Executive summary:

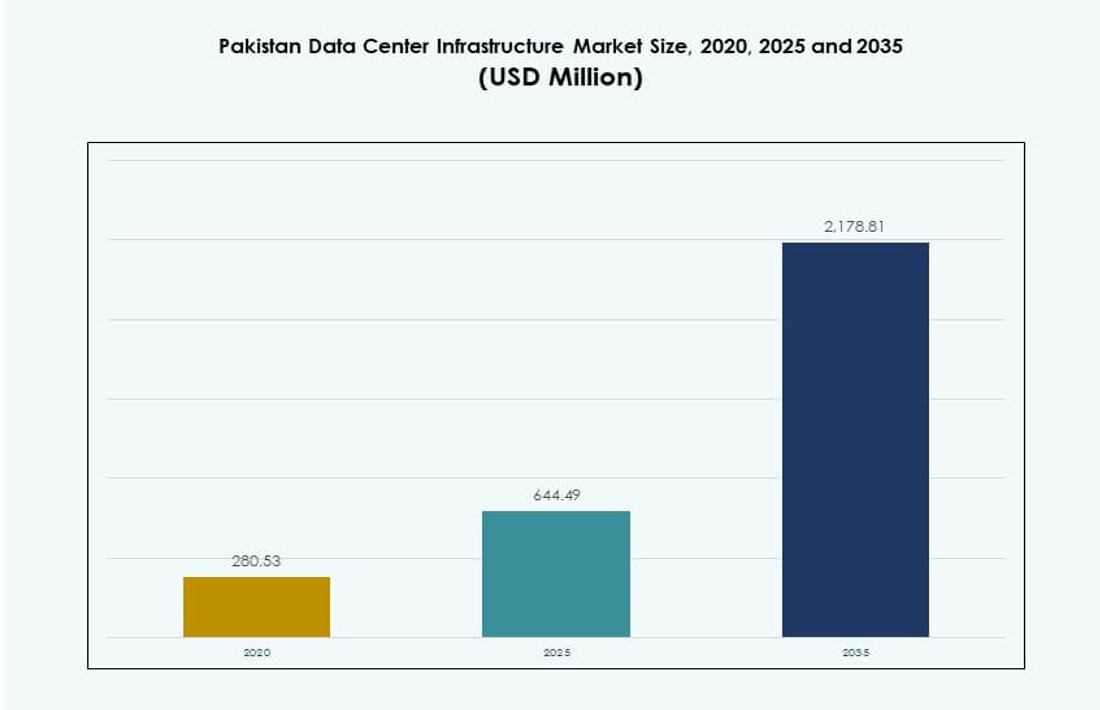

The Pakistan Data Center Infrastructure Market size was valued at USD 280.53 million in 2020 to USD 644.49 million in 2025 and is anticipated to reach USD 2,178.81 million by 2035, at a CAGR of 12.85% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Pakistan Data Center Infrastructure Market Size 2025 |

USD 644.49 Million |

| Pakistan Data Center Infrastructure Pakistan , CAGR |

12.85% |

| Pakistan Data Center Infrastructure Market Size 2035 |

USD 2,178.81 Million |

The market is growing rapidly due to rising cloud adoption, enterprise digitalization, and government-led infrastructure programs. Telecom and BFSI sectors are deploying scalable and resilient data centers to support digital platforms. Edge computing, AI workloads, and real-time applications are driving demand for high-density, energy-efficient systems. The market is strategically important as it supports national data sovereignty, improves uptime for mission-critical services, and enables broader economic digital transformation. Businesses are adopting hybrid models, with a focus on compliance and local data hosting.

Karachi leads the market due to its submarine cable landing stations, dense enterprise clusters, and carrier-neutral hubs. Lahore follows, driven by a growing base of IT services and industrial users. Islamabad sees strong traction from public sector digitization and smart city projects. Secondary cities like Faisalabad and Multan are emerging with edge data center deployments to serve regional and disaster recovery needs. Market expansion is shaped by connectivity, power availability, and digital ecosystem maturity.

