Executive summary:

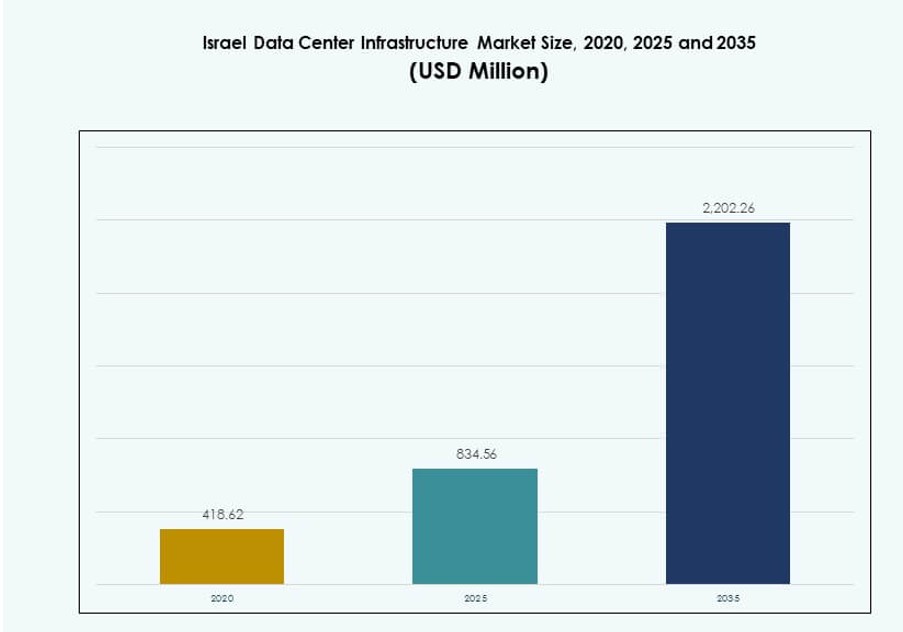

The Israel Data Center Infrastructure Market size was valued at USD 418.62 million in 2020, rising to USD 834.56 million in 2025, and is anticipated to reach USD 2,202.26 million by 2035, at a CAGR of 10.11% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Israel Data Center Infrastructure Market Size 2025 |

USD 834.56 Million |

| Israel Data Center Infrastructure Market, CAGR |

10.11% |

| Israel Data Center Infrastructure Market Size 2035 |

USD 2,202.26 Million |

The market is expanding rapidly due to accelerated cloud adoption, AI-based workloads, and rising data localization needs. Enterprises and government agencies are investing in scalable infrastructure to support mission-critical applications and compliance-driven digital systems. Innovation in cooling technologies, software-defined networking, and modular deployment models is driving transformation across the ecosystem. Investors view the market as a strategic entry point into the Middle East digital corridor, leveraging Israel’s cybersecurity leadership and tech-driven economy.

Tel Aviv leads the market due to its dense tech clusters, reliable grid, and connectivity infrastructure. Emerging zones like Be’er Sheva and Haifa are gaining traction due to cyber defense initiatives, academic collaboration, and smart city development. These regions benefit from targeted government support, growing cloud demand, and availability of skilled digital talent.

Market Dynamics:

Market Drivers

Cloud Service Expansion Driving High-Density Facility Investments and Infrastructure Scalability

Rapid cloud adoption is pushing demand for scalable, high-density data center infrastructure. Israel’s digital economy depends on real-time data processing, AI workloads, and low-latency platforms. Global hyperscalers and local cloud firms are building high-performance facilities with modular expansion plans. The Israel Data Center Infrastructure Market benefits from cloud-driven investments in cooling, power, and software-defined networks. IT infrastructure must support dynamic workloads and elastic scalability for seamless business continuity. Cloud providers prioritize Tier III and Tier IV readiness for fail-safe operations. Enterprises seek hybrid cloud platforms that blend private and public workloads securely. Data-intensive industries like banking, defense, and healthcare demand secure, redundant setups. High computing intensity is reshaping facility design standards.

