Executive summary:

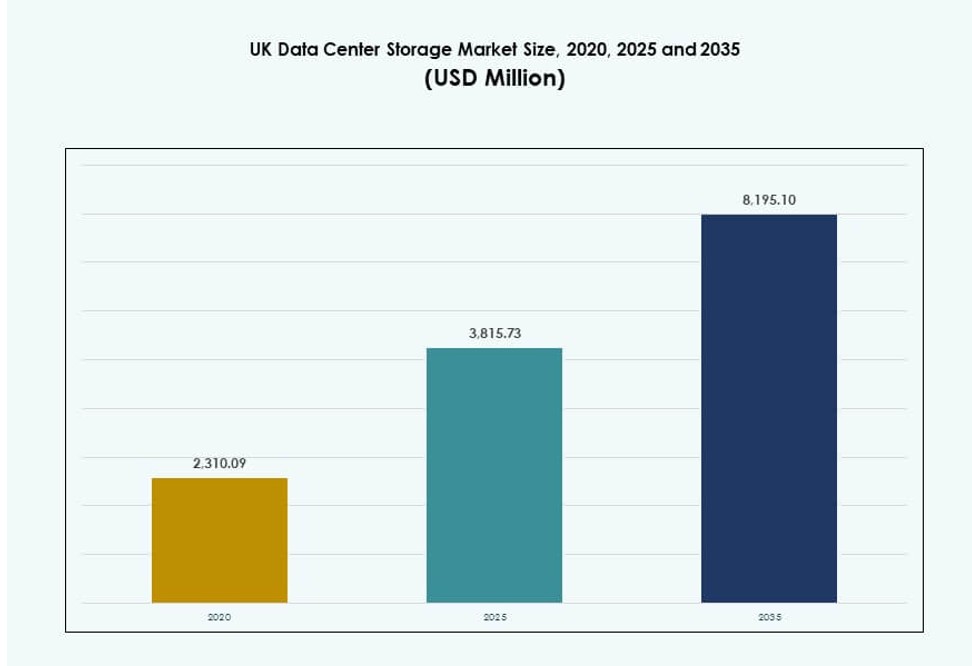

The UK Data Center Storage Market size was valued at USD 2,310.09 million in 2020 to USD 3,815.73 million in 2025 and is anticipated to reach USD 8,195.10 million by 2035, at a CAGR of 7.87% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| UK Data Center Storage Market Size 2025 |

USD 3,815.73 Million |

| UK Data Center Storage Market, CAGR |

7.87% |

| UK Data Center Storage Market Size 2035 |

USD 8,195.10 Million |

Enterprises are modernizing storage infrastructure to support cloud-native workloads, AI, and hybrid IT environments. All-flash arrays, software-defined storage, and NVMe technologies are being adopted to improve performance and scalability. Growing use of data analytics, real-time processing, and workload automation has increased demand for intelligent, high-availability storage systems. Businesses prioritize agility, security, and energy efficiency, making advanced storage critical to digital transformation strategies. The market holds strategic value for investors targeting long-term IT infrastructure resilience.

London remains the leading regional hub due to its hyperscale presence, financial sector concentration, and high connectivity. South East England is growing steadily, driven by expansion in Slough and Reading. Regional markets such as Manchester and Birmingham are emerging due to increasing enterprise activity, edge deployments, and colocation growth. Geographic diversification is helping balance capacity and reduce pressure on primary hubs.

Market Dynamics:

Market Drivers

Rising Enterprise Digitalization Demands Scalable and Resilient Storage Infrastructure

Enterprise digital transformation is a major driver for the UK Data Center Storage Market. Companies across sectors are shifting workloads from legacy systems to high-performance infrastructure. This transition creates sustained demand for secure, scalable, and high-availability storage systems. Cloud-native applications, edge computing, and containerized workloads further accelerate storage needs. It supports business continuity, regulatory compliance, and real-time analytics. Businesses prefer hybrid and multi-cloud environments, prompting growth in flexible storage platforms. Storage also underpins disaster recovery and backup strategies. The market gains importance as storage becomes central to digital business operations.

- For instance, National Grid partnered with Emerald AI in 2024 to pilot grid-interactive data center operations in the UK, aiming to improve power flexibility and efficiency. The project demonstrates how AI-driven systems can dynamically manage energy loads in real time across high-density digital infrastructure.

