Executive summary:

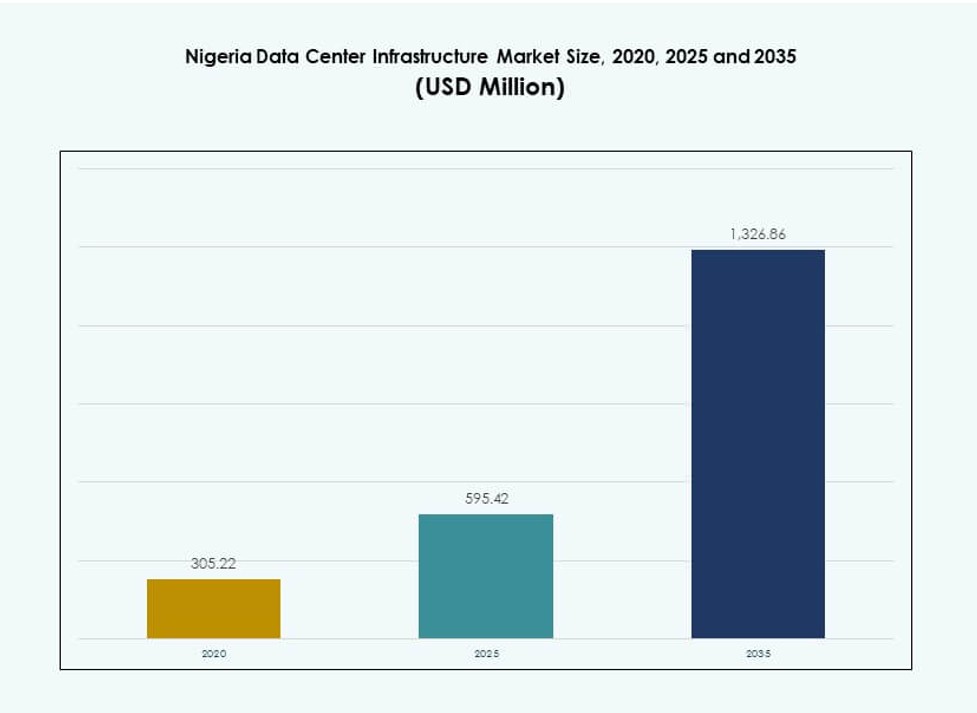

The Nigeria Data Center Infrastructure Market size was valued at USD 305.22 million in 2020, increased to USD 595.42 million in 2025, and is anticipated to reach USD 1,326.86 million by 2035, at a CAGR of 8.26% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Nigeria Data Center Infrastructure Market Size 2025 |

USD 595.42 Million |

| Nigeria Data Center Infrastructure Market, CAGR |

8.26% |

| Nigeria Data Center Infrastructure Market Size 2035 |

USD 1,326.86 Million |

Growth in the Nigeria Data Center Infrastructure Market is driven by enterprise cloud adoption, digital government initiatives, and next-gen telecom modernization. Businesses adopt modular, energy-efficient systems to meet workload demands and sustainability goals. Subsea cable landings and hybrid cloud strategies boost interconnectivity and service reliability. Investors see Nigeria as a gateway to West Africa’s digital economy, with increasing demand for colocation, hyperscale, and edge infrastructure. Technology firms continue expanding capacity to meet low-latency requirements.

Lagos leads the Nigeria Data Center Infrastructure Market due to its role as a digital and economic hub with multiple subsea cable landings. Abuja follows, supported by government digitization and enterprise demand. Port Harcourt and other southern cities emerge as secondary markets, driven by industrial activity and regional hosting needs. Infrastructure development aligns with connectivity upgrades and local business expansion across these regions.

Market Dynamics:

Market Drivers

Digital Transformation Initiatives Across BFSI, Telecom, and Government Fuel Infrastructure Expansion

The Nigeria Data Center Infrastructure Market benefits from growing digital adoption across banking, telecom, and public sectors. Enterprises migrate core applications to data centers to improve efficiency and latency. Government pushes like the National Digital Economy Policy accelerate local infrastructure deployment. Telecom operators upgrade backbone systems, increasing demand for secure colocation. Financial institutions modernize backend platforms and storage. Cloud-first strategies improve availability and performance. These moves create constant demand for reliable, scalable infrastructure. Investors view Nigeria as a West African digital entry point with rising service uptake.