Rise in AI, IoT, and Cybersecurity Demand Accelerating the Upgrade of Core Infrastructure Layers

Growing AI, IoT, and cybersecurity applications require low-latency compute nodes and real-time response systems. Machine learning workloads drive GPU-heavy configurations and precision cooling needs. Smart city initiatives demand infrastructure that supports high data throughput and security. The Israel Data Center Infrastructure Market enables this evolution with advanced IT and mechanical systems. Investors target facilities with software-defined power and automated failover capacity. Cybersecurity infrastructure must comply with strict national defense regulations. Integration of AI-based monitoring enhances uptime, energy use, and threat detection. Government and defense sectors influence tech choices in power backup and data isolation. Innovation in control systems strengthens infrastructure resilience for high-risk environments.

- For instance, AWS launched its Israel (Tel Aviv) Region in 2023 with three availability zones in locations including Tnuvot, Shoham, and Har Tov industrial park. Smart city initiatives demand infrastructure that supports high data throughput and security.

Government Policy Support and National Digital Transformation Framework Strengthening the Infrastructure Push

Israel’s Ministry of Communications and other agencies promote strategic digital infrastructure through policy and incentives. National frameworks support cloud-first initiatives, digital ID rollouts, and e-government platforms. These create foundational demand for stable and scalable data center infrastructure. The Israel Data Center Infrastructure Market aligns with government-led transformation goals. Urban tech zones and industrial parks encourage infrastructure investment near population and tech hubs. Public-private collaboration fuels Tier III and IV readiness in core regions. Regulatory frameworks enable speed in permits and clarity in design standards. Energy efficiency goals also push for sustainable infrastructure, backed by government carbon targets. This synergy supports long-term investor confidence.

Private Sector Digitization Across Banking, Healthcare, and Telecom Pushing Colocation and Edge Growth

Banking, healthcare, and telecom players are digitizing services at scale, driving colocation and edge site demand. Large private institutions offload infrastructure burden via reliable colocation models. Edge centers address low-latency needs for mobile services, fintech platforms, and real-time patient data. The Israel Data Center Infrastructure Market responds with scalable modular edge designs and enhanced connectivity. Telecom players focus on 5G-enabled edge nodes to reduce central server load. Colocation providers invest in physical and virtual security upgrades for enterprise clients. Medical data compliance and privacy norms demand isolated compute clusters with regulated access. Investors view this mix as a recurring revenue stream with rising demand certainty. Edge facilities near urban hubs improve network efficiency and app performance.

- For instance, PayBox, supervised by the Bank of Israel, fully hosts its operations on Google Cloud for regulatory compliance and to serve millions of daily customers.

Market Trends

Shift Toward Software-Defined Infrastructure and AI-Based Management for Operational Efficiency

Data centers across Israel are adopting software-defined architectures to improve automation and resource control. This trend is replacing traditional static infrastructure with programmable, adaptive systems. Software-defined power and cooling enhance efficiency during peak and idle loads. The Israel Data Center Infrastructure Market is embracing these trends to improve cost control and uptime. AI-driven data center infrastructure management (DCIM) tools improve predictive maintenance and thermal optimization. Real-time analytics help operators detect anomalies before outages occur. Dynamic resource allocation adapts to workload shifts in cloud-native environments. AI systems reduce human intervention in routine processes. This shift improves operational reliability and long-term sustainability.

Growing Use of Modular and Prefabricated Designs for Speed, Flexibility, and Scalability

Modular and prefabricated building systems are gaining traction for faster deployment and cost control. These systems are factory-built, tested, and assembled onsite with reduced labor and construction risk. Investors prefer them for edge locations and disaster recovery sites. The Israel Data Center Infrastructure Market is experiencing rising interest in modular deployments for urban and semi-urban regions. Prefabricated structures reduce energy waste and ease regulatory approvals. These models are flexible for scaling in phases and adapting to evolving tech needs. Time-to-market advantages make them ideal for fast-paced digital sectors. Providers benefit from lower upfront construction risk and predictable installation schedules. They also align with green building goals.

