Executive summary:

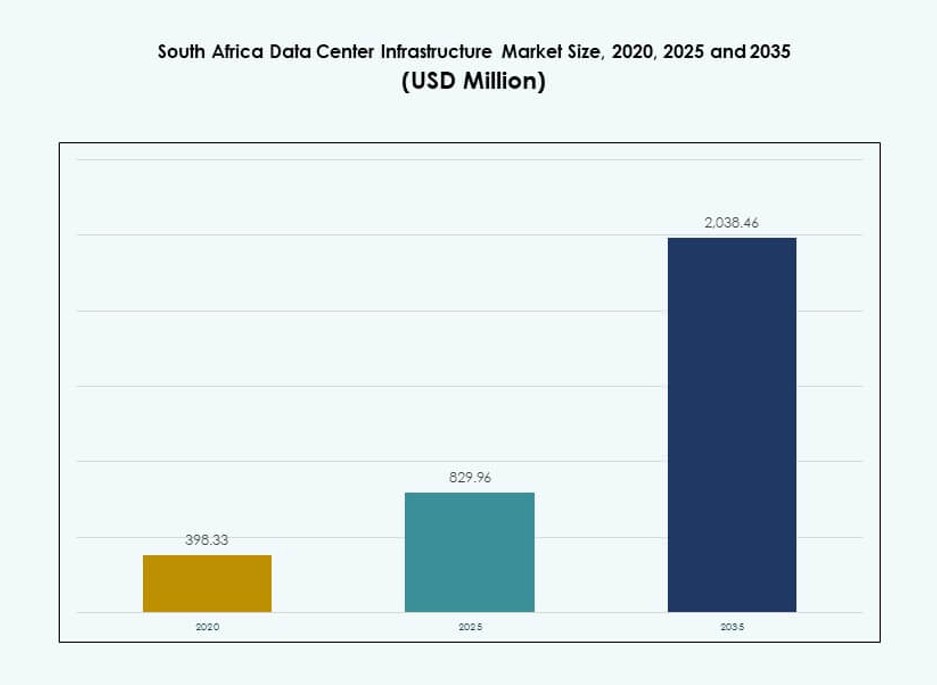

The South Africa Data Center Infrastructure Market size was valued at USD 398.33 million in 2020, reached USD 829.96 million in 2025, and is anticipated to reach USD 2,038.46 million by 2035, at a CAGR of 9.30% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| South Africa Data Center Infrastructure Market Size 2025 |

USD 829.96 Million |

| South Africa Data Center Infrastructure Market, CAGR |

9.30% |

| South Africa Data Center Infrastructure Market Size 2035 |

USD 2,038.46 Million |

The market is growing steadily due to a surge in cloud adoption, digital transformation, and enterprise outsourcing across key sectors. Investments in AI-ready infrastructure, high-density racks, and smart energy systems are reshaping facility design. Data localization laws and rising demand for real-time analytics are pushing regional capacity buildout. Energy efficiency, low-latency networks, and modular deployments are now critical for investor and operator decisions. The South Africa Data Center Infrastructure Market serves as a strategic digital bridge for pan-African services.

Gauteng, especially Johannesburg, leads the market due to strong enterprise concentration and fiber availability. Western Cape is gaining traction with hyperscale interest and renewable energy sources. KwaZulu-Natal and Eastern Cape are emerging with demand from e-government, banking, and telecom sectors. These subregions reflect different stages of maturity, influenced by infrastructure readiness, investment flow, and data connectivity corridors. The geographic spread supports growth beyond Tier I cities.

Market Dynamics:

Market Drivers

Rising Cloud Penetration and Digital-First Enterprise Transformation Across Core Industries

South Africa’s enterprise ecosystem is undergoing a digital shift driven by cloud-first policies and remote work needs. Financial services, healthcare, and retail industries are migrating workloads to local and regional data centers. Public cloud adoption and demand for hybrid cloud deployments are triggering new infrastructure investments. The South Africa Data Center Infrastructure Market is leveraging this shift with purpose-built facilities and multi-cloud integration systems. Local enterprises are forming strategic alliances with hyperscalers for low-latency delivery. The rise in SaaS, PaaS, and IaaS models continues to generate sustained infrastructure demand. Global providers such as AWS, Microsoft, and Huawei are expanding regional availability zones. This trend positions South Africa as a vital hub for Southern African cloud ecosystems.

- For instance, Microsoft announced a USD 300 million investment in 2025 for cloud and AI infrastructure expansion in Gauteng by 2027, strengthening its South Africa North and West regions.