Cloud Computing and Edge Deployment Drive the Need for Modular, Scalable Infrastructure

Cloud service providers enter the Nigeria Data Center Infrastructure Market to tap underserved demand. Firms deploy containerized modules and prefabricated data halls to reduce build time. Edge computing gains traction for IoT and content delivery use cases. Modular infrastructure supports quicker response to regional data needs. Cooling and power systems are optimized for density and uptime. Cloud-native architectures demand higher resilience and automation. Flexible deployment options lower CAPEX while supporting workload diversity. This shift increases demand for smart infrastructure investment.

- For instance, Rack Centre expanded its Lagos campus to approximately 14.5MW by 2025, including the launch of its LGS2 facility. Edge computing is gaining traction in Nigeria, supporting IoT and content delivery applications across enterprise and telecom sectors.

Energy Innovation and Cooling Technologies Reinforce Operational Efficiency

The Nigeria Data Center Infrastructure Market integrates energy-efficient systems to mitigate power costs and grid unreliability. UPS systems and lithium-ion BESS adoption reduce outages and diesel reliance. Liquid cooling and aisle containment improve thermal efficiency in dense setups. Operators use hybrid energy setups, including solar-diesel microgrids. AI-based systems manage power loads and cooling dynamically. Infrastructure suppliers localize solutions for hot, humid climates. Efficiency translates to lower TCO and environmental compliance. These innovations attract foreign hyperscale and edge investors.

Strategic National Location Makes Nigeria a Regional Connectivity and Interconnection Hub

Nigeria’s location and subsea cable access give it strategic value in West Africa. Lagos connects to several high-capacity subsea cables, enabling low-latency access to Europe and other African regions. It becomes a preferred interconnection point for regional content distribution and financial trading. Enterprises choose Nigerian facilities to ensure redundancy, compliance, and proximity to users. Data center campuses serve as cross-connect zones for ISPs, cloud, and enterprise workloads. Its role in regional cloud and fintech ecosystems continues to expand. These dynamics drive sustained infrastructure growth.

- For instance, Nigeria’s total installed and planned data center capacity approached 120 MW by late 2025, led by hyperscale and colocation expansions. New facilities in Lagos and Abuja significantly boosted national hosting and interconnection capabilities.

Market Trends

Subsea Cable Landings and Interconnection Ecosystems Expand Nigeria’s Digital Reach

Multiple subsea cable landings have transformed Nigeria into a high-connectivity gateway. Cables like Equiano and 2Africa provide massive bandwidth boosts. Data centers align with landing stations for low-latency access. Interconnection hubs form where cloud providers, telcos, and ISPs converge. These ecosystems offer enterprises direct cloud access and faster content delivery. Traffic remains local, improving speed and reducing costs. Global CDN and fintech companies leverage these hubs. The Nigeria Data Center Infrastructure Market benefits from these digital interconnection zones.

Shift Toward Carrier-Neutral Colocation and Hyperscale Buildouts Accelerates

Carrier-neutral colocation gains traction as enterprise workloads diversify. Operators provide neutral hosting with rich connectivity options and cross-connect flexibility. Hyperscale providers partner with local firms or build self-owned campuses. Campus-style setups include power redundancy, phased expansion, and secure ecosystems. These trends allow scalable hosting for large cloud tenants. Demand for dark fiber, peering, and neutral access supports vendor growth. Enterprises benefit from flexibility and data sovereignty. The Nigeria Data Center Infrastructure Market attracts diverse tenants in these environments.

AI and High-Density Workloads Push Advanced Cooling and Power Infrastructure

AI and HPC workloads require dense server configurations with precise cooling. Operators install liquid-cooled servers, hot/cold aisle containment, and CRAC enhancements. Lithium-ion battery backups and modular UPS ensure stable power for AI clusters. AI-based DCIM tools optimize power usage and environmental conditions. Equipment vendors offer density-ready hardware pre-tested for African climates. Infrastructure evolves to support next-gen computing and analytics needs. The Nigeria Data Center Infrastructure Market integrates smarter infrastructure to meet AI-driven workloads.

