Executive summary:

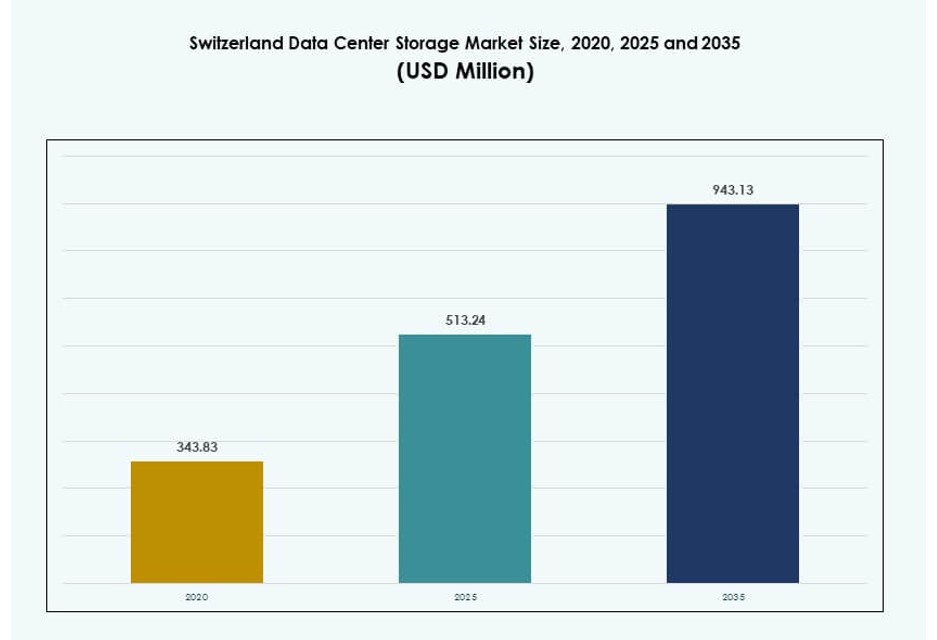

The Switzerland Data Center Storage Market size was valued at USD 343.83 million in 2020 to USD 513.24 million in 2025 and is anticipated to reach USD 943.13 million by 2035, at a CAGR of 6.22% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Switzerland Data Center Storage Market Size 2025 |

USD 513.24 Million |

| Switzerland Data Center Storage Market, CAGR |

6.22% |

| Switzerland Data Center Storage Market Size 2035 |

USD 943.13 Million |

Storage demand in Switzerland is growing with the shift to AI, analytics, and hybrid cloud platforms. Enterprises seek secure, high-performance systems to handle regulated workloads in BFSI, government, and healthcare sectors. Adoption of flash storage, software-defined platforms, and data lifecycle management is expanding. Vendors tailor solutions to support automation, sustainability, and compliance. Storage becomes a strategic focus for ensuring uptime, agility, and data control across mixed environments.

Zurich leads the market due to its strong financial ecosystem, data infrastructure, and hyperscale presence. Geneva and Lausanne follow as emerging hubs supporting research institutions, public agencies, and digital services. Basel and Bern contribute with pharma, government, and cross-border connectivity use cases. The distributed data center ecosystem enables regional storage growth with reliable power, regulatory alignment, and connectivity across European backbones.

Market Dynamics:

Market Drivers

Rising Demand for Secure, High-Availability Storage from Regulated Sectors Like Finance and Government

The Switzerland Data Center Storage Market is expanding due to strict data protection laws and regulatory oversight. Financial institutions and government bodies need storage systems with low-latency access and fault-tolerant architectures. These users prefer in-country data storage to maintain sovereignty and compliance. It supports adoption of private and hybrid cloud models with secure storage. Vendors respond with encrypted storage arrays and zero-trust infrastructure. Hardware and software providers emphasize reliability and uptime. Multinational companies prefer Swiss data centers for neutrality and policy stability. The country’s legal framework reinforces demand for enterprise-grade storage architecture. This market supports organizations where failure or breach poses critical risks.

