Executive summary:

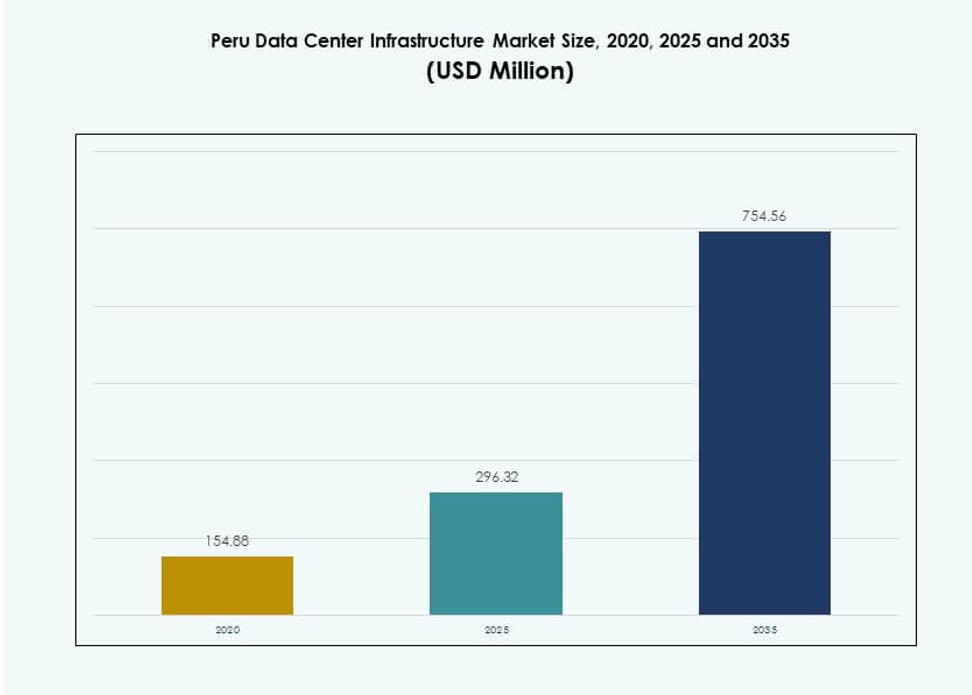

The Peru Data Center Infrastructure Market size was valued at USD 154.88 million in 2020 to USD 296.32 million in 2025 and is anticipated to reach USD 754.56 million by 2035, at a CAGR of 9.73% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Peru Data Center Infrastructure Market Size 2025 |

USD 296.32 Million |

| Peru Data Center Infrastructure Pakistan , CAGR |

9.73% |

| Peru Data Center Infrastructure Market Size 2035 |

USD 754.56 Million |

The market is driven by growing digital transformation across enterprises, cloud migration, and regulatory support for data localization. Businesses are adopting hybrid cloud models and colocation services to meet performance and compliance needs. Innovations in power and cooling systems help operators reduce energy use and improve uptime. The push toward AI, edge computing, and 5G also fuels demand for high-density and low-latency infrastructure. For investors, this sector offers strong returns backed by rising IT workloads and data sovereignty regulations.

Lima leads the market due to its established connectivity, concentration of enterprises, and subsea cable access. Secondary regions like Arequipa and Trujillo are emerging with improved infrastructure and regional business activity. These areas attract edge deployments, especially in sectors like mining, logistics, and telecom. Northern and jungle regions remain underdeveloped but present long-term potential through modular and mobile data centers. The geographic spread reflects Peru’s digital expansion beyond the capital.

Market Dynamics:

Market Drivers

Rising Digitalization and Government Push Towards Data Sovereignty

The Peru Data Center Infrastructure Market is expanding as enterprises accelerate digital transformation and cloud-first strategies. Government policies supporting local data storage compliance and digital public services create long-term growth visibility. The National Digital Transformation System aims to centralize digital governance, which boosts demand for reliable data infrastructure. Businesses are increasing investment in colocation and enterprise facilities to reduce latency and improve service delivery. The rise in e-governance, online tax filing, and public digital records management strengthens data center relevance. Local storage mandates also drive enterprise preference for in-country hosting. The regulatory focus aligns market momentum with digital trust, security, and data integrity. Infrastructure providers are responding with Tier III and IV designs to meet SLA expectations and uptime standards. The Peru Data Center Infrastructure Market benefits directly from these national-level initiatives and compliance pressures.

- For instance, Claro Peru inaugurated its Tier III data center in Lima in December 2023, featuring a 250 sqm IT room with capacity for 104 cabinets to support cloud migration for enterprises and public entities.

