Executive summary:

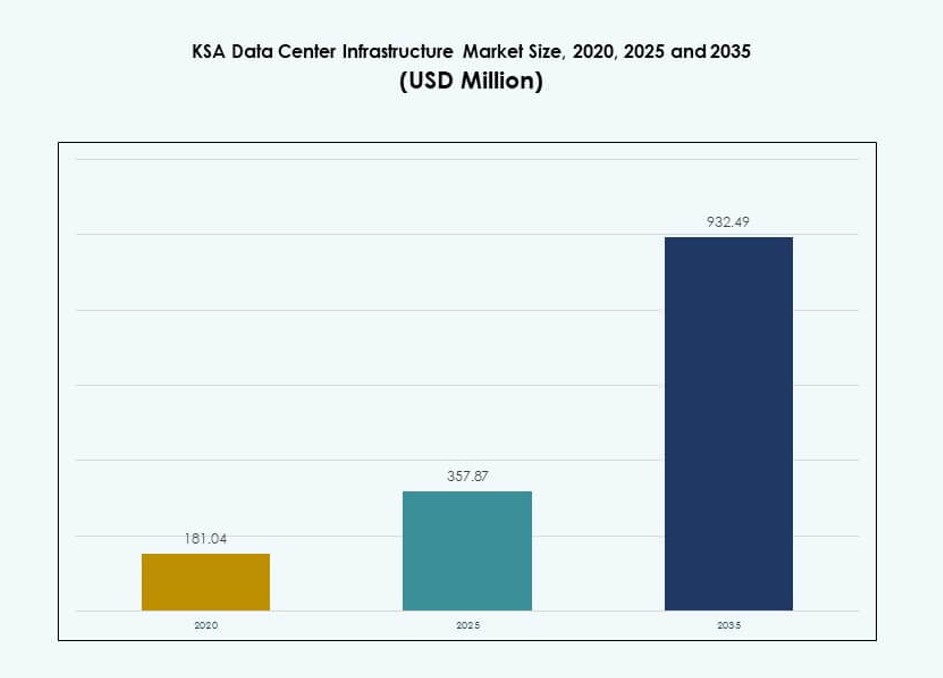

The KSA Data Center Infrastructure Market size was valued at USD 181.04 million in 2020 to USD 357.87 million in 2025 and is anticipated to reach USD 932.49 million by 2035, at a CAGR of 9.97% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| KSA Data Center Infrastructure Market Size 2025 |

USD 357.87 Million |

| KSA Data Center Infrastructure Market, CAGR |

9.97% |

| KSA Data Center Infrastructure Market Size 2035 |

USD 932.49 Million |

Strong cloud adoption supports steady infrastructure demand across enterprises and public entities. Hyperscale deployment expands to support AI workloads and digital platforms. Data localization policies push domestic hosting investments. Innovation in power, cooling, and modular design improves efficiency and uptime. Businesses rely on secure infrastructure for continuity and compliance. Investors view the market as a long-term digital asset base. Stable demand anchors future expansion strategies.

Riyadh leads development due to government concentration and hyperscale activity. Jeddah follows, supported by connectivity and enterprise demand. Eastern regions emerge with industrial and energy-driven data needs. NEOM shows early momentum from smart city planning. The market remains Saudi-focused, with limited cross-border dependence. Regional leadership comes from policy support and infrastructure readiness. Emerging zones gain relevance through targeted digital projects.

Market Dynamics:

Market Drivers

National Digitalization Strategy and Rising Government-Backed Infrastructure Spending Across ICT Sectors

Saudi Arabia’s Vision 2030 initiative drives robust digital transformation across sectors. The government prioritizes advanced IT infrastructure to power e-governance, smart cities, and automation. The KSA Data Center Infrastructure Market benefits from capital injection into tech parks, 5G networks, and AI platforms. It grows through public-private collaborations and data localization mandates. Regulatory clarity attracts foreign investment into high-resilience facilities. Expansion of digital banking, healthcare, and education boosts enterprise IT demand. Strategic diversification reduces oil reliance and deepens digital ecosystem roots. The market serves as a cornerstone for future-ready service delivery and business continuity.

- For instance, ICS Arabia commenced construction on its Desert Dragon data center Phase 1 in Riyadh in November 2024, a 65 MW Tier III facility set for operation by March 2026 as part of Vision 2030-aligned public-private partnerships.