Rising Demand for Local Cloud and SaaS Hosting Drives Data Sovereignty Compliance

Businesses prefer local hosting to meet data protection rules and improve service reliability. Local SaaS, PaaS, and IaaS firms grow under regulatory pressure on data residency. Government platforms increasingly demand onshore hosting. Local data centers offer compliance-ready hosting environments. Hosting proximity also improves service speed and user trust. Enterprises shift from offshore cloud to local partners. This demand supports investments in secure, Tier III and IV-certified data centers. The Nigeria Data Center Infrastructure Market sees strong growth in local hosting needs.

Market Challenges

Limited Grid Reliability and High Energy Costs Strain Operational Stability and Uptime

Power supply issues remain a major barrier in the Nigeria Data Center Infrastructure Market. Frequent outages and voltage instability force reliance on diesel generators and hybrid power setups. Energy costs represent a large share of operational expenses. Rural and secondary city deployments face more acute power issues. Even in Lagos, grid quality is unpredictable, leading to downtime risks. Investments in UPS, BESS, and solar are required but increase CAPEX. Operators face trade-offs between uptime assurance and cost control. Energy constraints delay market entry for new data center players.

Shortage of Local Talent and High Import Dependence Affect Deployment Timelines

Data center construction and operation need specialized skills in power, cooling, networking, and cybersecurity. Nigeria faces a talent gap in these technical roles, limiting scalability. Firms depend on external consultants for design and integration, raising costs. Import dependency for core hardware such as PDUs, CRAC units, and lithium-ion batteries leads to delays. Customs clearance and logistics add lead time. Local manufacturing is limited for critical components. These constraints extend project timelines and reduce ecosystem resilience. The Nigeria Data Center Infrastructure Market needs stronger local supply chains and training programs.

Market Opportunities

Strategic Expansion Into Secondary Cities for Decentralized Hosting and Enterprise Proximity

Cities beyond Lagos offer untapped potential for edge and enterprise hosting. Abuja, Port Harcourt, and Kano see growing demand from banks, telcos, and government offices. Localized hosting improves latency and data control. Regional campuses can offer hybrid models with hyperscale capacity and local delivery. The Nigeria Data Center Infrastructure Market expands as enterprises seek lower-cost, in-region hosting options.

Partnerships With Cloud and Telecom Operators to Co-Develop Scalable Infrastructure

Global players seek local partners to enter the Nigerian market efficiently. Telecom operators provide network access, while cloud firms bring hyperscale demand. Joint ventures support modular, fast-to-market facilities. Infrastructure providers benefit from assured demand and shared risk. This trend supports faster deployment and better resource utilization across the Nigeria Data Center Infrastructure Market.

Market Segmentation

By Infrastructure Type

The Nigeria Data Center Infrastructure Market is dominated by electrical infrastructure, contributing the highest share due to power availability challenges. Mechanical infrastructure, including advanced cooling and containment systems, also shows strong demand in high-density facilities. IT & network infrastructure expands with server and storage upgrades. Civil and architectural components are essential for greenfield and modular builds. The others segment includes environmental controls and safety systems, gaining importance in regulatory compliance efforts.

By Electrical Infrastructure

Uninterruptible Power Supply (UPS) systems lead the segment with the highest share, driven by frequent grid outages. Battery Energy Storage Systems (BESS) follow due to rising interest in lithium-ion solutions. Power Distribution Units (PDUs) and transfer switches are key for load management and redundancy. Switchgears and utility grid connections are standard components but require upgrades for newer facilities. The others category includes hybrid and solar-integration setups supporting efficient energy use.

By Mechanical Infrastructure

Cooling units like CRAC/CRAH dominate this segment, especially in Tier III facilities. Containment systems such as hot/cold aisle setups follow closely, improving thermal efficiency. Chillers, both air- and water-cooled, serve high-density deployments. Pumps and piping support closed-loop and liquid-cooled configurations. Other solutions include HVAC integration and airflow management, particularly important in Nigeria’s climate. The Nigeria Data Center Infrastructure Market integrates mechanical innovations for energy efficiency.