Next-Gen Power and Cooling Integration Supporting Energy-Efficient Hyperscale Deployments

Efficiency remains a primary design criterion for modern data centers in South Africa. Infrastructure suppliers are deploying modular UPS systems, high-efficiency BESS, and liquid-cooled systems. The need for sustainable energy use is prompting use of grid-tied renewable sources and real-time PUE optimization tools. The South Africa Data Center Infrastructure Market is advancing toward green certification standards. Operators are actively upgrading existing facilities to comply with ESG mandates. Hyperscale players are building new facilities that meet edge-scale performance and high energy-density requirements. Investment in solar-backed microgrids and smart switchgear drives operational efficiency. These developments support long-term reliability and lower lifecycle costs for stakeholders.

- For instance, Vantage Data Centers partnered with Attacq for Phase II of an 80MW campus in Johannesburg, incorporating advanced power systems. Infrastructure suppliers are deploying modular UPS systems, high-efficiency BESS, and liquid-cooled systems.

Strategic Positioning as a Continental Digital Gateway Attracting Foreign Direct Investment

South Africa’s geographic and submarine cable connectivity positions it as a digital transit point between Africa, Europe, and Asia. Government support for ICT development and data localization laws increases the investment appeal. The South Africa Data Center Infrastructure Market benefits from a growing pipeline of foreign-backed hyperscale and colocation projects. Regional headquarters of multinational corporations depend on secure and scalable IT infrastructure. International financial institutions and cloud-native startups are also contributing to rising demand. The digital services boom is prompting cloud vendors to locate infrastructure closer to end users. Telecom operators and infrastructure REITs are leveraging this to expand their data center portfolios. FDI inflows are expected to intensify as demand shifts toward high-availability computing.

Growth in AI, Big Data, and High-Performance Computing Requirements Across Business Verticals

AI and machine learning workloads are influencing rack power density, thermal management, and network latency requirements. South Africa’s tech startups and universities are running pilot projects in AI-driven healthcare, fintech, and logistics. The South Africa Data Center Infrastructure Market is adapting through high-core servers, low-latency fiber systems, and edge computing platforms. Infrastructure suppliers are offering AI-ready cooling units, structured cabling, and high-speed switches. Government AI policies are encouraging adoption of HPC platforms and data localization. Telecom providers are launching edge nodes to handle real-time data processing from IoT and 5G devices. These shifts are pushing infrastructure toward AI-native configurations and compute-intensive architectures. The market is entering a phase of vertical-specific infrastructure design and deployment.

Market Trends

Increased Adoption of Prefabricated and Modular Data Center Systems for Fast Deployment

Modular and prefabricated data centers are gaining preference due to faster deployment timelines and scalability. Stakeholders are choosing modular electrical and mechanical components to reduce construction time and lower CAPEX. The South Africa Data Center Infrastructure Market is seeing strong momentum in modular factory-built and retrofit projects. Enterprises demand rapid site commissioning to meet growing digital service needs. Vendors are offering containerized power and cooling units for edge and mid-tier deployments. EPC and turnkey firms are using BIM and digital twin tools to speed up execution. Flexibility in adding capacity over time supports long-term investment. This trend meets rising expectations for adaptable, efficient, and location-flexible designs.

High Rack Power Density and Server Consolidation Driving Data Hall Redesigns

The demand for compute-intensive workloads such as AI, analytics, and simulation is driving up rack power density. Facilities are being redesigned with higher kW/rack ratings, improved air and liquid cooling, and denser server configurations. The South Africa Data Center Infrastructure Market is evolving to support racks rated at 15 kW and beyond. Operators are phasing out legacy systems in favor of compact, high-performance hardware. Power and cooling systems are reconfigured to ensure balanced airflow and thermal zoning. Modern racks and enclosures come with integrated cable management and real-time monitoring. These redesigns help operators manage energy costs, maintain uptime, and meet customer SLAs.

Expansion of Edge Data Centers and Distributed Architecture to Support Latency-Sensitive Applications

Demand for local data processing, driven by 5G and IoT applications, is prompting interest in edge data centers. Telecom and content delivery firms are rolling out mini facilities near population centers and industrial zones. The South Africa Data Center Infrastructure Market is witnessing strong growth in distributed deployments beyond Tier I cities. Edge facilities require rugged infrastructure, modular power units, and compact cooling systems. These centers support real-time services such as video analytics, e-health, and smart logistics. Partnerships between ISPs and infrastructure vendors are enabling faster rollouts. By deploying edge nodes, service providers reduce backhaul loads and meet latency targets. This trend supports new revenue models and broader regional coverage.