Market Dynamics:

Market Drivers

Growing Digital Transformation Across Banking, Government, and Telecom Sectors Is Driving Infrastructure Demand

Digitalization of core sectors is accelerating the demand for secure and scalable data centers. Government initiatives like Digital Pakistan and rising fintech adoption require robust backend systems. Telecom operators and banks are shifting to virtualized platforms and cloud-native architectures. The Pakistan Data Center Infrastructure Market is gaining traction due to this shift toward resilient infrastructure. Demand for low-latency applications and compliance-driven workloads adds further pressure on legacy systems. Companies seek on-premise and hybrid models to maintain control while ensuring scalability. Public sector data migration and smart city ambitions also fuel market momentum. Strategic infrastructure upgrades have become critical for service continuity and disaster recovery. Businesses now prioritize data center resilience to ensure operational uptime.

- For instance, PTCL’s commercial data center in Lahore received Uptime Institute Tier III certification, supporting nationwide digital banking and cloud-native operations across over 1,900 enterprise clients.

Surge in Cloud Adoption and Platform Integration Fuels Core Infrastructure Investments

Cloud adoption is surging among enterprises seeking agility and scalability. Local and global cloud providers are entering partnerships with local data center firms. Platform integration across ERP, CRM, and core banking systems boosts need for uninterrupted power and cooling. The Pakistan Data Center Infrastructure Market benefits from these transitions, pushing electrical and mechanical investments. Businesses move away from monolithic systems and invest in modular IT infrastructure. High-density workloads demand energy-efficient designs with modern UPS and PDUs. Cloud-native applications require networked storage and structured cabling for seamless performance. Government support for cloud-first strategies encourages enterprise and SME adoption. Critical applications across telecom and finance further drive edge and core deployments.

Rising Demand for Energy-Efficient and Sustainable Solutions Among Enterprises and Colocation Providers

Green data centers are gaining importance due to high energy costs and sustainability goals. Enterprises and colocation providers invest in energy-efficient UPS systems and liquid cooling to manage power loads. The Pakistan Data Center Infrastructure Market is witnessing a shift toward eco-friendly buildings and BESS-based backup systems. Local developers now incorporate solar integration and power usage effectiveness (PUE) targets in facility planning. Regulatory pressure on carbon footprint reduction is guiding design specifications. High-capacity sites in major cities prefer chilled water systems and intelligent containment. Load optimization through software-defined power distribution further enhances efficiency. Demand for certifications like LEED or Uptime Institute standards is growing. Clean energy integration will define future investment patterns.

Strategic Importance of Data Localization, Business Continuity, and Hybrid Work Architectures

Data localization laws and hybrid work models are accelerating domestic infrastructure deployment. Enterprises prefer local storage to ensure compliance with national cybersecurity guidelines. The Pakistan Data Center Infrastructure Market reflects this shift with growth in enterprise and edge deployments. Business continuity needs during disruptions have led to active investment in DR and backup sites. Hybrid work models require secure, scalable, and latency-optimized environments. IT leaders are redesigning core and edge network topologies to support remote access. Sectors like healthcare, education, and logistics are deploying micro data centers for branch-level access. Regional data centers in smaller cities address local latency and redundancy. Localization, compliance, and work flexibility are reshaping infrastructure priorities.

- For instance, XDS DataCentre and Al Nahal IT Park partnered in October 2025 to launch Pakistan’s first AI liquid-immersion data center in Karachi, featuring containerized DR solutions to ensure fast access and regulatory-compliant storage.

Market Trends

Rise of Edge Data Centers to Serve Latency-Sensitive Applications in Secondary Cities

Growth in real-time services such as video streaming, gaming, and IoT accelerates the adoption of edge data centers. Demand is rising in Tier II and Tier III cities, where fiber expansion is improving connectivity. Localized content delivery requires low-latency processing close to users. The Pakistan Data Center Infrastructure Market sees growing investments in modular edge facilities. Telecom providers deploy edge nodes to reduce core network loads. Enterprises adopt compact edge deployments to manage distributed workloads. These facilities also support disaster recovery for core centers in major cities. Government digitization programs extend services to rural zones, supporting edge installations. Edge data centers improve digital access, especially in remote locations.