- For instance, Green Datacenter AG’s Metro Campus Zurich spans 46,000 m² and connects to over 700 global PoPs via direct fiber, supporting compliant in-country storage for finance workloads.

Adoption of Next-Generation Storage to Handle Advanced Analytics, AI, and Big Data Workloads

Storage infrastructure is evolving to support AI-based applications and real-time analytics. Enterprises in Switzerland implement flash arrays, NVMe, and hyperconverged systems for higher performance. Data generated from IoT sensors, video surveillance, and AI training workflows pushes storage beyond legacy formats. All-flash storage and edge-tiered storage reduce latency and improve agility. Data pipelines now demand storage that scales horizontally and vertically. The Switzerland Data Center Storage Market benefits from early AI adopters across finance, pharma, and energy. It also gains from local R&D efforts supporting industry-specific workloads. Businesses treat data as a strategic asset and invest accordingly.

- For instance, SAN solutions held 35.2% market share in 2024, driven by NVMe front-ends for performance-sensitive banking and ERP applications.

Integration of Cloud-Centric and Software-Defined Storage to Enable Flexibility and Scalability

Organizations in Switzerland shift toward software-defined storage (SDS) for improved control and cost-efficiency. SDS decouples storage from hardware, allowing dynamic scaling and automation. This shift aligns with multi-cloud and hybrid storage deployments common across Swiss enterprises. IT teams require centralized management of data workloads across public cloud, on-premises, and edge devices. Cloud-native applications also demand faster provisioning and autoscaling features. SDS platforms offer strong support for backup, archiving, and containerized environments. The Switzerland Data Center Storage Market gains traction with MSPs and telecom operators adopting storage-as-a-service. This unlocks new monetization models for providers and simplifies access for mid-size businesses.

Focus on Energy Efficiency and Sustainability Driving Investment in Modern Storage Infrastructure

Energy consumption of storage infrastructure has become a major concern in Swiss data centers. Stakeholders prefer energy-efficient drives, optimized cooling, and intelligent power management systems. Next-gen storage units are designed with sustainability and operational savings in mind. Government and corporate climate mandates push green IT adoption. Vendors offer carbon reporting and sustainability certifications with enterprise storage solutions. The Switzerland Data Center Storage Market supports businesses aiming to meet ESG targets. Colocation providers and hyperscalers invest in efficient infrastructure to reduce operating costs. It promotes long-term ROI and ensures alignment with national energy goals.

Market Trends

Edge Storage Demand Rising from Industrial IoT and Decentralized Computing Initiatives

Switzerland’s industrial sectors increasingly deploy edge computing setups for localized data processing. Edge storage becomes essential to reduce latency and manage data generated at remote sites. Sectors like manufacturing, logistics, and utilities deploy smart devices that produce real-time data. Edge-based data centers with built-in storage capabilities support autonomous decision-making. It enhances operations in regions with bandwidth constraints or regulatory needs. The Switzerland Data Center Storage Market aligns with the push for fast local response and decentralized infrastructure. Growth in private 5G, smart grids, and automation tools accelerates edge adoption. Vendors tailor rugged, compact storage for edge deployment.

Shift Toward High-Density Storage Racks to Maximize Real Estate Utilization and Operational Efficiency

Space is limited in Switzerland’s urban data centers, especially in Zurich and Geneva. Operators prioritize rack-level optimization to store more data in smaller footprints. High-density storage racks and scalable enclosures reduce the cost per TB stored. Cooling and power delivery systems are upgraded to support denser rack configurations. This trend supports hyperscale and colocation operators managing growing data volumes. The Switzerland Data Center Storage Market responds with rack-integrated storage and modular deployment models. It reduces expansion barriers while maintaining performance. Enterprises gain better TCO and resource utilization from these formats.