Shift Toward Liquid-Based and Immersive Cooling Systems for Thermal Efficiency Gains

Growing compute intensity is outpacing the limits of traditional CRAC and CRAH systems. Operators are turning to direct-to-chip liquid cooling and immersion cooling technologies. The South Africa Data Center Infrastructure Market is seeing pilot projects for two-phase cooling and dielectric fluid systems. Data centers with HPC and AI workloads are the first movers for such adoption. Suppliers are offering integrated systems with leak detection, redundancy, and compact footprint. This trend is aligned with sustainability goals and local temperature management needs. Lower energy usage and extended hardware life make these solutions viable. Adoption is expected to grow with maturing standards and vendor certifications.

Market Challenges

Energy Reliability Concerns and Grid Instability Impacting Facility Uptime and Expansion Plans

South Africa faces persistent grid instability, load shedding, and limited renewable integration. This forces data center operators to invest heavily in diesel gensets and backup power systems. The South Africa Data Center Infrastructure Market is constrained by high energy costs and frequent power disruptions. Energy insecurity increases operational expenditure and deters hyperscale investments. Delays in connecting to reliable utility infrastructure prolong project timelines. BESS deployment helps but remains cost-intensive and complex. Government efforts to liberalize energy procurement are underway but progress remains uneven. Operators need to balance sustainability with availability and uptime commitments to clients.

Regulatory and Zoning Bottlenecks Slowing Down Construction and Market Entry

Building new data centers requires navigating complex regulatory frameworks and municipal zoning codes. Environmental impact clearances and urban development permits often delay construction starts. The South Africa Data Center Infrastructure Market faces red tape in land acquisition, construction approvals, and cross-border data policies. Smaller municipalities lack technical expertise to support large-scale ICT projects. Foreign players face uncertainties around local equity mandates and operational approvals. Delays in fiber licensing and subsea cable landing permits affect timeline certainty. These factors limit scalability and increase risk for new market entrants.

Market Opportunities

Expansion of Subsea Cable Infrastructure Unlocking Regional Connectivity and Data Transit Growth

South Africa’s strategic location at the junction of major submarine cables positions it as a key digital corridor. New cables such as 2Africa and Equiano boost bandwidth and reduce latency to Europe and Asia. The South Africa Data Center Infrastructure Market is set to benefit from this improved international connectivity. This supports growth in fintech, content streaming, and cross-border cloud services. Data sovereignty laws in neighboring countries make South Africa a preferred hosting hub.

Rising Demand for Secure Colocation from Enterprises and Government Sector

Enterprises across banking, healthcare, and public services seek secure and compliant colocation environments. The South Africa Data Center Infrastructure Market gains from growing interest in off-premises hosting. Colocation reduces IT maintenance burden while ensuring data protection. Increasing cyber threats and evolving compliance norms drive this migration. High-specification Tier III and Tier IV facilities with on-site security are favored.

Market Segmentation

By Infrastructure Type

Electrical infrastructure dominates due to its foundational role in ensuring continuous uptime. It commands the highest share in the South Africa Data Center Infrastructure Market due to demand for resilient power systems. Mechanical infrastructure follows, supporting effective cooling in dense data environments. IT and network infrastructure segments gain traction from digital transformation and cloud adoption. Civil and architectural systems remain vital in modular and retrofit projects. Integration across all these layers drives complete facility readiness.

By Electrical Infrastructure

UPS and power distribution units (PDUs) hold major share, driven by redundancy and load balancing needs. BESS adoption is accelerating due to power reliability issues. Grid connection investments remain essential in new build projects. Transfer switches and switchgears support power routing during grid failures. The South Africa Data Center Infrastructure Market shows rising demand for scalable and modular electrical systems. Energy efficiency standards are pushing upgrades across legacy facilities.

By Mechanical Infrastructure

CRAC/CRAH units continue to dominate mechanical infrastructure deployment due to established reliability. Chillers, especially air-cooled, are favored in cost-sensitive deployments. Containment systems gain adoption to manage airflow and reduce energy loss. Pumps and piping systems support liquid-based and advanced cooling models. Mechanical infrastructure is evolving to support higher density workloads and reduce operational energy costs.

By Civil / Structural & Architectural

Modular and prefabricated building systems are gaining preference for their deployment speed and lower cost. Superstructures using steel or concrete frames dominate in large-scale builds. Site preparation and foundations remain cost-intensive but crucial. Building envelope upgrades are key for thermal insulation and energy efficiency. Raised floors and suspended ceilings support flexible airflow and cabling. Civil infrastructure ensures the facility’s long-term structural integrity.