Adoption of Liquid Cooling Technologies to Manage High-Density Racks and Reduce Energy Costs

Rising rack densities and thermal loads demand advanced cooling solutions. Liquid cooling is gaining traction due to better energy efficiency and space optimization. The Pakistan Data Center Infrastructure Market reflects a growing shift from traditional CRAC/CRAH systems to direct-to-chip cooling. Facilities supporting AI, ML, and blockchain workloads require higher power densities. Colocation providers offer liquid cooling-ready racks to support HPC customers. Data centers in Karachi and Lahore are early adopters of chilled water and in-row cooling units. Efficient cooling helps operators achieve PUE targets and reduce operational expenditure. Sustainable operations push demand for intelligent airflow management. Technology-driven efficiency becomes a key facility selection metric.

Deployment of Modular and Prefabricated Data Center Facilities for Faster Time-to-Market

Modular construction offers scalability, speed, and reduced capital risk. Data center developers in Pakistan increasingly adopt prefabricated infrastructure models. Factory-built power and cooling units enable faster site rollouts with minimal on-site work. The Pakistan Data Center Infrastructure Market is moving toward containerized and pod-based modules. Demand from colocation and enterprise clients favors standardization and plug-and-play models. Rapid digital service growth requires short deployment timelines, driving modular adoption. Facilities in Islamabad and Karachi use modular setups to meet early-phase demand. Pre-engineered buildings support future expansion without disrupting existing workloads. Modular designs also align with disaster-resilient architectures.

Expansion of Carrier-Neutral Colocation Facilities Supporting Multi-Cloud Ecosystems

Carrier neutrality is becoming a standard for enterprise cloud strategy in Pakistan. Businesses require flexible interconnects between cloud providers and ISPs. The Pakistan Data Center Infrastructure Market sees growth in colocation centers offering multiple carrier options. This enables seamless multi-cloud, hybrid cloud, and cross-border data flow. Large colocation providers expand network nodes for improved interconnectivity. Enterprises use colocation as a stepping stone to cloud migration. Carrier-neutral hubs attract fintech, e-commerce, and OTT platforms. The model promotes cost efficiency, network diversity, and service resilience. Data centers that support multiple tenants and cloud on-ramps gain competitive edge.

Market Challenges

Power Reliability Issues and Grid Instability Create Barriers for Uptime-Driven Facilities

Frequent load shedding and limited grid stability challenge operational efficiency. Data centers must invest heavily in backup power systems, increasing capital expenditure. The Pakistan Data Center Infrastructure Market struggles with high diesel costs for generator runtime. Grid dependency limits expansion in regions without infrastructure upgrades. Renewable integration is slow due to regulatory hurdles and unreliable feed-in. Power availability restricts development outside metro areas. Data centers in smaller cities face higher risks due to unstable electricity supply. Infrastructure resilience depends heavily on private power arrangements. These limitations hinder Tier III and Tier IV certifications.

Limited Local Supply Chain and Technical Talent Pool Slows High-Scale Deployment

Lack of specialized contractors and suppliers limits infrastructure buildout. Import dependence for UPS, PDUs, and cooling units increases costs and lead times. The Pakistan Data Center Infrastructure Market requires foreign vendors for system integration and commissioning. Absence of certified local professionals affects uptime and maintenance quality. Engineering talent familiar with ASHRAE and Uptime standards remains scarce. Regulatory approvals for land use and building codes delay project execution. Customization capabilities remain limited among local EPC firms. Without supply chain localization, market growth will remain urban-centric. Investment inflow slows in areas lacking technical execution capacity.

Market Opportunities

Rising Investments from Telecom and Financial Institutions for Core and Edge Facility Expansion

Telecom and BFSI players drive infrastructure demand through data growth and regulatory compliance. The Pakistan Data Center Infrastructure Market benefits from their long-term digitization and service reliability goals. Telecoms expand cloud and enterprise offerings, boosting rack and power requirements. Banks invest in DR, edge, and core upgrades to support digital banking platforms. Growth of digital payments also contributes to infrastructure expansion across cities.

