Executive summary:

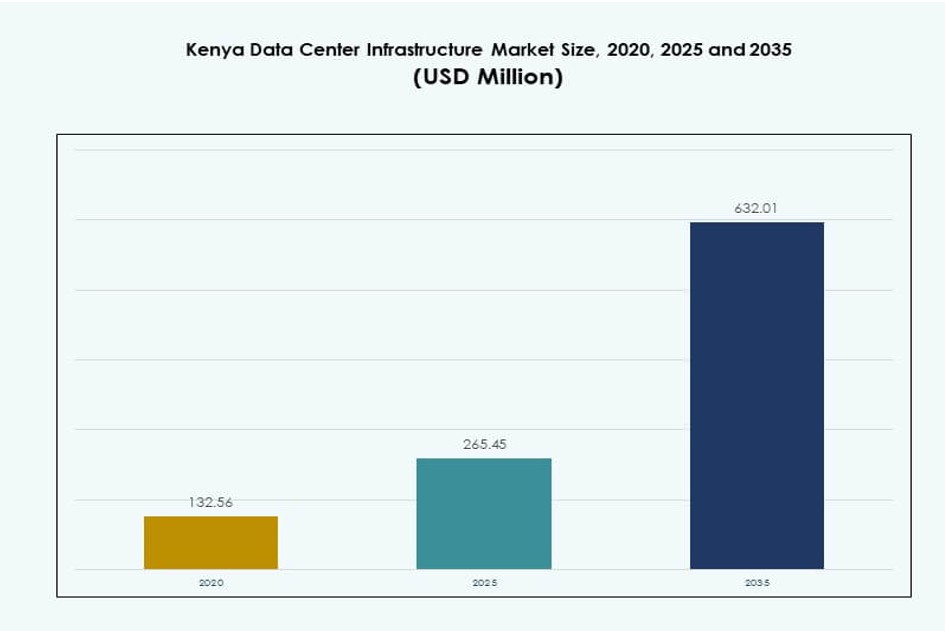

The Kenya Data Center Infrastructure Market size was valued at USD 132.56 million in 2020 to USD 265.45 million in 2025 and is anticipated to reach USD 632.01 million by 2035, at a CAGR of 8.90% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Kenya Data Center Infrastructure Market Size 2025 |

USD 265.45 Million |

| Kenya Data Center Infrastructure Market, CAGR |

8.90% |

| Kenya Data Center Infrastructure Market Size 2035 |

USD 632.01 Million |

Rapid digitalization across government and enterprise sectors is driving demand for reliable and scalable infrastructure. Companies are adopting cloud platforms, edge computing, and modular designs to meet evolving IT requirements. Innovations in power and cooling systems, along with regulatory support, are improving investment confidence. The market serves as a strategic digital gateway for East Africa. Growing demand for secure data hosting and AI-ready facilities positions the country as a vital hub. Telecom and fintech sectors are expanding local compute needs. Investors benefit from strong ROI potential. The infrastructure shift supports business continuity and regional leadership.

Nairobi leads the market due to dense enterprise presence, robust connectivity, and regulatory readiness. It attracts hyperscale, colocation, and cloud providers targeting both domestic and regional clients. Mombasa is emerging due to its subsea cable landings and role as a content distribution point. Secondary cities such as Kisumu and Eldoret are gaining traction with modular edge deployments. Their growth is supported by digital inclusion programs and government ICT initiatives. Kenya’s strategic location enhances cross-border data flow. The country’s expanding ecosystem is fueling multi-region infrastructure adoption.

Market Dynamics:

Market Drivers

Surging Digitalization Across Government and Enterprise Sectors Spurs Infrastructure Demand

The Kenya Data Center Infrastructure Market is expanding as government and private sectors digitize operations. Ministries are rolling out digital services requiring secure local hosting. Enterprises adopt hybrid IT setups to improve agility and data localization. Telecom operators and banks seek high-performance infrastructure to support core applications. The shift to digital-first operations supports demand for Tier III and Tier IV facilities. Rising e-governance adoption increases reliance on reliable compute environments. Public cloud service demand creates pressure for colocation and hyperscale builds. Growth in fintech, e-commerce, and telecom also expands infrastructure requirements. It is becoming a core enabler of national digital transformation goals.

