Executive summary:

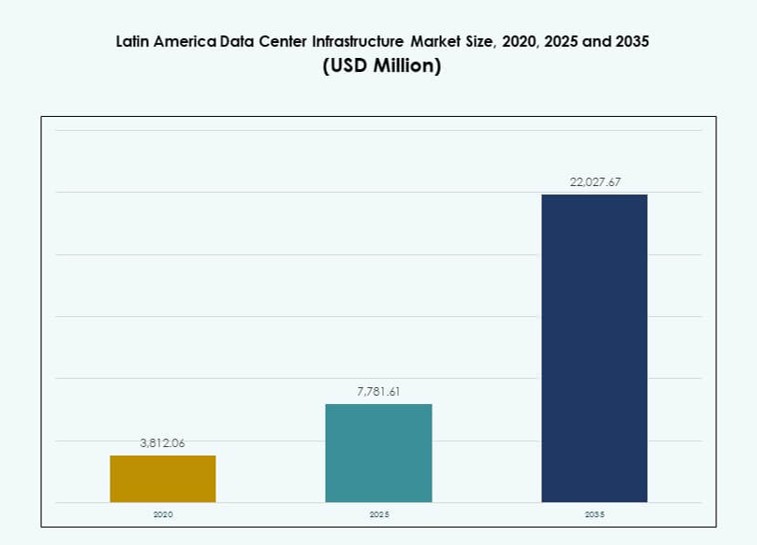

The Latin America Data Center Infrastructure Market size was valued at USD 3,812.06 million in 2020 to USD 7,781.61 million in 2025 and is anticipated to reach USD 22,027.67 million by 2035, at a CAGR of 10.89% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Latin America Data Center Infrastructure Market Size 2025 |

USD 7,781.61 Million |

| Latin America Data Center Infrastructure Market, CAGR |

10.89% |

| Latin America Data Center Infrastructure Market Size 2035 |

USD 22,027.67 Million |

Rising demand for cloud services, AI processing, and data-intensive applications is transforming the region’s digital infrastructure. Enterprises are modernizing legacy systems, and public sector agencies are advancing e-government initiatives. Innovation in cooling systems, modular builds, and renewable energy integration is reshaping facility design. Strong investor interest and strategic partnerships highlight the market’s role in regional digital transformation. Telecom firms and hyperscale operators are scaling operations to meet evolving latency and bandwidth needs. The market’s growth trajectory signals strong long-term potential for infrastructure developers, service providers, and equipment vendors.

Brazil leads the market due to its hyperscale deployments, robust fiber backbone, and growing enterprise IT adoption. Mexico and Chile follow, benefiting from proximity to global traffic routes, stable regulatory frameworks, and renewable energy sources. Colombia, Peru, and Argentina are emerging hubs driven by rising enterprise demand, improving connectivity, and government-backed digital expansion. These countries are gaining traction as new capacity zones in the regional data center ecosystem.

Market Dynamics:

Market Drivers

Rise in Cloud Computing and Digital Transformation Across Enterprise and Public Sectors

Cloud adoption is surging across Latin America, driven by demand for scalable digital services. Enterprises in finance, retail, and manufacturing are migrating to cloud-based operations for agility. Governments are also digitalizing public services, fueling data center buildouts. The Latin America Data Center Infrastructure Market benefits from this shift, creating strong demand for modernized infrastructure. Tier III and IV facilities are being prioritized to ensure uptime and security. Global hyperscale operators are entering the region through acquisitions and greenfield investments. Local providers are scaling operations to compete on latency and capacity. Investors view this as a long-term infrastructure opportunity aligned with enterprise digitization.

- For instance, in May 2024, Microsoft announced a R$14.7 billion (USD 2.9 billion) investment to expand its cloud and AI infrastructure across São Paulo state, with new data center campuses planned in Hortolândia and Sumaré.

Increased Deployment of AI, IoT, and Edge Devices Demands Low-Latency Infrastructure

Growing use of AI-driven applications, video analytics, and industrial IoT is reshaping infrastructure needs. Businesses require low-latency systems to support real-time analytics and device coordination. The Latin America Data Center Infrastructure Market is responding with edge and regional data centers. Telecom firms are upgrading networks to support distributed workloads. Demand for AI-ready servers, advanced cooling, and high-speed interconnects is accelerating. Infrastructure players are designing facilities to handle intensive workloads efficiently. Investors are backing buildouts targeting near-user deployment zones. This shift reinforces the importance of agile infrastructure for business continuity and growth.