Innovation in Software-Defined Storage Systems Enhancing Flexibility and Performance

The UK Data Center Storage Market benefits from rapid innovation in software-defined storage (SDS) architecture. SDS enables hardware-agnostic control, enhancing system agility and scalability. Enterprises use SDS to unify storage across cloud, edge, and on-premise environments. This shift increases operational efficiency and lowers total cost of ownership. It supports automation, intelligent tiering, and real-time resource optimization. Storage providers invest in AI-powered analytics and predictive maintenance. New architectures help handle unstructured data growth from IoT, surveillance, and business intelligence. These innovations align with evolving enterprise IT priorities.

- For instance, Pure Storage expanded its Portworx Enterprise 3.0 in November 2022, enhancing Kubernetes data management for production environments with improved scalability across hybrid setups.

Growth in AI, HPC, and Analytics Driving Demand for High-Speed Storage

Workloads such as artificial intelligence, high-performance computing (HPC), and real-time analytics reshape storage demand. The UK Data Center Storage Market supports these intensive applications through faster IOPS, lower latency, and high bandwidth. Businesses adopt NVMe-based systems, all-flash arrays, and parallel file systems. Storage must accommodate massive throughput for training and inference cycles. Enterprises in healthcare, finance, and research sectors require deterministic performance. GPU clusters rely on optimized storage pipelines for peak utilization. These workloads push vendors to offer specialized, high-speed solutions. It becomes a competitive differentiator across data-intensive verticals.

Strategic Cloud Integration Enhancing Data Mobility and Business Continuity

Cloud storage integration is central to storage modernization strategies in the UK Data Center Storage Market. Organizations need seamless movement of data across public, private, and hybrid clouds. This capability supports business agility, application scalability, and secure remote access. Cloud-native tools simplify backup, archiving, and disaster recovery workflows. Storage-as-a-Service (STaaS) solutions are gaining traction among mid-sized enterprises. Multi-cloud environments reduce vendor lock-in and enhance data control. Security, compliance, and governance tools embedded within cloud storage offerings attract regulated industries. It reinforces the market’s strategic role in enterprise IT.

Market Trends

Edge Data Centers Fueling Demand for Distributed and Modular Storage Models

Edge infrastructure expansion drives localized storage demand across the UK. Enterprises deploy micro data centers near end-users to minimize latency. This shift supports real-time processing in sectors like retail, healthcare, and transportation. The UK Data Center Storage Market reflects a rising preference for modular storage units. These systems integrate with edge hardware and require compact form factors. Edge deployments prioritize resilience and low-maintenance architecture. Vendors respond with ruggedized, energy-efficient, and scalable products. This trend diversifies revenue streams beyond traditional hyperscale hubs. Storage innovation supports latency-sensitive applications at the network edge.

Sustainability and Energy Efficiency Becoming Critical Storage Selection Criteria

Enterprises prioritize energy efficiency in storage procurement to meet sustainability targets. The UK Data Center Storage Market evolves with rising ESG commitments across industries. Vendors optimize storage power consumption through energy-aware software and flash-first designs. All-flash arrays offer higher performance per watt than traditional disk-based systems. Efficient cooling, intelligent data placement, and workload-aware tuning reduce energy footprints. Enterprises evaluate carbon intensity of infrastructure in procurement decisions. Energy efficiency also supports operational cost savings. This trend aligns with the UK’s decarbonization goals and corporate sustainability mandates.

Rise of Cyber Resilient Storage Systems to Address Security and Compliance

Cybersecurity concerns reshape storage design across UK data centers. Enterprises seek storage solutions with built-in ransomware protection and data immutability. The UK Data Center Storage Market integrates features like zero-trust architecture, multi-factor authentication, and encryption by default. Storage vendors offer air-gapped backups and versioned snapshots. Industries handling sensitive data, such as healthcare and finance, adopt cyber-resilient systems. Compliance with GDPR and industry regulations requires secure retention and traceability. Security becomes a primary differentiator in vendor selection. This trend boosts demand for tamper-proof, self-healing, and verifiable storage architecture.