Increased Cloud and Colocation Adoption by Local Enterprises and Global Platforms

Hybrid cloud and multicloud models are gaining traction across Peru’s banking, retail, and mining sectors. Businesses seek flexibility, scalability, and disaster recovery readiness through colocation partnerships and managed hosting models. Global hyperscalers are evaluating the country for future presence or indirect edge deployments. The market supports edge computing rollouts in remote and high-demand areas like mining zones or telecom hubs. Cloud-first procurement by SMEs and large enterprises fosters investment in secure, compliant infrastructure. Local service providers build scalable facilities to support SaaS, IaaS, and DRaaS platforms. These shifts create a reliable revenue base for long-term operators and EPC contractors. The Peru Data Center Infrastructure Market is seeing increased CAPEX from neutral providers and telcos aiming to diversify revenue from traditional connectivity services. This colocation-led ecosystem supports accelerated cloud migration and regional competitiveness.

Technological Advancements in Power and Cooling Infrastructure Efficiency

Rising power costs and sustainability pressures are driving Peru-based operators to adopt energy-efficient electrical and mechanical infrastructure. Tier III and Tier IV data centers focus on integrating battery energy storage systems (BESS), smart UPS, and modular PDUs to enhance uptime. Intelligent power routing and real-time energy monitoring help reduce operational risk and cost. Cooling systems are shifting to indirect evaporative models and hot/cold aisle containment to reduce PUE ratios. These innovations improve cost-efficiency, environmental sustainability, and SLA compliance. Builders are using prefabricated and modular mechanical units for speed, flexibility, and integration. AI-based energy optimization platforms are also being trialed in larger deployments. The Peru Data Center Infrastructure Market is embracing these energy-centric innovations to lower TCO and comply with environmental norms.

- For instance, Claro Peru’s Lima facility integrates renewable energy certification from Luz del Sur distributor, ensuring energy-efficient operations across its 104-cabinet capacity.

Strategic Business Relevance Driven by Regional Connectivity and Latency Needs

With growing demand for digital platforms, Peru’s geographic position strengthens its role as a regional edge hub. Its subsea cable links to Chile and the U.S. enhance international bandwidth, while fiber backbone improvements reduce latency for internal workloads. Financial services, healthcare, and retail industries are driving local storage demand for faster transaction and application performance. Latency-sensitive applications like fintech, video streaming, and logistics automation depend on localized compute. The Peru Data Center Infrastructure Market serves as a regional node for reducing data transfer bottlenecks and improving user experience. International content providers, CDNs, and telecom operators target the market to deploy low-latency infrastructure. Peru’s mix of connectivity, political stability, and demand density make it a strategic investment zone for investors and infrastructure players.

Market Trends

Modular and Prefabricated Construction Gains Momentum Across Edge and Mid-Sized Builds

Data center developers are increasingly shifting toward modular construction to reduce build time, cost, and complexity. Prefabricated units allow consistent quality control and faster deployment, especially in remote regions with limited skilled labor. These units simplify integration across power, cooling, and network layers. Modular deployments also support incremental capacity expansion based on demand. Prefab designs are gaining preference in Tier II and III cities to support regional enterprise workloads. Manufacturers are scaling offerings to include power skids, integrated cooling blocks, and rack-ready modules. The Peru Data Center Infrastructure Market is seeing demand for modular builds to support edge computing, disaster recovery, and government infrastructure modernization. Modular systems also align well with phased investments and rapid commissioning goals.

Sustainable Design Integration and Renewable Energy Adoption by Operators

Sustainability is becoming a key consideration in Peru’s data center planning. Operators focus on reducing energy consumption and carbon footprint by adopting renewable energy and efficient cooling. Green building certification, such as LEED or EDGE, is gaining interest among new developers. Use of solar energy, wind sourcing, and BESS for peak load balancing is increasing. Government incentives for green infrastructure further encourage this transition. Local utilities are also partnering to provide cleaner energy for data center parks. Cooling technology selection is influenced by water consumption and emissions reduction targets. The Peru Data Center Infrastructure Market reflects this shift in mindset, with large and mid-sized facilities incorporating green power goals and transparent sustainability metrics.