By Civil / Structural & Architectural

Superstructure design, including steel and concrete frames, holds the largest share due to full-building data center campuses. Building envelopes and raised flooring systems contribute significantly to energy containment and cabling. Modular/prefabricated systems gain momentum for their fast deployment and lower cost. Site preparation and foundations are key to location-specific setups. Suspended ceilings support airflow and fire safety systems. This segment supports long-term facility scaling.

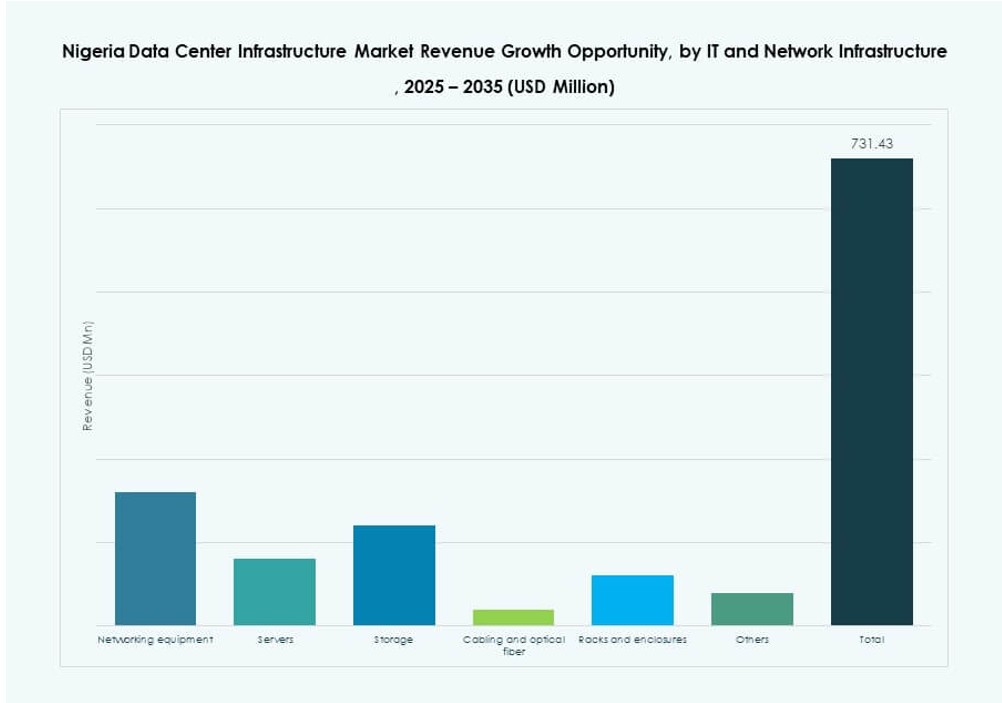

By IT & Network Infrastructure

Networking equipment dominates due to interconnectivity needs with subsea and terrestrial fiber. Servers and storage contribute significantly to hyperscale and enterprise builds. Racks and enclosures see strong demand in modular designs. Cabling and fiber optics play a vital role in ensuring high-speed data flow. The Nigeria Data Center Infrastructure Market sees increasing investments in scalable, cloud-ready IT stacks.

By Data Center Type

Colocation data centers hold the dominant market share, driven by enterprise outsourcing. Hyperscale data centers are expanding rapidly with cloud adoption. Enterprise-owned data centers are still present but losing share. Edge data centers grow in secondary cities for local content hosting. Other facilities like disaster recovery sites and training labs form a small portion. Colocation leads due to flexibility, cost benefits, and network access.

By Delivery Model

Design-build/EPC remains dominant, especially for hyperscale and Tier III/IV builds. Turnkey solutions and modular factory-built models are gaining traction for quick deployment. Construction management and retrofit/upgrade models are used for brownfield sites. These options support firms that already have real estate or legacy infrastructure. The Nigeria Data Center Infrastructure Market favors hybrid delivery strategies to meet diverse client needs.