- For instance, in 2024, Telefónica deployed edge computing nodes across its Latin American network, enabling sub‑10 millisecond latency for industrial IoT and video analytics use cases in Brazil and Colombia.

Strategic Push for Renewable Integration and Energy Efficiency in Data Center Design

Sustainability is becoming a critical factor in facility design and operation. Operators are integrating renewable energy sources and battery storage systems to reduce carbon intensity. The Latin America Data Center Infrastructure Market aligns with global ESG goals through energy optimization. Governments are offering incentives for clean energy adoption. Developers are prioritizing efficient cooling and modular construction to limit emissions. Sustainable infrastructure attracts institutional capital focused on green assets. Power purchase agreements with renewable firms are common among hyperscale operators. Energy efficiency is emerging as a competitive differentiator in regional project bidding.

Strong Policy Support and Regulatory Incentives Accelerate Infrastructure Investments

National digital agendas and public-private initiatives are catalyzing market growth. Governments across Brazil, Chile, and Mexico are offering tax incentives and fast-track approvals. The Latin America Data Center Infrastructure Market benefits from stable policy frameworks for ICT expansion. Regulatory clarity around data privacy and cross-border flows boosts investor confidence. Local agencies are supporting smart city deployments and regional interconnectivity projects. Such efforts encourage global players to localize operations. Policy-driven infrastructure clusters are emerging in tech parks and economic zones. This environment creates favorable conditions for capacity addition and long-term leasing commitments.

Market Trends

Surge in Hyperscale and Multi-Tenant Colocation Facilities to Meet Expanding Cloud Demand

Hyperscale facilities are increasing across Latin America to meet cloud and platform provider needs. Colocation providers are expanding white space and power capacity to support multi-tenant clients. The Latin America Data Center Infrastructure Market is witnessing strong leasing activity from SaaS and IaaS players. Interconnection density and carrier-neutral models are in focus. Hyperscale customers seek scalable, high-redundancy environments with access to submarine cables. Facilities in key metros are being designed with 20MW–80MW load profiles. This trend is pushing real estate and energy planning at strategic industrial zones.

Adoption of Liquid Cooling Systems and Thermal Innovation to Support AI Workloads

Thermal management is evolving with rising rack densities and GPU deployments. Operators are adopting liquid cooling, including direct-to-chip and immersion systems. The Latin America Data Center Infrastructure Market is moving beyond traditional air cooling in high-performance zones. Energy savings and footprint reduction are key advantages. Data centers hosting AI and HPC workloads prioritize advanced thermal design. Vendors are introducing closed-loop systems to manage heat in confined spaces. This trend is enabling vertical scaling within brownfield expansions. Adoption is expected to grow in metro hubs with power constraints.

Growth of Modular and Prefabricated Data Centers to Accelerate Deployment Timelines

To meet fast-track demand, modular and prefabricated data centers are gaining traction. Factory-built units reduce construction time and simplify permitting. The Latin America Data Center Infrastructure Market benefits from modular design in underdeveloped and remote locations. Enterprises deploy pre-assembled pods for regional redundancy. Modular setups also aid in phased capacity planning and hybrid cloud integration. Operators can shift capex to opex through flexible design-build models. Vendors are standardizing modular kits for power, cooling, and IT zones. This model suits government, telecom, and BPO-driven demand clusters.

Integration of Battery Energy Storage Systems and Smart Grid Interfaces for Energy Resilience

Battery energy storage systems (BESS) are being integrated to enhance uptime and grid flexibility. Data centers are connecting with smart grid platforms to optimize load and frequency response. The Latin America Data Center Infrastructure Market is adopting lithium-ion and advanced chemistries for long-duration backup. Facilities are blending solar or wind with onsite storage to manage peak demand. BESS reduces reliance on diesel generators and supports ESG targets. Operators are using AI for battery lifecycle monitoring. These systems support demand response programs in regions with grid variability.