Acceleration of Cloud Adoption and Surge in Hyperscale Deployment by Major Global Operators

Rapid migration to cloud services accelerates local infrastructure growth. AWS, Google Cloud, and Oracle expand hyperscale presence to serve regional workloads. Enterprises choose cloud-native apps, demanding scalable backend support. The KSA Data Center Infrastructure Market gains traction from hybrid models blending on-prem and public cloud. Strategic data sovereignty concerns push localized hosting solutions. Service providers add edge computing and CDNs to improve latency. High-performance hardware, modular deployment, and advanced cooling support hyperscale scalability. Energy-efficient designs gain relevance for large-scale cloud operations.

- For instance, Equinix announced a $1 billion hyperscale data center project in Riyadh during February 2025, targeting up to 100 MW of IT capacity to support cloud and AI workloads. The project aligns with Saudi Arabia’s Vision 2030 and marks a major investment in the KSA Data Center Infrastructure Market.

Innovation in Power and Cooling Systems to Meet Operational Efficiency and Sustainability Standards

Energy usage and operational efficiency remain top focus areas for new facilities. Investors prefer green-certified buildings using liquid cooling and AI-powered energy optimization. The KSA Data Center Infrastructure Market adopts smart UPS systems, renewable integration, and high-efficiency CRAC/CRAH units. Cooling innovations such as chilled water systems and hot/cold aisle containment reduce thermal stress. UPS and BESS upgrades provide backup resilience. Modular and prefabricated infrastructure shorten deployment cycles. Operators standardize on PUE thresholds and sustainability benchmarks. Future builds consider carbon neutrality as part of ESG mandates.

Rising Strategic Importance of Localized Infrastructure for Business Continuity and Data Sovereignty

Growing digital risk awareness highlights the need for domestic hosting and disaster recovery. Enterprises demand secure, low-latency access to sensitive data. The KSA Data Center Infrastructure Market aligns with compliance needs tied to data residency and cross-border regulations. Colocation firms expand to serve banking, telecom, and public-sector clients. Geopolitical shifts elevate infrastructure sovereignty across Gulf nations. Multinational firms establish regional nodes for faster service delivery. Market maturity supports industry-specific infrastructure formats. High-availability zones strengthen business continuity frameworks.

Market Trends

Shift Toward Modular, Prefabricated Data Center Deployments to Accelerate Time-To-Market

Enterprises seek faster facility rollout to keep pace with service demand. Modular builds enable scalable growth and consistent quality control. Prefabricated units reduce construction timelines and lower setup risks. The KSA Data Center Infrastructure Market integrates off-site assembly for electrical and mechanical subsystems. Factory-built systems also simplify compliance with Tier certification. Large operators select containerized designs for edge and enterprise use cases. Innovation in modular architecture allows flexible layouts and quick reconfiguration. Demand from urban and remote sites supports this trend. Builders rely on proven templates to meet faster ROI cycles.

Wider Use of Artificial Intelligence and Machine Learning for Predictive Maintenance and Thermal Management

Data centers use AI to optimize cooling, energy use, and uptime metrics. Smart algorithms manage airflow, fan speeds, and load balancing dynamically. The KSA Data Center Infrastructure Market incorporates ML tools to flag anomalies, forecast failures, and extend asset life. Operators integrate AI into building management systems for centralized control. Use cases include automated patching, thermal tuning, and energy forecasting. Vendors offer embedded intelligence in UPS, CRAC, and PDUs. Real-time alerts improve incident response. AI adoption enhances SLA compliance and reduces operational costs.

Growth in Edge Data Center Deployments for Real-Time Workloads Across Remote or Industrial Zones

Edge facilities meet growing needs for low-latency data handling. Applications like industrial IoT, autonomous vehicles, and surveillance require localized processing. The KSA Data Center Infrastructure Market sees a rise in micro and modular edge nodes. Remote oilfields, ports, and logistics hubs adopt containerized edge infrastructure. Providers launch edge services to enhance content delivery and user experience. Telecommunications firms integrate edge compute with 5G towers. Smaller data center footprints support distributed networks. Edge builds reduce backhaul congestion and enable faster insights.

Expansion of Smart City and Digital Economy Projects Drives Long-Term Infrastructure Demand

Smart urban planning creates consistent demand for IT infrastructure. Riyadh, NEOM, and Jeddah plan for AI-powered traffic, surveillance, and citizen services. The KSA Data Center Infrastructure Market supports these cities through localized compute, data lakes, and digital twin platforms. IoT systems generate real-time data requiring robust backend support. Digital twins of utilities, buildings, and mobility grids require high-availability infrastructure. Smart grids need low-latency control centers. These projects offer long-term anchor demand for data facilities. Vendors tailor designs to city-level resilience needs.