Public-Private Partnerships and SEZ-Based Data Parks to Support Localized Infrastructure Rollout

Government support for Special Economic Zones (SEZs) and industrial corridors creates room for infrastructure projects. Investors explore land banks and incentives for data center parks. The Pakistan Data Center Infrastructure Market gains from PPP-led initiatives to create national IT zones. This model reduces entry barriers and accelerates private participation in regional hubs.

Market Segmentation

By Infrastructure Type

Electrical infrastructure dominates the [Pakistan Data Center Infrastructure Market] due to high power dependency in uptime-sensitive facilities. Mechanical infrastructure holds strong share with growing adoption of precision cooling systems. Civil/structural and architectural demand rises with expansion of new facilities. IT & network infrastructure sees steady growth led by server virtualization and cloud deployment. Electrical and mechanical subsegments are expected to lead with over 60% combined market share.

By Electrical Infrastructure

UPS systems and grid connection form the backbone of electrical setups in mission-critical sites. Battery Energy Storage Systems (BESS) gain popularity due to power instability issues. PDUs and switchgear adoption grow alongside rack density increases. The [Pakistan Data Center Infrastructure Market] shows growing interest in redundant electrical paths and scalable switchboards. Utility integration in SEZs and metro zones drives long-term growth for this segment.

By Mechanical Infrastructure

Cooling units like CRAC/CRAH and chillers are essential for maintaining thermal balance in high-load environments. Containment systems and efficient airflow design are prioritized to achieve target PUE. Growth in water-cooled and in-row solutions is evident across large colocation sites. The [Pakistan Data Center Infrastructure Market] sees innovation in liquid cooling for AI and HPC applications. Mechanical systems remain vital to ensure compliance with uptime standards.

By Civil / Structural & Architectural

Superstructures and prefabricated buildings dominate due to faster construction cycles. Modular floor systems support scalability and airflow control. The [Pakistan Data Center Infrastructure Market] increasingly adopts modern wall and roof materials for insulation. Strong demand emerges for raised floors and ceiling grids. Urban data centers favor compact and high-load structures for space optimization.

By IT & Network Infrastructure

Server, storage, and cabling systems are critical for supporting core and distributed workloads. Networking gear supports multi-cloud environments and secure traffic routing. The [Pakistan Data Center Infrastructure Market] prioritizes rack design and optical fiber adoption. Modern enclosures enable high-density deployments with energy efficiency. This segment forms the digital backbone of expanding facilities.

By Data Center Type

Enterprise and colocation data centers dominate the landscape with over 70% share. Hyperscale deployments remain limited but are expected to rise. Edge data centers emerge in telecom-driven use cases and public service digitization. The [Pakistan Data Center Infrastructure Market] is gradually transitioning from legacy facilities to hybrid models. Each type plays a strategic role in the national digital infrastructure.

