Executive summary:

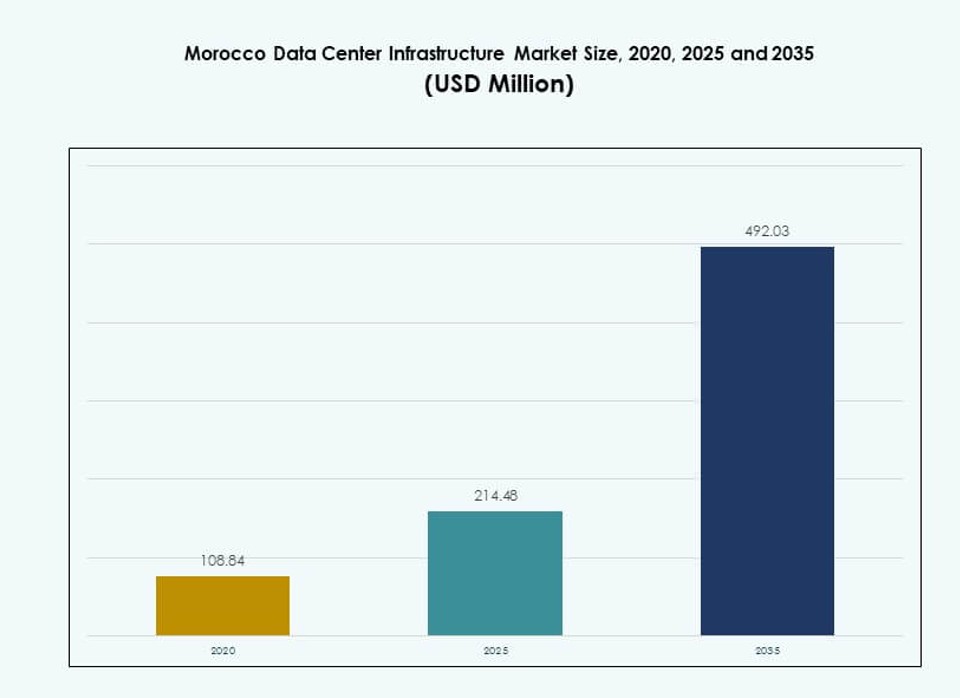

The Morocco Data Center Infrastructure Market size was valued at USD 108.84 million in 2020 to USD 214.48 million in 2025 and is anticipated to reach USD 492.03 million by 2035, at a CAGR of 8.53% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Morocco Data Center Infrastructure Market Size 2025 |

USD 214.48 Million |

| Morocco Data Center Infrastructure Market, CAGR |

8.53% |

| Morocco Data Center Infrastructure Market Size 2035 |

USD 492.03 Million |

Strong digitalization across finance, telecom, and government sectors drives demand for scalable data center infrastructure. Enterprises adopt cloud, AI, and edge computing to support smart platforms and real-time services. Innovation in modular builds, hybrid cooling, and energy storage enables faster deployment and long-term operational savings. Government initiatives focused on digital sovereignty and interconnectivity elevate the market’s strategic appeal. Businesses and investors view Morocco as a regional hub for secure, low-latency digital services.

The Greater Casablanca region leads due to dense fiber connectivity, carrier-neutral hubs, and proximity to business centers. Rabat and the Atlantic corridor follow, supported by public-sector modernization and smart infrastructure rollouts. Southern regions, including Agadir, are emerging due to land availability and growing industrial zones. Morocco’s geographic location between Europe and West Africa further strengthens its regional relevance.

Market Dynamics:

Market Drivers

Rising Cloud Adoption and Digital Services Transformation Across Key Sectors

The Morocco Data Center Infrastructure Market is gaining traction from accelerated digitalization across banking, telecom, and government sectors. Businesses seek scalable and secure infrastructure to support cloud migration and digital services expansion. Local and international firms are shifting to hybrid cloud models, which require high-density computing and resilient architecture. Increased mobile penetration drives demand for data-intensive applications, pushing enterprises to modernize IT infrastructure. Financial institutions are adopting real-time transaction systems requiring low-latency environments. Public sector entities are deploying digital public service platforms backed by secure hosting infrastructure. This shift enhances operational agility and regulatory compliance. The market attracts investment from hyperscale and regional players focused on future-ready builds.