Market Challenges

Limited Renewable Energy Integration and Rising Power Demand Increase Cost and Operational Complexity

Energy remains a critical cost and reliability factor for operators. While the government promotes renewables, grid-level integration is slow. The KSA Data Center Infrastructure Market depends heavily on conventional sources, limiting sustainability gains. Power-intensive cooling in desert conditions increases energy use. Unpredictable tariffs affect long-term OPEX planning. Limited renewable procurement options restrict ESG compliance for global firms. Solar installations remain small-scale due to infrastructure gaps. Heat loads require overprovisioning for redundancy. Energy efficiency improvements must balance initial capital outlay.

Shortage of Specialized Workforce and Regional Expertise Hinders Local Talent Development and Operations

High-growth infrastructure demands experienced professionals across electrical, mechanical, and IT roles. The KSA Data Center Infrastructure Market faces gaps in locally trained staff for design, construction, and operations. Companies often import talent, driving up costs. Lack of dedicated training institutes delays local capacity building. Limited exposure to advanced UPS, BMS, and HVAC systems weakens support reliability. Certification for Tier design and IT equipment remains low among domestic engineers. Long lead times to train technicians challenge growth momentum. HR teams face difficulties in sourcing skilled professionals.

Market Opportunities

Surging Demand for AI, Cloud, and Enterprise Hosting Enables Expansion Across Colocation and Hyperscale Segments

Growing AI adoption and cloud migration present long-term infrastructure demand. The KSA Data Center Infrastructure Market opens doors for foreign operators, developers, and equipment vendors. Enterprise cloud spending supports multi-tenant colocation growth. National digital services create anchor clients. Regional firms seek scalable solutions within data sovereignty boundaries. Smart city projects offer multi-year build-out opportunities. Vendors can provide hybrid, edge, and software-defined infrastructure models.

Favorable Regulatory Environment and Sovereign Investment in Technology Zones Encourage Long-Term Investments

Government-backed tech zones, SEZs, and tax benefits draw infrastructure players. The KSA Data Center Infrastructure Market offers high-growth potential for modular, greenfield, and retrofit developers. Public-private models offer stable demand and reduced investment risks. Investors gain from utility-backed power availability. Partnerships with NEOM, PIF, and ministries ensure long-term demand visibility. Demand from education, telecom, and fintech firms remains strong.

