Executive summary:

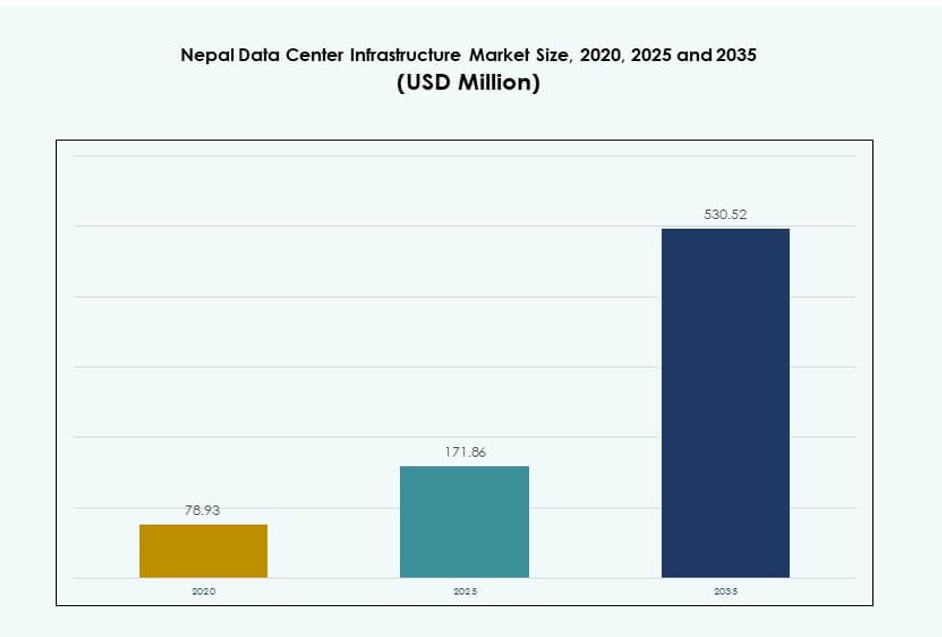

The Nepal Data Center Infrastructure Market size was valued at USD 78.93 million in 2020 to USD 171.86 million in 2025 and is anticipated to reach USD 530.52 million by 2035, at a CAGR of 11.83% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Nepal Data Center Infrastructure Market Size 2025 |

USD 171.86 Million |

| Nepal Data Center Infrastructure Market, CAGR |

10.00% |

| Nepal Data Center Infrastructure Market Size 2035 |

USD 530.52 Million |

Rapid digital transformation in banking, telecom, and government sectors is driving infrastructure demand. Enterprises are migrating to cloud-based systems, pushing investments in UPS systems, high-efficiency cooling, and modular data centers. Innovation in edge computing, AI-based monitoring, and hybrid cloud adoption is accelerating. The market holds strategic importance for businesses aiming to improve uptime, scalability, and data security. Investors see value in the untapped demand, growing digitization, and favorable policy support. Demand for green infrastructure and energy-efficient systems continues to rise.

Kathmandu Valley dominates due to urban density, policy incentives, and better connectivity. The Eastern and Western provinces are emerging with growing data needs from expanding enterprises and e-governance. Smaller cities benefit from improving fiber access and land availability for modular setups. Rural zones remain underserved but show potential for edge deployments. Regional growth reflects infrastructure readiness, enterprise presence, and targeted government incentives.

Market Dynamics:

Market Drivers

Accelerating Digital Transformation Across Banking, Telecom, and Government Sectors

Digital adoption is rising fast across financial services, telecom, and government initiatives in Nepal. Banks expand core banking platforms and digital wallets, requiring secure, scalable infrastructure. Telecom players upgrade mobile broadband networks, increasing the volume of user data. E-governance projects push agencies to digitize citizen records and automate services. These shifts increase demand for low-latency, high-availability data centers. The Nepal Data Center Infrastructure Market supports this shift by enabling reliable digital services. Infrastructure modernization aligns with public service reforms and digital financial inclusion goals. Local data centers reduce dependency on foreign hosting. Businesses view data infrastructure as critical to operational agility.