- For instance, Kenya’s Digital Superhighway program expanded the national fiber optic network to 13,590 km by 2025 from 8,900 km in 2022, enabling low-latency cloud access for ministries. Ministries are rolling out digital services requiring secure local hosting.

Rapid Cloud Service Adoption and Rising Data Volumes Drive Capacity Expansions

Cloud computing is reshaping digital infrastructure needs across Kenya’s enterprises. Local firms embrace SaaS, IaaS, and PaaS models for scalability and cost control. Rising digital service usage across sectors results in growing data volumes. Secure and low-latency infrastructure is necessary to host workloads regionally. Global and regional cloud providers are forming joint ventures and investing in in-country deployments. New data centers are being built with cloud-native features and modular architecture. AI-driven automation improves facility management and reduces downtime. The Kenya Data Center Infrastructure Market supports future-ready platforms to attract enterprise and hyperscale tenants. It offers long-term strategic value for cloud and tech investors.

- For instance, Nxtra by Airtel Africa broke ground on East Africa’s largest data center in Tatu City, Kenya, with 44MW IT capacity designed for cloud workloads.

Strategic Importance of Data Sovereignty and Compliance Shapes Facility Buildout

Data sovereignty regulations influence how and where companies store and process data. Kenya’s data protection laws mandate sensitive data localization and stronger privacy compliance. This encourages firms to adopt local hosting and colocation solutions for audit readiness. Critical sectors such as health, finance, and telecom must align with evolving policies. The infrastructure must support compliance, security protocols, and operational transparency. Investors prioritize facilities that meet certification and tier requirements. The Kenya Data Center Infrastructure Market enables businesses to operate within regulatory frameworks efficiently. It positions Kenya as a data gateway for Eastern Africa.

Innovation in Power and Cooling Infrastructure Optimizes Energy Efficiency and Uptime

Infrastructure innovation drives efficiency gains across power and cooling systems. Energy-efficient UPS, smart PDUs, and lithium-ion BESS improve sustainability and uptime. Liquid and in-row cooling reduce power usage and heat loads in high-density racks. Operators implement N+1 or 2N redundancy models for power backup assurance. Green energy integration lowers total operational cost. Modular builds allow phased expansion based on demand. AI and DCIM tools optimize energy use and facility operations. The Kenya Data Center Infrastructure Market supports these innovations, aligning with environmental and uptime standards. It enables operators to serve mission-critical workloads with reliability.

Market Trends

Rise of Carrier-Neutral Facilities Supporting Multi-Tenant and Cross-Connect Needs

Carrier-neutral data centers are growing as enterprises seek flexible network options. Telecom disaggregation and peering requirements drive demand for neutral colocation hubs. Businesses prefer facilities offering cross-connectivity to multiple network and cloud providers. Carrier-neutral sites support improved latency and reduced data transit cost. They serve as regional internet exchange points and content delivery hubs. This trend strengthens data center role in Kenya’s digital value chain. The Kenya Data Center Infrastructure Market benefits from demand for agile, high-speed connections. It drives investments in open-access architectures and connectivity-rich sites.

Deployment of Edge Data Centers to Support Latency-Sensitive Applications

Edge computing is gaining traction with increased demand for low-latency services. Applications like IoT, mobile payments, and video streaming require regional data processing. Edge data centers bring compute power closer to users and devices. Regional cities and economic zones see new deployments of micro or modular edge sites. Energy-efficient and containerized designs allow quick rollout. Smart city developments integrate edge data centers for real-time analytics. The Kenya Data Center Infrastructure Market supports this shift to localized infrastructure. It ensures service continuity for latency-sensitive applications.