Demand Growing for Multi-Tenant Storage Solutions in Carrier-Neutral Facilities

Carrier-neutral facilities in Switzerland support data exchange and interconnectivity for multi-cloud use. Businesses adopt multi-tenant storage solutions to gain flexibility and cost-sharing benefits. These setups support SMEs that require secure storage without maintaining private infrastructure. Managed storage services, including storage-as-a-service and backup-as-a-service, are widely adopted. Operators optimize facilities with pooled storage, dynamic allocation, and dedicated data protection. It enables fast provisioning and regulatory compliance at scale. The Switzerland Data Center Storage Market sees increased activity from platform providers and regional ISPs. Strong network ecosystems and cross-connect capabilities fuel further demand.

Data Lifecycle Management and Compliance Driving Intelligent Storage Adoption

With growing data volumes, organizations implement lifecycle management to optimize costs and compliance. Automated tiering shifts data between performance, capacity, and archival storage based on usage patterns. Data deletion policies, GDPR readiness, and retention mandates drive intelligent storage solutions. Storage platforms now feature policy-based automation and metadata tagging. It improves governance, lowers storage costs, and enhances audit readiness. The Switzerland Data Center Storage Market integrates AI-powered storage for analytics and compliance tasks. It benefits sectors like healthcare, finance, and legal where data sensitivity is high. Vendors develop compliance-oriented features to cater to Swiss and EU standards.

Market Challenges

High Infrastructure and Operational Costs Limit Entry for Small and Medium-Sized Data Storage Players

Switzerland has some of the highest operational costs in Europe due to electricity rates, land, and labor. These cost factors limit new entrants from competing with established hyperscalers and telecom operators. SMEs find it difficult to set up and sustain independent storage infrastructure. Regulatory compliance adds further cost, especially for industries handling sensitive data. The Switzerland Data Center Storage Market requires continuous investment in hardware and management platforms. Rising utility prices also impact total cost of ownership for data center operators. It puts pressure on margins and slows expansion into underserved regions. Cost-sensitive verticals delay modernization without external support.

Skilled Workforce Shortage and Cybersecurity Threats Challenge Storage Expansion and Adoption

Switzerland faces a shortage of skilled IT professionals with expertise in cloud storage, data security, and orchestration. This talent gap restricts rapid deployment and customization of modern storage solutions. High-value industries like BFSI and pharma also face increased cyber risks targeting sensitive stored data. Storage systems must include advanced encryption, threat detection, and immutable backups. The Switzerland Data Center Storage Market requires resilient infrastructure to meet strict SLAs. Addressing threats from ransomware, insider attacks, and misconfigurations adds complexity and cost. Vendors must balance security, performance, and usability to meet buyer expectations.

Market Opportunities

Growth in AI, Genomics, and Research Computing Creating Demand for Scalable Storage Solutions

Swiss universities, biotech firms, and R&D institutes need large, scalable storage to manage massive datasets. AI training, genomic sequencing, and simulation workloads generate multi-petabyte files. The Switzerland Data Center Storage Market supports growth in scientific computing through performance-oriented storage systems. Public-private partnerships and innovation grants encourage investment in compute-linked storage.

Cloud-Native Startups and SaaS Providers Expanding Need for Flexible Storage Infrastructure

Switzerland’s growing startup ecosystem, especially in fintech and medtech, demands scalable cloud-native storage. These businesses prioritize speed, agility, and cost-efficiency in data handling. Hybrid storage with fast provisioning appeals to SaaS vendors building next-gen platforms. The Switzerland Data Center Storage Market attracts vendors offering on-demand, pay-as-you-grow models.