- For instance, NMB Bank received the Digital Services ICT Award 2025 for its enterprise digital transformation, operating through 202 branches, 184 ATMs, and paperless banking platforms that reduced physical visits.

Rise Of Cloud And Hybrid IT Driving Infrastructure Investments From Enterprises

Cloud adoption among enterprises fuels data center capacity growth. SMEs and large businesses migrate to hybrid models combining on-premise and public cloud systems. Workload distribution requires robust colocation and managed services. Enterprise IT buyers demand redundancy, scalability, and lower total cost of ownership. Hosting service providers invest in modular rack setups, virtualization tools, and high-speed connectivity. The Nepal Data Center Infrastructure Market evolves to support this shift in architecture. It provides platforms for centralized control and flexible deployment. Enterprises invest to improve uptime, ensure disaster recovery, and meet data localization norms. Cloud-driven digital operations increase long-term infrastructure demand.

Emergence Of Green Data Centers And Sustainable Infrastructure Practices

Energy efficiency is gaining importance among infrastructure planners in Nepal. Operators aim to reduce carbon footprints through renewable energy sourcing and efficient cooling. Hydropower availability supports a shift toward low-emission infrastructure models. Liquid cooling, airflow optimization, and modular designs improve performance per watt. The Nepal Data Center Infrastructure Market integrates sustainability metrics into planning and execution. Policy focus on green development encourages private sector compliance. Data center certifications aligned with global standards improve investor confidence. Energy-saving hardware reduces lifetime operational costs. This trend reshapes procurement and design strategies across data center projects.

Strategic Location And Growing Regional Connectivity Make Nepal An Emerging Digital Hub

Nepal’s geography offers connectivity advantages between India and China. Cross-border fiber projects boost bandwidth and network diversity. Government policies aim to make Nepal a regional digital gateway. International cloud players and telecoms explore partnerships with local firms. The Nepal Data Center Infrastructure Market benefits from regional data routing and edge deployments. Urban centers like Kathmandu attract infrastructure investments due to policy ease and talent availability. Strategic planning zones promote land allocation for IT parks. Regional linkages drive interest from hyperscale operators and content delivery networks. Businesses recognize Nepal’s potential as a latency-efficient, cost-effective regional node.

- For instance, in July 2025, IFC and Standard Chartered committed $29 million to WorldLink and its subsidiary Data World to expand fiber networks and develop Nepal’s first EDGE-certified data center, supporting digital connectivity in remote areas.

Market Trends

Growing Role Of Edge Data Centers To Support Localized Applications And Latency-Sensitive Services

Edge infrastructure gains momentum to handle real-time processing needs. Applications such as e-health, mobile banking, and surveillance require minimal latency. Edge deployments reduce pressure on core networks by processing data closer to users. Nepal’s diverse geography encourages edge setups in underserved regions. The Nepal Data Center Infrastructure Market sees traction in small footprint, modular edge units. Telecoms integrate edge data centers into tower infrastructure. Power-efficient micro-modules enable expansion in remote areas. Enterprises use edge nodes to run lightweight AI and analytics locally. This trend decentralizes infrastructure while enhancing service quality.

Increased Deployment Of Software-Defined Infrastructure For Better Resource Management

Software-defined data center (SDDC) technologies are adopted to manage infrastructure with higher agility. Virtualization of compute, storage, and networking improves control and scalability. Operators deploy centralized software layers for policy enforcement and workload balancing. Automation tools reduce human error and simplify configuration updates. The Nepal Data Center Infrastructure Market embraces software-defined systems to optimize performance. SDDC supports hybrid cloud environments and accelerates provisioning. Vendors introduce solutions tailored for small and mid-size operators. Organizations gain visibility across physical and virtual assets. This trend enhances infrastructure efficiency while supporting innovation cycles.