- For instance, Maroc Telecom opened a data center in downtown Casablanca comprising two white spaces of 2,420 sq. ft. and 1,670 sq. ft., capable of housing up to 100 racks for server hosting targeted at SMEs.

Government-Backed Innovation Programs and National Digital Strategy Rollout

Government-led initiatives play a central role in shaping the Morocco Data Center Infrastructure Market. The digital Morocco strategy outlines infrastructure upgrades and data sovereignty efforts. Smart city developments, e-governance platforms, and 5G-readiness initiatives create demand for data handling and real-time analytics. Authorities are offering land access and policy incentives for private sector participation in high-tech infrastructure. Several state-linked entities are developing secure colocation zones for digital startups. The country’s strategic positioning makes it a tech entry point for Francophone West Africa. It supports seamless data traffic with Europe and MENA. These drivers help Morocco attract anchor tenants and foster investor confidence.

Energy Resilience and Infrastructure Modernization for Data Reliability

Uninterrupted power supply and cooling innovation are key enablers of infrastructure modernization in the Morocco Data Center Infrastructure Market. Operators deploy modular BESS and liquid cooling to maintain uptime in high-load environments. Urban data centers face energy grid constraints, prompting hybrid energy deployments integrating solar and backup generators. Industrial parks hosting data centers focus on long-term energy cost optimization. Equipment manufacturers and system integrators push prefabricated modular solutions to fast-track construction timelines. Thermal containment systems and airflow optimization reduce energy consumption. Sustainability goals drive green design and low-PUE targets. These shifts support long-term cost control and uptime assurance across facilities.

Strategic Connectivity and International Cable Integration Supporting Growth

Morocco’s data center expansion benefits from its growing subsea cable connectivity and geographic proximity to Europe. Casablanca and Rabat host key interconnection hubs linked to multiple international fiber routes. Data centers in these zones serve as gateways for digital services bridging Europe, North Africa, and West Africa. Enterprise clients favor Morocco for regional backups and latency-sensitive applications. Telecom players invest in core routing infrastructure to support regional IP traffic. New facilities offer direct cloud on-ramps and carrier-neutral environments for edge processing. Interconnected data zones drive value for multinational businesses entering the MENA region. This makes Morocco a rising digital bridge across continents.

- For instance, Morocco connects internationally via four subsea cables, enabling data centers like those from Maroc Telecom and Inwi to support regional IP traffic and colocation for Europe-Africa bridging.

Market Trends

Surge in Modular and Prefabricated Facility Deployments Across Urban and Semi-Urban Zones

The Morocco Data Center Infrastructure Market is witnessing a sharp rise in modular and prefabricated designs. Developers use factory-built modules for faster assembly and cost control. These systems help reduce deployment time by 30–40% and allow scalability based on tenant needs. Prefab units improve site efficiency and reduce local labor reliance. Government agencies and telcos deploy micro-data centers in remote areas using containerized solutions. Modular builds also support expansion in bandwidth-heavy zones with limited land availability. This trend supports flexibility and aligns with Morocco’s urban infrastructure push.

Increasing Use of Renewable Energy and Low-PUE Cooling Technologies

Sustainability trends are transforming infrastructure planning across the Morocco Data Center Infrastructure Market. Operators adopt solar energy integration and deploy rooftop photovoltaic panels at edge facilities. Thermal energy storage and indirect evaporative cooling replace older systems in large data halls. Developers target PUE levels below 1.4 using liquid cooling and optimized airflow. Battery systems now include lithium-ion and flow batteries to enhance backup reliability. Data centers reduce dependency on diesel by using hybrid grids and microgrid controllers. These steps lower emissions while meeting uptime goals and national climate policies.

Growth in Carrier-Neutral Facilities Supporting Multi-Tenant Demands

Carrier-neutral setups are becoming a preferred model in the Morocco Data Center Infrastructure Market. Enterprise clients seek choice in connectivity for redundancy and competitive pricing. Neutral data centers attract international ISPs and hyperscale cloud platforms. Facilities in Casablanca and Rabat offer multiple carriers with fiber routes across Europe and Africa. This trend supports low-latency services such as gaming, streaming, and cross-border collaboration. Colocation firms offer interconnect hubs for fintech and telecom clients. Expansion in carrier-neutral hubs improves market liquidity and client onboarding speed.