Increased Rack Density and Virtualization in Enterprise and Colocation Spaces

Operators are transitioning to high-density rack configurations to optimize space and energy. Virtualization and hyperconverged infrastructure adoption are pushing rack power requirements beyond 10 kW per rack. Colocation providers adjust facility layouts and cooling distribution accordingly. Blade servers, GPU-based systems, and AI/ML workloads contribute to higher density requirements. This shift demands stronger airflow management, liquid cooling options, and precise thermal zoning. Higher rack density reduces footprint and improves ROI on real estate. Enterprises deploy virtualization to maximize compute per square foot and support hybrid environments. The Peru Data Center Infrastructure Market responds to these shifts with facility upgrades that accommodate rising power and heat loads per rack.

Localized Data Center Investment by Telecom Providers and Domestic IT Firms

Domestic telecom companies and ISPs are actively investing in data center infrastructure to extend digital service portfolios. These firms are building small to mid-sized facilities closer to user populations to support CDN, caching, and 5G edge applications. IT firms are developing their own facilities or entering colocation agreements to serve clients with hosted ERP, CRM, and analytics platforms. Regional differentiation strategies drive localized infrastructure in secondary cities. Private equity and infrastructure funds are backing these expansions with a focus on scalability and recurring revenue. Demand for multi-tenant models is increasing as small businesses seek scalable yet affordable hosting solutions. The Peru Data Center Infrastructure Market supports this distributed model that combines national reach with localized service delivery.

Market Challenges

Power Infrastructure Limitations and Rising Energy Costs Impact Facility Scalability

Electricity cost and availability remain key bottlenecks for large-scale data center expansion in Peru. Several regions lack grid resilience and backup redundancy, forcing developers to over-invest in UPS and generator capacity. Fluctuating energy prices create uncertainty in OPEX forecasting. Regulatory barriers delay power connection approvals and increase compliance complexity. Grid integration of renewable energy is still in early stages and lacks seamless interconnection with industrial-scale loads. This slows deployment timelines and affects project ROI calculations. Power quality concerns, such as voltage stability, affect high-density compute operations. The Peru Data Center Infrastructure Market requires structural grid upgrades and policy reform to address these power-related limitations.

Skilled Workforce Shortage and Limited Vendor Ecosystem in Key Infrastructure Segments

Peru faces a shortage of local expertise in mission-critical infrastructure design, operation, and maintenance. Engineering talent in power systems, HVAC design, and facility automation is in short supply. This leads to dependency on foreign firms and increases project cost. Lack of skilled staff for on-site support and compliance management affects operational uptime. The vendor ecosystem is limited for advanced infrastructure components like containment systems, DCIM software, and high-density racks. Import dependence creates longer procurement cycles and limits customization. Training and certification programs are insufficient to meet the growing workforce demand. The Peru Data Center Infrastructure Market requires targeted skill development and local vendor ecosystem expansion.

Market Opportunities

Emerging Cloud-Native Startups and SME Digitalization Drive Edge Infrastructure Growth

A rise in cloud-native startups and digitally transforming SMEs creates new demand nodes outside Lima. These businesses require localized edge infrastructure for latency-sensitive applications and backup services. Edge nodes in secondary cities support real-time analytics, e-commerce, and SaaS platforms. Service providers can deploy micro data centers or containerized units to capture this segment. The Peru Data Center Infrastructure Market is poised to benefit from this decentralization of demand.

Public-Private Partnerships to Build Regional Data Hubs and Upgrade Telecom Infrastructure

Government focus on regional digitization creates opportunities for public-private investments in data hubs. Infrastructure developers can collaborate with municipalities to build resilient, low-latency digital ecosystems. Telecom backbone upgrades and smart city initiatives increase demand for distributed compute and storage. Investors can leverage state-backed funding to accelerate infrastructure deployment across underserved zones.

Market Segmentation

By Infrastructure Type

The Peru Data Center Infrastructure Market sees strong traction in electrical and mechanical infrastructure, driven by uptime and cooling demands. Electrical infrastructure holds the dominant share due to high power reliability requirements. IT and network infrastructure also grow steadily, with rising server virtualization and high-speed networking needs. Civil and structural components grow as new builds increase in both greenfield and brownfield formats. Modular architecture adoption supports rapid installation and flexible expansion.

By Electrical Infrastructure

Uninterruptible power supply (UPS) systems dominate the electrical infrastructure segment due to Peru’s unstable grid in many areas. Utility service upgrades are increasing, but reliability gaps keep demand high for BESS and transfer switch systems. Power distribution units (PDUs) and smart monitoring units see growth with higher rack densities. Investment in advanced switchgears and smart load balancing improves energy use efficiency.