Integration Of AI-Powered Monitoring And Predictive Maintenance Capabilities

AI and ML tools are being used to monitor equipment health, optimize energy usage, and predict failures. Intelligent systems detect anomalies in power supply, temperature, and airflow. Predictive maintenance avoids costly outages and improves uptime. Operators use AI to forecast load spikes and automate cooling responses. The Nepal Data Center Infrastructure Market integrates AI for smarter operations. AI-driven dashboards improve response time and resource planning. Vendors offer built-in analytics in power and thermal management systems. Data centers evolve from reactive models to intelligent automation. This trend boosts resilience and sustainability of operations.

Rising Preference For Modular And Scalable Design Frameworks Among Infrastructure Builders

Demand grows for modular systems that allow phased expansion based on usage. Modular racks, containers, and power systems reduce upfront capital expenditure. This approach aligns with uncertain demand patterns and evolving technologies. The Nepal Data Center Infrastructure Market adopts modularity to speed up deployments. Prefabricated components improve build quality and shorten project timelines. Operators scale capacity without disrupting current operations. Vendors offer plug-and-play solutions for fast onboarding. This trend supports flexible growth and reduces lifecycle costs. It fits the needs of startups, enterprises, and cloud providers.

Market Challenges

Limited Power Reliability And High Operational Risks Across Several Locations

Power supply remains a major concern for data center operators in Nepal. Despite strong hydropower potential, outages and fluctuations persist in several areas. Backup generators raise fuel and maintenance costs. Voltage instability impacts sensitive IT equipment and cooling systems. The Nepal Data Center Infrastructure Market contends with higher energy risks compared to mature markets. Infrastructure providers must invest in UPS systems, dual power feeds, and smart grids. Rural regions lack reliable distribution networks. These conditions deter foreign direct investment in Tier III or higher-grade facilities. Ensuring stable and clean energy remains a critical hurdle.

Shortage Of Skilled Workforce And Regulatory Bottlenecks Hinder Project Timelines

Nepal faces a shortage of trained professionals in critical areas like facility management, network engineering, and cybersecurity. Many skilled workers migrate abroad, creating a persistent talent gap. Training programs in data center operations remain limited in reach and relevance. The Nepal Data Center Infrastructure Market depends heavily on outsourced expertise for project setup. Regulatory frameworks around data handling, land approvals, and environmental compliance add delays. Slow bureaucratic procedures extend project lead times and increase development costs. Inconsistencies in policy enforcement affect investor confidence. Talent and governance gaps challenge large-scale infrastructure scale-up.

Market Opportunities

Expansion Of Fintech, Cloud Gaming, And Digital Learning Platforms Creating Strong Infrastructure Demand

Digital services are expanding across financial inclusion, entertainment, and education sectors. Fintech adoption grows through mobile payment apps and digital lending platforms. Cloud gaming gains traction among youth, demanding low-latency infrastructure. Remote learning platforms increase traffic volumes. The Nepal Data Center Infrastructure Market supports these ecosystems with reliable backend capacity. Demand for colocation and cloud nodes expands beyond Kathmandu. Service providers target edge connectivity and rural market access. These trends open new revenue paths for infrastructure developers and investors.

Cross-Border Connectivity And Government Incentives Fueling Private Sector Participation

Nepal’s strategic positioning between India and China enhances regional data exchange prospects. Government initiatives such as IT parks, tax breaks, and land leasing promote private investment. Infrastructure operators explore cross-border partnerships and data routing services. The Nepal Data Center Infrastructure Market benefits from policy-level efforts to attract regional players. Private equity firms and infrastructure funds enter early-stage projects. Export-focused data hosting and regional caching gain policy backing. These conditions create a supportive environment for long-term growth.