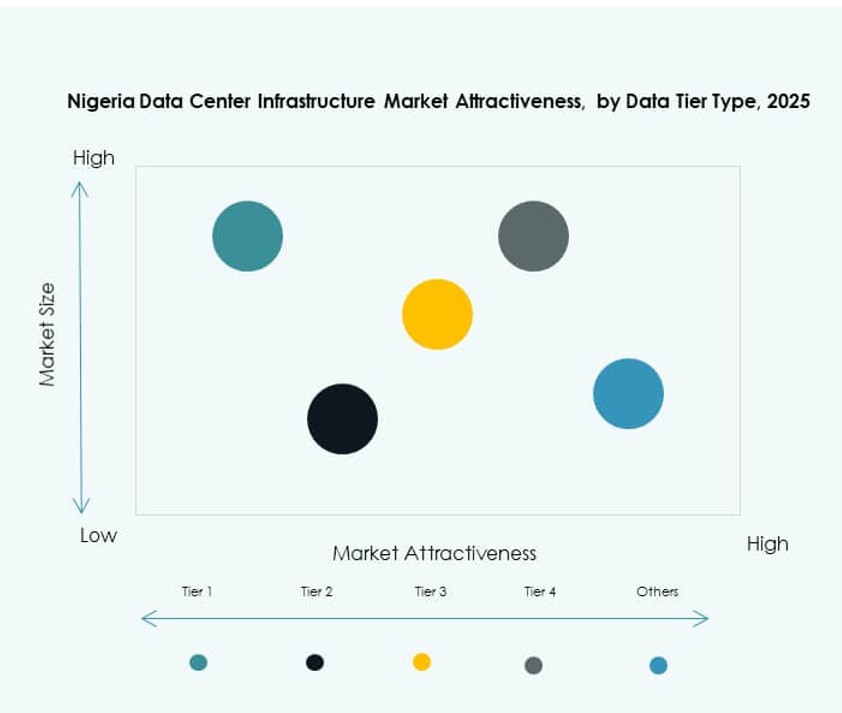

By Tier Type

Tier III facilities dominate the Nigeria Data Center Infrastructure Market, offering a balance of reliability and cost. Tier IV follows with growth among hyperscale and financial service providers. Tier I and II see use in small-scale or legacy setups. Certification compliance and uptime requirements drive Tier III dominance. The market evolves toward higher-tier certifications as demand for SLA-backed services increases.

Regional Insights

Lagos Region Leads the Market with Over 55% Share Due to Cable Access and Economic Density

Lagos dominates the Nigeria Data Center Infrastructure Market with over 55% share. It hosts major subsea cable landings and global cloud entry points. The region includes the most mature colocation and enterprise data center clusters. Strong financial and telecom activity supports sustained infrastructure demand. Lagos also benefits from stronger grid connectivity relative to other regions. International firms use Lagos as a base for West African operations. The state government supports digital investment zones.

- For instance, MTN Nigeria’s Dabengwa Sifiso Data Centre in Ikeja (Phase 1) supports 780 racks with a 4.5MW IT load across three floors and operates as a Tier III-certified facility. This strengthens MTN’s core infrastructure for digital service delivery in Nigeria.

Abuja and North Central Nigeria Account for 20% Share with Rising Government and Banking Needs

Abuja holds around 20% of market share, driven by public sector digitization and regulatory hosting mandates. The region hosts government data centers, fintech operations, and central bank infrastructure. Proximity to federal institutions supports growth in enterprise and colocation builds. Operators deploy hybrid setups to address unreliable grid supply. Abuja’s importance grows due to its central location and public-private partnerships. Local hosting demand accelerates data center expansion plans.

- For instance, Digital Realty’s ABV1 facility at 23 Kolda Street offers 2MW capacity with N+1 redundancy and connects to the Nigeria Internet Exchange Point (NIXP). Its location near key federal institutions supports strong enterprise and colocation demand in Abuja.

South-South and South-East Regions Hold 15% Share, with Port Harcourt Emerging as an Industrial Hub

These regions account for 15% of the market, supported by oil, gas, and industrial demand. Port Harcourt emerges as a key location due to petrochemical activity and logistics access. Tier II cities like Enugu and Calabar attract regional enterprise data hosting. Fiber deployment improves accessibility, encouraging edge facility development. Investment in connectivity and security boosts private sector confidence. These regions present long-term growth potential in the Nigeria Data Center Infrastructure Market.