By Mechanical Infrastructure

Cooling units like CRAC and CRAH dominate mechanical infrastructure, followed by containment systems for thermal management. Chillers, particularly air-cooled, are preferred in low-humidity regions. Data centers increasingly deploy hot/cold aisle configurations to optimize energy use. Modular pump and piping systems improve reliability and ease maintenance. Operators invest in smart cooling to improve PUE across facilities.

By Civil / Structural & Architectural

Superstructures using steel frames dominate construction practices in urban zones due to seismic resilience and cost-efficiency. Raised floors and modular ceilings are standard in most Tier III facilities. Modular building systems are gaining traction in rural deployments. Envelope design improvements improve thermal insulation and fire safety compliance. Foundations and site prep demand increase as brownfield redevelopment rises.

By IT & Network Infrastructure

Server and networking equipment hold the largest market share under IT infrastructure. Racks and enclosures see steady demand, especially from colocation providers. Fiber cabling and optical interconnects are growing fast due to rising high-speed data needs. Storage infrastructure grows with demand for edge caching and archival services. Overall, this segment grows with enterprise cloud and SaaS adoption.

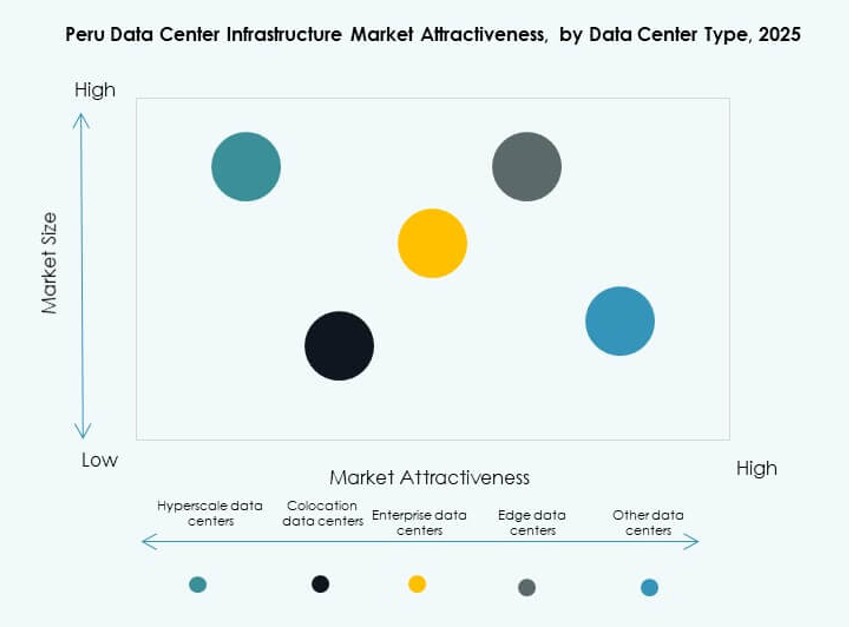

By Data Center Type

Colocation data centers lead the market due to demand from mid-size enterprises, CDNs, and telecoms. Hyperscale players are limited but show interest in strategic partnerships. Edge data centers grow in remote and mining zones. Enterprise facilities continue to evolve into hybrid cloud nodes. The Peru Data Center Infrastructure Market supports all types with varying delivery and scale models.

By Delivery Model

Design-build and turnkey models dominate new construction due to speed, cost, and accountability benefits. Retrofit and modular upgrades gain traction as enterprises update legacy sites. Construction management remains niche, mostly used by large industrial developers. Modular factory-built solutions gain share in edge deployments requiring rapid setup and scalability.