Market Segmentation:

By Infrastructure Type

The Nepal Data Center Infrastructure Market is dominated by the electrical infrastructure segment, driven by rising demand for uninterrupted power in mission-critical environments. UPS systems, PDUs, and advanced switchgears are key to maintaining operational continuity. Mechanical infrastructure follows, supported by the need for efficient cooling systems due to high rack density. IT & network infrastructure sees rapid growth with rising server and storage needs. Civil and architectural components remain essential but grow at a steady pace. Overall, electrical infrastructure leads in both value and investment share.

By Electrical Infrastructure

Uninterruptible power supply (UPS) leads the electrical infrastructure segment in the Nepal Data Center Infrastructure Market, due to the country’s unreliable grid and frequent voltage fluctuations. UPS systems provide clean backup power, essential for protecting IT assets. PDUs and switchgears also show strong traction as data centers aim for optimized load management. Battery energy storage systems (BESS) are gaining ground, supporting sustainability goals and backup efficiency. The push toward grid independence and renewable power integration further accelerates investment across this segment.

By Mechanical Infrastructure

Cooling units (CRAC/CRAH) dominate the mechanical infrastructure segment in the Nepal Data Center Infrastructure Market. High-performance computing and rising server density increase heat output, requiring precision cooling solutions. Chillers, especially water-cooled systems, are gaining interest due to better energy efficiency. Containment systems like hot and cold aisles improve airflow and thermal management. Pumps and piping systems play a vital role in maintaining consistent cooling performance. Demand for energy-efficient mechanical systems rises as sustainability metrics gain importance in project design.

By Civil / Structural & Architectural

Site preparation and modular building systems dominate the civil/structural segment of the Nepal Data Center Infrastructure Market. Urban land constraints and project timelines drive demand for prefabricated and modular solutions. Superstructures using steel frames gain preference for their strength and faster assembly. Building envelopes and raised flooring systems are key to maintaining controlled environments. Investment is rising in modular shells that reduce lead time. Structural innovations that support seismic resistance are vital due to Nepal’s geography, shaping procurement priorities.

By IT & Network Infrastructure

Servers and networking equipment are the leading contributors to the IT & network infrastructure segment in the Nepal Data Center Infrastructure Market. Cloud deployments and digital service delivery boost demand for scalable and high-speed computing resources. Storage systems grow steadily as data volume increases across sectors. Cabling and optical fiber investments rise with growing emphasis on high-throughput, low-latency architecture. Racks and enclosures are evolving to support both air and liquid-cooled setups. Operators prioritize flexible, modular IT systems to future-proof deployments.

By Data Center Type

Colocation data centers hold the largest share in the Nepal Data Center Infrastructure Market, supported by rising enterprise outsourcing and cloud-neutral facility demand. Small and medium businesses opt for shared infrastructure to reduce capex. Hyperscale developments remain limited but are under exploration due to regional cloud service expansion. Edge data centers are gaining traction in remote or low-connectivity zones. Enterprise data centers are stable, with growth driven by banks and telecom firms modernizing legacy setups. The shift toward hybrid IT models supports colocation momentum.