Edge Computing Infrastructure Expansion for Distributed Processing Needs

Edge data centers are emerging in Morocco to support IoT, smart city, and content delivery workloads. Operators build micro-facilities in industrial zones and logistics corridors. Enterprises deploy edge sites to reduce latency and avoid bandwidth congestion. Public infrastructure such as smart transportation and surveillance systems use distributed processing. Renewable-powered edge hubs offer data resilience during outages. Telecom players invest in edge-capable infrastructure to manage 5G workload surges. This trend enhances service availability and regional access to critical data applications.

Market Challenges

Grid Dependency and Limited Renewable Energy Access for Continuous Power Supply

Power supply remains a key challenge in the Morocco Data Center Infrastructure Market. Facilities in urban centers rely heavily on the national grid, which may face instability during peak demand. Backup diesel generators raise operational costs and emissions. Renewable integration remains limited by land access and permitting issues. Data centers require reliable power sources for Tier III and Tier IV certifications. Battery energy storage adoption is in early stages, with high CAPEX constraints. Many legacy facilities operate at high PUE due to poor energy design. These conditions reduce competitiveness against global benchmarks. Investors seek clear policies supporting energy-as-a-service and infrastructure subsidies.

Shortage of Skilled Workforce and Technical Expertise Slowing Innovation Cycles

The lack of data center professionals and certified engineers creates operational bottlenecks in the Morocco Data Center Infrastructure Market. Data center builds require project managers with specialized electrical and mechanical skills. Cooling, UPS, and network system integration depend on trained field teams. However, technical training in high-availability systems remains underdeveloped. Many projects rely on foreign contractors for design and commissioning, raising costs and project risk. Talent shortage limits innovation adoption and impacts O&M capabilities. Upskilling initiatives remain fragmented across regions. It reduces the pace of local capacity development and impacts long-term ROI.

Market Opportunities

Hyperscale Expansion and Enterprise Workload Migration Creating Long-Term Growth Potential

Enterprise migration from on-premise to colocation and cloud-hosted platforms opens growth paths in the Morocco Data Center Infrastructure Market. Hyperscale players plan capacity addition for regional hosting and BCDR environments. Strategic land banks near Casablanca attract long-term infrastructure investment. These opportunities support next-generation compute and storage demand.

Data Localization Mandates and Interconnect Hub Development Offering Business Entry Points

Rising emphasis on data localization fuels investment in regional data zones. Regulatory support for sovereign data hosting attracts compliance-focused sectors. Interconnect hub expansion enables low-latency cross-border data flow. Telecom reforms improve network infrastructure viability for new entrants.

Market Segmentation

By Infrastructure Type

The Morocco Data Center Infrastructure Market is led by the electrical infrastructure segment due to growing demand for backup systems, PDUs, and UPS setups. IT & network infrastructure follows closely as enterprises invest in servers and cabling for digital service delivery. Mechanical and civil infrastructure gain traction from increased greenfield builds and modular facilities.

By Electrical Infrastructure

Uninterruptible power supply (UPS) and battery energy storage systems (BESS) dominate the electrical infrastructure segment. Tier III and Tier IV facilities demand advanced power control systems to ensure 99.99% uptime. Grid integration and switchgears are also seeing rising deployment in enterprise campuses and telecom zones.

By Mechanical Infrastructure

Cooling units such as CRAC/CRAH and air-cooled chillers lead the mechanical segment due to thermal efficiency goals. Data centers increasingly adopt hot/cold aisle containment and airflow optimization to improve energy usage. Pumping systems and closed-loop setups support large-scale deployments in high-density zones.