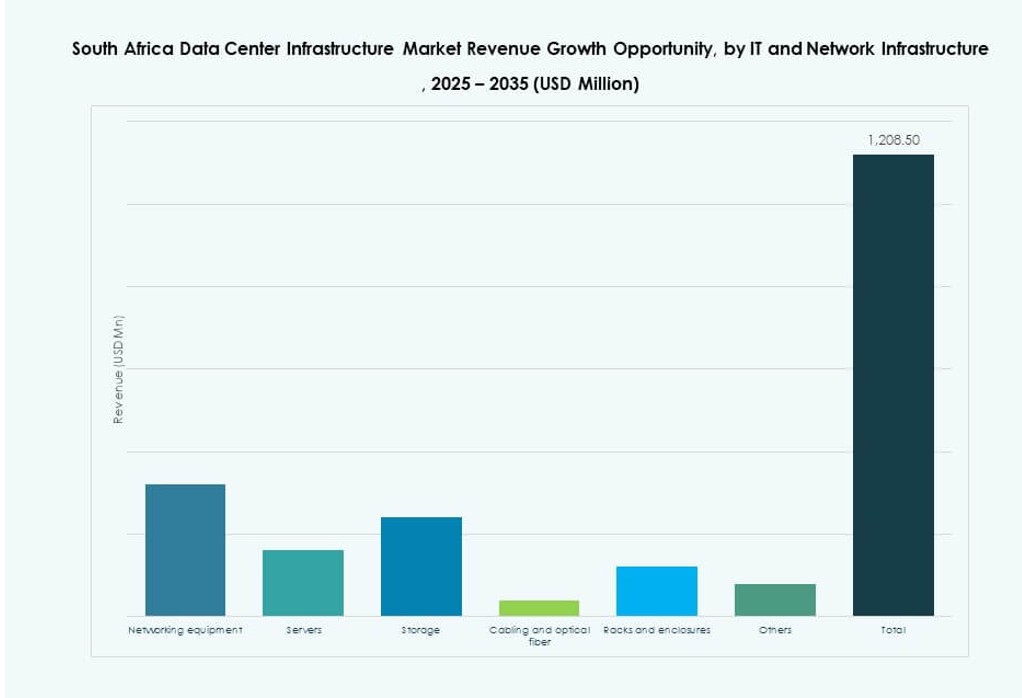

By IT & Network Infrastructure

Servers and storage dominate spend due to compute-heavy applications and cloud adoption. Networking gear and optical cabling ensure seamless connectivity across racks. Racks and enclosures are evolving to support high-density hardware and improved airflow. The South Africa Data Center Infrastructure Market supports rising demand for scalable, high-performance IT systems. Structured cabling and software-defined storage gain interest in enterprise builds.

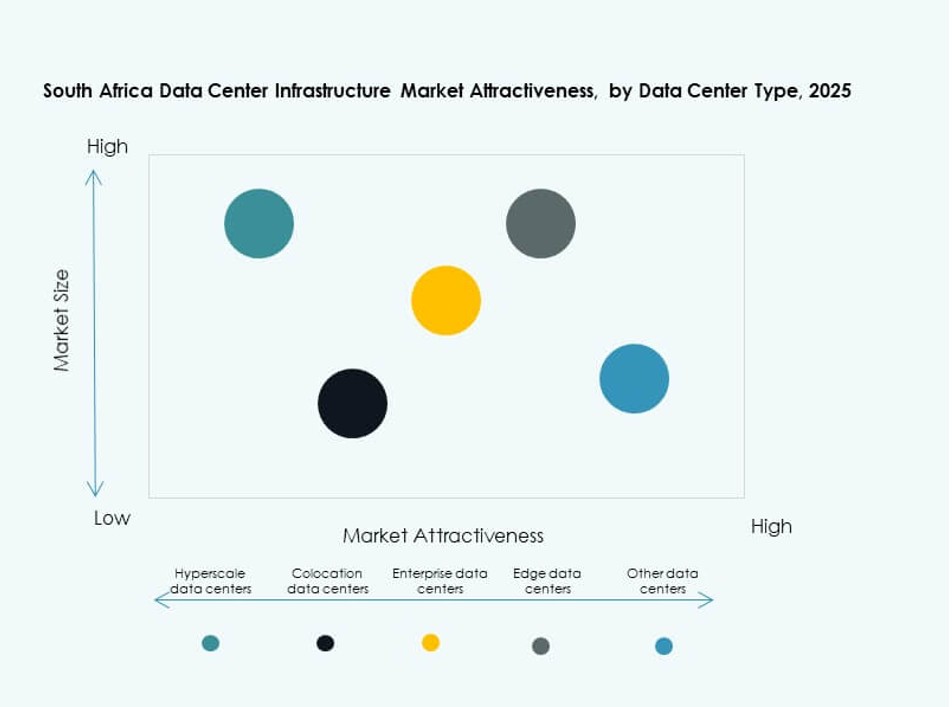

By Data Center Type

Colocation data centers hold a leading share, supported by enterprise outsourcing. Hyperscale facilities are expanding through global vendor entry and rising cloud workloads. Enterprise data centers maintain relevance in regulated sectors. Edge data centers gain share for local content delivery and IoT deployments. The market supports a hybrid mix tailored to client scale and application needs.