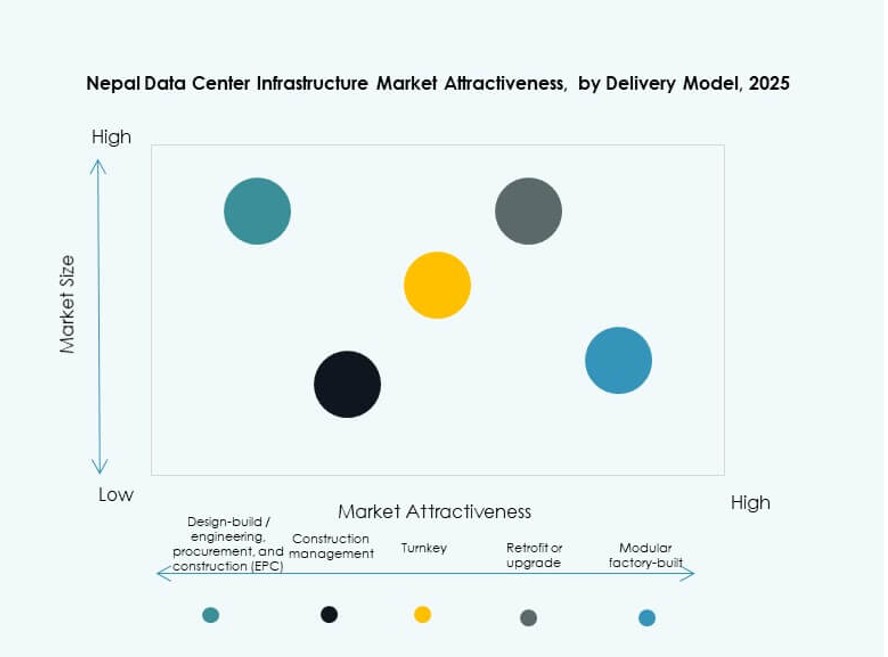

By Delivery Model

Design-build/EPC is the leading delivery model in the Nepal Data Center Infrastructure Market, preferred for integrated execution and reduced risk. Turnkey models follow, offering speed and simplicity for end-users. Construction management sees use in large-scale custom builds requiring close project oversight. Retrofit and upgrade models grow as older facilities seek modernization. Modular factory-built solutions are emerging due to their shorter deployment cycles. Stakeholders value delivery models that ensure compliance, speed, and cost control in a dynamic environment.

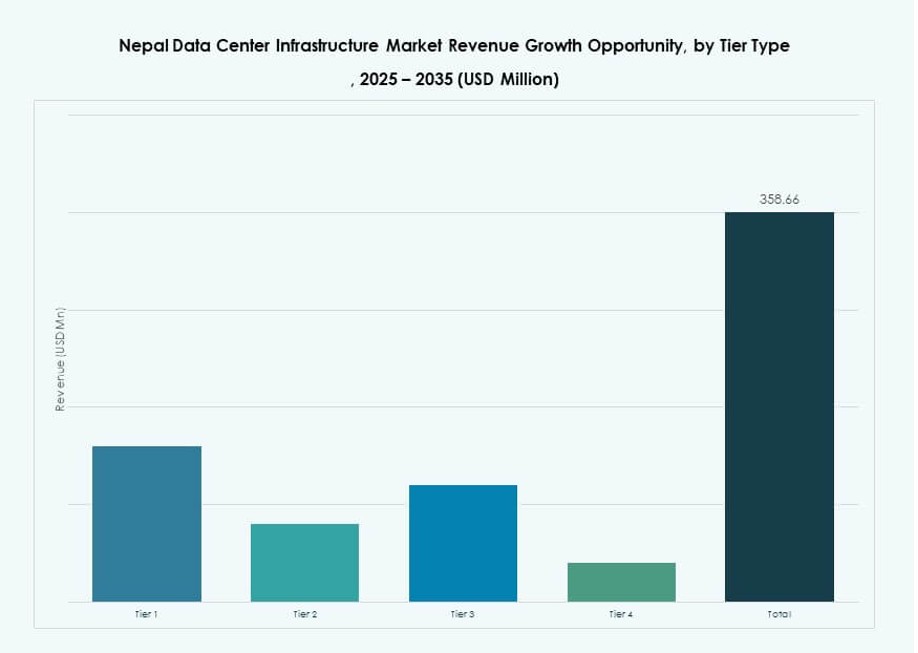

By Tier Type

Tier 3 dominates the tier classification in the Nepal Data Center Infrastructure Market due to its balance between uptime, cost, and scalability. These facilities offer N+1 redundancy and support for critical applications. Tier 1 and Tier 2 centers serve SMEs and non-critical workloads in rural or low-demand zones. Tier 4 remains niche, considered for high-security or financial data centers. Investment in Tier 3 grows with demand for compliance, SLA guarantees, and multi-zone failover support. The market trends toward resilient yet cost-efficient infrastructure builds.