Market Challenges

Limited Grid Reliability, High Power Costs, and Infrastructure Bottlenecks Affect Operational Stability

Many Latin American countries face challenges with unstable power grids and high electricity costs. Frequent outages force data centers to rely heavily on diesel generators and UPS systems. This raises both capital expenditure and operational complexity. In rural and secondary cities, grid expansion lags behind digital infrastructure demand. The Latin America Data Center Infrastructure Market must account for these issues during site selection and design. Regulatory hurdles, long permitting cycles, and unclear zoning laws further delay project execution. Infrastructure costs are also high due to limited domestic component manufacturing. These barriers increase project risk and require strategic partnerships with local utilities and governments.

Shortage of Skilled Workforce and Limited Vendor Ecosystem Hinders Rapid Scaling

There is a shortage of qualified data center professionals in fields like HVAC, power systems, and network architecture. Training and certification programs are limited in many regional markets. The Latin America Data Center Infrastructure Market faces delays in commissioning due to this talent gap. International vendors dominate core systems, which inflates costs and limits local integration capabilities. Import dependence also makes the sector vulnerable to supply chain disruptions. Fragmented vendor ecosystems complicate large-scale deployments. Operators must invest in workforce development, localization, and supplier diversification to overcome these issues.

Market Opportunities

Expansion of Greenfield Developments and Regional Clusters in Emerging Cities Across Latin America

Several emerging cities across Peru, Colombia, Argentina, and Ecuador are seeing greenfield data center projects. Government support, improved connectivity, and land availability attract investments in new zones. The Latin America Data Center Infrastructure Market is expanding beyond top-tier metros into regional hubs. Demand for localized hosting, low-latency delivery, and sovereign data storage is driving these developments. Investors are targeting growth corridors with strong fiber infrastructure and renewable energy access.

Cross-Border Connectivity, AI-Driven Demand, and Digital Inclusion Fuel Long-Term Upside

New submarine cable projects and AI adoption trends are expanding market potential. Operators are investing in infrastructure that connects Latin America to the U.S., Europe, and Africa. The Latin America Data Center Infrastructure Market is poised to benefit from increased international bandwidth and content demand. Cloud-native enterprises and OTT platforms require high-throughput, scalable systems. This creates long-term opportunities for colocation, interconnection, and hybrid service models.

Market Segmentation

By Infrastructure Type

The Latin America Data Center Infrastructure Market is dominated by electrical infrastructure, given its critical role in ensuring uptime and reliability. IT and network infrastructure follow closely, driven by the rise in cloud and enterprise workloads. Mechanical and civil infrastructure segments are expanding due to large-scale greenfield deployments and prefabricated builds. Each component plays a vital role in capacity planning and energy optimization strategies.

By Electrical Infrastructure

Uninterruptible power supply (UPS) systems lead the electrical infrastructure segment, as uptime remains critical across Tier III and Tier IV facilities. Battery energy storage systems (BESS) are growing rapidly due to their ESG alignment and grid resilience capabilities. Transfer switches, PDUs, and switchgears are also seeing strong demand, especially in hyperscale environments requiring high load balancing.

By Mechanical Infrastructure

Cooling units, including CRAC and CRAH, dominate the mechanical infrastructure due to their reliability and ease of integration. However, chillers and containment systems are gaining share, driven by higher rack densities and need for precision cooling. The use of hot/cold aisle containment improves energy efficiency, and operators are expanding adoption of liquid-cooled systems.

By Civil / Structural & Architectural

Superstructure and modular building systems are driving the segment due to demand for scalable and fast-track deployments. Building envelope solutions and raised floors support airflow optimization and thermal control. Site preparation and structural design are key for seismic stability, especially in countries like Chile and Peru with higher geological risks.