Demand for Unified Storage Solutions Supporting Mixed Workloads Across Platforms

Businesses need storage platforms that consolidate block, file, and object data types. The UK Data Center Storage Market responds with unified storage offerings. These solutions reduce infrastructure complexity and simplify data management. Unified systems support diverse workloads—virtual machines, containers, databases, and analytics. This trend supports centralized control, efficient provisioning, and policy-based governance. IT teams streamline operations with single-pane management tools. Unified platforms lower hardware sprawl and improve resource utilization. They enable dynamic scaling across hybrid environments. This approach enhances ROI and supports digital maturity.

Market Challenges

High Capital Costs and Complexity Limiting Access for Small and Medium Enterprises

Storage modernization demands significant capital investment, making it difficult for SMEs to adopt advanced solutions. The UK Data Center Storage Market must address entry barriers created by hardware and licensing costs. Budget constraints lead many small firms to delay upgrades or adopt piecemeal solutions. Storage infrastructure also requires skilled IT teams for setup and maintenance. Complexity in configuration, integration, and performance tuning raises operational challenges. SMEs often lack dedicated teams for continuous monitoring and optimization. Limited access to affordable, scalable storage restricts broader market penetration. This gap slows adoption in emerging business segments.

Data Sovereignty and Regulatory Pressure Complicating Cross-Border Storage Strategies

Strict compliance with GDPR and local data residency laws challenges multinational companies. The UK Data Center Storage Market faces scrutiny around data location, retention, and control. Enterprises must ensure that storage practices align with evolving UK and EU regulations. Cloud vendors and colocation providers must guarantee verifiable compliance. Legal ambiguity around cross-border data transfers increases operational risk. Companies with global operations struggle with storage fragmentation. Storage providers must offer local presence, legal transparency, and real-time auditability. Regulatory complexity slows storage architecture modernization for multinational enterprises.

Market Opportunities

Growing Adoption of AI and Data Analytics in the UK Creating New Storage Requirements

AI and big data adoption offer strong growth opportunities in the UK Data Center Storage Market. Enterprises require fast, scalable systems that support large-scale data ingestion and parallel processing. Storage vendors can tap into demand from life sciences, automotive, and financial analytics. AI inference and model training drive need for performance-optimized, high-capacity storage. It allows providers to differentiate through tailored, application-specific designs.

Government and Public Sector Digital Transformation Unlocking Procurement Potential

Government-led digital initiatives are expanding data infrastructure needs across public sector agencies. The UK Data Center Storage Market can capitalize on storage demand from healthcare, education, and municipal services. Cloud-first strategies create opportunities for Storage-as-a-Service and secure hybrid models. Public funding and policy support lower procurement risks. It enables vendors to scale through public contracts.

Market Segmentation

By Storage Type

Traditional storage holds a moderate share due to existing installations, but demand is shifting rapidly. All-flash storage dominates the UK Data Center Storage Market owing to high performance and lower latency. Hybrid storage solutions are growing among enterprises balancing cost and speed. Other niche storage formats serve archival and specific industrial use cases. Flash adoption continues to rise due to better power efficiency and IOPS.

By Storage Deployment

Storage Area Network (SAN) systems lead the deployment segment due to their reliability and performance. Network-attached Storage (NAS) systems follow closely, popular for shared access and ease of use. Direct-attached Storage (DAS) systems maintain relevance in edge and compact environments. Other architectures include object-based deployments for cloud-native apps. The UK Data Center Storage Market leans towards hybrid SAN-NAS convergence in modern builds.

By Component

Hardware accounts for the largest share in the UK Data Center Storage Market due to capital-intensive infrastructure. This includes arrays, racks, and drives that form the core of storage architecture. Software adoption is increasing with SDS, management layers, and orchestration platforms. Software is gaining share due to its role in automation and AI-driven optimization. Vendors focus on combining robust hardware with intelligent software.

By Medium

Solid-State Drives (SSD) dominate due to performance, energy savings, and compact design. SSD adoption continues to rise across hyperscale and enterprise environments. Hard Disk Drives (HDD) remain relevant for archival and cost-sensitive storage tiers. Tape storage persists in compliance-driven sectors requiring long-term backup. The UK Data Center Storage Market sees a steady shift toward flash-dominant configurations.