Market Segmentation

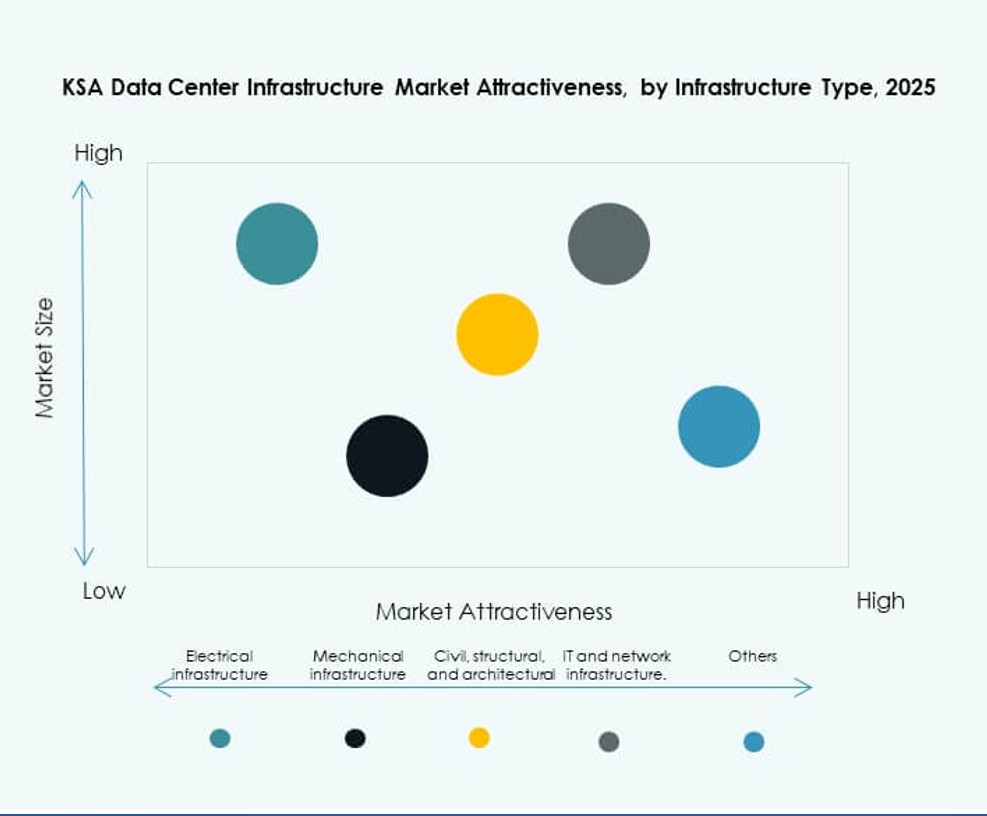

By Infrastructure Type

The KSA Data Center Infrastructure Market is led by electrical and IT & network infrastructure segments. Electrical systems account for the largest share due to high power availability needs in extreme climates. UPS, switchgears, and PDUs dominate this segment. IT & network infrastructure ranks second with strong demand for high-speed storage, servers, and optical fiber. Mechanical infrastructure is growing through efficient cooling units and containment systems. Civil and architectural elements are key in new builds, especially modular systems.

By Electrical Infrastructure

Uninterruptible power supply (UPS) holds the largest share due to reliability needs during outages. Battery Energy Storage Systems (BESS) show fast growth due to sustainability goals. Power distribution units (PDUs) and switchgears enable energy load balancing across critical areas. Utility and grid connection upgrades support high-load zones. The KSA Data Center Infrastructure Market emphasizes smart, scalable power components to match hyperscale needs.

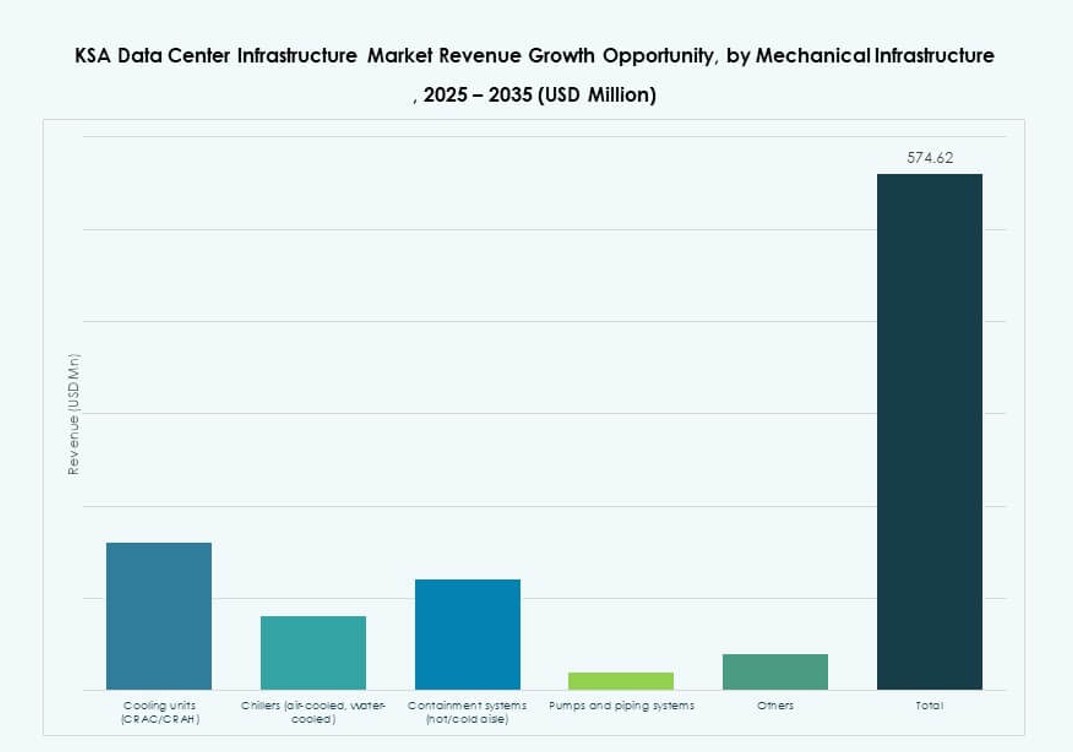

By Mechanical Infrastructure

Cooling units like CRAC and CRAH remain dominant due to high ambient temperatures. Chillers and containment systems gain importance in Tier III and IV facilities. Hot and cold aisle containment improves energy use. Pumps and piping support chilled water systems in hyperscale and enterprise builds. Efficiency and resilience guide mechanical upgrades in the [KSA Data Center Infrastructure Market].

By Civil / Structural & Architectural

Modular building systems grow due to their speed and design consistency. Site preparation and steel/concrete frames form the foundation of new campuses. Raised floors and suspended ceilings enable airflow management. Superstructures and building envelopes are optimized for thermal and seismic conditions. The market adopts prefabricated solutions to meet deployment speed.