Market Segmentation

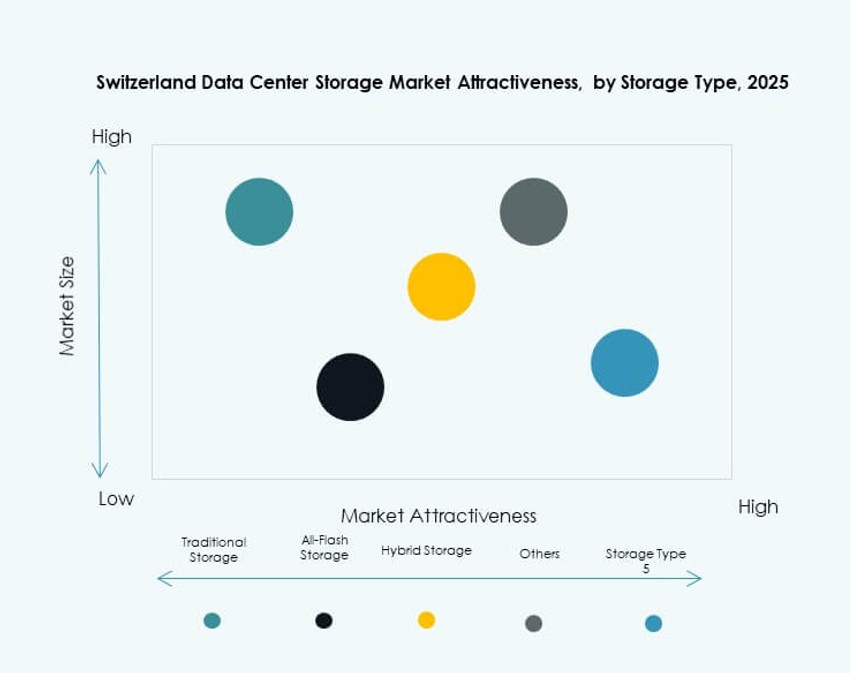

By Storage Type

The all-flash storage segment dominates the Switzerland Data Center Storage Market due to high performance and energy efficiency. Enterprises favor flash-based arrays for real-time analytics and latency-sensitive applications. Hybrid storage also holds a significant share by balancing performance and cost. Traditional storage is gradually declining but remains relevant for archival and backup use.

By Storage Deployment

Storage Area Network (SAN) systems lead the market with high-speed connectivity and enterprise-grade availability. SAN is widely used in BFSI, telecom, and healthcare sectors for mission-critical workloads. NAS systems are gaining traction among SMEs for their ease of use and cost-effectiveness. DAS systems serve edge deployments and branch offices with simple configuration.

By Component

Hardware holds the larger share in the Switzerland Data Center Storage Market due to continuous infrastructure modernization. High-capacity drives, enclosures, and controllers represent major investments. Software is growing fast, led by SDS, backup platforms, and data management tools. Vendors bundle software with hardware for integrated performance.

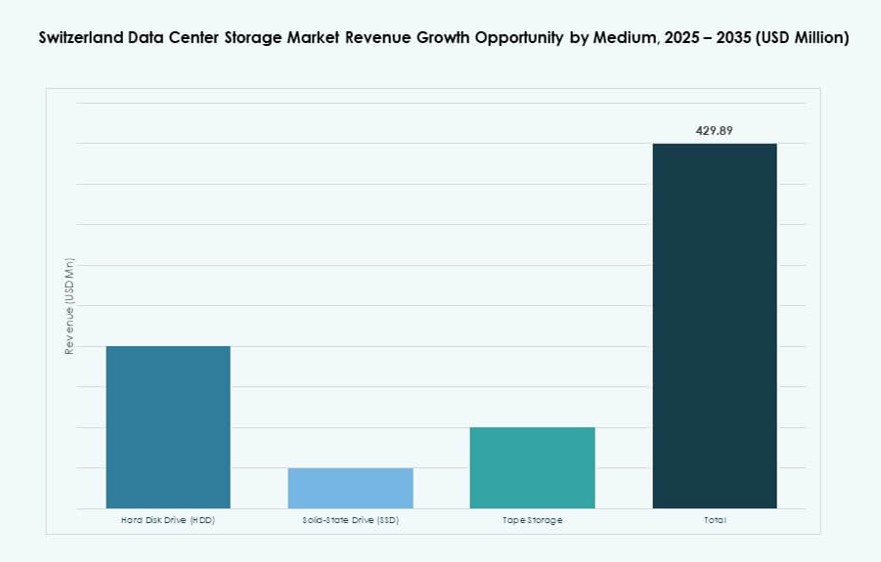

By Medium

Solid-State Drives (SSD) dominate the market because of speed, reliability, and declining cost per GB. SSD adoption is high in AI, financial analytics, and hybrid cloud deployments. HDD remains in use for bulk storage and cold data needs. Tape storage is niche, used mainly in long-term archival and compliance-driven environments.