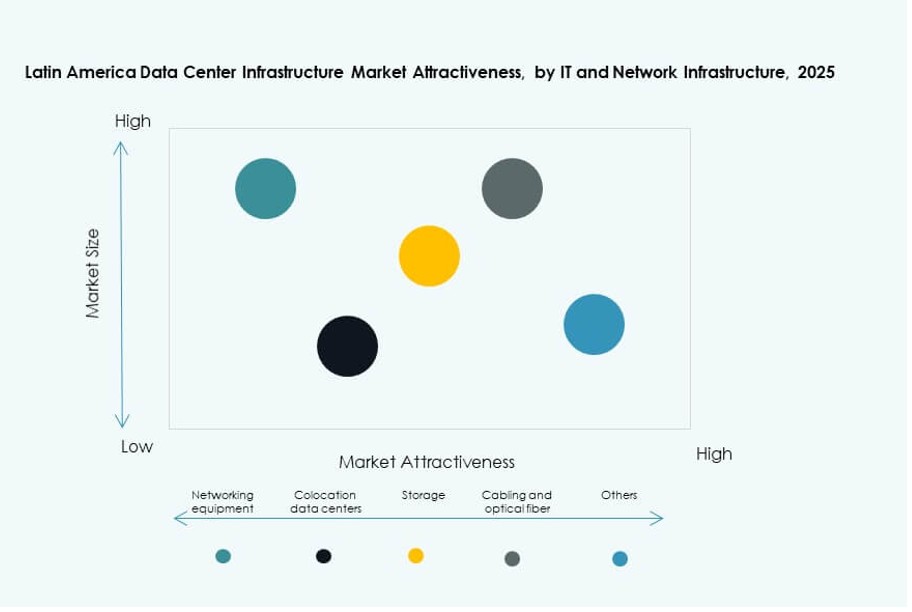

By IT & Network Infrastructure

Servers and networking equipment dominate this segment due to hyperscale deployments and AI-led computing needs. Storage and cabling systems are also growing due to multi-tenant data centers expanding cross-connect offerings. Racks and enclosures are evolving to support higher weight loads and denser layouts, enhancing equipment performance and airflow.

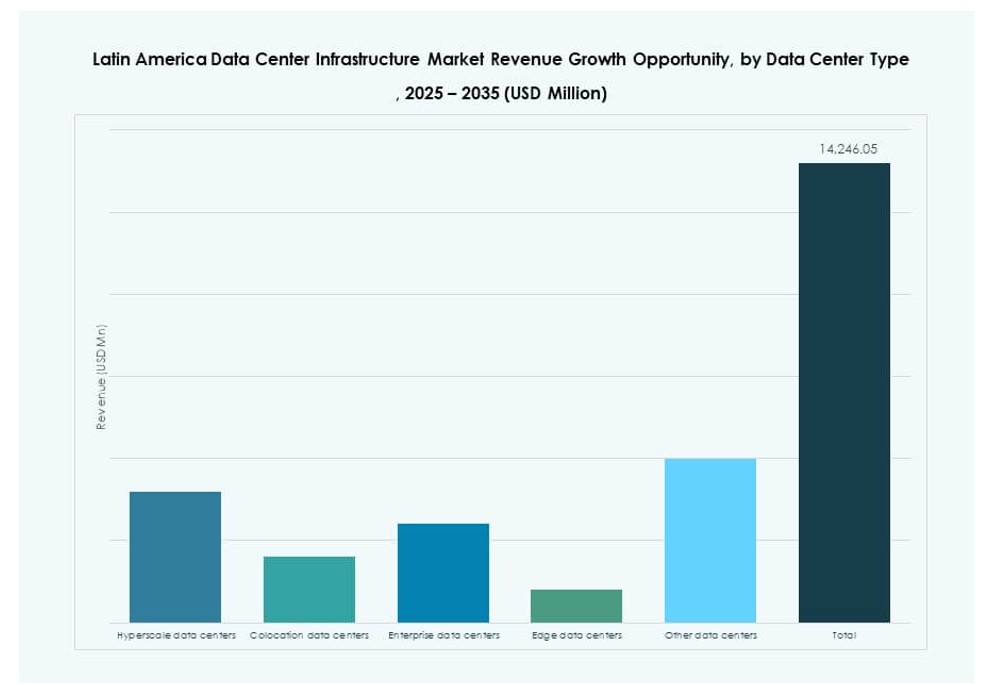

By Data Center Type

Hyperscale data centers hold the largest share in the Latin America Data Center Infrastructure Market, driven by cloud providers and OTT platforms. Colocation facilities are also expanding, offering enterprises lower capex models. Edge data centers are gaining momentum in underserved areas to support low-latency delivery for IoT and content platforms.