Sustainable Infrastructure Demand Growing with Emphasis on Renewable Energy Integration

Data centers face pressure to reduce carbon footprints and energy costs through green technology. Operators focus on integrating solar, wind, and battery storage systems into power architecture. This trend influences UPS systems, cooling design, and building materials. The Israel Data Center Infrastructure Market sees this as a key competitive factor among providers. Energy-efficient cooling technologies, like liquid immersion, are being piloted. Carbon offset models and green certification standards guide infrastructure decisions. Backup systems shift from diesel to gas turbines and fuel cells. Hybrid renewable grid connections support sustainable uptime. Clients increasingly favor providers with visible sustainability commitments.

High-Density Rack Deployment and Liquid Cooling Adoption Gaining Traction in Hyperscale Builds

High-performance computing (HPC) and GPU-intensive workloads require denser rack configurations with specialized thermal systems. Liquid cooling adoption is rising to manage heat output beyond the limits of air cooling. The Israel Data Center Infrastructure Market is adopting these solutions in hyperscale and AI-focused builds. Direct-to-chip and immersion cooling systems are now part of new facility designs. They improve energy efficiency and reduce white space demand. High-density racks support AI, modeling, and fintech applications with continuous processing needs. Liquid cooling helps lower PUE and reduce mechanical infrastructure complexity. These trends reflect a shift toward performance-driven architecture over traditional scale-based models.

Market Challenges

Power Supply Limitations, Grid Reliability, and High Energy Costs Impacting Infrastructure Scalability

Energy cost volatility and power reliability pose major constraints for data center expansion in Israel. Grid capacity is limited in certain industrial areas, restricting the scale of Tier III and IV developments. Operators face high operational costs due to electricity pricing structures and peak load tariffs. The Israel Data Center Infrastructure Market must navigate these constraints through energy-efficient design and grid collaboration. Battery Energy Storage Systems (BESS) adoption remains slow due to high upfront costs. Renewable energy integration is complex due to permitting and variability in supply. Power backup systems must meet stringent uptime standards while minimizing emissions. Grid dependency creates delays in large-scale builds and scaling of colocation facilities.

Security, Regulatory Compliance, and Land Scarcity Creating Structural and Design-Level Complexities

Geopolitical tensions and national security considerations mandate strict control over data movement and facility access. Compliance with defense-related data norms adds cost and limits flexibility in site design. Land availability for new builds is constrained near major urban zones. The Israel Data Center Infrastructure Market faces site approval delays due to environmental and zoning requirements. Design teams must accommodate blast-proof architecture and biometric access in critical facilities. Edge deployments in rural areas face connectivity gaps and high fiber installation costs. Regulatory ambiguity around data localization creates investment hesitation. Cross-border partnerships must comply with cyber laws and joint control frameworks.

Market Opportunities

Rising Demand for Colocation, Edge Facilities, and Interconnectivity Among Regional Cloud Players

The growth of regional cloud firms and digital service platforms fuels demand for flexible, scalable colocation solutions. Edge sites near user clusters improve latency and reduce congestion. The Israel Data Center Infrastructure Market is positioned to offer hybrid deployment models that combine urban density and rural edge resilience. Colocation providers can capture rising demand from SMBs and fintech companies. Interconnection hubs offer cross-carrier access and direct cloud onramps, expanding addressable opportunities.

Expansion of Smart Cities, E-Governance Platforms, and Health Data Systems Drives Future Demand

National programs for smart governance, digital health records, and defense modernization increase infrastructure needs. The Israel Data Center Infrastructure Market supports this demand with robust civil and IT infrastructure capabilities. Smart cities need real-time processing at the edge, while hospitals require compliant data hosting. Future demand will arise from AI governance, defense cloud systems, and citizen platforms requiring continuous uptime and security.