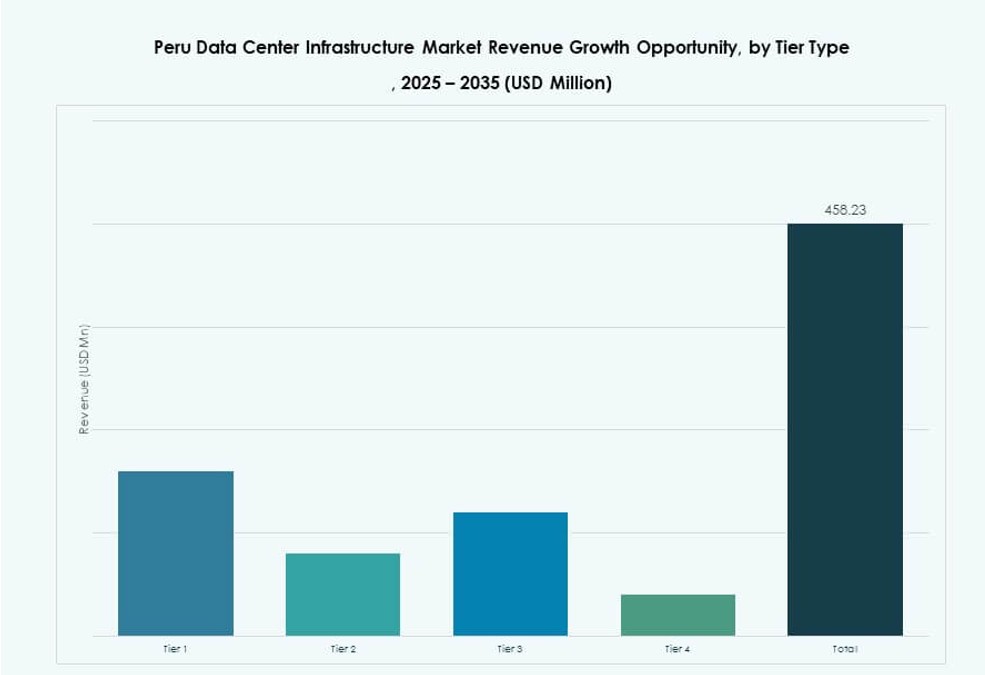

By Tier Type

Tier III facilities dominate due to their balance of cost and reliability for Peru’s enterprise and colocation needs. Tier IV grows slowly but attracts high-end clients in finance and telecom. Tier II holds niche relevance for disaster recovery or secondary nodes. Tier I presence is minimal due to low uptime suitability for commercial clients.

Regional Insights

Lima Metropolitan Region Dominates Market with Over 75% Revenue Share

Lima is the primary data center hub due to its role as Peru’s business, telecom, and regulatory capital. Most enterprises, banks, and IT service firms operate from Lima, driving demand for reliable hosting. High connectivity, access to skilled labor, and developed real estate make it the preferred site for new data centers. The Lima region contributes over 75% of the Peru Data Center Infrastructure Market revenue. Its subsea cable landing points and robust power grid enhance its dominance.

Arequipa and Trujillo Emerging as Secondary Data Center Growth Zones

Secondary cities such as Arequipa and Trujillo account for 12–15% of the market and show high growth potential. Government digitization programs and industrial development drive infrastructure investment in these zones. Regional enterprises seek colocation services closer to operations. Local governments encourage IT zone development to decentralize services from Lima. Infrastructure developers are exploring edge facilities and micro data centers in these cities.

- For instance, Canvia opened its third data center in Lima’s San Isidro area in October 2023 as a USD 6 million facility, supporting broader colocation expansion.

Northern and Jungle Regions Offer Long-Term Edge Expansion Potential

Amazonas, Loreto, and northern departments remain underserved, representing under 10% of current market share. Lack of connectivity and infrastructure challenges slow growth. However, expanding telecom networks and satellite broadband open new edge infrastructure opportunities. Future growth depends on regional economic programs, mining activity, and improved transport links. The Peru Data Center Infrastructure Market can expand here through modular and mobile data center formats.

- For instance, Cirion Technologies broke ground on a 20MW data center in Lima in June 2023, signaling potential for modular expansions to underserved regions.

Competitive Insights:

- ABB

- Scala Data Centers

- MDC Data Centers

- Ascenty

- Cisco Systems, Inc.

- Dell Inc.

- Equinix, Inc.

- Schneider Electric

- Vertiv Group Corp.

The Peru Data Center Infrastructure Market shows moderate concentration with a mix of global technology vendors and regional data center operators. International players lead in electrical, cooling, and IT infrastructure due to strong product portfolios and proven reliability. Colocation specialists focus on scalable facilities and carrier-neutral designs to attract enterprise and cloud clients. Competition centers on uptime assurance, energy efficiency, and modular deployment capability. Vendors differentiate through turnkey delivery models, lifecycle services, and local partnerships. Regional operators compete by offering proximity, lower latency, and customized solutions for domestic enterprises. Pricing discipline and service-level guarantees influence contract decisions. The market favors companies with strong EPC expertise and long-term support capability. It continues to reward firms that align infrastructure design with efficiency, compliance, and future scalability needs.

Recent Developments:

- In February 2025, Vertiv opened new offices in Peru to support growth in the data center market amid rising demands for connectivity, AI, and 5G.

- In October 2024, GTD opened its 20MW data center in the Lurín area outside Lima, Peru, with 960 cabinets across 2,100 sqm of white space on a 10,000 sqm plot, supported by a $50 million investment and Tier III certification.