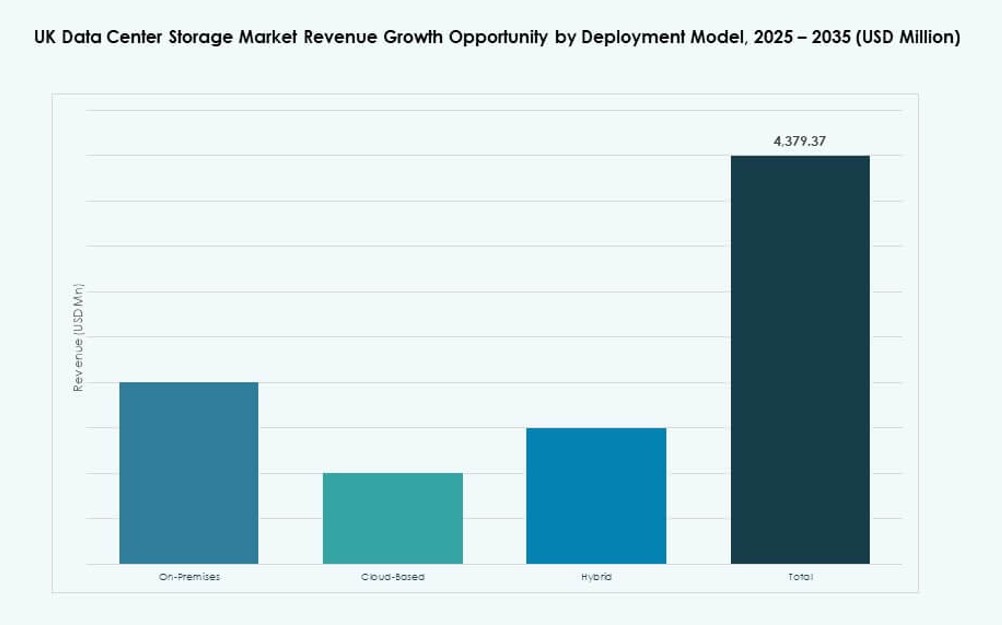

By Deployment Model

Cloud-based deployment leads the UK Data Center Storage Market due to its scalability and remote access. On-premises models retain importance in highly regulated or security-conscious industries. Hybrid deployment is gaining traction by combining cloud flexibility with local control. Enterprises prefer this model for backup, disaster recovery, and workload distribution. Vendors optimize solutions for seamless integration across deployment models.