Market Segmentation

By Infrastructure Type

The Israel Data Center Infrastructure Market sees dominance in electrical infrastructure, driven by backup power and load balancing needs. Mechanical systems follow due to complex cooling requirements for HPC and AI workloads. IT and network infrastructure gain traction with rising digital service penetration. Civil/structural infrastructure demand rises in modular builds. Others include environmental monitoring and safety systems critical for data center uptime and compliance.

By Electrical Infrastructure

Uninterruptible Power Supply (UPS) systems lead due to their role in maintaining uptime during outages. Power Distribution Units (PDUs) and Battery Energy Storage Systems (BESS) grow as grid resilience becomes a focus. Transfer switches and grid connectivity remain essential for seamless operations. Israel’s energy pricing and stability challenges make this segment vital for Tier III and IV builds.

By Mechanical Infrastructure

Cooling units such as CRAC and CRAH dominate the mechanical segment due to high-density workloads. Chillers, especially air-cooled, are preferred for moderate energy efficiency. Containment systems improve cooling efficiency and airflow control. Pumps and piping systems ensure optimal thermal transfer. The market adopts liquid cooling systems in high-performance builds, accelerating this segment’s importance.

By Civil / Structural & Architectural

Site preparation and foundations form the core of early-phase construction. Raised floors and suspended ceilings are widely adopted to support flexible cabling and airflow. Modular/prefabricated building systems gain popularity for speed and scalability. Superstructures built with steel or concrete frames enable seismic resilience and longevity. Envelope systems focus on thermal insulation and structural integrity.

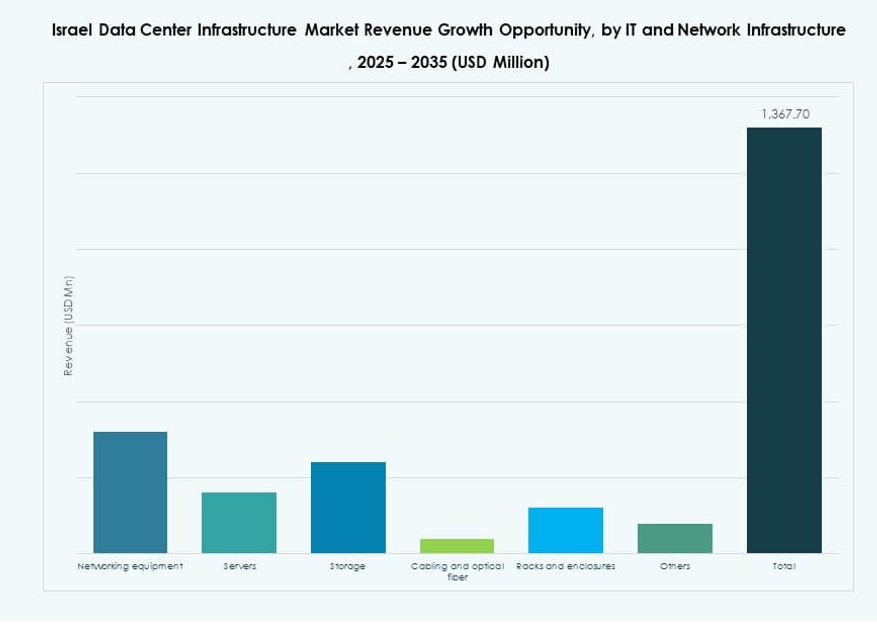

By IT & Network Infrastructure

Server infrastructure leads due to cloud and AI processing needs. Networking equipment and storage solutions follow closely for managing throughput and redundancy. Racks and enclosures grow with demand for high-density equipment. Optical fiber cabling supports fast interconnectivity between zones. Israel’s tech ecosystem boosts this segment’s scale and innovation.

By Data Center Type

Colocation data centers dominate due to enterprise outsourcing trends. Hyperscale growth is limited to select cloud and defense players. Edge centers expand near mobile and smart city clusters. Enterprise data centers exist for core industries needing private infrastructure. Others include academic or research-based centers with specialized workloads.