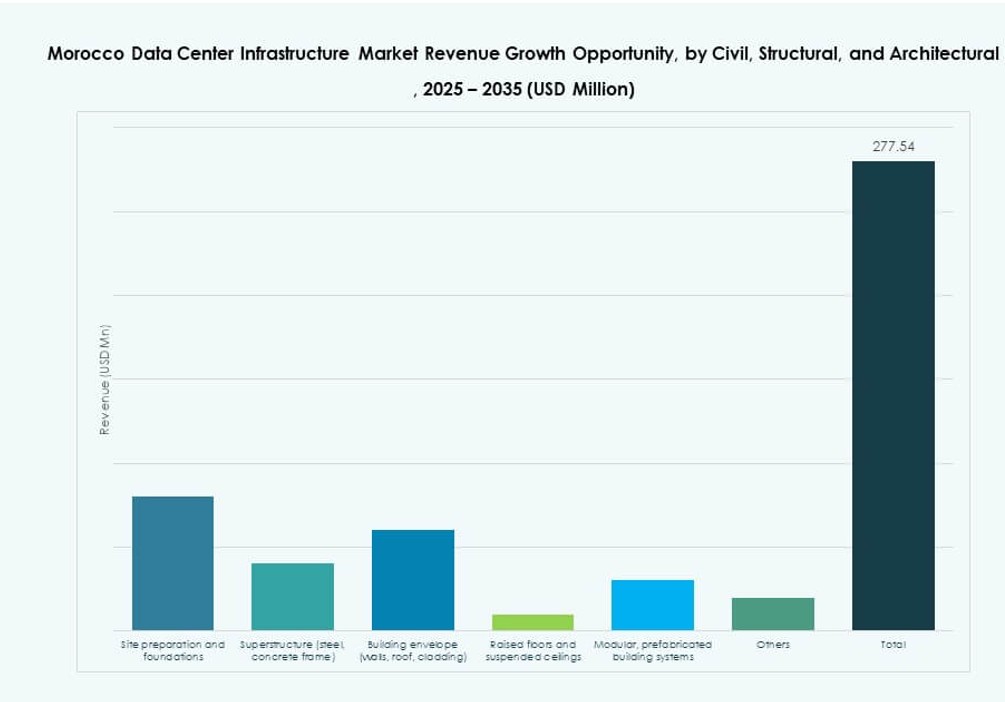

By Civil / Structural & Architectural

Site preparation and modular envelope construction are the largest segments under civil and architectural components. Builders use steel and concrete frames with raised floors for thermal isolation. Prefabricated buildings gain preference in projects with faster turnaround targets and constrained land.

By IT & Network Infrastructure

Server, storage, and cabling systems dominate this segment in the Morocco Data Center Infrastructure Market. Enterprises and cloud service providers upgrade their digital backbones with high-speed fiber and scalable racks. Enclosures with thermal zoning improve equipment longevity and performance.

By Data Center Type

Colocation data centers hold the largest share, offering flexible and scalable hosting for SMEs and enterprises. Hyperscale builds are emerging, supported by demand for cloud-native infrastructure. Enterprise and edge data centers also see interest from telecom and public sector projects.

By Delivery Model

Turnkey and design-build/EPC models dominate due to their full-scope project coverage and accountability. Retrofit and modular factory-built models gain traction for facility upgrades and remote setups. Construction management sees moderate adoption in enterprise-led custom builds.