By Delivery Model

Turnkey and design-build models dominate due to their speed and end-to-end integration. Retrofit and modular builds are increasing in urban zones where space constraints and energy upgrades are priorities. EPC contractors are seeing demand in hyperscale projects requiring scalable design with integrated MEP and IT systems.

By Tier Type

Tier III facilities lead in deployment due to their balance between performance and cost. Tier IV data centers are being built for mission-critical workloads requiring full fault tolerance. Tier I and II remain in use for edge and smaller enterprise setups, especially in secondary cities with moderate hosting needs.

Regional Insights

Brazil Dominates the Market with 45% Share Due to Urban Density, Subsea Connectivity, and Cloud Demand

Brazil holds around 45% of the Latin America Data Center Infrastructure Market share, making it the largest contributor. São Paulo is a key hub due to its dense enterprise base and access to multiple submarine cables. Major hyperscale providers and colocation firms have established multi-MW campuses. The government supports ICT infrastructure through tax benefits and smart city initiatives. Brazil’s cloud adoption rate and regional connectivity further reinforce its leadership position.

- For instance, in November 2025, Omnia, backed by Brazilian investment firm Pátria, joined a project in Brazil’s Pecém port complex featuring a planned 300 MW power capacity, marking one of the country’s largest single-client data center developments.

Mexico and Chile Account for 30% Combined Due to Strategic Location and Policy Stability

Mexico and Chile together contribute roughly 30% of the regional market. Mexico benefits from proximity to the U.S., robust manufacturing, and financial sectors needing low-latency services. Chile’s political stability, renewable energy capacity, and connectivity to Pacific routes support sustained growth. Both countries attract hyperscale and colocation investments focused on regional coverage and regulatory clarity.

- For instance, in October 2025, Equinix filed environmental declarations to develop its fifth data center (ST5) in Santiago, Chile, expanding its presence with a new multi‑MW facility in one of the region’s key Pacific-connected digital hubs.

Argentina, Colombia, and Peru Represent 25% as Emerging Growth Clusters in the Region

Argentina, Colombia, and Peru contribute about 25% of the Latin America Data Center Infrastructure Market. These countries are emerging as growth hubs due to improved policy frameworks and expanding digital ecosystems. Colombia is a rising connectivity hub in the Andean region. Argentina and Peru are seeing new builds aimed at financial services, telecom, and BPO sectors. Investments are shifting toward secondary cities in these nations to expand access and reduce latency.

Competitive Insights:

- Scala Data Centers

- Ascenty

- ODATA Data Centers

- Equinix, Inc.

- KIO

- MDC Data Centers

- Huawei Technologies Co., Ltd.

- Schneider Electric

- Vertiv Group Corp.

- Hewlett Packard Enterprise (HPE)

The Latin America Data Center Infrastructure Market features a mix of regional specialists and global infrastructure giants. Scala Data Centers and Ascenty dominate hyperscale buildouts across Brazil and Chile, leveraging green power and scalable designs. ODATA and KIO support enterprise colocation growth across Mexico, Colombia, and Peru. Global players such as Equinix and Huawei strengthen cross-border connectivity and integrated services. Power and cooling leaders like Schneider Electric and Vertiv enable energy-efficient builds with modular systems. HPE and other IT vendors provide scalable computing and storage for hybrid workloads. It is becoming more competitive as providers localize operations, form regional alliances, and expand edge deployments to meet latency demands. Strategic investments, sustainability leadership, and multi-region presence define the positioning strength of key players in this evolving infrastructure landscape.

Recent Developments:

- In September 2025, ODATA, a subsidiary of Aligned Data Centers, officially announced a landmark $1.02 billion green financing packageto accelerate sustainable data center development across Latin America.

- In August 2025, ODATA launched its fourth hyperscale data center, QR04, near San Miguel de Allende in Mexico’s Querétaro region, with 24 MW capacity using Aligned’s Delta³ cooling technology. This facility completes a network of interconnected sites to meet surging AI and cloud needs.

- In July 2025, Scala Data Centers secured USD 328 million in international financing for expanding three data centers and building a power substation in Chile. This marks the largest project finance deal for a single-country data center initiative in Latin America, supporting 23 MW of contracted IT capacity and additional reserved expansion.