Adoption of Liquid Cooling Technologies to Meet High-Density Rack Needs

High-performance workloads increase rack densities and thermal output. Traditional air-cooling systems become inefficient at scale. Operators adopt liquid-cooled racks, immersion cooling, and rear-door heat exchangers. These solutions support AI, machine learning, and analytics workloads. Cooling upgrades reduce energy consumption and improve PUE. Facilities integrate predictive maintenance for cooling systems to avoid outages. Kenya’s climate and energy context favor adoption of efficient thermal management. The Kenya Data Center Infrastructure Market responds with advanced mechanical infrastructure designs.

Focus on Modular Construction and Prefabricated Solutions for Faster Deployment

Speed-to-market has become a critical factor in data center expansion plans. Modular construction and prefabricated units reduce build time and labor cost. Standardized modules improve quality control and simplify regulatory approvals. Operators use containerized solutions for edge, enterprise, and rapid deployment use cases. Phased capacity expansion allows better capital allocation. Facilities with plug-and-play power and cooling modules gain preference. This trend reshapes how facilities are designed and built in Kenya. The Kenya Data Center Infrastructure Market benefits from demand for flexible, scalable construction models.

Market Challenges

Limited Power Grid Capacity and Energy Stability Constraints Impact Facility Uptime

Kenya faces recurring challenges related to power stability and grid limitations. Data centers require high power availability with redundancy to meet uptime needs. Grid outages, voltage fluctuations, and energy cost spikes increase OPEX risks. Backup diesel generators raise environmental and operational concerns. Limited access to clean and consistent energy deters hyperscale investments. Renewable energy integration faces slow permitting and regulatory delays. Infrastructure operators must invest heavily in on-site energy and battery storage. The Kenya Data Center Infrastructure Market must navigate these constraints to meet tier uptime standards. It increases the cost and complexity of maintaining consistent power supply.

Skilled Workforce Shortage and Regulatory Complexity Affect Project Timelines

Kenya’s data center industry suffers from limited availability of specialized technical talent. Key roles in electrical engineering, HVAC systems, and facility operations face talent shortages. Operators depend on foreign expertise during build and commissioning phases. Regulatory compliance adds another layer of complexity, slowing permitting and inspections. Building codes, fire safety norms, and zoning issues vary by region. Delays in approvals extend project timelines and inflate cost. The Kenya Data Center Infrastructure Market must invest in workforce training and policy harmonization. It creates barriers for new entrants and slows ecosystem growth.

Market Opportunities

Expansion of Subsea Cable Connectivity Strengthens Kenya’s Role as a Regional Hub

Kenya is emerging as a landing point for major subsea cable systems. This expands its bandwidth capacity and positions it as a regional interconnect zone. Enhanced connectivity reduces latency for East and Central Africa. Local data centers benefit from improved international throughput. The Kenya Data Center Infrastructure Market gains from this strategic geographic location. It enables facilities to serve cross-border clients and content networks. Investors see long-term value in gateway infrastructure development.

Government Incentives and Digital Policy Support Encourage Infrastructure Investments

Kenya’s government promotes ICT sector development through tax incentives and policy frameworks. Data localization laws, digital economy blueprints, and export processing zone benefits support data center expansion. Public-private partnerships boost investor confidence. Local government initiatives offer land, energy subsidies, and regulatory fast-tracking. The Kenya Data Center Infrastructure Market is positioned to attract infrastructure capital. It offers growth opportunities for both domestic and international operators.

Market Segmentation

By Infrastructure Type

The Kenya Data Center Infrastructure Market is dominated by electrical and IT & network infrastructure segments. Electrical infrastructure supports critical functions like UPS, BESS, and switchgears, ensuring power reliability. IT & network infrastructure sees demand from server and storage upgrades across enterprises. Mechanical infrastructure is growing with advanced cooling needs, especially for AI and cloud workloads. Civil/structural systems adopt modular design to improve scalability. Demand for prefabricated systems grows due to reduced deployment time. Other infrastructure includes monitoring tools and building management systems.