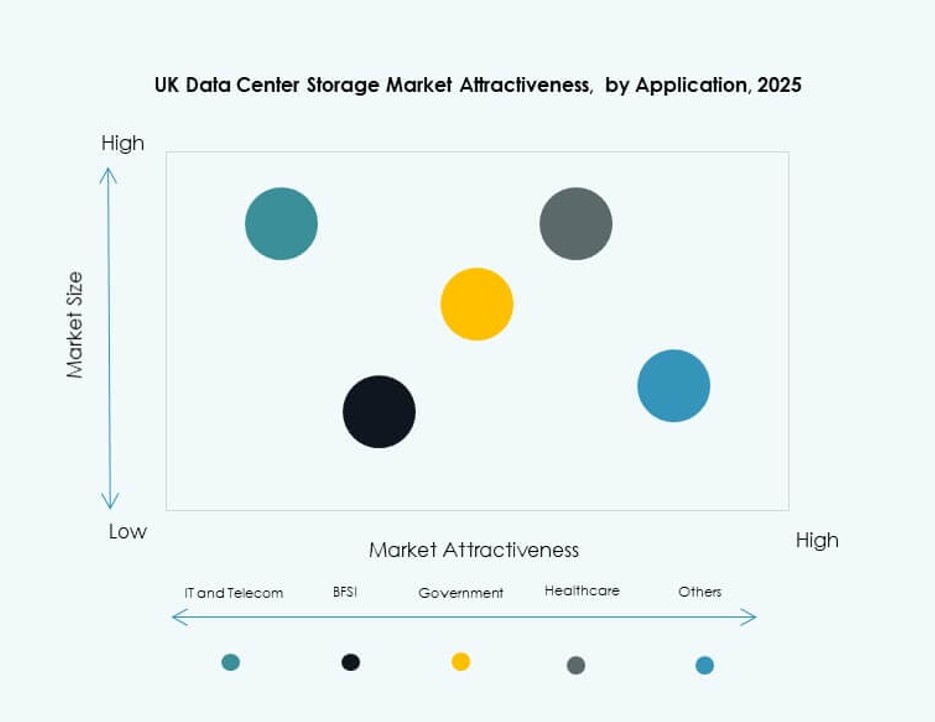

By Application

IT and Telecommunications lead storage demand in the UK Data Center Storage Market due to large-scale data operations. BFSI follows with growing needs for secure, high-performance storage. Government agencies are expanding capacity under digital transformation mandates. Healthcare providers adopt storage solutions for imaging, patient records, and analytics. Other sectors include manufacturing, retail, and education, all requiring scalable storage systems.

Regional Insights

London Leading the Market with Over 45% Share Driven by Hyperscale and Financial Sectors

London dominates the UK Data Center Storage Market with over 45% share due to dense hyperscale clusters and financial services. It hosts major cloud regions and colocation campuses, making it the top storage consumption hub. Enterprises in fintech, telecom, and digital media drive high throughput demand. London offers strong fiber connectivity, regulatory advantages, and skilled IT workforce. The region remains central to national data strategies and cloud adoption growth.

- For instance, Equinix’s LD6 facility in Slough offers approximately 129,000 sq ft of colocation space and supports power densities of 4–6 kVA per cabinet. The site has expanded to accommodate up to 2,770 cabinets, meeting growing enterprise and cloud storage demands.

South East England Emerging with 25% Share Through Expansion in Slough, Reading, and Maidenhead

South East England ranks second with a 25% share, boosted by facilities in Slough, Reading, and Maidenhead. Colocation and enterprise demand in these hubs continue to grow. These areas provide proximity to London with lower operating costs and power availability. New data center parks and greenfield developments attract cloud and IT firms. The UK Data Center Storage Market benefits from scalable capacity expansion in this corridor. Infrastructure investment and government incentives support ongoing growth.

Other Regions Including Manchester, Birmingham, and Leeds Account for Nearly 20% and Growing

Secondary regions such as Manchester, Birmingham, and Leeds together contribute nearly 20% to market share. These cities see rising demand from public cloud zones, enterprise data centers, and edge deployments. Local governments support tech clusters and digital ecosystems. Storage vendors explore these markets to diversify footprint and serve latency-sensitive clients. The UK Data Center Storage Market gains regional balance through tier-2 city infrastructure buildouts. Growth accelerates with 5G rollout and regional digital transformation projects.

- For instance, Telehouse’s London Docklands North Two facility supports a total power capacity of approximately 18.5 MW with dual redundant feeds and multiple generators at its Docklands campus. It forms part of the broader Telehouse London ecosystem, one of Europe’s most connected colocation hubs.

Competitive Insights:

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- Cisco Systems, Inc.

- NetApp

- IBM Corporation

- Veeam Software

- Seagate Technology

- Lenovo Group

- Fujitsu Limited

- Hitachi Vantara

The UK Data Center Storage Market is shaped by strong competition among global infrastructure providers and domestic integrators. Dell Technologies and HPE lead the enterprise segment with broad hardware and software portfolios. Cisco and NetApp offer integrated networking-storage solutions tailored for hybrid environments. IBM and Veeam focus on software-defined storage, backup, and resilience, appealing to regulated industries. Seagate and Lenovo compete in hardware-intensive workloads, while Fujitsu and Hitachi target high-density and AI-ready deployments. The market favors vendors with cloud compatibility, strong support services, and scalable architectures. It continues to shift toward flash-based systems, cyber-resilient storage, and workload-aware infrastructure. Vendors that align with digital transformation strategies and offer localized support remain competitive across public and private sector buyers.

Recent Developments:

- In March 2025, Hewlett Packard Enterprise partnered with NVIDIA to introduce a unified data layer for enterprise data centers. The collaboration strengthens AI-enabled storage, hybrid cloud integration, and accelerated data processing.

- In March 2025, Cohesity enhanced its Gaia platform by launching AI-powered search for on-premises backup data through collaboration with NVIDIA. The update improves data discovery, recovery speed, and analytics efficiency.