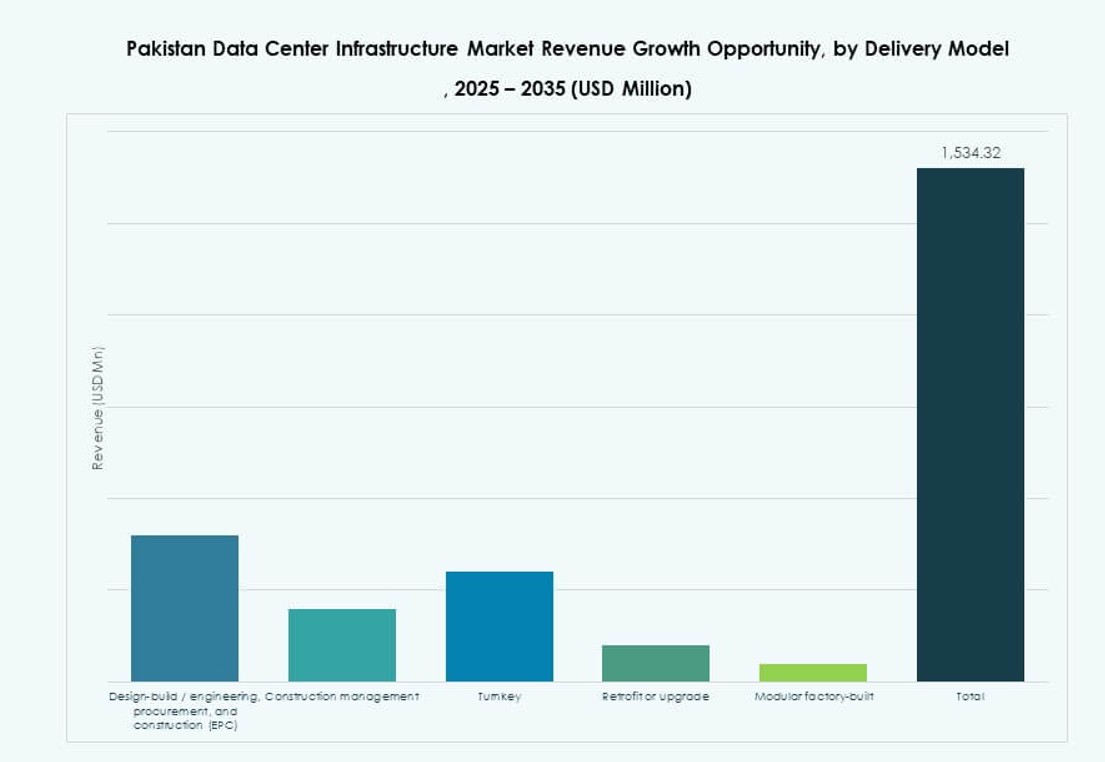

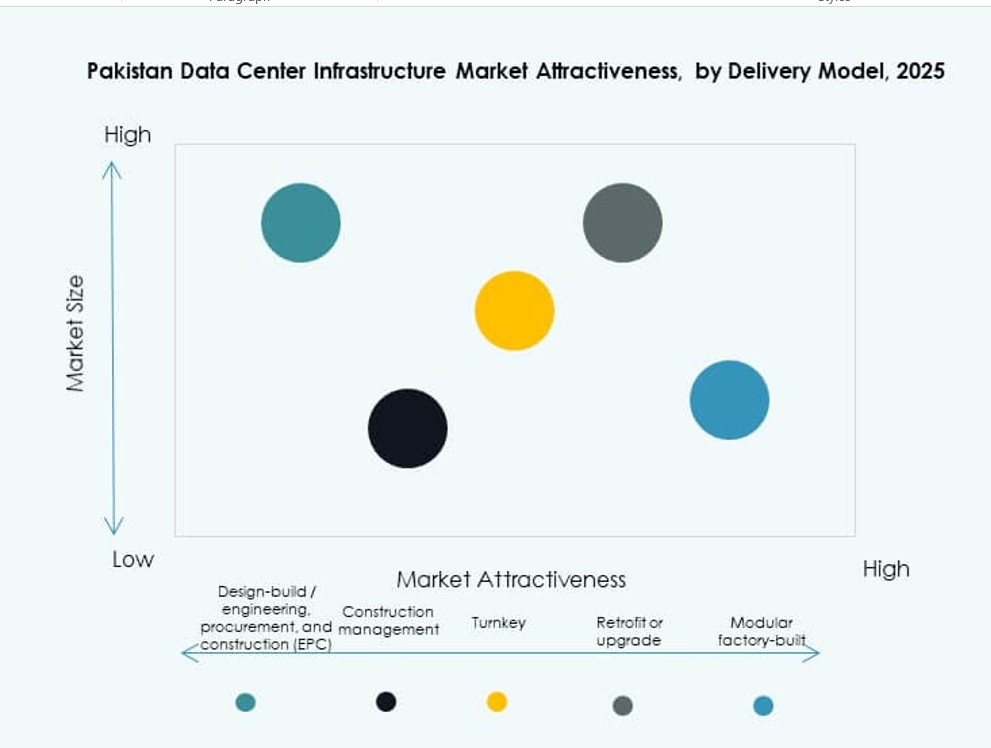

By Delivery Model

Turnkey and modular factory-built models are gaining share due to reduced lead times. Design-build and EPC still dominate large-scale projects in metro cities. Retrofit and upgrade demand is growing among banks and telecoms. The [Pakistan Data Center Infrastructure Market] shifts toward plug-and-play models for edge deployment. Construction management remains relevant for legacy site expansion.