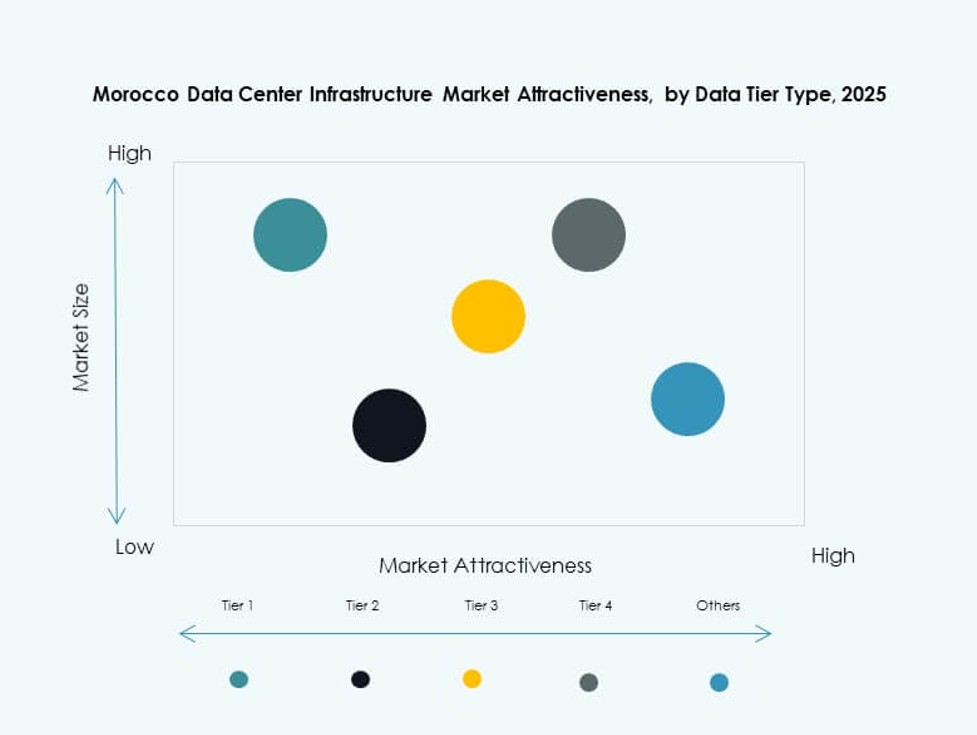

By Tier Type

Tier III dominates with high uptime and redundancy levels for core business applications. Tier IV sees limited but strategic use in financial and telecom sectors. Tier II finds relevance in small-scale or regional edge deployments where redundancy demand is lower.

Regional Insights

Greater Casablanca Region Holding Over 58% Market Share with High Interconnection Density

Casablanca remains the epicenter of the Morocco Data Center Infrastructure Market, hosting over 58% of installed capacity. Its proximity to business districts, subsea cable landing points, and logistics zones makes it a top choice for hyperscale and colocation projects. Carrier-neutral hubs in the region attract enterprise clients and financial institutions seeking secure and fast connectivity.

- For instance, Orange Morocco launched a new 1.5 MW data center in Casablanca’s Nouaceur area in November 2025, equipped with over 1,000 solar panels generating 700 kWp of renewable power.

Rabat and Atlantic Belt Covering 22% Share, Driven by Government Projects and ICT Uptake

Rabat and surrounding cities in the Atlantic corridor contribute 22% of market activity. Government ministries and public institutions adopt secure cloud and colocation setups. The region sees rising ICT training, innovation hubs, and smart infrastructure investments. Data centers in this zone support e-governance and public service digitization.

Southern and Inland Regions Representing 20%, Emerging with Industrial and Edge Deployments

Southern Morocco and inland cities account for 20% of infrastructure growth, mainly through industrial and edge deployments. Areas like Agadir and Fès benefit from renewable energy access and land availability. Micro-data centers serve logistics corridors and emerging business parks. These zones offer low-cost expansion potential with growing connectivity.

- For instance, in 2024, U.S.-based Iozera signed an MoU with the Moroccan government to build a 386 MW data center and AI hub in Tetouan. The project aims to integrate renewable energy and support Morocco’s digital infrastructure expansion.

Competitive Insights:

- N+ONE Datacenters

- Orange Morocco

- ABB

- Cisco Systems, Inc.

- Dell Inc.

- Equinix, Inc.

- Hewlett Packard Enterprise Development LP

- Huawei Technologies Co., Ltd.

- IBM

- Schneider Electric

The Morocco Data Center Infrastructure Market features a mix of domestic players and global technology providers competing across power, cooling, and IT infrastructure layers. N+ONE Datacenters leads local development with hyperscale ambitions and regional interconnectivity. Global firms like Equinix and Orange Morocco support carrier-neutral and telecom-hosted infrastructure models. ABB, Schneider Electric, and Vertiv offer modular power and cooling systems aligned with Tier III and Tier IV requirements. Cisco, Huawei, and HPE lead in IT and network stack integration, serving both enterprise and colocation customers. Market differentiation depends on energy efficiency, rapid deployment models, and SLA-driven reliability. It remains attractive for global players due to Morocco’s strategic position, increasing workload localization, and rising enterprise digital transformation demand. Strategic partnerships, green designs, and edge-focused innovation define future competition.

Recent Developments:

- In November 2025, Orange Morocco launched a new 1.5MW data center called “Orange Tech” in Casablanca to support cloud services, AI, and cybersecurity needs. This facility, equipped with solar panels and meeting Uptime standards, aligns with Morocco’s Maroc Digital 2030 strategy for digital sovereignty.

- In February 2025, AWS, in partnership with Orange Morocco, launched its first Wavelength Zone edge location in Casablanca, marking the cloud company’s inaugural Wavelength site in Africa. The deployment, hosted in Orange data centers and linked to AWS’s Paris region, enables low-latency applications for sectors like telecom, finance, healthcare, and gaming.