By Delivery Model

Design-build/EPC leads the segment with turnkey projects for global clients. Retrofit/upgrade models gain momentum in older facilities being modernized. Modular factory-built systems accelerate rollout timelines. Construction management and turnkey delivery models serve well in phased deployments. Hybrid models combining EPC and modular are emerging.

By Tier Type

Tier III remains dominant due to its balance of uptime and cost. Tier IV adoption grows in defense and finance segments. Tier II is still relevant for small enterprise builds. Tier I exists in test and development facilities. Israel’s regulatory push supports growth toward Tier III and above, especially in colocation and cloud zones.

Regional Insights

Tel Aviv Metropolitan Area Leads with 52% Market Share Due to Dense Tech Ecosystem and Infrastructure

Tel Aviv holds the largest share of the Israel Data Center Infrastructure Market due to its role as the digital and financial capital. The region has advanced power grids, dense fiber networks, and proximity to headquarters of banks, startups, and telecoms. Major colocation and cloud providers choose Tel Aviv for its reliable uptime infrastructure. Hyperscale projects and modular designs also concentrate here for operational scale and ecosystem integration. Market share stands at 52%, led by urban demand and consistent energy infrastructure.

- For instance, MedOne’s flagship data center operates 15 meters underground within a Tier IV-certified facility, offering 72-hour autonomous operation capability.

Northern District, Including Haifa, Accounts for 26% Share Driven by R&D and Industrial Integration

Haifa and nearby areas in the Northern District represent 26% of the market, benefiting from research institutions and industrial zones. Tech parks and military-industrial collaboration drive demand for resilient infrastructure. Haifa Port adds connectivity for international cloud players and subsea cable projects. These regions favor hybrid cloud and defense-grade data infrastructure. Data privacy compliance and proximity to academic centers attract enterprise deployments in these zones.

Southern Region Including Be’er Sheva Holds 22% Market Share Supported by Smart City and Cyber Initiatives

Be’er Sheva, with its CyberSpark hub, supports 22% of the Israel Data Center Infrastructure Market. The region focuses on national cyber security, smart governance platforms, and defense cloud operations. Strong government backing and education-industry collaboration create demand for robust infrastructure. Connectivity remains a challenge, but modular edge centers address that gap. The region shows high potential for growth in colocation and military-linked data hosting.

- For instance, MedOne’s Dimona facility offers over 25 MW IT capacity in a highly secure southern location suitable for defense applications.

Competitive Insights:

- Schneider Electric

- Vertiv Group Corp.

- Cisco Systems, Inc.

- Dell Inc.

- IBM

- Equinix, Inc.

- Oracle

- ABB

- Lenovo

- Fujitsu

The Israel Data Center Infrastructure Market features strong competition among global technology providers and regional infrastructure specialists. It is driven by rising demand for scalable, energy-efficient, and secure solutions. Companies such as Schneider Electric and Vertiv lead in electrical and cooling systems, offering advanced modular designs and energy management platforms. Cisco and Dell provide integrated IT infrastructure for hybrid cloud environments. Equinix and Oracle compete through colocation and cloud interconnect services. Localized strategies, strategic partnerships, and custom deployments for hyperscale and enterprise needs shape market success. Players invest in AI-driven monitoring, liquid cooling, and software-defined systems to enhance facility performance. The competitive landscape continues to shift as new builds prioritize sustainability, edge readiness, and government compliance.

Recent Developments:

- In December 2025, ABB entered into an agreement to acquire IPEC, a UK‑based technology firm specializing in electrical diagnostics and predictive monitoring systems. This acquisition enhances ABB’s ability to offer advanced monitoring solutions for data center electrical infrastructure, improving reliability and reducing downtime.

- In April 2025, NED DC commenced construction on its first major facility outside Tel Aviv, marking a significant infrastructure development in the Israel Data Center Infrastructure Market. The project, named Alpha Campus, is designed to support AI and cloud workloads with modern power, cooling, and networking systems.