Regional Insights:

Central Region (Bagmati Province – Kathmandu Valley, Lalitpur, Bhaktapur)

The Central Region holds the largest share of the Nepal Data Center Infrastructure Market, accounting for approximately 68% of the total market. Kathmandu Valley acts as the digital and administrative core, driving most infrastructure investments. High population density, robust fiber connectivity, and concentration of financial institutions contribute to this dominance. Enterprises, banks, telecom providers, and cloud service integrators prefer this region for Tier 3 and modular data center deployments. Government-supported IT zones and data localization regulations support growth in this subregion. The Central Region continues to attract greenfield and brownfield investments from domestic and international players.

- For instance, Ncell operates a Tier III integrated data center in Nakkhu, Lalitpur, which became Nepal’s first officially certified facility by the Department of Information Technology in April 2025 after inspections of fire safety, security policies, and IP infrastructure.

Eastern and Western Regions (Province 1 & 2, Gandaki, Lumbini)

The Eastern and Western Regions together account for 22% of the Nepal Data Center Infrastructure Market. Cities like Biratnagar, Pokhara, and Butwal are emerging as data center nodes due to improving digital adoption and power access. Enterprises in manufacturing, retail, and healthcare begin investing in regional hosting and colocation solutions. Government efforts to decentralize digital services push infrastructure into these provinces. Connectivity upgrades and new power grid extensions are supporting local infrastructure scale-up. These regions offer cost advantages in land and utilities compared to the capital.

- For instance, Ncell operates two disaster recovery data centers in Pokhara (Gandaki Province) and Hetauda, certified as part of its Tier III ecosystem by DoIT in April 2025 to ensure business continuity.

Far-Western & Mid-Western Regions (Karnali, Sudurpashchim)

The Far-Western and Mid-Western regions hold the remaining 10% share of the Nepal Data Center Infrastructure Market. Limited power reliability, poor fiber infrastructure, and lower commercial activity restrict large-scale deployments. However, telecom operators and government agencies initiate pilot edge data centers and micro-sites to improve service access. Digital literacy and infrastructure development programs are gradually improving the region’s readiness. Operators view this region as a long-term opportunity for rural digitization and edge computing expansion. Investment remains limited but is expected to grow with infrastructure upgrades.

Competitive Insights:

- Equinix

- Delta Electronics

- IBM

- ABB

- Acer Inc.

- Cisco Systems, Inc.

- Dell Inc.

- KIO

- Lenovo

- Oracle

- Schneider Electric

- Vertiv Group Corp.

- Others

The competitive landscape shows global and regional players focusing on tailored solutions for data centers in Nepal. Leading vendors differentiate through technology portfolios, service reliability, and partner networks. Equinix and KIO expand infrastructure partnerships, while Cisco and Dell strengthen networking and server offerings. Schneider Electric, Delta Electronics, and Vertiv push power and cooling efficiencies critical for uptime. IBM and Oracle support hybrid cloud and enterprise workloads. Lenovo and Acer target scalable hardware deployments. ABB delivers automation and power systems that improve operational stability. Competition centers on reliability, energy efficiency, and total cost of ownership. It drives innovation and pushes new service models that attract enterprise and telecom clients. Firms with integrated solutions gain early mover advantages in the growing market.

Recent Developments:

- In July 2025, IFC and Standard Chartered Bank Nepal committed $29 million to WorldLink Communications and its subsidiary Data World to expand fiber networks and build innovative data centers, including Nepal’s first EDGE-certified facility. The partnership aims to bridge the digital divide and boost economic growth through sustainable infrastructure.

- In April 2025, Ncell became the first (and only) company in Nepal to be officially listed as a Data Center and Cloud Service Providerby the Department of Information Technology (DoIT).

- In February 2025, WorldLink Communications launched a 3.5MW carrier-neutral data center in Chandragiri, Kathmandu, with capacity for 520 racks near the Mata Tirtha substation. This facility supports Nepal’s expanding digital needs amid rising technology reliance.