By Electrical Infrastructure

Uninterruptible power supply (UPS) and power distribution units (PDUs) hold the highest share in this segment. UPS adoption grows due to power reliability issues and uptime requirements. Lithium-ion battery systems are gaining ground over traditional VRLA models. PDUs with smart monitoring features help optimize energy use. Switchgears and transfer switches support N+1 and 2N redundancy standards. Utility grid connections are challenged by unstable power supply. The Kenya Data Center Infrastructure Market sees demand for on-site solar and hybrid power systems under “others”.

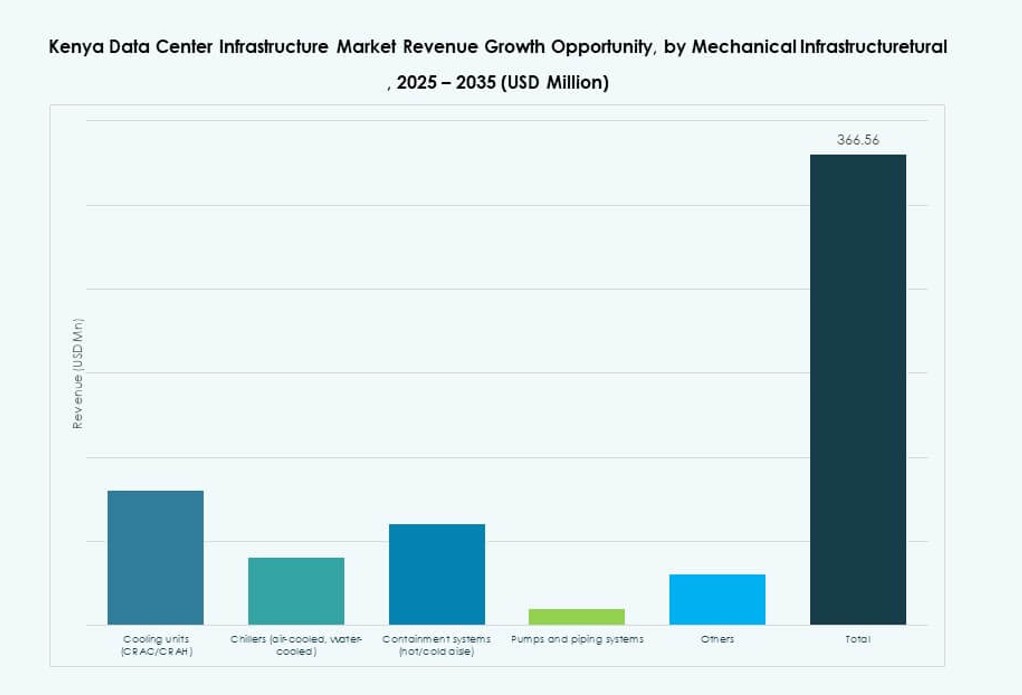

By Mechanical Infrastructure

Cooling units and containment systems dominate mechanical infrastructure in Kenya’s data centers. CRAC/CRAH units remain standard, while chilled water systems grow in hyperscale builds. Containment systems enhance airflow management and energy efficiency. Pumps and piping infrastructure enable heat exchange operations. Energy-saving cooling strategies like free-air cooling remain limited by climatic constraints. Liquid cooling gains traction for high-density zones. The Kenya Data Center Infrastructure Market supports mechanical innovation to meet performance and sustainability benchmarks.

By Civil / Structural & Architectural

Modular and prefabricated building systems lead due to speed and cost advantages. Superstructure builds use steel frames for flexibility and rapid assembly. Site preparation remains vital for foundation stability, especially in seismic zones. Raised floors and suspended ceilings aid airflow and cable routing. Building envelopes are designed to reduce thermal gain. Demand for scalable, repeatable designs drives adoption. The Kenya Data Center Infrastructure Market adapts civil engineering approaches for Tier III and IV requirements.