By Deployment Model

Cloud-based storage leads the deployment model segment due to flexibility, scalability, and growing SaaS adoption. Hybrid storage is rising as enterprises combine cloud agility with on-prem security. On-premises deployment still serves sectors with strict compliance requirements like government and healthcare. It supports workflows that demand full data control.

By Application

The IT and telecom segment is the largest end-user of data center storage in Switzerland. It supports digital platforms, video services, and application hosting. BFSI follows closely, driven by the need for secure, high-throughput storage. Government and healthcare also show strong demand due to regulatory compliance. Other sectors such as retail and manufacturing contribute to market growth through digital transformation.

Regional Insights

Zurich Region Holds Over 45% Market Share Due to Dense Data Center Ecosystem and Financial Sector Presence

Zurich dominates the Switzerland Data Center Storage Market with over 45% share. It hosts most of the country’s hyperscale and colocation facilities, supported by strong network infrastructure. Major banks, insurers, and cloud firms operate storage-intensive platforms in this region. Zurich benefits from real estate readiness, power availability, and connectivity to European IXPs. It attracts both global vendors and enterprise customers with stringent data security requirements.

- For instance, Vantage Data Centers announced its ZRH2 campus in April 2024, providing 24MW of critical IT capacity across 21,000 square meters to support hyperscalers and AI workloads.

Geneva and Lausanne Combined Account for Around 35% Market Share Driven by Public Sector and Academia

Geneva and Lausanne are emerging as strong secondary data center hubs. Together, they hold around 35% of the market share. Geneva supports international organizations, embassies, and NGOs with compliant storage solutions. Lausanne benefits from proximity to research institutions and startups focused on innovation. Both cities benefit from multilingual talent pools and access to renewable energy resources.

Other Regions Including Basel and Bern Contribute 20% Market Share Backed by Industry and Government Demand

Basel and Bern collectively hold around 20% share of the Switzerland Data Center Storage Market. Basel’s pharma and life sciences industry relies on secure, high-capacity data platforms. Bern hosts federal government infrastructure and agencies requiring secure digital workflows. These cities support mid-size data centers and edge nodes connected to Zurich-Geneva backbones. Their role is expected to grow as storage decentralization accelerates.

- For instance, Equinix ZH5 in the broader Zurich-area ecosystem supports N+1 power and cooling redundancy across 71,800 square feet of usable space.

Competitive Insights:

- Swisscom

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- IBM Corporation

- NetApp

- Lenovo Group

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Cohesity, Inc.

- Hitachi Vantara

The Switzerland Data Center Storage Market features a mix of domestic and global technology providers. Swisscom maintains a strong local presence with integrated data and cloud services. Global players such as Dell, HPE, and IBM lead in hardware and software-defined storage offerings. NetApp and Cohesity focus on data management, backup, and hybrid cloud solutions. Cisco and Lenovo support enterprise-grade systems with robust infrastructure portfolios. Huawei and Hitachi Vantara contribute to dense storage deployment with scalable products. It remains competitive due to ongoing innovation in flash storage, disaggregated systems, and AI-integrated platforms. The market favors vendors offering energy-efficient, flexible, and compliance-ready solutions.

Recent Developments:

- In March 2025, Hewlett Packard Enterprise (HPE) partnered with NVIDIA to launch AI solutions tailored for enterprise data management and model deployment, enhancing hybrid cloud capabilities relevant to Switzerland’s data center storage ecosystem.

- In March 2025, at the NVIDIA GTCevent, Cohesity announced a significant expansion of its Cohesity Gaia platform to deliver one of the industry’s first AI-powered search capabilities for on-premises backup data.

- In April 2024, Vantage Data Centers invested over 370 million Swiss francs in a new hyperscale facility, Zurich 2, in Glattfelden, featuring 24 MW IT capacity with energy-efficient technologies like heat pumps and green roofs.