By Tier Type

Tier III facilities dominate the [Pakistan Data Center Infrastructure Market] with demand for redundant systems and operational flexibility. Tier II is used for DR and edge deployments in secondary cities. Tier IV adoption is limited but growing among financial institutions. Tier I usage is phasing out due to limited resilience. Operators prioritize certifications to meet SLA demands.

Regional Insights

Karachi Region Leads with Over 40% Share Due to Its Strategic Role in Connectivity and Finance

Karachi is the dominant hub for large-scale data centers in Pakistan. Its coastal location and access to submarine cable landing stations support global connectivity. Financial institutions, telecoms, and government entities drive demand for secure infrastructure. The Pakistan Data Center Infrastructure Market sees over 40% share concentrated in Karachi. Growing e-commerce, fintech, and media companies further boost infrastructure investments. Energy supply constraints are offset through private power and backup systems. Carrier-neutral facilities in Karachi support multi-tenant use and cloud hosting.

- For instance, PTCL’s Tier III certified campus in Karachi hosts primary transaction engines for United Bank Limited and the State Bank of Pakistan. Growing e-commerce, fintech, and media companies further boost infrastructure investments.

Lahore Region Holds Around 30% Market Share with Strong Enterprise and Education Clusters

Lahore has a growing ecosystem of enterprise, IT services, and academic institutions. The region supports mid-sized colocation and enterprise data centers. The Pakistan Data Center Infrastructure Market sees 30% contribution from Lahore due to telecom innovation and government projects. Business parks and technology zones attract data-driven startups and public platforms. Expansion of smart city initiatives further increases infrastructure demand. Proximity to central Punjab allows deployment of DR sites and training centers.

Islamabad Capital Region and Secondary Cities Contribute Around 30% Through Government and Edge Deployments

Islamabad hosts several public sector, regulatory, and cloud-first government initiatives. The Pakistan Data Center Infrastructure Market sees the remaining 30% share distributed across Islamabad, Faisalabad, Multan, and Quetta. These cities support edge data centers, disaster recovery, and localized storage hubs. Public cloud adoption in education and healthcare accelerates demand. Infrastructure in these zones focuses on modularity and regional compliance. Data center investments in SEZs outside core metro areas show early-stage momentum.

- For instance, Jazz Digital Park in Islamabad operates as a Tier III facility with 3 MW power capacity and over 300 racks.

Competitive Insights:

- Delta Electronics

- IBM

- ABB

- Cisco Systems, Inc.

- Dell Inc.

- Equinix, Inc.

- KIO

- Oracle

- Schneider Electric

- Vertiv Group Corp.

The Pakistan Data Center Infrastructure Market features a blend of global tech giants and regional specialists. Vertiv, Schneider Electric, and Delta Electronics lead the electrical and mechanical infrastructure segment through strong UPS, cooling, and power system portfolios. IBM, Oracle, and Dell dominate the IT and network infrastructure space, enabling digital transformation across telecom and enterprise sectors. Equinix and KIO support the colocation segment, offering carrier-neutral interconnection hubs. Cisco drives innovation in network security and automation, addressing cloud-first and hybrid models. The market is competitive, with companies focusing on energy efficiency, modularity, and scalable architecture. Strong vendor-client partnerships, integration expertise, and localized delivery remain key differentiators across the infrastructure lifecycle.

Recent Developments:

- In December 2025, US-based data-center operator Datarocx partnered with Pakistan’s Data Vault to establish advanced computing facilities in Karachi, enhancing high-performance infrastructure for the market.

- In October 2025, XDS DATACENTRE and Al Nahal IT Park & Data Center signed an agreement at GITEX Global to develop Pakistan’s first AI Liquid Immersion Data Centre in Karachi, featuring a disaster recovery site and containerized solutions for rapid AI compute access.