By IT & Network Infrastructure

Networking equipment and server segments dominate due to high-speed data needs. Storage infrastructure is expanding with local cloud and big data deployments. Optical fiber and cabling see upgrades to support higher bandwidth applications. Rack and enclosure systems adapt to high-density workloads. Kenya’s market requires robust IT infrastructure to meet digital demands. The Kenya Data Center Infrastructure Market experiences upgrades in IT assets for better compute efficiency and reliability.

By Data Center Type

Colocation data centers lead Kenya’s market, supported by demand from SMEs, telecom, and financial sectors. Enterprise data centers are built by banks and large institutions to host sensitive applications. Hyperscale adoption is nascent but expanding through international partnerships. Edge data centers are emerging to support regional service delivery. The Kenya Data Center Infrastructure Market supports hybrid data center models, offering flexibility and cost efficiency.

By Delivery Model

Turnkey and design-build/EPC models are the most preferred due to speed and integration. Modular factory-built approaches are gaining share due to rising edge deployments. Construction management sees demand in large-scale phased projects. Retrofit and upgrade models address legacy IT rooms being transformed into modern facilities. The Kenya Data Center Infrastructure Market supports multiple delivery methods based on client size and technical needs.

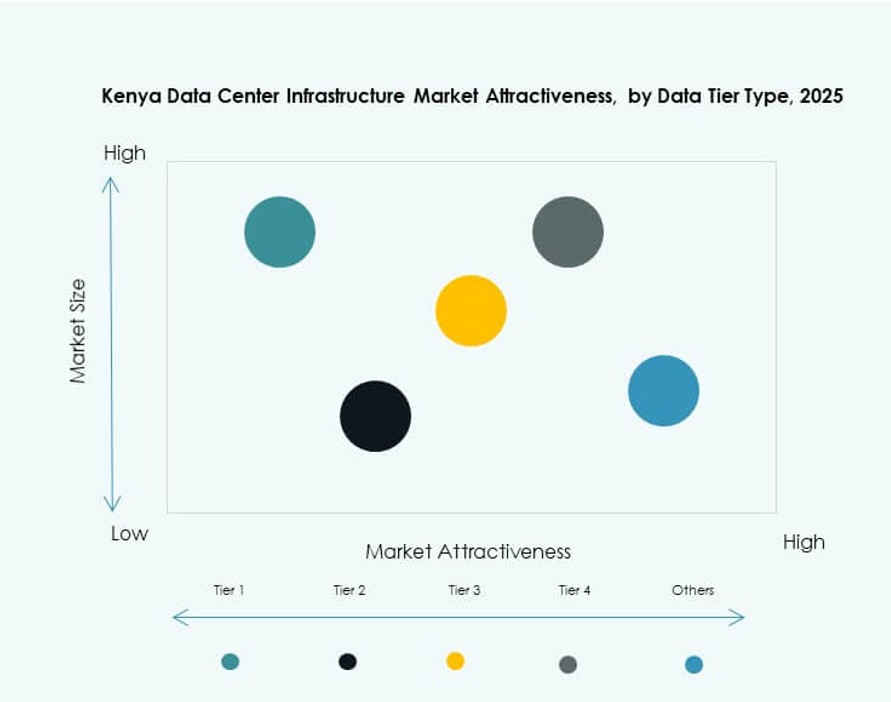

By Tier Type

Tier III data centers dominate the market due to high uptime requirements and cost efficiency. Tier II facilities serve small-scale and edge deployments with moderate availability needs. Tier IV is still limited but gaining attention from critical application providers. Tier I sites are minimal due to low fault tolerance. The Kenya Data Center Infrastructure Market increasingly focuses on Tier III upgrades with future-ready Tier IV pathways.

