Market benefits from the nation’s fast-growing digital infrastructure. Businesses shift operations to digital platforms, increasing demand for resilient data center ecosystems. Hyperscale data centers are expanding to support cloud, AI, and IoT applications. These high-density environments require efficient thermal control for uninterrupted operations. Operators seek advanced systems to maintain uptime and optimize energy usage. Government initiatives to digitalize services further push capacity buildouts. Domestic and international firms invest in greenfield developments. The growing complexity of workloads drives investment in scalable cooling infrastructure. The market plays a strategic role in enabling digital transformation across sectors.

Technological Advancements in Liquid and Hybrid Cooling Systems

Innovation drives adoption of liquid-based and hybrid thermal management solutions. Liquid cooling supports high-performance computing by removing heat from chips and GPUs more efficiently. Direct-to-chip and immersion cooling reduce energy loss and improve thermal reliability. Hybrid systems integrate air and liquid cooling for workload flexibility. These systems align with sustainability goals and allow efficient use of energy resources. Global suppliers introduce modular cooling products tailored to Turkey’s climate and rack densities. Vendors target hyperscale operators with customized thermal designs. The Turkey Data Center Thermal Management Market benefits from rising awareness of long-term operating cost reductions. Investors see value in technology-driven cooling transformation.

- For instance, CoolIT Systems expanded its direct liquid cooling portfolio in 2025, introducing solutions tested to support up to 100 kW per rack for AI and HPC workloads. These systems target high-density deployments in hyperscale and research data centers globally.

Strong Push for Energy Efficiency and Regulatory Alignment

Energy efficiency remains a central driver for thermal system upgrades in Turkish data centers. Power consumption from cooling infrastructure accounts for a large share of operational costs. Government and EU-aligned sustainability goals promote low-PUE facility design. Air-based cooling systems are enhanced with variable-speed fans and intelligent airflow control. DCIM platforms and AI analytics help balance heat loads and improve overall thermal performance. Operators focus on reducing total cost of ownership while meeting climate targets. The Turkey Data Center Thermal Management Market aligns with energy standards and performance-based building codes. Businesses prioritize compliance without sacrificing uptime or scalability.

- For instance, in April 2025, Fujitsu launched an AI-driven liquid cooling control platform in collaboration with Supermicro and Nidec, targeting high-density workloads. The system enables real-time monitoring and autonomous thermal management, with energy efficiency gains of up to 40% over traditional air-cooling methods.

Expansion of Cloud, Colocation, and Edge Facilities Across Major Cities

Data localization policies and rising cloud adoption fuel the need for scalable colocation infrastructure. Turkish cities such as Istanbul, Ankara, and Izmir host many emerging cloud and edge data centers. These facilities require compact and efficient thermal systems suited for urban environments. Small and medium data centers increasingly use rack-based and row-based cooling for flexibility. Growth in video streaming, fintech, and enterprise cloud workloads increases rack power density. This shift strengthens the business case for next-gen thermal innovations. The Turkey Data Center Thermal Management Market supports varied facility designs across the value chain. It offers investment opportunities in both metro and edge deployments.

Market Trends

Integration of AI-Powered DCIM and Predictive Thermal Monitoring Tools

Vendors integrate AI and machine learning tools with DCIM platforms to automate thermal optimization. Predictive algorithms monitor real-time heat generation and adjust cooling output dynamically. These systems prevent hotspots and reduce overcooling across zones. Large facilities deploy thermal digital twins using CFD simulations for airflow validation. Turkish data centers embrace smart monitoring for proactive maintenance. AI modules optimize fan speeds, chiller loads, and airflow balance. This trend helps reduce energy waste and enhances equipment longevity. The Turkey Data Center Thermal Management Market reflects strong adoption of intelligent cooling operations.

Modular and Scalable Cooling Systems Supporting Agile Facility Design

Operators increasingly deploy modular cooling units that scale with IT capacity growth. These systems enable faster deployment and integration into existing layouts. Rear door heat exchangers and in-rack units support on-demand expansion. Prefabricated units reduce installation time and align with agile development models. Vendors offer pre-engineered kits with flexible piping and distribution layouts. Retrofit-friendly solutions enable older facilities to modernize cooling without downtime. The Turkey Data Center Thermal Management Market supports growth of modular colocation and edge facilities. It enables customized thermal setups based on evolving business needs.

Emergence of Sustainability-Focused Cooling Metrics and Design Approaches

Operators shift toward sustainability KPIs beyond PUE, including water usage and carbon footprint. New facilities integrate renewable energy sources and prioritize free-cooling modes. Eco-friendly refrigerants and thermoelectric systems reduce environmental impact. Facility certifications increasingly evaluate thermal performance in green rating systems. Turkish operators explore phase-change cooling and adiabatic cooling to lower emissions. Liquid cooling designs prioritize closed-loop systems with minimal water use. The Turkey Data Center Thermal Management Market encourages greener cooling procurement policies. It helps align infrastructure with corporate ESG goals.