By IT & Network Infrastructure

Server and networking equipment dominate IT infrastructure spending. Optical fiber and structured cabling enable high-speed connectivity. Racks and enclosures support cooling efficiency. Storage demand grows with AI and analytics adoption. Vendors offer integrated IT systems tailored for hybrid workloads. The KSA Data Center Infrastructure Market focuses on scalable IT systems to serve hyperscale and enterprise demand.

By Data Center Type

Hyperscale data centers lead with growing deployments from global cloud firms. Colocation follows with strong demand from banking, government, and telecom. Enterprise facilities remain stable, often for private workloads. Edge centers gain traction near logistics and industrial zones. The KSA Data Center Infrastructure Market supports all types based on end-user needs.

By Delivery Model

Turnkey and design-build models dominate for hyperscale and colocation builds. Retrofit/upgrade demand grows in existing enterprise campuses. Modular factory-built delivery enables speed and cost control. Construction management remains relevant for large campuses. The KSA Data Center Infrastructure Market shows rising preference for integrated delivery solutions.

By Tier Type

Tier III leads due to demand for uptime and N+1 resilience. Tier IV gains in government and finance deployments. Tier I and II serve smaller or regional builds. Redundancy, fault tolerance, and SLA needs drive tier selection. The KSA Data Center Infrastructure Market aligns tier investments with business criticality and compliance needs.

Regional Insights

Central Region – Riyadh Leads with 46% Market Share Due to Government, Financial, and Hyperscale Demand

Riyadh dominates the [KSA Data Center Infrastructure Market], driven by digital government initiatives, banking sector demand, and hyperscale cloud deployments. It hosts key ministries, enterprise HQs, and regional offices of global providers. Strong grid infrastructure, power availability, and land access enhance its appeal. The region also sees strategic public-private collaborations.

- For example, Al Moammar Information Systems (MIS) received a Development Commencement Notice for a 72 MW data center expansion under a 112 MW framework agreement with Saudi Data Centres Fund 1, valued at approximately 3 billion SAR, with financial impact starting Q1 2026.

Western Region – Jeddah Commands 28% Share with Strategic Location and Subsea Cable Access

Jeddah ranks second due to its port connectivity, commercial zone expansion, and proximity to Africa and Europe subsea cables. Content delivery networks and media companies prefer the location for regional distribution. The growing e-commerce, transport, and hospitality sector strengthen local demand. Investment in edge and enterprise facilities supports growth.

- For instance, Oracle expanded its public cloud region in Riyadh and enhanced the existing Jeddah region under a US $1.5 billion investment to build advanced cloud and AI infrastructure in Saudi Arabia. The expansion reinforces growth in the KSA Data Center Infrastructure Market and supports broader digital transformation goals.

Eastern Region – Dammam and Khobar Gain 18% Share with Industrial and Oil Sector Needs

Eastern Province holds growing potential with demand from energy, petrochemical, and logistics sectors. Dammam and Khobar see investments in industrial cloud and edge nodes. Smart factory rollouts and oilfield digitization drive localized processing needs. NEOM adds future demand with smart infrastructure needs. The region sees interest in scalable and modular solutions.

Competitive Insights:

- Khazna Data Centers

- Gulf Data Hub

- Center3 (stc)

- G42 / Core42

- Equinix, Inc.

- Schneider Electric

- Vertiv Group Corp.

- Dell Inc.

- Cisco Systems, Inc.

- IBM

The KSA Data Center Infrastructure Market features a mix of domestic and global players competing across hyperscale builds, colocation operations, and infrastructure systems. Local giants like Center3 and Gulf Data Hub focus on expanding colocation and sovereign cloud capacity, aligned with Vision 2030. Khazna and G42 bring regional strength through integrated GCC strategies. Global firms such as Equinix and IBM target enterprise workloads and partner with telecom operators to deepen regional reach. Equipment leaders like Schneider Electric, Vertiv, and Dell supply core power, cooling, and IT infrastructure to Tier III and IV sites. The market favors players with modular capabilities, ESG-aligned designs, and edge computing support. It rewards firms that offer high-availability, scalable infrastructure with localized service models. Competitive advantage depends on integration speed, power efficiency, and ecosystem partnerships.

Recent Developments:

- In December 2025, Khazna acquired a 225,000-square-metre land parcel in Dammam, Saudi Arabia, to build up to 200 MW of AI-ready data center capacity, marking its first facility in the Kingdom.

- In October 2025, Core42, a G42 company, unveiled a self-service, on-demand AI Cloud platform powered by NVIDIA accelerated computing at GITEX Global 2025 enabling instant deployment of AI workloads.