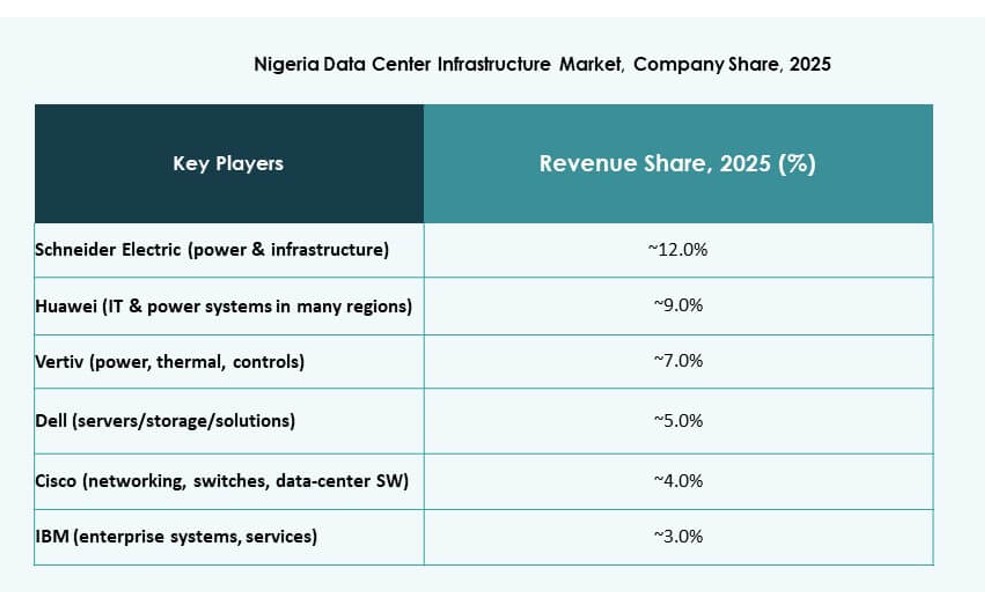

Competitive Insights:

- Rack Centre

- Gulf Data Hub

- G42 / Core42

- Equinix, Inc.

- Schneider Electric

- Vertiv Group Corp.

- Huawei Technologies Co., Ltd.

- Dell Inc.

- Cisco Systems, Inc.

The Nigeria Data Center Infrastructure Market shows a mixed competitive structure with local operators, global colocation firms, and infrastructure vendors. Rack Centre leads local colocation through carrier neutrality and strong enterprise links. Gulf Data Hub and G42/Core42 expand hyperscale capacity through campus-style builds. Equinix strengthens interconnection appeal for global cloud and fintech clients. Schneider Electric and Vertiv supply power and cooling systems aligned with grid constraints. Huawei, Dell, and Cisco support server, storage, and network layers across deployments. Competition centers on uptime assurance, energy efficiency, and rapid scalability. Partnerships with telecom operators shape market access. The landscape favors firms with modular design expertise, local execution capability, and strong enterprise trust.

Recent Developments:

- In November 2025, Rack Centre partnered with EdgeNext to launch CDN and cloud hosting services in its 12MW Lagos facility, boosting digital infrastructure in Nigeria’s data center market. This collaboration aims to accelerate digital transformation for local businesses.

- In November 2025, Equinix announced plans for a new high-performance data center, LG3, in Lagos as part of a $100 million investment over two years. The $22 million first phase is set to open in Q1 2026, enhancing Nigeria’s digital landscape.

- In June 2025, Rack Centre signed a colocation agreement with TelCables Nigeria, integrating international subsea connectivity into its Lagos campus. TelCables, a subsidiary of Angola Cables, extends high-capacity networks and cloud infrastructure to the carrier-neutral site. The partnership was highlighted.

- In April 2025, Rack Centre commissioned its second data center, LGS2, in Lagos’ Ikeja area, offering 12MW capacity across six halls and 3,240 sqm of white space. This expansion supports growing demands in Nigeria’s data center infrastructure.