Localized Manufacturing and Vendor Partnerships Strengthening Supply Chain Resilience

Turkey sees growth in local assembly of thermal management hardware. Strategic partnerships with international vendors help reduce import lead times. OEMs set up regional distribution for chillers, heat exchangers, and airflow components. This shift supports rapid response to project demands and maintenance needs. Localized support enhances equipment uptime and client confidence. Software developers also customize thermal dashboards for Turkish data center operators. The Turkey Data Center Thermal Management Market benefits from regional ecosystem maturity. It increases self-sufficiency and reduces sourcing risks in large-scale deployments.

Market Challenges

High Capital Expenditure and Budget Constraints Limit New Technology Adoption

Initial deployment of liquid-based and hybrid thermal systems involves higher capital outlay. Many local operators hesitate to shift from traditional air-cooled designs. Retrofit complexity in older facilities further delays modernization. Budget limitations hinder the use of advanced automation or AI-driven tools. Custom solutions for high-density environments increase project cost. Financial pressure from inflation and currency fluctuations worsens CAPEX planning. Maintenance of imported components adds to recurring operational costs. The Turkey Data Center Thermal Management Market faces challenges in balancing cost with energy savings.

Climate Variability and Infrastructure Gaps Complicate Cooling System Design

Turkey’s diverse climate zones require region-specific thermal design strategies. Some inland regions experience harsh summers that strain air-based cooling systems. Lack of uniform grid reliability in remote areas adds risk for high-power thermal units. Data centers in emerging cities face delays in accessing water or chilled water infrastructure. Utility planning constraints make large-scale cooling integration difficult. Operators must overdesign systems to handle worst-case conditions, increasing energy use. Inconsistent urban development patterns affect heat load distribution in metro facilities. The Turkey Data Center Thermal Management Market must overcome design constraints from geographic and infrastructure gaps.

Market Opportunities

Surge in Edge Deployments and Regional Cloud Zones Creates Cooling Demand

Edge computing growth in Turkey creates strong demand for compact, efficient thermal systems. Local cloud zones established by global hyperscalers drive cooling needs in urban clusters. These smaller deployments require low-maintenance thermal designs. The Turkey Data Center Thermal Management Market benefits from increasing edge installations in retail, telecom, and banking. Vendors targeting edge-specific cooling gain early mover advantages.

Rising Retrofit and Upgrade Potential in Legacy Enterprise Data Centers

Turkey’s older enterprise data centers offer vast potential for retrofit-based cooling upgrades. Operators seek energy-efficient replacements for aging CRAC units and airflow components. Modular retrofits and DCIM-driven thermal control support quick modernization. The Turkey Data Center Thermal Management Market enables performance improvement in legacy environments through tailored upgrade solutions.

Market Segmentation

By Data Center Size

Large data centers dominate the Turkey Data Center Thermal Management Market due to rising hyperscale and colocation investments. These facilities demand high-performance cooling systems to manage heat from dense workloads. Medium data centers are expanding rapidly across second-tier cities. Small data centers, often edge or enterprise facilities, rely on compact and modular thermal units. Growth across all sizes drives demand for scalable thermal infrastructure.