By Delivery Model

Turnkey and modular factory-built models are leading due to ease of deployment and cost savings. Design-build remains active in large-scale and greenfield projects. Retrofit and upgrade models cater to aging legacy facilities. The South Africa Data Center Infrastructure Market sees growing use of construction management models in complex urban deployments.

By Tier Type

Tier III facilities dominate due to balance of cost, availability, and compliance. Tier IV adoption is growing for mission-critical and high-security needs. Tier I and II see limited use in edge and non-critical facilities. The South Africa Data Center Infrastructure Market prioritizes uptime certifications to gain enterprise and cloud customer trust.

Regional Insights

Gauteng Province Leads with Over 58% Market Share Due to Fiber Access and Business Demand

Gauteng remains the epicenter of data center activity, driven by Johannesburg’s robust enterprise landscape. Major operators prefer the region for its skilled labor, existing connectivity, and strong utility infrastructure. The South Africa Data Center Infrastructure Market relies heavily on this subregion for hyperscale and colocation developments. High concentration of banks, telecoms, and cloud firms sustains demand. Government projects and digital startups contribute to the ecosystem. Real estate availability and favorable policies enable steady pipeline growth.

- For instance, Teraco completed JB5, a 30MW hyperscale facility with 12 data halls of 1,000 sqm each at its Isando campus, enabling zero water usage for cooling via 100% free air cooling.

Western Cape Emerges as a Secondary Hub Backed by Green Power and Coastal Access

The Western Cape accounts for nearly 21% market share, with Cape Town becoming a hub for hyperscale entry. The region attracts investment due to its cooler climate, access to renewables, and submarine cable landing points. The South Africa Data Center Infrastructure Market sees consistent traction here from cloud firms and fintech startups. Local policies supporting tech clusters and green buildings drive further interest. Port infrastructure aids equipment imports for large-scale construction.

KwaZulu-Natal and Eastern Cape Show Early-Stage Growth with Enterprise and Public Sector Demand

KwaZulu-Natal and Eastern Cape collectively represent around 14% of the market and show potential in enterprise and e-government projects. Durban is emerging as a localized hosting option for regional industries. Smaller colocation and edge data center projects are planned to serve growing urban populations. The South Africa Data Center Infrastructure Market identifies these regions as strategic for edge rollouts and regional redundancy. Growth depends on public-private partnerships and infrastructure incentives.

- For instance, Teraco completed expansion of its Durban DB1 facility, doubling capacity to support over 700 racks across 5,800 sqm. Durban is emerging as a localized hosting option for regional industries.

Competitive Insights:

- Digital Realty

- Equinix, Inc.

- Teraco (Digital Realty)

- Huawei Technologies Co., Ltd.

- Schneider Electric

- Vertiv Group Corp.

- Dell Inc.

- Hewlett Packard Enterprise (HPE)

- Cisco Systems, Inc.

- IBM

The South Africa Data Center Infrastructure Market features a competitive mix of global giants and regional players. Digital Realty and Equinix lead in hyperscale and colocation capacity. Teraco holds strong domestic presence, offering interconnection-rich campuses. Infrastructure vendors like Huawei, Schneider Electric, and Vertiv deliver critical power, cooling, and monitoring systems. HPE, Dell, Cisco, and IBM supply servers, storage, and network gear to enterprise and cloud data centers. The market favors integrated service portfolios, energy-efficient systems, and regional expansion strategies. Players compete on uptime, compliance, and low-latency delivery capabilities. Strategic alliances with telecoms and renewable energy providers shape new projects. Competitive pressure is high, driven by rising demand and limited premium data center land.

Recent Developments:

- In November 2024, Digital Realty, through its subsidiary Teraco, announced the start of construction on the JB7 data center in South Africa, featuring 40 MW of IT load capacity with liquid-to-air and liquid-to-liquid cooling designs to support AI deployments.

- In October 2024, Equinix announced the launch of JINX, the Johannesburg Internet Exchange, within its new South Africa data center in Johannesburg to enhance connectivity.