Regional Insights

Nairobi Metropolitan Area Leads with 68% Market Share Due to Infrastructure and Demand Concentration

Nairobi remains the core hub of the Kenya Data Center Infrastructure Market. It accounts for nearly 68% of the total market share due to strong fiber connectivity, real estate availability, and enterprise demand. The city hosts major colocation and cloud facilities driven by banks, telcos, and tech startups. Nairobi’s positioning as the economic and administrative capital supports continuous infrastructure investments. Most international operators and investors choose Nairobi as their East Africa base. It benefits from policy focus and energy access.

- For instance, IXAfrica Data Centres signed a deal in August 2023 with Tilisi Developments to purchase 11 acres of prime land for its second hyperscale data center campus in Nairobi, targeting over 30MW capacity.

Mombasa Region Emerges with 16% Share Leveraging Subsea Connectivity and Port Activity

Mombasa holds a 16% share and grows as a strategic coastal region. Its subsea cable landings support intercontinental bandwidth and peering services. Proximity to the port allows seamless logistics for modular deployments. Data centers in Mombasa serve as disaster recovery and content distribution points. The Kenya Data Center Infrastructure Market recognizes Mombasa’s role in diversifying hosting options. It also enables edge and regional expansion into the coastal belt and northern corridor.

Rest of Kenya Accounts for 16% Share Driven by Edge Deployments and Public Initiatives

Secondary cities and rural zones contribute the remaining 16% of the market. Counties like Kisumu, Eldoret, and Nakuru see small-scale edge and enterprise data centers. Government and education sector ICT initiatives drive demand. Digital inclusion programs push infrastructure toward underserved regions. The Kenya Data Center Infrastructure Market sees regional expansion as essential for future growth. It supports broader economic inclusion and digital access across Kenya.

- For instance, Kenya had at least six Uptime Institute Tier III certified facilities by late 2025, including sites by Safaricom, iColo, and Africa Data Centres. These centers ensure 99.982% uptime through N+1 power and cooling redundancy, supporting high-availability operations.

Competitive Insights:

- iColo

- Africa Data Centres

- Schneider Electric

- Vertiv Group Corp.

- Huawei Technologies Co., Ltd.

- Dell Inc.

- ABB

- Cisco Systems, Inc.

- Hewlett Packard Enterprise (HPE)

- IBM

The Kenya Data Center Infrastructure Market features a mix of regional facility operators and global technology providers. iColo and Africa Data Centres lead in colocation services, offering Tier III certified infrastructure across Nairobi and Mombasa. Schneider Electric, Vertiv, and ABB dominate power and cooling infrastructure through modular systems and energy-efficient designs. Huawei, Dell, Cisco, and HPE compete in the IT and network infrastructure segment with integrated server, storage, and connectivity solutions. The market remains competitive due to rising demand for cloud-ready, carrier-neutral, and scalable platforms. It supports multiple facility delivery models and tier configurations, attracting both local and international investments. Technology partnerships and service integration drive competitive differentiation. The Kenya Data Center Infrastructure Market continues to evolve as players target edge deployments, green energy adoption, and hyperscale readiness.

Recent Developments:

- In September 2025, Nxtra by Airtel Africa began construction on East Africa’s largest data centre in Tatu City, Kenya, boosting the market’s capacity amid rapid growth projections to 150 MW by 2028

- In July 2024, iXAfrica Data Centres launched East Africa’s first and largest hyperscale AI-ready data centre, NBOX1, in Nairobi, Kenya. Schneider Electric partnered to provide resilient power infrastructure, including UPS systems and EcoStruxure solutions, ensuring 99.999% uptime and sustainability goals.

- In May 2024, Microsoft and G42 announced a $1 billion initiative with the Kenyan government to build a state-of-the-art green data center in Olkaria, powered by renewable geothermal energy. This facility will support a new East Africa Cloud Region for Microsoft Azure, emphasizing digital safety and local AI development.