By Cooling Technology

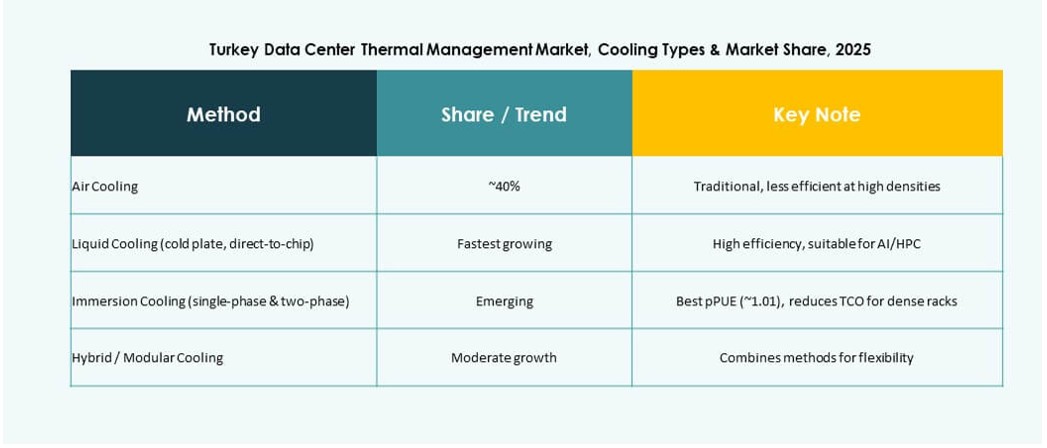

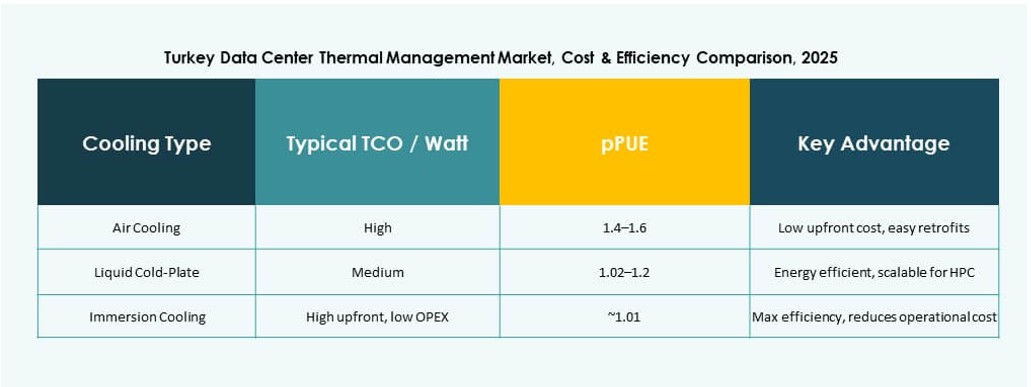

Air-based cooling holds the largest share due to cost efficiency and familiarity. Hot/Cold aisle and direct air cooling remain widely adopted. Liquid-based cooling sees high adoption in AI-ready setups using direct-to-chip and immersion systems. Hybrid cooling grows steadily in edge and modular environments. Thermoelectric and phase-change methods emerge in niche use cases, such as compact installations. The market embraces technology combinations to balance performance and cost.

By Component

Hardware leads the component segment, driven by demand for chillers, piping, and airflow equipment. Software adoption grows with DCIM integration and AI-based cooling optimization. Services gain traction in new deployments and ongoing retrofits. The Turkey Data Center Thermal Management Market sees increased outsourcing for monitoring and preventive maintenance tasks.

By Hardware

Cooling units and chillers dominate the hardware segment. Piping and distribution systems support liquid-based expansion. Heat exchangers and fans enhance airflow efficiency in traditional setups. Other components, including sensors and in-row modules, help optimize thermal performance. Vendors focus on modularity and energy efficiency across all categories.

By Software

DCIM dashboards remain the most used tool for visualizing and managing thermal systems. AI optimization tools gain momentum in large facilities. CFD simulation tools support layout validation and pre-deployment analysis. BMS modules integrate thermal performance with overall building systems. The software segment supports smarter, data-driven thermal decision-making.

By Services

Preventive maintenance services lead the segment, followed by retrofits and system upgrades. Monitoring as a service gains attention for remote facility management. Installation and commissioning services remain vital during new builds. The Turkey Data Center Thermal Management Market sees growth in managed service models for thermal infrastructure.

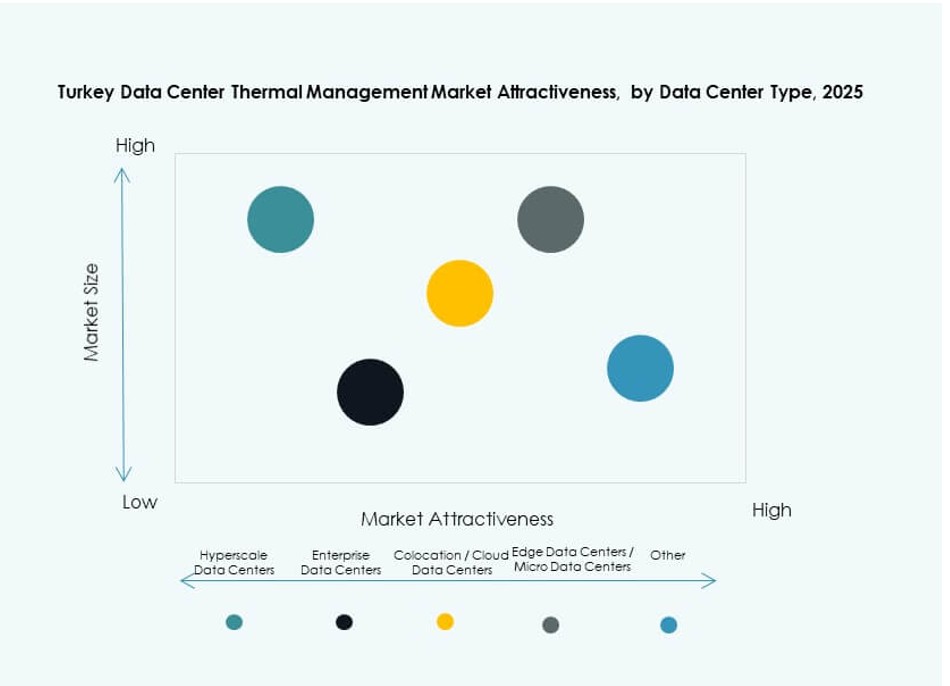

By Data Center Type

Colocation and cloud data centers lead due to demand from hyperscale deployments. Enterprise facilities maintain relevance in telecom and banking sectors. Edge and micro data centers gain share from urban expansion. Hyperscale projects create high-density demand requiring advanced thermal systems. Other facility types include telco switching hubs and government-run DCs.

By Structure

Room-based cooling systems remain common but are gradually replaced. Rack-based and row-based solutions grow with higher density and modularity needs. Row-based systems offer a balance between performance and ease of retrofit. Rack-based designs enable targeted cooling in edge environments. The market shifts toward adaptable thermal architectures that suit varied facility layouts.

Regional Insights

Istanbul Leads with Over 65% Share Driven by Hyperscale and Colocation Growth

Istanbul dominates the Turkey Data Center Thermal Management Market with more than 65% market share. The city hosts the highest concentration of hyperscale, colocation, and enterprise data centers. Strong connectivity infrastructure, energy availability, and strategic location drive investment. Global and local players prioritize Istanbul for new deployments and expansions. High-density workloads in this region accelerate adoption of advanced cooling systems. Vendors offer location-specific designs tailored to Istanbul’s coastal climate.

- for instance, Turkcell’s Gebze data center near Istanbul featuring 20 rooms of 500 m² each with Tier III design certification.

Ankara and Izmir Emerging as Secondary Hubs with 20% Combined Market Share

Ankara and Izmir together account for roughly 20% of the market. Ankara sees growth in government-backed IT infrastructure and public cloud demand. Izmir attracts private investments in regional edge and colocation facilities. Both cities face moderate climate conditions, enabling energy-efficient cooling methods. Facilities in these regions adopt row-based and hybrid systems to balance performance and cost. Operators target underserved enterprise and SME customers in these zones.

- For instance, Turkcell plans to expand its total data center space to approximately 107,000 m², including facilities in cities like Izmir. This expansion supports regional cloud growth and national digital infrastructure goals.

Other Cities Hold 15% Share with Rising Edge Deployment and Urban Digitization

The remaining 15% of the Turkey Data Center Thermal Management Market is shared by cities like Bursa, Antalya, and Gaziantep. These regions gain traction with localized edge deployments supporting telecom, retail, and smart city use cases. Operators prioritize compact cooling designs for space-constrained facilities. Infrastructure gaps and climate challenges persist in certain zones, prompting modular and adaptable thermal solutions. Investments in regional IT zones support market expansion outside core metros.

Competitive Insights:

- Vertiv Group Corp.

- Schneider Electric

- Daikin Industries Ltd.

- Delta Electronics, Inc.

- Johnson Controls International plc

- Mitsubishi Electric Corporation

- Canovate Group

- Türk Telekom Data Centers

- Turkcell

- LG Electronics

The Turkey Data Center Thermal Management Market features a mix of global OEMs and domestic infrastructure providers competing across segments. Vertiv, Schneider Electric, and Daikin lead in high-density cooling hardware and integrated systems. Delta Electronics and Mitsubishi Electric provide advanced modular units for hyperscale builds. Canovate Group, Türk Telekom, and Turkcell leverage localized operations and telecom-linked data centers. Players invest in liquid cooling, AI-based optimization, and retrofit solutions to serve rising cloud and colocation demand. The market remains highly competitive, with companies prioritizing energy-efficient performance, service uptime, and technology partnerships. It continues to shift toward modular, hybrid, and sustainable solutions tailored to Turkey’s evolving digital ecosystem.

Recent Developments:

- In December 2025, Türk Telekom announced its move to enhance data center efficiency through immersion liquid cooling systems. The company began adopting this technology to reduce energy consumption and environmental impact across its facilities. This strategic step enables support for high-density workloads while aligning with national sustainability goals.

- In November 2025, Turkcell signed a strategic agreement with Google Cloud to establish Turkey’s first hyperscale data center region. The partnership focuses on strengthening national cloud infrastructure and enhancing data sovereignty. Construction of the Ankara-based data centers is scheduled to begin in Q1 2026, with operations targeted between 2028 and 2029.

- In August 2025, Vertiv announced the Vertiv AI Infrastructure Program to enhance data center efficiency and thermal performance, applicable to global markets including Turkey where Vertiv operates.